Question: Bouwens Corporation manufactures a solvent used in

Bouwens Corporation manufactures a solvent used in airplane maintenance shops. Bouwens sells the solvent to both U.S. military services and commercial airlines. The solvent is produced in a single plant in one of two buildings. Although the solvent sold to the military is chemically identical to that sold to the airlines, the company produces solvent for the two customer types in different buildings at the plant. The solvent sold to the military is manufactured in building 155 (B-155) and is labeled M-Solv. The solvent sold to the commercial airlines is manufactured in building 159 (B-159) and is labeled C-Solv.

B-155 is much newer and is considered a model work environment with climate control and other amenities. Workers at Bouwens, who all have roughly equal skills, bid on their job locations (the buildings they will work in) and are assigned based on bids and seniority. As workers gain seniority, they also receive higher pay.

The solvent sold to the two customers is essentially identical, but the military requires Bouwens to use a base chemical with a brand name, MX. The solvent for the commercial airlines is called CX. MX is required for military applications because it is sold by vendors on a preferred vendor list.

The company sells solvent for the market price to the airlines. solvent sold to the military is sold based on cost plus a fixed fee. That is, the government pays Bouwens for the recorded cost of the solvent plus a fixed amount of profit. The cost can be computed according to “commonly used product cost methods, including job costing or process costing methods using either FIFO or weighted-average methods.†Competition for the government business is very strong and Bouwens is always looking for ways to reduce the cost and the price it quotes the government.

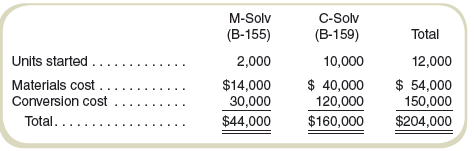

Currently, Bouwens uses a job costing system in which each month’s production for each customer type is considered a “job.†Thus, every month, Bouwens starts and completes one job in B-155 and one job in B-159. (There is never any beginning or ending work in process at Bouwens.) Recently, a dispute arose between Jack, the product manager for the military solvent, and Jill, the product manager for the commercial solvent, over the proper costing system.

Jack: It is ridiculous to use job costing for this. We are producing solvent. Everyone knows that the chemicals are the same. The fact the B-155 has high-cost labor is because all the senior employees want to work there. We could produce the same product with the employees in B-159. We should be using process costing and consider all the production, in both buildings for each month, as the batch.

Jill: Jack, the fact is that the military requires us to use a special chemical and their contracts require we keep track of the costs for their business. If we don’t separate the costing, we won’t know how profitable either business is. The following is production and cost information for a typical month, July:

Required

a. Compute the unit costs of M-Solv and C-Solv for July using the current system (job costing) at Bouwens.

b. Compute the costs of M-Solv and C-Solv for July if Bouwens were to treat all production as the same (combining B-155 and B-159 production).

c. Recommend a costing method that best reflects the cost of producing M-Solv and C-Solv.

d. For your recommended costing system, compute the cost of both M-Solv and C-Solv for July.

Transcribed Image Text:

C-Solv (B-159) M-Solv (B-155) Total Units started ..... 2,000 10,000 12,000 Materials cost.... Conversion cost $14,000 30,000 $ 40,000 120,000 $160,000 $ 54,000 150,000 Total...... $44,000 $204,000

> Describe a transaction that resulted in each of the following entries affecting the accounting equation. Assets Liabilities + Owner's Equity Office Professional Ассounts Cash + Equipment + Equipment Payable + B. Lake, Capital (a) +18,200 +18,200 (b)

> Define assets, liabilities, owner’s equity, revenues, and expenses.

> California Circuits Company (3C) manufactures a variety of components. Its Valley plant specializes in two electronic components used in circuit boards. These components serve the same function and perform equally well. The difference in the two products

> ACE Industries is a manufacturer of machined parts located in the midwestern United States. Its primary customers are suppliers to the automobile industry, although it has diversified its customer base in recent years to reduce its dependence on any one

> Cawker Products has two manufacturing facilities—Lucas plant and Russell plant—that produce the same product. Until recently, the production process in both plants has been the same. Last year, the Russell production supervisor, Ann Tyler, determined tha

> Refer to Problem 9-45. The intern decides to look more closely at the manufacturing activity and determines that it can be broken down into two activities: production and engineering. Production covers the costs of on-going manufacturing while engineerin

