Question: 1. On January 1, 2016, Pam Company

1. On January 1, 2016, Pam Company sold equipment to its wholly owned subsidiary, Sun Company, for $1,800. The equipment cost Pam $2,000. Accumulated depreciation at the time of sale was $500. Pam was depreciating the equipment on the straight-line method over 20 years with no salvage value, a procedure that Sun continued. On the consolidated balance sheet at December 31, 2016, the cost and accumulated depreciation, respectively, should be:

a $1,500 and $600

b $1,800 and $100

c $1,800 and $500

d $2,000 and $600

2. In the preparation of consolidated financial statements, intercompany items for which eliminations will not be made are:

a Purchases and sales where the parent employs the equity method

b Receivables and payables where the parent employs the cost method

c Dividends received and paid where the parent employs the equity method

d Dividends receivable and payable where the parent employs the equity method

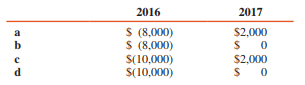

3. Pam Corporation owns 100 percent of Sun Corporation’s common stock. On January 2, 2016, Pam sold to Sun for $40,000 machinery with a carrying amount of $30,000. Sun is depreciating the acquired machinery over a five-year life by the straight-line method. The net adjustments to compute 2016 and 2017 consolidated income before income tax would be an increase (decrease) of:

4. Pam Company owns 100 percent of Sun Company. On January 1, 2016, Pam sold Sun delivery equipment at a gain. Pam had owned the equipment for two years and used a five-year straight-line depreciation rate with no residual value. Sun is using a three-year straight-line depreciation rate with no residual value for the equipment. In the consolidated income statement, Sun’s recorded depreciation expense on the equipment for 2016 will be decreased by:

a 20% of the gain on sale

b 33.33% of the gain on sale

c 50% of the gain on sale

d 100% of the gain on sale

Transcribed Image Text:

2016 2017 $ (8,000) $ (8,000) S(10,000) S(10,000) a $2,000 b $2,000 d

> Company X is expected to pay an end-of-year dividend of $5 a share. After the dividend its stock is expected to sell at $110. If the market capitalization rate is 8%, what is the current stock price?

> Portfolio managers are frequently paid a proportion of the funds under management. Suppose you manage a $100 million equity portfolio offering a dividend yield (DIV1/P0) of 5%. Dividends and portfolio value are expected to grow at a constant rate. Your a

> The constant-growth DCF formula: P0 = DIV1 /r − g is sometimes written as: P0 = ROE (1 − b) BVPS / r − b ROE where BVPS is book equity value per share, b is the plowback ratio, and ROE is the ratio of earnings per share to BVPS. Use this equation

> Phoenix Corp. faltered in the recent recession but is recovering. Free cash flow has grown rapidly. Forecasts made in 2016 are as follows. Phoenix’s recovery will be complete by 2021, and there will be no further growth in free cash&Aci

> Mexican Motors’ market cap is 200 billion pesos. Next year’s free cash flow is 8.5 billion pesos. Security analysts are forecasting that free cash flow will grow by 7.5% per year for the next five years. a. Assume that the 7.5% growth rate is expected to

> Why might one expect managers to act in shareholders’ interests? Give some reasons.

> Look back to the numerical example graphed in Figure 1A.1. Suppose the interest rate is 20%. What would the ant (A) and grasshopper (G) do if they both start with $100,000? Would they invest in their friend’s business? Would they borrow or lend? How muc

> Comparative consolidated financial statements for Pop Corporation and its subsidiary, Son Corporation, at and for the years ended December 31, 2017 and 2016 follow (in thousands). Pop Corporation and Subsidiary Comparative Consolidated Financial Stateme

> Pam Corporation paid $10,000,000 for Sun Corporation’s voting common stock on January 2, 2016, and Sun was dissolved. The purchase price consisted of 200,000 shares of Pam’s common stock with a market value of $8,000,0

> Pop Corporation paid $1,800,000 for 90,000 shares of Son Company’s 100,000 outstanding shares on January 1, 2016, when Son’s equity consisted of $1,000,000 of $10 par common stock and $500,000 retained earnings. The ex

> OP company issued 120,000 shares of $10 par common stock with a fair value of $2,550,000 for all the voting common stock of Son Company. In addition, Pop incurred the following additional costs: Legal fees to arrange the business combination ...........

