Question: Alubar, a U.S. multinational, receives royalties

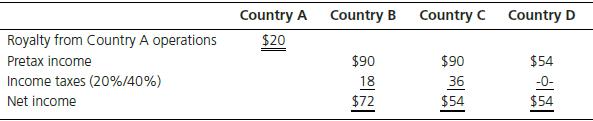

Alubar, a U.S. multinational, receives royalties from Country A, foreign-branch earnings from Country B, and dividends equal to 50 percent of net income from subsidiaries in Countries C and D. There is a 10 percent withholding tax on the royalty from Country A and a 10 percent withholding tax on the dividend from Country C. Income tax rates are 20 percent in Country B and 40 percent in Country C. Country D assesses indirect taxes of 40 percent instead of direct taxes on income. Selected data are as follows:

Required:

Calculate the foreign and U.S. taxes paid on each foreign-source income.

Transcribed Image Text:

Country A Country B Country C Country D Royalty from Country A operations $20 Pretax income $90 $90 $54 Income taxes (20%/40%) 18 36 -0- Net income $72 $54 $54

> Countries of the European Union are establishing oversight bodies to regulate the activities of statutory auditors. These national bodies are also coordinated at the EU level. Required: Find information on the European Group of Auditors’ Oversight Bodi

> The role of government in developing accounting and auditing standards differs in the five countries discussed in this chapter. Required: Compare the role of government in developing accounting and auditing standards in France, Germany, the Czech Repub

> To Exhibit 3-6. Required: Which country’s GAAP appears to be the most oriented toward equity investors? Which country’s GAAP appears to be the least oriented toward equity investors? Why do you say so? EXHIBIT 3

> Analyze the five national accounting practice systems summarized in this chapter. Required: a. For each of the five countries discussed in this chapter, select the most important financial accounting practice or principle at variance with international

> Reread Chapter 3 and its discussion questions. Required: a. As you go through this material, prepare a list of five expressions, terms, or short phrases that are unfamiliar or unusual in your home country. b. Write a concise definition or explanation o

> The International Federation of Accountants (IFAC) is a worldwide organization of professional accounting bodies. IFAC’s Web site (www.ifac.org) has links to a number of accounting bodies around the world. Required: Visit IFAC’s Web site. List the acco

> Why have international accounting issues grown in importance and complexity in recent years?

> Refer to your answer to Exercise 1. Required: Which country discussed in this chapter appears to have the most effective accounting and financial reporting supervision mechanism for companies whose securities are traded in public financial markets? Sho

> This chapter provides synopses of national accounting practice systems in five European countries. Required: For each country, list: a. the name of the national financial accounting standard-setting board or agency. b. the name of the agency, institute,

> Auditor oversight bodies have recently been established in several countries discussed in this chapter. Identify the auditor oversight bodies discussed in the chapter. What is the reason for this recent trend?

> Compare and contrast the main features of financial reporting in the five countries discussed in this chapter.

> Compare and contrast the mechanisms for regulating and enforcing financial reporting in the five countries discussed in this chapter.

> A feature of British accounting is the “true and fair override.” What is the meaning of this term? Why is the true and fair override found in the United Kingdom but almost nowhere else?

> The most novel feature of the Dutch accounting scene is the Enterprise Chapter of the Court of Justice of Amsterdam. What is the mission of the Enterprise Chamber? How is this mission carried out?

> How have accounting requirements and practices in the Czech Republic been influenced by European Union requirements?

> Consider the following statement: “The German Accounting Standards Committee is modeled on Anglo-American and international practice.” Do you agree? Why or why not?

> In France, financial accounting standards and practices originate primarily from three authoritative sources: (a) companies legislation (Plan Comptable Général and Code de Commerce), (b) professional opinions and recommendations (CNC, CRC, OEC, and CNC

> Given the international heritage of accounting, do you feel that efforts to harmonize global accounting standards are a good thing? Why or why not?

> Consider the following statement: “Experience shows that the needs of national and international markets, for international harmonization in particular, are better served by self-regulation and development than by government regulation.” Do you agree? Wh

> What is the difference between consolidated and individual company financial statements? Why do some EU countries prohibit IFRS in individual company financial statements while others permit or require IFRS at the individual company level?

> As an analyst for a securities firm, you are aware that accounting practices differ around the world. Yet you wonder whether these differences really have any material effect on companies’ financial statements. You also know that the SEC in the United St

> As an analyst for a securities firm, you are aware that accounting practices differ around the world. Yet you wonder whether these differences really have any material effect on companies’ financial statements. You also know that the SEC in the United St

> The ethical climate in the Czech Republic has improved since the early days, but we still have a long way to go,” said Josef Machinka, an economic adviser to the Ministry of Finance, while attending an investment seminar sponsored by the Prague Stock Exc

> Think ahead 10 years from now. Prepare a classification of accounting systems that you think will exist then. What factors motivate your classification?