> Cain Components manufactures and distributes various plumbing products used in homes and other buildings. Over time, the production staff has noticed that products they considered easy to make were difficult to sell at margins considered reasonable while

> Utica Manufacturing (UM) was recently acquired by MegaMachines, Inc. (MM), and organized as a separate division within the company. Most manufacturing plants at MM use an ABC system, but UM has always used a traditional product costing system. Bob Miller

> College Supply Company (CSC) makes three types of drinking glasses: short, medium, and tall. It presently applies overhead using a predetermined rate based on direct labor-hours. A group of company employees recommended that CSC switch to activity-based

> Refer to Problem 9-38. Assume that you have prepared financial statements that show the operating profit for each of the two baskets manufactured by Bob’s Baskets. Further assume that under the activity-based costing approach (requireme

> Bob’s Baskets, Inc., manufactures and sells two types of baskets, deluxe and standard. Last year, Bob’s Baskets had the following costs and revenues: Bob’s Baskets currently uses labor costs to allo

> EZ-Seat, Inc., manufactures two types of reclining chairs, Standard and Ergo. Ergo provides support for the body through a complex set of sensors and requires great care in manufacturing to avoid damage to the material and frame. Standard is a convention

> The management of a liquid cleaning product company is trying to decide whether to install a job or process costing system. The manufacturing vice president has stated that job costing gives the best control because it is possible to assign costs to spec

> John’s Custom Computer Shop (JCCS) assembles computers for both individual and corporate customers. The company is organized into two divisions: Personal and Business. Once a computer is built, it is shipped to the customer. Billing for

> The Personnel Department at LastCall Enterprises handles many administrative tasks for the two divisions that make up LastCall: LaidBack and StressedOut. LaidBack division manages the company’s traditional business line. This business,

> Carolina Fashions, a shirt manufacturer, recently switched to activity-based costing from the department product costing method. The manager of Building S, which manufactures the shirts, has identified the following cost drivers and rates for overhead:

> Delta Parts, Inc., recently switched to activity-based costing from the department allocation method. The Fabrication Department manager has estimated the following cost drivers and rates: Direct materials costs were $300,000 and direct labor costs wer

> Wendy Chen established Windy City Coaching (WCC) to provide teen counseling and executive coaching services to its clients. WCC charges a $300 fee per hour for each service. The revenues and costs for the year are shown in the following income statement:

> Isadore’s Implements, Inc., manufactures pens and mechanical pencils often used for gifts. Overhead costs are currently allocated using direct labor-hours, but the controller has recommended an activity-based costing system using the fo

> We-Clean, Inc., is a home-cleaning service. It originally specialized in serving small residential clients but recently started contracting for work in large apartment and office buildings. Julie Lodge, the owner, believes that the commercial sector has

> Doaktown Products manufactures fishing equipment for recreational uses. The Miramichi plant produces the company’s two versions of a special reel used for river fishing. The two models are the M-008, a basic reel, and the M-123, a new a

> Rodent Corporation produces two types of computer mice, wired and wireless. The wired mice are designed as low-cost, reliable input devices. The company only recently began producing the higher-quality wireless model. Since the introduction of the new pr

> Cathy, the manager of Cathy’s Catering, Inc., uses activity-based costing to compute the costs of her catered parties. Each party is limited to 20 guests and requires four people to serve and clean up. Cathy offers two types of parties,

> Give examples of cost drivers commonly used to allocate overhead costs to products and services.

> After reviewing the new activity-based costing system that Janis McGee has implemented at Joplin Industries’s Port Arthur manufacturing facility, Kris Kristoff, the production supervisor, believes that he can reduce production costs by

> Refer to exercise 9-24. Kurt, the manager of the Ohio unit, is unhappy with the results of the controller’s study. He asks the controller to develop separate rates for fixed and variable costs in the Personnel Department. The controller

> The Personnel Department at Drumm Corporation is centralized and provides services to the two operating units: Illinois and Ohio. The Illinois unit is the original unit of Drumm and is well established. The Ohio unit is new, much like a start-up company.