> On January 1, 2009, Pam Corporation acquired 60 percent of the voting common shares of Sun Corporation at an excess of fair value over book value of $1,000,000. This excess was attributed to plant assets with a remaining useful life of five years. For th

> Pam Corporation acquired a 70 percent interest in Sun Corporation’s outstanding voting common stock on January 1, 2016, for $490,000 cash. The stockholders’ equity of Sun on this date consisted of $500,000 capital stoc

> On January 1, Pop Corporation pays $400,000 cash and also issues 36,000 shares of $10 par common stock with a market value of $660,000 for all the outstanding common shares of Son Corporation. In addition, Pop pays $60,000 for registering and issuing the

> Pam Company issued 480,000 shares of $10 par common stock with a fair value of $10,200,000 for all the voting common stock of Sun Company. In addition, Pam incurred the following costs: Legal fees to arrange the business combination ....................

> The stockholders’ equities of Pop Corporation and Son Corporation at January 1 were as follows (in thousands): On January 2, Pop issued 300,000 of its shares with a market value of $20 per share for all of Son’s shar

> 1. Pop Corporation paid $100,000 cash for the net assets of Son Company, which consisted of the following: Assume Son Company is dissolved. The plant and equipment acquired in this business combination should be recorded at: a $220,000 b $200,000 c $18

> The balance sheets of Pop Corporation and Son Corporation at December 31, 2015, are summarized with fair-value information as follows (in thousands): On January 1, 2016, Pop Corporation acquired all of Son’s outstanding stock for $300

> 1. A business combination in which a new corporation is formed to take over the assets and operations of two or more separate business entities, with the previously separate entities being dissolved, is a/an: a Consolidation b Merger c Pooling of interes

> Can gains or losses to a parent/investor result from a subsidiary’s/investee’s treasury stock transactions? Explain.

> Assume that a subsidiary has 10,000 shares of stock outstanding, of which 8,000 shares are owned by the parent. If the parent purchases an additional 2,000 shares of stock directly from the subsidiary at book value, how should the parent record its addit

> Assume that a subsidiary has 10,000 shares of stock outstanding, of which 8,000 shares are owned by the parent. What equity method adjustment will be necessary on the parent books if the subsidiary sells 2,000 additional shares of its own stock to outsid

> Pam Corporation’s Investment in Sun Company account had a balance of $475,000 at December 31, 2016. This balance consisted of goodwill of $35,000 and 80 percent of Sun’s $550,000 stockholders’ equity. On January 2, 2017, Sun increased its outstanding sha

> Pop Corporation purchased an 80 percent interest in Son Corporation for $1,200,000 on January 1, 2017, at which time Son’s stockholders’ equity consisted of $1,000,000 common stock and $400,000 retained earnings. The e

> When a parent sells a part of its interest in a subsidiary during an accounting period, is the income applicable to the interest sold up to the time of sale included in consolidated net income and parent income under the equity method? Explain.

> How is the gain or loss determined for the sale of part of an investment interest that is accounted for as a one-line consolidation? Is the amount of gain or loss affected by the accounting method used by the investor?

> Separate company financial statements for Pop Corporation and its subsidiary, Son Company, at and for the year ended December 31, 2017, are summarized as follows (in thousands): ADDITIONAL INFORMATION: 1. Pop Corporation acquired 13,500 shares of Son C

> Isn’t preacquisition income really noncontrolling interest share?

> On January 2, 2016, Pam Corporation issues its own $10 par common stock for all the outstanding stock of Sun Corporation in an acquisition. Sun is dissolved. In addition, Pam pays $40,000 for registering and issuing securities and $60,000 for other costs

> Assume that an 80 percent investor of Sub Company acquires an additional 10 percent interest in Sub halfway through the current fiscal period. Explain the effect of the 10 percent acquisition by the parent on noncontrolling interest share for the period

> How are preacquisition earnings accounted for by a parent under the equity method? How are they accounted for in the consolidated income statement?

> Explain the terms preacquisition earnings and preacquisition dividends.