> Consider the development factors in the following five countries: France, India, Japan, the United States, and the United Kingdom: Required: Based on the information provided in this chapter, prepare a profile of accounting in each of the countries.

> Many countries permit or require their domestic listed companies to use International Financial Reporting Standards (IFRS) in their consolidated financial statements for investor reporting. Required: Consider the following 10 countries: China, the Czec

> Refer to Exercise 6. Required: a. Go to Hofstede’s Web site (www.geerthofstede. com/hofstede_dimensions. php) and find the uncertainty avoidance scores for the same 10 countries. b. Characterize the uncertainty avoidance scores as high, medium, or low. c

> Gray proposed a framework linking culture and accounting. He predicts four accounting values (professionalism, uniformity, conservatism, and secrecy) based on Hofstede’s four cultural dimensions (individualism, uncertainty avoidance, po

> Describe in two short paragraphs how foreign direct investment activities differ from international trade and the implications of this difference for accounting.

> Refer to Exercise 4. In May 2004, the EU expanded to incorporate 10 Central and East European nations: Cyprus, the Czech Republic, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovakia, and Slovenia. Bulgaria and Romania joined in January 2007. R

> The European Union (EU)—formerly known as the European Community and, at its start, as the European Common Market—was founded in 1957 and had 15 members at the end of 2003: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxe

> Go to the World Federation of Exchanges Web site (www.world-exchanges.org) and obtain the latest annual report. The market statistics section on equity markets has information on the numbers of domestic and foreign companies listed on member stock exchan

> Consider the following countries: (1) Belgium, (2) China, (3) the Czech Republic, (4) Gambia, (5) India, (6) Mexico, (7) Senegal, and (8) Taiwan. Required: Where would they be classified based on legal system? Where would they be classified bas

> The chapter identifies seven economic, historical, and/or institutional variables that influence accounting development: sources of finance, legal system, taxation, political and economic ties, inflation, level of economic development, and education leve

> How do cultural values influence accounting? Are there parallel influences between the factors identified in Question 1 and the cultural factors identified here?

> The chapter identifies seven economic, sociohistorical, and institutional factors believed to influence accounting development. Explain how each one affects accounting practice.

> What are the prospects of a convergence or harmonization of national systems of accounting and financial reporting? What factors might be influential in promoting or inhibiting change?

> The authors contend that a classification based on fair presentation vs. legal compliance describes accounting in the world today better than one based on common law and code law legal systems. Do you agree? Why or why not?

> Why does the chapter contend that many accounting distinctions at the national level are becoming blurred? Do you agree? Why or why not?

> What contemporary factors are contributing to the internationalization of the subject of accounting?

> What are the major accounting classifications in the world? What are the distinguishing features of each model?

> What is the purpose of classifying systems of accounting? What is the difference between a judgmental and an empirical classification of accounting?

> Countries that have relatively conservative measurement practices also tend to be secretive in disclosure, while countries that have less conservative measurement practices tend to be transparent in disclosure. Why is this so?

> The partial income statement of the Lund Manufacturing Company, a Swedish-based concern producing pharmaceutical products, is presented below: During the year, short-term interest rates in Sweden averaged 7 percent, while net operating assets averaged SE

> Lumet Corporation, a manufacturer of cellular telephones, wishes to invoice a sales affiliate located in Fontainebleau for an order of €10,000 units. Wanting to minimize its exchange risk, it invoices all intracompany transactions in euros. Relevant fact

> Drawing on the background facts in Exercises 6 and 7, assume that the manufacturing cost per unit, based on operations at full capacity of 10,000 units, is $60, and that the uncontrolled selling price of the unit in Country Ais $120. Costs to transport t

> Using the facts stated in Exercise 6, what would be the tax effects of the transfer pricing action if corporate income tax rates were 30 percent in Country Aand 40 percent in Country B?

> The four approaches to accounting development discussed in the chapter were originally outlined in 1967. Do you think these patterns will persist in the future? Why or why not?

