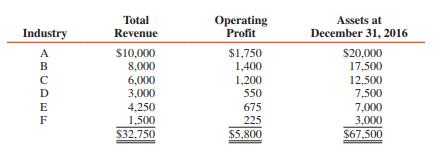

Question: 1. Coy Corporation and its divisions are

1. Coy Corporation and its divisions are engaged solely in manufacturing operations. The following data (consistent with prior years’ data) pertain to the industries in which operations were conducted for the year ended December 31, 2016 (in thousands):

In its segment information for 2016, how many reportable segments does Coy have?

a Three

b Four

c Five

d Six

2. Hen Corporation’s revenues for the year ended December 31, 2016, are as follows (in thousands):

Consolidated revenue per income statement.............. $1,200

Intersegment sales.............................................................. 180

Intersegment transfers......................................................... 60

Combined revenues of all segments............................. $1,440

Hen has a reportable segment if that segment’s revenues exceed:

a $6

b $24

c $120

d $144

3. The following information pertains to Ari Corporation and its divisions for the year ended December 31, 2016 (in thousands):

Sales to unaffiliated customers................................... $4,000

Intersegment sales of products similar to those............1,200

sold to unaffiliated customers

Interest earned on loans to other industry segments....... 80

The intersegment interest is not reported by the divisions on internal reports reviewed by the chief operating officer. Ari and all of its divisions are engaged solely in manufacturing operations. Ari has a reportable segment if that segment’s revenue exceeds:

a $528

b $520

c $408

d $400

4. The following information pertains to revenue earned by Wig Company’s operating segments for the year ended December 31, 2016:

In conformity with the revenue test, Wig reportable segments were:

a Only DG

b Beck and DG

c Ames, Beck, and DG

d Ames, Beck, Cyns, and DG

Use the following information in answering questions 5 and 6:

Gum Corporation, a publicly owned corporation, is subject to the requirements for segment reporting. In its income statement for the year ended December 31, 2016, Gum reported revenues of $50,000,000, operating expenses of $47,000,000, and net payroll costs of $15,000,000. Gum’s combined identifiable assets of all industry segments at December 31, 2016, were $40,000,000.

5. In its 2016 financial statements, Gum should disclose major customer data if sales to any single customer amount to at least:

a $300,000

b $1,500,000

c $4,000,000

d $5,000,000

6. In its 2016 financial statements, if Gum is organized on an industry basis, it should disclose foreign operations data on a specific country if revenues from that country’s operations are at least:

a $5,000,000

b $4,700,000

c $4,000,000

d $1,500,000

7. Selected data for a segment of a business enterprise are to be separately reported in accordance with GAAP when the revenues of the segment exceed 10 percent of the:

a Combined net income of all segments reporting profits

b Total revenues obtained in transactions with outsiders

c Total revenues of all the enterprise’s operating segments

d Total combined revenues for all segments reporting profits

8. In financial reporting of segment data, which of the following items is used in determining a segment’s operating income?

a Income tax expense

b Sales to other segments

c General corporate expense

d Gain or loss on discontinued operations

Transcribed Image Text:

Total Revenue Operating Profit Assets at Industry December 31, 2016 S10,000 8,000 $1,750 1,400 S20,000 17,500 6,000 3,000 1,200 12,500 550 7,500 4,250 675 7,000 F 1.500 $32.750 225 $5,800 3,000 $67,500 ABCDE

> 1. Partners All, Bak, and Coe share profits and losses 50:30:20, respectively. The balance sheet at April 30, 2016, follows: The assets and liabilities are recorded and presented at their respective fair values. Jon is to be admitted as a new partner w

> 1. Cob, Inc., a partner in TLC Partnership, assigns its partnership interest to Ben, who is not made a partner. After the assignment, Ben asserts the rights to: I. Participate in the management of TLC II. Cob’s share of TLC’s partnership profits Ben is c

> 1. Shi purchased an interest in the Ton and Olg partnership by paying Ton $40,000 for half of his capital and half of his 50 percent profit-sharing interest. At the time, Ton’s capital balance was $30,000 and Olg’s cap

> 1. Bil and Ken enter into a partnership agreement in which Bil is to have a 60 percent interest in capital and profits and Ken is to have a 40 percent interest in capital and profits. Bil contributes the following: There is a $30,000 mortgage on the bu

> The capital account balances and profit- and loss-sharing ratios of the Byd, Box, Dar, and Fus partnership on December 31, 2016, after closing entries are as follows: Byd (30%)............................ $30,000 Box (20%)..............................