> Pam Corporation acquired all the outstanding stock of Sun Corporation on April 1, 2016, for $15,000,000, when Sun’s stockholders’ equity consisted of $5,000,000 capital stock and $2,000,000 retained earnings. The price

> Financial statements for Pop and Son Corporations for 2016 are as follows (in thousands): ADDITIONAL INFORMATION: 1. Pop acquired an 80 percent interest in Son on January 2, 2014, for $580,000, when Son’s stockholdersâ€

> Pam Corporation acquired a 90 percent interest in Sun Corporation on January 1, 2016, for $2,700,000, at which time Sun’s capital stock and retained earnings were $1,500,000 and $900,000, respectively. The fair value cost/book value dif

> Income statement information for 2016 for Pam Corporation and its 60 percent–owned subsidiary, Sun Corporation, is as follows: Intercompany sales for 2016 are upstream (from Sun to Pam) and total $100,000. Pam’s Dece

> Pop Corporation acquired a 90 percent interest in Son Corporation’s outstanding voting common stock on January 1, 2016, for $630,000 cash. The stockholders’ equity of Son on this date consisted of $500,000 capital stoc

> Pam Corporation acquired a 90 percent interest in Sun Corporation on January 1, 2016, for $540,000, at which time Sun’s capital stock and retained earnings were $300,000 and $180,000, respectively. The entire fair value/book value diffe

> Son Corporation, a 90 percent–owned subsidiary of Pop Corporation, was acquired on January 1, 2016, at a price of $90,000 in excess of underlying book value. The excess was due to goodwill. Separate financial statements for Pop and Son

> On January 2, 2016, Pop Corporation enters into a business combination with Son Corporation in which Son is dissolved. Pop pays $1,650,000 for Son, the consideration consisting of 66,000 shares of Pop $10 par common stock with a market value of $25 per s

> Income data from the records of Pam Corporation and Sun Corporation, Pam’s 80 percent–owned subsidiary, for 2016 through 2019 follow (in thousands): Pam acquired its interest in Sun on January 1, 2016, at a price of

> Pop Industries manufactures heavy equipment used in construction and excavation. On January 3, 2016, Pop sold a piece of equipment from its inventory that cost $360,000 to its 60 percent–owned subsidiary, Son Corporation, at Pop’s standard price of twice

> Do common stock dividends and stock splits by a subsidiary affect the amounts that appear in the consolidated financial statements? Explain, indicating the items, if any, that would be affected.

> Pam Corporation has an 80 percent interest in Sun Corporation, its only subsidiary. The 80 percent interest was acquired on July 1, 2016, for $800, at which time Sun’s equity consisted of $600 capital stock and $200 retained earnings. T

> Pop Corporation owns 40 percent of the outstanding voting stock of Son Corporation, acquired for $200,000 on July 1, 2016, when Son’s common stockholders’ equity was $400,000. The excess of investment fair value over book value acquired was due to valuab

> Information needed to prepare the Cash Flow from Operating Activities section of Pam Corporation’s consolidated statement of cash flows is included in the following list: Amortization of patents........................................................ $

> A summary of the separate income of Pam Corporation and the net income of its 75 percent–owned subsidiary, Sun Corporation, for 2016 is as follows: Sun Corporation sold machinery with a book value of $10,000 to Pam Corporation for $16

> The separate incomes (which do not include investment income) of Pop Corporation and Son Corporation, its 80 percent– owned subsidiary, for 2016 were determined as follows (in thousands): During 2016, Pop sold merchandise

> 1. Son Corporation is an 80 percent–owned subsidiary of Pop Corporation. In 2016, Son sold land that cost $15,000 to Pop for $25,000. Pop held the land for eight years before reselling it in 2024 to Roy Company, an unrelated entity, for $55,000. The 2024

> Comparative balance sheets for Pop and Son Corporations at December 31, 2015, are as follows (in thousands): On January 2, 2016, Pop issues 240,000 shares of its stock with a market value of $40 per share for all the outstanding shares of Son Corporati

> Sun is a 90 percent–owned subsidiary of Pam Corporation, acquired at book value several years ago. Comparative separate-company income statements for the affiliates for 2016 are as follows: On January 5, 2016, Pam sold a building with