> Global Enterprises has a manufacturing affiliate in Country A that incurs costs of $600,000 for goods that it sells to its sales affiliate in Country B. The sales affiliate resells these goods to final consumers for $1,700,000. Both affiliates incur oper

> Sweden has a classical system of taxation. Calculate the total taxes that would be paid by a company headquartered in Stockholm that earns 1,500,000 Swedish krona (SEK) and distributes 50 percent of its earnings as a dividend to its shareholders. Assume

> Ajewelry manufacturer domiciled in Amsterdam purchases gold from a precious metals dealer in Belgium for € :2,400. The manufacturer fabricates the raw material into an item of jewelry and wholesales it to a Dutch retailer for 4,000. Required: Compute t

> Kowloon Trading Company, a wholly owned subsidiary incorporated in Hong Kong, imports macadamia nuts from its parent company in Honolulu for export to various duty-free shops in the Far East. During the current fiscal year, the company imported $2,000,00

> A Chinese manufacturing subsidiary produces items sold in Australia. The items cost the equivalent of $7.00 to produce and are sold to customers for $9.50. A Cayman Islands subsidiary buys the items from the Chinese subsidiary for $7.00 and sells them to

> What philosophies and types of taxes exist worldwide?

> What is tax neutrality? Are taxes neutral with regard to business decisions? Is this good or bad?

> What is an advance pricing agreement (APA)? What are the advantages and disadvantages of entering into an APA?

> Explain the arm’s-length price. Is the U.S. Internal Revenue Service alone in mandating such pricing of intracompany transfers? Would the concept of an arm’s-length price resolve the measurement issue in pricing intracompany transfers?

> Are national differences in accounting practice better explained by culture or by economic and legal factors? Why?

> Identify the major bases for pricing intercompany transfers. Comment briefly on their relative merits. Which measurement method is best from the viewpoint of the multinational executive?

> The pricing of intracompany transfers is complicated by many economic, environmental, and organizational considerations. Identify six major considerations described in the chapter and briefly explain how they affect transfer pricing policy.

> Multinational transfer pricing causes serious concern for various corporate stakeholders. Identify potential concerns from the viewpoint of a. minority owners of a foreign affiliate, b. foreign taxing authorities, c. home-country taxing authorities, d. f

> Compare and contrast the role of transfer pricing in national versus international operations.

> Carried to its logical extreme, tax planning implies a conscientious policy of tax minimization. This mode of thinking raises an ethical question for international tax executives. Deliberate tax evasion is commonplace in many parts of the world. In Italy

> Consider the statement “National differences in statutory tax rates are the most obvious and yet least significant determinants of a company’s effective tax burden.” Do you agree? Explain.

> Muscle Max–Asia, a wholly owned affiliate of a French parent company, functions as a regional headquarters for operating activities in the Pacific Rim. It enjoys great autonomy from its French parent in conducting its primary line of business, the manufa

> Do accountants share the blame for Third World poverty? A report by the U.K.-based Christian Aid says so.31 It attacks accounting firms for helping to perpetuate poverty in the developing world through their aggressive marketing of tax-avoidance schemes:

> In June, Mu Corporation, a U.S. manufacturer of specialty confectionery products, submits a bid to supply a prestigious retail merchandiser with boxed chocolates for the traditional Valentine’s Day. At the time the spot rate for francs was $0.89 = CHF1.

> On June 1, ACL International, a U.S. confectionery products manufacturer, purchases on account bulk chocolate from a Swiss supplier for 166,667 Swiss francs (CHF) when the spot rate is $0.90 = CHF 1. The Swiss franc payable is due on September 1. To mini

> The Volkswagen Group adopted International Accounting Standards (IAS, now International Financial Reporting, or IFRS) for its 2001 fiscal year. The following is taken from Volkswagen’s 2001 annual report. It discusses major differences

> On April 1, Anthes Corporation, a calendar-year U.S. electronics manufacturer, invests 30 million yen in a three-month yen-denominated CD with a fixed coupon of 8 percent. To hedge against the depreciation of the yen prior to maturity, Anthes designates

> Trojan Corporation USA borrowed 1,000,000 New Zealand dollars (NZ$) at the beginning of the calendar year when the exchange rate was $0.60 = NZ$1. Before repaying this one-year loan, Trojan learns that the NZ dollar has appreciated to $0.70 = NZ$1. It di

> Refer to Exercise 5. Assume that the shekel is forecast to devalue such that the new exchange relationship after the devaluation is (£ /$/ILS = 1/2/8). Required: Calculate the consolidated gain or loss that would result from this exchange rate movement

> Following is the consolidated balance sheet (000s omitted) of Worberg Bank, a U.S. financial institution with wholly owned corporate affiliates in London and Jerusalem. Cash and due from banks includes ILS100,000 and a £ 40,000 bank overdraf

> Exhibit 11-5 contains a hypothetical balance sheet of a foreign subsidiary of a U.S. MNC. Exhibit 11-6 shows how the foreign exchange loss is determined assuming the parent company employs the temporal method of currency translation. Required: Demonstr