> Main Street Ice Cream Company uses a plantwide allocation method to allocate overhead based on direct labor-hours at a rate of $3 per labor-hour. Strawberry and vanilla flavors are produced in Department SV. Chocolate is produced in Department C. Sven ma

> Munoz Sporting Equipment manufactures baseball bats and tennis rackets. Department B produces the baseball bats, and Department T produces the tennis rackets. Munoz currently uses plantwide allocation to allocate its overhead to all products. Direct labo

> A manager tells you that her company’s cost accounting system divides overhead into two pools: (1) Inspect material and (2) Assemble product. The inspect material pool is allocated on the basis of direct material dollars and the assemble product pool is

> Select an administrative function commonly found in a fi rm. Examples include personnel, accounts payable, purchasing, and so on. Outline an activity-based costing system for the function, including major activities, potential cost drivers, and relevant

> “We all know that cost allocation can distort decision making. We should stop doing this and just report direct costs.” Do you agree? Explain.

> Jim, the vice president of marketing, says the company should not adopt activity-based costing because it will result in the costs of some of the products going up but the market will not allow for raising prices. How would you respond?

> “Activity-based costing could not be applied in a business school.” Do you agree? Explain.

> The more important individual unit costs are used for decisions, the more likely it is that process costing will be preferred to job costing. Do you agree?

> “Activity-based costing does a better job of allocating both direct and indirect cost than traditional methods do.” Is this statement true, false, or uncertain? Explain.

> In what ways is implementing an activity-based costing system in a manufacturing firm’s personnel department the same as implementing it in the plant? In what ways is it different?

> What type of organization is most likely to benefit from using activity-based costing for product costing? Why?

> What are the basic steps in computing costs using activity-based costing?

> What are the costs of moving to an activity-based cost system? What are the benefits?

> Why do companies commonly use direct labor-hours or direct labor cost but not the number of units to allocate overhead?

> The product costs reported using either plantwide or department allocation are the same. The only difference is in the number of cost drivers used. True or false? Explain.

> Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an increase in revenues. With profits declining and revenues increasing, Rockness knew there must be a problem with costs. Rockness

> “Activity-based costing is just another inventory valuation method. It isn’t relevant for making operating decisions.” Do you agree with this statement? Explain.

> You have been asked to determine whether a company uses an activity-based cost system. What information would you look for to answer the question?

> It has been said that a prior department’s costs behave similarly to direct materials costs. Under what conditions are the costs similar? Why account for them separately?

> “Activity-based costing breaks down the indirect costs into several activities that cause costs (cost drivers). These should be the same for each department in an organization.” Is this true, false, or uncertain? Explain.

> “One of the lessons learned from activity-based costing is that all costs are really a function of volume of output.” Is this true, false, or uncertain? Explain.

> “It is clear after reading this chapter that activity-based costing is the best system. Whenever someone asks, I’ll recommend its adoption.” Do you agree? Explain.

> Vermont Company uses continuous processing to produce stuffed bears and FIFO process costing to account for its production costs. It uses FIFO because costs are quite unstable due to the volatile price of fi ne materials it uses in production. The bears

> Pacific Siding Incorporated produces synthetic wood siding used in the construction of residential and commercial buildings. Pacific Siding’s fiscal year ends on March 31, and the weighted-average method is used for the companyâ&#

> Miller Outdoor Equipment (MOE) makes four models of tents. The model names are Rookie, Novice, Hiker, and Expert. MOE manufactures the tents in two departments: Stitching and Customizing. All four models are processed initially in Stitching where all mat

> “Activity-based costing is the same as department costing.” Is this true, false, or uncertain? Explain.

> For each of the following independent cases, determine the units or equivalent units requested (assuming weighted-average costing). a. The WIP Inventory account had a beginning balance of $11,400 for conversion costs on items in process and, during the p

> For each of the following independent cases, use FIFO costing to determine the information requested. a. The ending inventory included $87,000 for conversion costs. During the period, 42,000 equivalent units were required to complete the beginning invent

> What is the distinction between equivalent units under the FIFO method and equivalent units under the weighted-average method?

> Refer to the information in Problem 8-47. Department R uses FIFO process costing to account for production. In January, beginning work-in-process inventory consisted of 50,000 units, 80 percent complete with respect to conversion. The cost of rubber pell

> Saline Solutions uses process costing to account for production of its unique compound BG at its River Plant. The River Plant has two departments: R and S. Raw materials are added at two points in the production of BG. First, rubber pellets are added at

> Why are cost drivers based on direct labor widely used?