> Kat and Edd formed the K & E partnership several years ago. Capital account balances on January 1, 2016, were as follows: Kat................................... $496,750 Edd.................................. $268,250 The partnership agreement provides

> A balance sheet at December 31, 2016, for the Bec, Dee, and Lyn partnership is summarized as follows: Dee is retiring from the partnership. The partners agree that partnership assets, excluding Dee’s loan, should be adjusted to their

> Capital balances and profit- and loss-sharing ratios for the Nix, Man, and Per partnership on December 31, 2016, just before the retirement of Nix, are as follows: Nix capital (30%)................................... $128,000 Man capital (30%)..........

> Capital balances and profit-sharing percentages for the partnership of Man, Eme, and Fot on January 1, 2016, are as follows: Man (36%)............................ $140,000 Eme (24%).............................. 100,000 Fot (40%)........................

> The capital balances and profits- and loss-sharing percentages for the Sip, Jog, and Run partnership at December 31, 2016, are as follows: Sip capital (30%)............................ $160,000 Jog capital (50%)........................... $180,000 Run c

> Are the treasury stock and conventional approaches equally applicable to all mutual holdings? Explain.

> Bow and Mon are partners in a retail business and divide profits 60 percent to Bow and 40 percent to Mon. Their capital balances at December 31, 2016, are as follows: Bow capital................................... $120,000 Mon capital...................

> The capital accounts of the Fax and Bel partnership on September 30, 2016, were: Fax capital (75% profit)..................... $140,000 Bel capital (25% profit).......................... 60,000 Total capital........................................ $200,

> Revenue information for Mahoney Corporation is as follows: Consolidated revenue (from the income statement).............. $400,000 Intersegment sales and transfers.................................................. 80,000 Combined revenues of all industr

> What is the difference between the integral theory and the discrete theory with respect to interim financial reporting?

> Describe the 10 percent revenue test for determining reportable segments.

> Describe the 10 percent operating-profit test for determining reportable segments.

> How are the segments that are not reportable segments handled in the required disclosures of FASB ASC Topic 280?

> What is a reportable segment according to FASB ASC Topic 280? What criteria are used in determining what operating segments are also reportable segments?

> What is an operating segment?

> Describe the minimum financial information to be disclosed in interim reports under the provisions of FASB ASC Topic 270.

> P owns 80 percent of S1, and S1 owns 70 percent of S2. Separate incomes of P, S1, and S2 are $20,000, $10,000, and $5,000, respectively, for 2016. During 2016, S1 sold land to P at a gain of $1,000. Compute S1’s income on an equity basis. Discuss why you

> Explain how a company estimates its annual effective tax rate for interim reporting purposes.

> Do the requirements of FASB ASC Topic 280 apply to financial statements for interim periods? If so, how?

> Must a major customer be identified by name?

> When is an enterprise required to include information in its financial statements about its foreign and domestic operations?

> What disclosures are required for the reportable segments and all remaining segments in the aggregate?

> Assume that an enterprise has 10 operating segments. Of these, five segments qualify as reportable segments by passing one of the 10 percent tests. However, their combined revenues from sales to unaffiliated customers total only 70 percent of the combine

> Describe the 10 percent asset test for determining reportable segments.

> When preparing interim reports, does an entity need to use the same method to value inventory that they use at the annual report date? What options are accepted?

> Does an entity need to disclose segment level information about depreciation and amortization (D&A) if the chief decision maker does not consider D&A in their assessment of the segments?

