Question: Casa Royale, Inc., a public company, retains

Casa Royale, Inc., a public company, retains Ying and Company CPA to audit its financial statements and internal control. Howard Smythe, the partner in charge of the audit, drafted the following unqualified report:

Respond as to the accuracy of the following comments made by a reviewer of the report:

Transcribed Image Text:

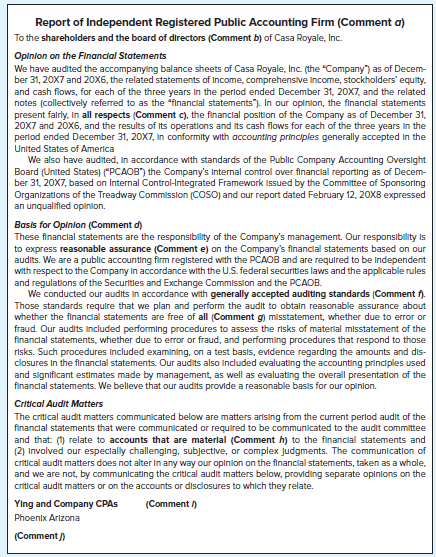

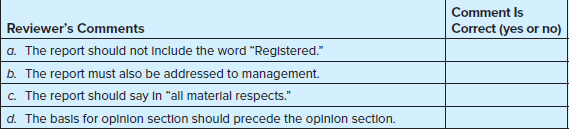

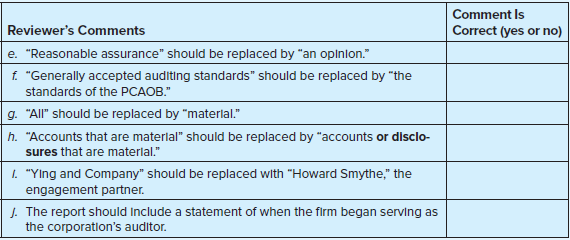

Report of Independent Registered Public Accounting Firm (Comment a) To the shareholders and the board of directors (Comment b) of Casa Royale, Inc. Oplnion on the Financial Statements We have audited the accompanying balance sheets of Casa Royale, Inc. (the "Company) as of Decem- ber 31, 20X7 and 20X6, the related statements of Income, comprehensive Income, stockholders' equity. and cash flows, for each of the three years In the perlod ended December 31, 20X7, and the related notes (collectively referred to as the "financlal statements"). In our opinion, the flnanclal statements present falrly, In all respects (Comment c), the financlal position of the Company as of December 31, 20X7 and 20X6, and the results of Its operations and its cash flows for each of the three years in the perlod ended December 31, 20X7, In conformity with accounting principles generally accepted In the United States of America We also have audited, In accordance with standards of the Public Company Accounting Oversight Board (United States) ("PCAOB") the Company's Internal control over financial reporting as of Decem- ber 31, 20X7, based on Internal Control-Integrated Framework Issued by the Committee of Sponsoring Organizatlons of the Treadway Commisslon (COSO) and our report dated February 12, 20X8 expressed an unqualifled opinion. Basis for Opinion (Comment d) These financlal statements are the responsibility of the Company's management. Our responsibility Is to express reasonable assurance (Comment e) on the Company's financlal statements based on our audits. We are a public accounting filrm registered with the PCAOB and are requlred to be Independent with respect to the Company In accordance with the U.S. federal securitles laws and the applicable rules and regulations of the Securitles and Exchange Commisslon and the PCAOB. We conducted our audits In accordance with generally accepted auditing standards (Comment f). Those standards require that we plan and perform the audit to obtaln reasonable assurance about whether the financlal statements are free of all (Comment g) misstatement, whether due to error or fraud. Our audits Included performing procedures to assess the risks of materlal misstatement of the financlal statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures Included examining, on a test basis, evidence regarding the amounts and dis- closures In the financlal statements. Our audits also Indluded evaluating the accounting prindples used and significant estimates made by management, as well as evaluating the overall presentation of the financlal statements. We belleve that our audits provide a reasonable basis for our opinlon. Critical Audit Matters The critical audit matters communicated below are matters arlsing from the current perlod audit of the financlal statements that were communicated or required to be communicated to the audit committee and that (1) relate to accounts that are materlal (Comment h) to the financial statements and (2) Involved our especlally challenging, subjective, or complex Judgments. The communication of critical audit matters does not alter In any way our opinilon on the financial statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinlons on the critical audit matters or on the accounts or disclosures to which they relate. Ying and Company CPAS (Comment /) Phoenlx Arizona (Comment) Comment Is Reviewer's Comments Correct (yes or no) a. The report should not Include the word "Registered." b. The report must also be addressed to management. c. The report should say In "all materlal respects." d. The basis for opinion sectlon should precede the oplnlon sectlon. Comment Is Reviewer's Comments Correct (yes or no) e. "Reasonable assurance" should be replaced by "an oplnlon." f. "Generally accepted auditing standards" should be replaced by "the standards of the PCAOB." g. "All" should be replaced by "materlal." h. "Accounts that are materlal" should be replaced by "accounts or disclo- sures that are materlal." I. "Ying and Company" should be replaced with "Howard Smythe," the engagement partner. J. The report should Include a statement of when the firm began serving as the corporatlon's auditor.