> Son Company is a 90 percent–owned subsidiary of Pop Corporation, acquired several years ago at book value equal to fair value. For 2016 and 2017, Pop and Son report the following: The only intercompany transaction between Pop and Son

> Sun Corporation is a 90 percent–owned subsidiary of Pam Corporation, acquired in 2016. During 2019 Pam sells land to Sun for $100,000 for which it paid $50,000. Sun still owns this land at December 31, 2019. REQUIRED: 1. How and in what amount will the

> Pop Company sells land with a book value of $5,000 to Son Company for $6,000 in 2016. Son is a wholly owned subsidiary of Pop. Son Company holds the land during 2017. Son Company sells the land for $8,000 to an outside entity in 2018. 1. In 2016 the unr

> How do the treasury stock transactions of a subsidiary affect the parent’s accounting for its investment under the equity method?

> Describe the computation of noncontrolling interest share in a year in which there is unrealized inventory profit from upstream sales in both the beginning and ending inventories of the parent.

> Unrealized profit in the ending inventory is eliminated in consolidation workpapers by increasing cost of sales and decreasing the inventory account. How is unrealized profit in the beginning inventory reflected in the consolidation workpapers?

> How is the combined cost of goods sold affected by unrealized profit in (a) the beginning inventory of the subsidiary and (b) the ending inventory of the subsidiary?

> Pam Corporation owns an 80 percent interest in the common stock of Sun Corporation, acquired several years ago at book value. Pam regularly sells merchandise to Sun. Information relevant to the intercompany sales and profits of Pam and Sun for 2016, 2017

> The stockholder’s equity accounts of Pop Corporation and Son Corporation at December 31, 2015, were as follows (in thousands): On January 1, 2016, Pop Corporation acquired an 80 percent interest in Son Corporation for $580,000. The ex

> On January 2, 2000, Pop and Son Corporation merged their operations through a business combination accounted for as a pooling of interests. The $300,000 direct costs of combination were paid in cash by the surviving entity on January 2, 2000. At December

> How does a parent adjust its investment income for unrealized profit on sales it makes to its subsidiaries, (a) in the year of the sale and (b) in the year in which the subsidiaries sell the related merchandise to outsiders?

> Under what circumstances is noncontrolling interest share affected by intercompany sales activity?

> Would failure to eliminate unrealized profit in inventories at December 31, 2016, have any effect on consolidated net income in 2017? 2018?

> Explain the designations upstream sales and downstream sales. Of what significance are these designations in computing parent and consolidated net income?

> What effect does the elimination of intercompany accounts receivable and accounts payable have on consolidated working capital?

> What effect does the elimination of intercompany sales and cost of goods sold have on consolidated net income?

> Again, consider the facts presented in PR 8-1 above. Is it acceptable for Pop to continue to account for its investment in Son for the current year, using the equity method of accounting and delaying consolidation until the following year?

> Pop Corporation purchased a 75 percent interest in Son Corporation in the open market on January 1, 2017, for $690,000. A summary of Son’s stockholders’ equity on December 31, 2016 and 2017, is as follows (in thousands

> Is the amount of intercompany profit to be eliminated from consolidated financial statements affected by the existence of a noncontrolling interest? Explain.

> 1. Pam Corporation owns 70 percent of Sun Company’s common stock, acquired January 1, 2017. Patents from the investment are being amortized at a rate of $20,000 per year. Sun regularly sells merchandise to Pam at 150 percent of Sun&acir

> Pam and Sun Corporations entered into a business combination accounted for as a pooling of interests in which Sun was dissolved. Net assets and stockholders’ equities of the two companies immediately before the pooling follow (in thousa

> When does goodwill result from a business combination? How does goodwill affect reported net income after a business combination?

> What are the legal distinctions between a business combination, a merger, and a consolidation?

> Is dissolution of all but one of the separate legal entities necessary in order to have a business combination? Explain.

> What is the accounting concept of a business combination?

> Does current GAAP provide any exceptions to the fair-value measurement principle for business combinations?

> What are the required disclosures related to goodwill included in the consolidated balance sheet?