> DaP Corporation’s home country is the United States, but it also has operations in Canada, Mexico, Brazil, and South Africa and reports internally on a geographic basis. Information relevant to DaP’s operating-segment

> Pat Corporation owns 80 percent of the stock of Sam Corporation, and Sam owns 70 percent of the stock of Stan Corporation. Separate earnings of Pat, Sam, and Stan are $200,000, $160,000, and $100,000, respectively. Compute controlling and noncontrolling

> The following data for 2016 relate to Hay Industries, a worldwide conglomerate: REQUIRED: Answer the following questions related to Hay’s required segment disclosures and show computations: 1. Which segments are reportable segments un

> The following information has been accumulated for use in preparing segment disclosures for Wod Corporation (in thousands): REQUIRED: 1. Determine Wod’s reportable segments under the 10 percent revenue test. 2. Are additional reportab

> Tor Corporation is subject to income tax rates of 20 percent on its first $50,000 pretax income and 34 percent on amounts in excess of $50,000. Quarterly pretax accounting income for the calendar year is estimated by Tor to be as follows: Quarter.......

> The information that follows is for Cob Company at and for the year ended December 31, 2016. Cob’s operating segments are cost centers currently used for internal planning and control purposes. Amounts shown in the Total Consolidated co

> The consolidated income statement of Tut Company for 2016 is as follows (in thousands): TUT CONSOLIDATED INCOME STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2016 Sales.................................................................................... $360

> Selected information, which is reported to the chief operating officer, for the five segments of Rad Company for the year ended December 31, 2016, is as follows: The lumber segment has not been a reportable segment in prior years and is not expected to

> Mer Corporation has five major operating segments and operates in both domestic and foreign markets. Mer is organized internally on an industry basis. Information about its revenue from operating segments and foreign operations for 2016 is as follows (in

> Sur Corporation’s internal divisions are based on industry. The revenues, operating profits, and assets of the operating segments of Sur are presented in thousands of dollars as follows: REQUIRED: Determine the reportable segments of

> Vic Corporation operates entirely in the United States but in different industries. It segments the business based on industry. Total sales of the segments, including intersegment sales, are as follows: Concrete and stone products.......................

> 1. The disclosure requirements for an operating segment do not include: a Unusual items b Income tax expense or benefit c Interest revenue d Cost of goods or services sold 2. A reconciliation between the numbers disclosed in operating segments and conso

> Par Corporation owns a 30 percent interest in Sox Corporation, which Par properly accounts for using the equity method. Sox is in need of capital and decides to issue an additional 10,000 shares of common stock to the public. After issuance, Par’s owners

> Tap Manufacturing Company records sales of $1,000,000 and cost of sales of $550,000 during the first quarter of 2016. Tap uses the LIFO inventory method, and its inventories are computed as follows: Before year-end, Tap expects to replace the 4,000 uni

> 1. An inventory loss from a market price decline occurred in the first quarter, and the decline was not expected to reverse during the fiscal year. However, in the third quarter, the inventory’s market price recovery exceeded the market decline that occu

> The estimated and actual pretax incomes of Ent Corporation by quarter for 2016 were as follows: Ent calculated its estimated annual effective income tax rate to be 27.8333 percent, based on estimated pretax income and existing income tax rates. REQUIR

> 1. Interim reporting under FASB ASC Topic 270 guidelines refers to financial reporting: a On a monthly basis b On a quarterly basis c On a regular basis d For periods less than a year 2. A liquidation of LIFO inventories for interim reporting purposes m

> A summary of the segment operations of the Nog Corporation for the year ended December 31, 2016, follows: 1. For which of the following geographic areas will separate disclosures be required if only the 10 percent revenue test is considered? a United S

> The sales in thousands of dollars of the segments of Wow Corporation (Wow is organized on a geographic basis) for 2016 are as follows: The $178,000 sales to unaffiliated customers is the amount of revenue reported in Wow’s consolidate

> The gain or loss on remeasurement is included in net income each year if the temporal method is used. Explain why this makes sense economically.

> How does ASC Topic 830 define a highly inflationary economy? If the economy is deemed to be highly inflationary, which method for converting the financial statements to the reporting currency is used? How does the use of this method improve the economic

> Define the functional currency concept and briefly describe how a foreign entity’s functional currency is determined. Why is this definition critical from a financial reporting perspective?

> Pop Corporation owns 80 percent of Son Corporation, and properly included Son as a subsidiary in preparing consolidated financial statements for the year ended December 31, 2016. Pop issued the financial statements on March 1, 2017. In May of 2017, Son h

> How does the choice of functional currency affect how the gain or loss on a hedge of a net investment in a foreign subsidiary is reported in the financial statements?