> You own a firm with a single new product that is about to be introduced to the public for the first time. Your marketing analysis suggests that the annual demand for this product could be anywhere between 500,000 units and 5,000,000 units. Given such a w

> What is the advantage of using a simulation analysis instead of a scenario analysis to assess the risk of a project?

> Why are capital investments considered the most important decisions made by a firm’s management?

> You are involved in the planning process for a firm that is expected to have a large increase in sales next year. Which type of firm would benefit the most from that sales increase: a firm with low fixed costs and high variable costs or a firm with high

> Explain the difference between marginal and average tax rates, and identify which of these rates is used in capital budgeting and why?

> How is the MACRS depreciation method under IRS rules different from the straight-line depreciation allowed under GAAP rules? What is the implication on incremental after-tax free cash flows from firms’ investments?

> High-End Fashions, Inc., bought a production line of ankle-length skirts last year at a cost of $500,000. This year, however, miniskirts are in and ankle-length skirts are completely out of fashion. High-End has the option to rebuild the production line

> QualityLiving Trust is a real estate investment company that builds and remodels apartment buildings in northern California. It is currently considering remodeling a few idle buildings that it owns in San Jose into luxury apartment buildings. The company

> MusicHeaven, Inc., is a producer of media players which currently have either 20 gigabytes or 30 gigabytes of storage. Now the company is considering launching a new production line making mini media players with 5 gigabytes of storage. Analysts forecast

> Suppose that FRA Corporation already has divisions in both Dallas and Houston. FRA is now considering setting up a third division in Austin. This expansion will require that one senior manager from Dallas and one from Houston relocate to Austin. Ignore r

> You are providing financial advice to a shrimp farmer who will be harvesting his last crop of farm-raised shrimp. His current shrimp crop is very young and will, therefore, grow and become more valuable as their weight increases. Describe how you would d

> What is the opportunity cost of using an existing asset? Give an example of the opportunity cost of using the excess capacity of a machine?

> When two mutually exclusive projects have different lives, how can an analyst determine which is better? What is the underlying assumption in this method?

> Describe the process of capital rationing?

> Do you agree or disagree with the following statement given the discussion in this chapter? We can calculate future cash flows precisely and obtain an exact value for the NPV of an investment?

> Under what circumstances might the IRR and NPV approaches produce conflicting results?

> What are the strengths and weaknesses of the accounting rate of return approach?

> Identify the weaknesses of the payback period method?

> a. A firm invests in a project that is expected to earn a return of 12 percent. If the appropriate cost of capital is also 12 percent, did the firm make the right decision. Explain. b. What is the impact on the firm if it accepts a project with a negati

> In the context of capital budgeting, what is “capital rationing”?

> a. Sykes, Inc. management is considering two projects: a plant expansion and a new computer system for the firm’s production department. Classify these projects as independent, mutually exclusive, or contingent projects and explain your reasoning. b. A c

> Elkridge Construction Company has an overall (composite) cost of capital of 12 percent. This cost of capital reflects the cost of capital for an Elkridge Construction project with average risk. However, the firm takes on projects of various risk levels.

> Explain why the cost of capital is referred to as the “hurdle” rate in capital budgeting?

> The profitability index is a tool for measuring a project’s benefits relative to its costs. How might this help to eliminate bias in project selection?

> What is the cost of capital?

> What is the general formula used to calculate the price of a share of a stock? What does it mean?