> Separate-company financial statements for Pop Corporation and its subsidiary, Son Company, at and for the year ended December 31, 2017, are summarized as follows (in thousands): ADDITIONAL INFORMATION: 1. Pop Corporation acquired 13,500 shares of Son C

> Pop Corporation acquired a 75 percent interest in Son Corporation on January 1, 2016, for $720,000 in cash. Financial statements of Pop and Son Corporations for 2016 are as follows (in thousands): REQUIRED: Prepare consolidation work papers for Pop Co

> What special procedures are required to consolidate the statements of a parent that reports on a calendar year basis and a subsidiary whose fiscal year ends on October 31?

> Pop Corporation issued its own common stock for all the outstanding shares of Son Corporation in a pooling of interests business combination on January 1, 2000. The balance sheets of the two companies at December 31, 1999, were as follows (in thousands):

> On January 1, 2000, Pam Corporation held 2,000 shares of Sun Corporation common stock acquired at $15 per share several years earlier. On this date, Pam issued 1.5 of its $10 par value shares for each of the other 98,000 outstanding shares of Sun in a po

> The effect of unrealized profits and losses on sales between affiliated companies is eliminated in preparing consolidated financial statements. When are profits and losses on such sales realized for consolidated statement purposes?

> Consolidation workpaper procedures are usually based on the assumption that any unrealized profit in the beginning inventory of one year is realized through sales in the following year. If the related merchandise is not sold in the succeeding period, wou

> Is the effect of unrealized profit on consolidated cost of goods sold influenced by (a) the existence of a noncontrolling interest and (b) the direction of intercompany sales?

> 1. Pam Corporation owns a 70 percent interest in Sun Corporation, acquired several years ago at book value. On December 31, 2016, Sun mailed a check for $80,000 to Pam in part payment of an $160,000 account with Pam. Pam had not received the check when t

> In eliminating unrealized profit on intercompany sales of inventory items, should gross profit or net profit be eliminated?

> Does noncontrolling interest represent a liability or an equity in the consolidated balance sheet?

> Should the consolidated financial statements include the subsidiary’s retained earnings at the acquisition date?

> Pam Corporation acquired its 90 percent interest in Sun Corporation at its book value of $3,600,000 on January 1, 2016, when Sun had capital stock of $3,000,000 and retained earnings of $1,000,000. The December 31, 2016 and 2017, inventories of Pam inclu

> Pop Corporation purchased a 90 percent interest in Son Corporation on December 31, 2016, for $5,400,000 cash, when Son had capital stock of $4,000,000 and retained earnings of $1,000,000. All Son’s assets and liabilities were recorded a

> Pop Corporation has owned a 30 percent interest in Son Corporation for ten years, and has properly recorded this investment using the equity method of accounting. On July 1 of the current year Pop purchased an additional 40 percent interest in Son. Is it

> 1. Consolidation workpaper entries normally: a Are posted to the general ledger accounts of one or more of the affiliates b Are posted to the general ledger accounts only when the financial statement approach is used c Are posted to the general ledger ac

> Pop Corporation acquired 100 percent of Son Corporation’s outstanding voting common stock on January 1, 2016, for $660,000 cash. Son’s stockholders’ equity on this date consisted of $300,0

> Pam Corporation purchased a 90 percent interest in Sun Corporation on December 31, 2015, for $2,700,000 cash, when Sun had capital stock of $2,000,000 and retained earnings of $500,000. All Sun’s assets and liabilities were recorded at

> Pop Corporation acquired a 75 percent interest in Son Corporation for $600,000 on January 1, 2016, when Son’s equity consisted of $300,000 capital stock and $100,000 retained earnings. The fair values of Son’s assets a

> Pam Corporation acquired 100 percent of Sun Corporation’s outstanding voting common stock on January 1, 2016, for $660,000 cash. Sun’s stockholders’ equity on this date consisted of $300,000 capital s

> Comparative income statements of Son Corporation for the calendar years 2016, 2017, and 2018 are as follows (in thousands): ADDITIONAL INFORMATION: 1. Son was a 75 percent–owned subsidiary of Pop Corporation throughout the 2016â

> Why is the equity method referred to as a “one-line consolidation”?