> Under the current rate method, all the expenses are translated using some form of current-period exchange rate. Under the temporal method, some expenses such as salaries and utilities are translated using current rates but others, such as cost of goods s

> In the current-rate-method example in the chapter, the parent’s other comprehensive income adjustment related to its investment in the subsidiary was larger than the other comprehensive income adjustment on the subsidiary’s translated financial statement

> If a company’s sales were very seasonal—for example, a holiday-tree grower—would it be appropriate to use the annual average exchange rate to translate and remeasure sales and other expenses? Why or why not?

> Under what circumstances would a foreign entity’s financial statements need to be both remeasured and translated? Would this process have an effect on both the income statement and other comprehensive income? Explain.

> If the current rate method is used, the gain or loss on translation is included under other comprehensive income. Explain why this makes sense economically.

> Describe what the temporal method is and under what circumstances it should be used.

> Describe what the current rate method is and under what circumstances it should be used.

> What procedure is used to allocate the investment purchase price at the date of acquisition of a foreign subsidiary?

> Should a firm readjust after the fiscal period end if before the release of their statements the exchange rate is materially different?

> A summary of the assets and equities of Pot Corporation and its 80 percent–owned subsidiary, Sea Corporation, at December 31, 2016, is given as follows (in thousands): On January 2, 2017, Sea acquired a 70 percent interest in Toy Corp

> Pam Corporation owns 60 percent of Sun Corporation and 80 percent of Tim Corporation. Tim owns 20 percent of Sun. Separate income and loss data (not including investment income) for the three affiliates for 2016 are as follows: Pam......................

> What is required to disclose concerning the changes in a firm’s cumulative translation adjustment?

> Pet acquired 80 percent of the common stock of Sul for $4,000,000 on January 2, 2016, when the stockholders’ equity of Sul consisted of 5,000,000 euros capital stock and 2,000,000 euros retained earnings. The spot rate for euros on this date was $0.50. A

> Pyl acquired all the outstanding capital stock of Soo of London on January 1, 2016, for $800,000, when the exchange rate for British pounds was $1.50 and Soo’s stockholders’ equity consisted of £400,000 ca

> Pla purchased a 40 percent interest in Sor, a foreign company, on January 1, 2016, for $342,000, when Sor’s stockholders’ equity consisted of 3,000,000 LCU capital stock and 1,000,000 LCU retained earnings. Sorâ&

> Pak purchased a 40 percent interest in Sco of Germany for $1,080,000 on January 1, 2016. The excess cost over book value is due to a patent with a 10-year amortization period. A summary of Sco’s net assets at December 31, 2015, and at D

> San is a 90 percent–owned foreign subsidiary of Par, acquired by Par on January 1, 2016, at book value equal to fair value, when the exchange rate for LCUs of San’s home country was $0.24. San’s funct

> PWA Corporation paid $1,710,000 for 100 percent of the stock of SAA Corporation on January 1, 2016, when the stockholders’ equity of SAA consisted of 5,000,000 LCU capital stock and 3,000,000 LCU-retained earnings. SAA’

> Pel, a U.S. firm, paid $308,000 for all the common stock of Sar of Israel on January 1, 2016, when the exchange rate for sheqels was $0.35. Sar’s equity on this date consisted of 500,000 sheqels common stock and 300,000 sheqels retained

> Phi, a U.S. firm, acquired 100 percent of Stu’s outstanding stock at book value on January 1, 2016, for $112,000. Stu is a New Zealand–based company, and its functional currency is the U.S. dollar. The exchange rate for New Zealand dollars (NZ$) was $0.7

> Par of Chicago acquired all the outstanding capital stock of Sar of London on January 1, 2016, for $1,120,000. The exchange rate for British pounds was $1.40 and Sar’s stockholders’ equity was £800,000, consisting of £500,000 capital stock and £300,000 r

> The affiliation structure for Pad Corporation and its subsidiaries is diagrammed as follows: The incomes and dividends for the affiliates for 2016 are (in thousands): ADDITIONAL INFORMATION: 1. Axe sold land to Sal during 2016 at a $20,000 gain. The