> Select the best answer for each of the following questions. Explain the reasons for your selection. a. Which of the following is not a financial statement assertion made by management? (1) Existence of recorded assets and liabilities. (2) Completeness of

> For each definition (or portion of a definition) in the first column, select the term that most closely applies. Each term may be used only once or not at all. Partial (or Complete) Definition Term a. A federal securities statute covering registrat

> Items (a) through ( f ) relate to what a plaintiff who purchased securities must prove in a civil liability suit against a CPA. For each item, determine whether it must be proved assuming application of the following acts: 1. Only applies to Section 11 o

> Match the important cases listed below with the appropriate legal precedent or implication. Case: a. Hochfelder v. Ernst b. Escott v. BarChris Construction Corp. c. Credit Alliance v. Arthur Andersen & Co. d. Ultramares v. Touche & Co. e. Rosenblum v. A

> Assume that in a particular audit the CPAs were negligent but not grossly negligent. Indicate whether they would be “liable” or “not liable” for the following losses proximately caused by their negligence and determine that liability under the various th

> Dandy Container Corporation engaged the accounting firm of Adams and Adams to audit financial statements to be used in connection with an interstate public offering of securities. The audit was completed, and an unqualified opinion was expressed on the f

> Gloria and Deloria, CPAs, have recently started their public accounting firm and intend to provide attestation and a variety of consulting services for their clients, which are all nonpublic. Both Ms. Gloria and Mr. Deloria have particular expertise in d

> The firm of Schilling & Co., CPAs, has offices in Chicago and Green Bay, Wisconsin. Gillington Company, which has 1 million shares of outstanding stock, is audited by the Chicago office of Schilling; Welco, of the Chicago office, is the partner in charge

> The firm of Bell & Greer, CPAs, has been asked to perform attest services for Trek Corporation (a nonpublic company) for the year ended December 31, Year 5. Bell & Greer has two offices: one in Los Angeles and the other in Newport Beach. Trek Corporation

> Describe briefly the function of the GAO.

> The cost of an audit might be significantly reduced if the auditors relied upon a representation letter from the client instead of observing the physical counting of inventory. Would this use of a representation letter be an acceptable means of reducing

> James Daleiden, CPA, is interested in expanding his practice through acquisition of new clients. For each of the following independent cases, indicate whether Daleiden would violate the AICPA Code of Professional Conduct by engaging in the suggested prac

> The firm of Harwood & Toole, CPAs, has been the auditor and tax return preparer for Tucker, Inc., a nonpublic company, for several years. In the current year, the management of Tucker discharged Harwood & Toole from the audit and tax engagement because o

> The firm of McGraw and West, CPAs, has two offices, one in Phoenix and one in San Diego. The firm has audited the Cameron Corporation out of its Phoenix office for the past five years. For each of the following independent cases, which occurred during th

> Donald Westerman is president of Westerman Corporation, a nonpublic manufacturer of kitchen cabinets. He has been approached by Darlene Zabish, a partner with Zabish and Co., CPAs, who suggests that her firm can design a payroll system for Westerman that

> The firm of Wilson and Wiener (WW), CPAs, has had requests from a number of clients and prospective clients to perform various types of services. Please reply as to whether the appropriate independence rules (AICPA and/or PCAOB) allow the following engag

> Select the best answer for each of the following. Explain the reasons for your selection. a. Which of the following is not a covered member for an attest engagement under the Independence Rule of the AICPA Code of Professional Conduct? (1) An individual

> For each term in the first column, select the partial (or complete) definition or illustration. Each partial (or complete) definition or illustration may be used only once. Term Partial (or Complete) Definition or Illustration a. A report providing

> State whether each of the following is or is not a principle (or a portion of a principle) underlying an audit conducted in accordance with generally accepted auditing standards. Principles Yes (Y) or No (N) 1. The purpose of an audit Is to provide

> Match each the following statements with the appropriate type of auditors’ report (each auditors’ report may be used once, more than once, or not at all): A. Adverse. D. Disclaimer. Q. Qualified. S. Standard unmodified

> State whether you agree (A) or disagree (D) with each of the following statements concerning the auditors’ unqualified report of a public company. Agree (A) or Disagree (D) Statement a. The report should begln with "CPA's Report"

> What are the major purposes of obtaining representation letters from audit clients?

> Spacecraft, Inc., is a large corporation that is audited regularly by a public accounting firm but also maintains an internal auditing staff. Explain briefly how the relationship of the public accounting firm to Spacecraft differs from the relationship o

> Select the best answer for each of the following items and give reasons for your choice. a. Which of the following organizations can revoke the right of an individual to practice as a CPA? (1) The Public Company Accounting Oversight Board. (2) The Americ

> For the purposes of this problem, assume the existence of five types of auditors: CPA, GAO, IRS, bank examiner, and internal auditor. Also assume that the work of these various auditors can be grouped into five classifications: audits of financial statem

> Susan Harris is a new assistant auditor with the public accounting firm of Sparks, Watts, and Wilcox, CPAs. On her third audit assignment, Harris examined the documentation underlying 60 disbursements as a test of controls over purchasing, receiving, vou

> Wanda Young, doing business as Wanda Young Fashions, engaged the CPA partnership of Scott & Green to audit her financial statements. During the audit, Scott & Green discovered certain irregularities that would have indicated to a reasonably prudent audit