> As one of your first assignments as a new hire on the corporate treasurer’s staff of Global Enterprises, Ltd., you are asked to prepare an exchange rate forecast for the Zonolian ecru (ZOE). Specifically, you are expected to forecast what the spot rate f

> Reexamine the Risk-Mapping Cube in Exhibit 11-3. Provide examples of how the various market risks—foreign exchange, interest rate, commodity price, and equity price—might affect the value driver: current assets. E

> Refer to Exhibit 11-1 which discloses the risk management paradigm for Infosys Technologies. Explain in your own words what each step of the cycle entails, including the feedback loop from the last to the first step. EXHIBIT 11-1 Risk Management Cyc

> Your company has just decided to purchase 50 percent of its inventory from China and purchases will be invoiced in Chinese yuan. What four processes do you need to consider in designing a foreign exchange risk protection system?

> What is market risk? Illustrate this risk with a foreign exchange example.

> Consider the following statements by David Cairns, former secretary-general of the International Accounting Standards Committee.26 When we look at the way that countries or companies account for particular transactions and events, it is increasingly dif

> The notion of an “opportunity cost” was perhaps first introduced to you in your first course in microeconomics. Explain how this notion can be applied in evaluating the effectiveness of FX risk hedging programs.

> All hedging relationships must be “highly effective” to qualify for special accounting treatment. What is meant by the term highly effective and why is its measurement important for financial managers?

> Identify three major types of hedges recognized by IAS 39 and FAS 133 and describe their accounting treatments.

> What is a financial futures contract? How does it differ from a forward exchange contract?

> Explain how a company might use a currency swap to hedge its foreign exchange risk on a foreign currency borrowing.

> Explain, in your own words, the difference between a multicurrency translation exposure report and a multicurrency transactions exposure report.

> List 10 ways to reduce a firm’s foreign exchange exposure for a foreign affiliate located in a devaluation-prone country. In each instance, identify the cost–benefit trade-offs that need to be measured.

> Compare and contrast the terms translation, transaction, and economic exposure. Does FAS No. 52 resolve the issue of accounting versus economic exposure?

> The scene is a conference room on the 10th floor of an office building on Wall Street, occupied by Anthes Enterprises, a small, rapidly growing manufacturer of electronic trading systems for equities, commodities, and currencies. The agenda for the 8:00

> You have just landed a summer internship (congratulations) with the management information services group of Pirelli, the Italian global tire manufacturer. Management is acutely aware of the importance of risk management and the market’

> If you had a nontrivial sum of money to invest and decided to invest it in a country index fund, in which country or countries identified in Exhibit 1-7 would you invest your money? What accounting issues would play a role in your decision? Ten Exch

> Parent Company establishes three wholly owned affiliates in countries X, Y, and Z. Its total investment in each of the respective affiliates at the beginning of the year, together with year-end returns in parent currency (PC), appear here: Parent Compa

> Exhibit 10-9 contains a performance report that breaks out various operating variances of a foreign affiliate, assuming the parent currency is the functional currency under FAS No. 52. Using the information in Exhibit 10-9, repeat the variance analysis,

> To encourage its foreign managers to incorporate expected exchange rate changes into their operating decisions, Vancouver Enterprises requires that all foreign currency budgets be set in Canadian dollars using exchange rates projected for the end of the

> In evaluating the performance of a foreign manager, a parent company should never penalize a manager for things the manager cannot control. Given the information provided in Exercise 6, prepare a performance report identifying the relevant elements for e

> Global Enterprises, Inc. uses a number of performance criteria to evaluate its overseas operations, including return on investment. Compagnie de Calais, its Belgian subsidiary, submits the performance report shown in Exhibit 10-13 for the current fisca

> Assume the following: • Inflation and Zambian kwacha (ZMK) devaluation is 30 percent per month, or 1.2 percent per workday. • Foreign exchange rates at selected intervals for the current month are: 1/1 ……………………………………………….100.0 1/10 ……………………………………………..10

> Assume that management is considering whether to make the foreign direct investment described in Exercise 3. Investment will require $6,000,000 in equity capital. Cash flows to the parent are expected to increase by 5 percent over the previous year for e

> Review the operating data incorporated in Exhibit 10-3 for the Russian subsidiary of the U.S. parent company. Required: Using Exhibit 10-3 as a guide, prepare a cash flow report from a parent currency perspective identifying the components of the expe

> Slovenia Corporation manufactures a product that is marketed in North America, Europe, and Asia. Its total manufacturing cost to produce 100 units of product X is 2,250, detailed as follows: Raw materials ………………………………………………………………………€500 Direct labor ………