> On January 1, 2016, Pan acquired all the stock of Sim of Belgium for $1,200,000, when Sim had 20,000,000 euros (Eu) capital stock and 15,000,000 euros (Eu) retained earnings. Sim’s net assets were fairly valued on this date and any cost/ book value diffe

> Stadt Corporation of the Netherlands is a 100 percent–owned subsidiary of Port Corporation, a U.S. firm, and its functional currency is the U.S. dollar. Stadt’s books of record are maintained in euros and its inventory is carried at cost. The current exc

> On January 1, 2016, Pai, a U.S. firm, purchases all the outstanding capital stock of Sta, a British firm, for $880,000, when the exchange rate for British pounds is $1.55. The book values of Sta’s assets and liabilities are equal to fai

> 1. When consolidated financial statements for a U.S. parent and its foreign subsidiary are prepared, the account balances expressed in foreign currency must be converted into the currency of the reporting entity. One objective of the translation process

> 1. A German subsidiary of a U.S. firm has the British pound as its functional currency. Under the provisions of ASC Topic 830, the U.S. dollar from the subsidiary’s viewpoint would be: a Its local currency b Its recording currency c A foreign currency d

> 1. Fay had a realized foreign exchange loss of $15,000 for the year ended December 31, 2016, and must determine whether the following items will require year-end adjustment: Fay had an $8,000 equity adjustment resulting from the translation of the accou

> Pac of the United States purchased all the outstanding stock of Swi of Switzerland for $1,350,000 cash on January 1, 2016. The book values of Swi’s assets and liabilities were equal to fair values on this date except for land, which was

> Pal acquired all the stock of Sta of Britain on January 1, 2016, for $163,800, when Sta had capital stock of £60,000 and retained earnings of £30,000. Sta’s assets and liabilities were fairly valued, except for equipment with a three-year life that was u

> Interest rate swaps were used in the chapter to highlight the differences between fair-value and cash-flow hedge accounting. Explain what type of risk is being hedged when a pay-fixed, receive variable swap is used to hedge an existing variable-rate loan

> A hedged firm purchase or sale commitment typically qualifies for fair-value hedge accounting if the hedge is documented to be effective. Compare the accounting for both the derivative and the firm purchase or sale commitment under each of these circumst

> Pop Corporation purchased an 80 percent interest in Son Corporation for $170,000 on January 1, 2016, when Son’s stockholders’ equity was $200,000. The excess of fair value over book value is due to goodwill. At Decembe

> Hedge effectiveness must be documented before a particular hedge qualifies for hedge accounting. Describe the most common approaches used to determine hedge effectiveness and when they are appropriate. In each of the approaches, when would a particular h

> Explain the differences between options, forward contracts, and futures contracts and the potential benefits and potential costs of each type of contract.

> Explain the objective of hedge accounting and how this objective should improve the transparency of financial statements.

> Briefly describe how derivatives are accounted for according to the International Accounting Standards Board. Is the accounting similar to U.S. GAAP? How is it different?

> Briefly describe how derivatives are accounted for according to the International Accounting Standards Board. Is the accounting similar to U.S. GAAP? How is it different?

> ASC 815 allows companies to account for certain hedges of existing foreign currency–denominated receivables and payables as cash-flow hedges. Also in ASC 815, hedges of existing assets and liabilities must be accounted for as fair-value hedges. Explain t

> Explain the circumstances under which fair-value hedge accounting should be used and when cash-flow hedge accounting should be used.

> Interest rate swaps were used in the chapter to highlight the differences between fair-value and cash-flow hedge accounting. Explain what type of risk is being hedged when a receive-fixed, pay-variable swap is used to hedge an existing fixed-rate loan.

> What criteria are required for a hedged item to qualify for special accounting as a fair-value hedge?

> What criteria are required for a hedged item to qualify for special accounting as a cash-flow hedge?

> Par Corporation acquired an 80 percent interest in Sip Corporation for $180,000 cash on January 1, 2016, when Sip had capital stock of $50,000 and retained earnings of $150,000. The excess of fair value over book value acquired is due to a patent, which

> On January 1, 2016, Cam borrows $400,000 from Ven. The five-year term note is a variable-rate one in which the 2016 interest rate is determined to be 8 percent, the LIBOR rate at January 1, 2016, +2%. Subsequent years’ interest rates are determined in a