> In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. It sells the products at cost. The direct materials costs are zero, but the operation requires the use of direct labor and overhead. The compa

> Cost allocation allocates only a given amount of costs to products. The total allocated is the same; therefore the choice of the system does not matter. True or false? Explain.

> Refer to the facts in Problem 8-42. In Problem 8-42 Douglas Toys is a manufacturer that uses the weighted-average process costing method to account for costs of production. It produces a plastic toy in three separate departments: Molding, Assembling, an

> Douglas Toys is a manufacturer that uses the weighted-average process costing method to account for costs of production. It produces a plastic toy in three separate departments: Molding, Assembling, and Finishing. The following information was obtained f

> The following pertains to the Cereal Division of McKenzie Corporation. Conversion costs for this division were 80 percent complete as to beginning work-in-process inventory and 50 percent complete as to ending work-in-process inventory. Information about

> Select the best answer for each of the following independent multiple-choice questions. a. Adams Company’s production cycle starts in Department A. The following information is available for July: _____________________________Units Wor

> Ferdon Watches, Inc., makes four models of watches, Gag-Gift, Commuter, Sport, and Retirement. Ferdon manufactures the watches in four departments: Assembly, Polishing, Special Finishing, and Packaging. All four models are started in Assembly where all m

> If costs increase from one period to another, will costs that are transferred out of one department under FIFO costing be higher or lower than costs transferred out using weighted-average costing? Why?

> Brokia Electronics manufactures three cell phone models, which differ only in the components included: Basic, Photo, and UrLife. Production takes place in two departments, Assembly and Special Packaging. The Basic and Photo models are complete after Asse

> Refer to the information in Exercise 8-36. In Exercise 8-36 Calgary Corporation produces a liquid solvent in two departments: Mixing and Finishing. Assume that Calgary Corporation provides you with the following information for Finishing operations for

> Calgary Corporation produces a liquid solvent in two departments: Mixing and Finishing. Assume that Calgary Corporation provides you with the following information for Finishing operations for November (no new material is added in the Finishing Departmen

> Refer to the information in Exercise 8-34. In Exercise 8-34 Assume that El Paso Corporation provides you with the following information for one of its department’s operations for September (no new material is added in Department B): WIP inventory—Depar

> Assume that El Paso Corporation provides you with the following information for one of its department’s operations for September (no new material is added in Department B): WIP inventory—Department B Beginning inventory (7,500 units, 20% complete with r

> Refer to the data in Exercise 8-30. Compute the cost of goods transferred out and the cost of ending inventory using the FIFO method. Is the ending inventory higher or lower under the weighted-average method compared to FIFO? Why? In Exercise 8-30 Pacif

> Refer to the data in Exercise 8-30. Compute the cost per equivalent unit for direct materials and for conversion costs using the FIFO method. In Exercise 8-30 Pacific Ink had beginning work-in-process inventory of $744,960 on October 1. Of this amount,

> Refer to the data in Exercise 8-30. Compute the costs of goods transferred out and the ending inventory using the weighted-average method. In Exercise 8-30 Pacific Ink had beginning work-in-process inventory of $744,960 on October 1. Of this amount, $30

> Pacific Ink had beginning work-in-process inventory of $744,960 on October 1. Of this amount, $304,920 was the cost of direct materials and $440,040 was the cost of conversion. The 48,000 units in the beginning inventory were 30 percent complete with res

> Refer to the data in Exercises 8-26 and 8-28. Compute the cost of goods transferred out and the ending inventory using the FIFO method. In Exercises 8-26 and 8-28 The Matsui Lubricants plant uses the weighted-average method to account for its work-in-pr

> A manufacturing company has records of its activity during the month in work-in-process inventory and of its ending work-in-process inventory; however, the record of its beginning inventory has been lost. What data are needed to compute the beginning inv

> Using the data in Exercise 8-26, compute the cost per equivalent unit for direct materials and for conversion costs using the FIFO method. In Exercises 8-26 The Matsui Lubricants plant uses the weighted-average method to account for its work-in-process

> Refer to the data in Exercise 8-26. Compute the cost of goods transferred out and the ending inventory using the weighted-average method. In Exercises 8-26 The Matsui Lubricants plant uses the weighted-average method to account for its work-in-process i

> The Matsui Lubricants plant uses the weighted-average method to account for its work-in process inventories. The accounting records show the following information for a particular day: Beginning WIP inventory Direct materials . . . . . . . . . . . . . .

> Refer to the data in Exercise 8-24. Cost data for April show the following: Beginning WIP inventory Direct materials costs . . . . . . . . . . . . . . $ 24,300 Conversion costs . . . . . . . . . . . . . . . . . . . . 38,700 Current period costs Direct

> Materials are added at the beginning of the production process at Santiago Company, which uses a FIFO process costing system. The following information on the physical flow of units is available for the month of April: Beginning work in process (40% com

> Refer to the data in Exercise 8-22. In Exercise 8-22. The following information pertains to the Davenport plant for the month of May (all materials are added at the beginning of the process): Required Compute the cost per equivalent unit for materials

> The following information pertains to the Davenport plant for the month of May (all materials are added at the beginning of the process): Required Compute the cost per equivalent unit for materials using the weighted-average method. Units Material

> Delhi, Inc., seeks your assistance in developing cash and other budget information for August, September, and October. At July 31, the company had cash of $22,000, accounts receivable of $1,748,000, inventories of $1,237,600, and accounts payable of $532

> Capstone Corporation has just received its sales expense report for January, which follows. Item _____________________Amount Sales commissions . . . . . . . . . . . . . . . . . $121,500 Sales staff salaries . . . . . . . . . . . . . . . . . . . 28,800 Te

> Lotus Fixtures, Inc. (LFI), manufactures steel fittings. Each fitting requires both steel and an alloy that allows the fitting to be used under extreme conditions. The following data apply to the production of the fittings: Direct materials per unit 2 po

> Refer to the data in Problem 13-42. Estimate the cash from operations expected in year 2. In Problem 13-42 Cameron Parts has the following data from year 1 operations, which are to be used for developing year 2 budget estimates: Sales revenue (12,500 un

> Refer to the data in Problem 13-40. Estimate the cash from operations expected in year 2. In Problem 13-40 The following information is available for year 1 for Dancer Components: Sales revenue (300,000 units) . . . . . . $5,700,000 Manufacturing costs

> Bay Area Limos operates transportation services to Bay City airport. The price of service is fixed at a flat rate for each trip and most costs of providing the service are fixed for each trip. Betty Smith, the owner, forecasts income by estimating two fa

> Sanjana’s Sweet Shoppe operates on the boardwalk of a New England coastal town. The store only opens for the summer season and the business is heavily dependent on the weather and the economy in addition to new competition. Sanjana Swee

> Elizabeth Jablonski is the director of Research and Development for Galaxy Electronics. Last week, she submitted the following funding request as part of the annual budget process. Project ___________________Funding Request 1. Portable audio project . .

> Bears, Inc., adds materials at the beginning of the process in Department MO. The following information on physical units for Department MO for the month of July is available: Work in process, July 1 (75% complete with respect to conversion). . . . . .

> The controller of Northwest Hardware has just received two forecasts for sales in the Montana District for the coming year. Based on an econometric analysis of consumer spending and economic trends, a marketing research firm estimates sales of $1 million

> BK Consulting is a management consulting fi rm. Other than the senior leadership (who manage the firm, but do not actively consult), the managers and staff are billed to clients on an hourly basis. The workload varies quite a bit from month to month requ

> Carreras Café is a Spanish restaurant in a college town. The owner expects that the number of meals served in June will be 40 percent below those served in May, because so many students leave for the summer. In May, the restaurant served 4,200 meals at a

> Rhodes, Inc., is a fast-growing start-up firm that manufactures bicycles. The following income statement is available for July: Sales revenue (200 units @ $500 per unit) . . . . $100,000 Less Manufacturing costs Variable costs . . . . . . . . . . . . . .

> Refer to the data in Exercise 13-31. Varmit-B-Gone estimates that the number of subscribers in September should fall 10 percent below August levels, and the number of service calls per subscriber should decrease by an estimated 20 percent. The following

> Varmit-B-Gone is a pest control service that operates in a suburban neighborhood. The company attempts to make service calls at least once a month to all homes that subscribe to its service. It makes more frequent calls during the summer. The number of s