> The public accounting firm of Hanson and Brown was expanding very rapidly. Consequently, it hired several staff assistants, including James Small. Subsequently, the partners of the firm became dissatisfied with Small’s production and warned him that they

> Jensen, Inc., filed suit against a public accounting firm, alleging that the auditors’ negligence\ was responsible for failure to disclose a large defalcation that had been in process for several years. The public accounting firm responded that it may ha

> Glover, Inc., engaged Herd & Irwin, CPAs, to assist in the installation of a new computerized production system. Because the firm did not have experienced staff available for the engagement, Herd & Irwin assigned several newly hired staff assistants with

> What would you accept as satisfactory documentary evidence in support of entries in the following? a. Sales journal. b. Sales returns journal. c. Voucher or invoice register. d. Payroll journal. e. Check register.

> Provide at least four examples of specialists whose findings might provide appropriate evidence for the independent auditors.

> Auditors are required on every engagement to obtain a representation letter from the client. Required: a. What are the objectives of the client’s representation letter? b. Who should prepare and sign the client’s representation letter? c. When should th

> Is an independent status possible or desirable for internal auditors as compared with the independence of a public accounting firm? Explain.

> When analytical procedures disclose unexpected changes in financial relationships relative to prior years, the auditors consider the possible reasons for the changes. Give several possible reasons for the following significant changes in relationships: a

> Analytical procedures are extremely useful throughout the audit. Required: a. Explain how analytical procedures are useful in (1) The risk assessment stage of the audit. (2) The substantive procedures stage of the audit. (3) Near the end of the audit. b

> Comment on the reliability of each of the following examples of audit evidence. Arrange your answer in the form of a separate paragraph for each item. Explain fully the reasoning employed in judging the reliability of each item. a. Copies of client’s sal

> In an audit of financial statements, the auditors gather various types of audit evidence. List seven major types of evidence and provide a procedural example of each.

> Marion Watson & Co., CPAs, is planning its audit procedures for its tests of the valuation of inventories of East Coast Manufacturing Co. The auditors on the engagement have assessed inherent risk and control risk for valuation of inventories at 100 perc

> Financial statements contain a number of assertions about account balances, classes of transactions, and disclosures. a. Identify who makes these assertions. b. List and describe each of the assertions regarding each financial statement component.

> At 12 o’clock, when the plant whistle sounded, George Jones, an assistant auditor, had been working on his laptop computer. Jones stopped work immediately, but not wanting to waste a lot of time, he simply closed his laptop. He then departed for lunch. T

> Working papers should contain facts and nothing but facts,” said student A. “Not at all,” replied student B. “The audit working papers also may include expressions of opinion. Facts are not always available to settle all issues.” “In my opinion,” said st

> Use of data analytics is likely to increase the use of sampling and eliminate the audit of all items in a population.” Comment on the accuracy of this quotation.

> Gordon & Moore, CPAs, were the auditors of Fox & Company, a brokerage firm. Gordon & Moore examined and reported on the financial statements of Fox, which were filed with the Securities and Exchange Commission. Several of Fox’s customers were swindled by

> The international CPA firm of Arthur Andersen faced significant liability in conjunction with its audits of Enron Corporation. Required: a. From a legal liability perspective, describe the unique features of this audit case. b. Describe the important im

> Distinguish between a compliance audit and an operational audit.

> Sawyer and Sawyer, CPAs, audited the financial statements of Rattler Corporation that were included in Rattler’s Form 10-K, which was filed with the SEC. Subsequently, Rattler Corporation went bankrupt and the stockholders of the corporation brought a cl

> Ron Barber, CPA, is auditing the financial statements of DGF, Inc., a publicly held company. During the course of the audit, Barber discovered that DGF has been making illegal bribes to foreign government officials to obtain business, and he reported the

> Tracy Smith, CPA, is in charge of the audit of Olympic Fashions, Inc. Seven young members of the public accounting firm’s professional staff are working with Smith on this engagement, and several of the young auditors are avid skiers. Olympic Fashions ow

> The firm of Williams, Kline & Chow, CPAs, is the auditor of Yuker Corporation, a nonpublic company. The president of Yuker, Karen Lester, has been putting pressure on Chee Chow, the audit partner, to accept a questionable accounting principle. She has ev

> Jenko Corp. is an audit client of the Phoenix office of Williams and Co., CPAs. Williams and Co. has offices in Arizona, including ones in Phoenix, Tucson, and Tombstone. For purposes of independence, the AICPA requires that no “covered member” may have

> Roger Royce, CPA, has encountered a situation that he thinks may pose a threat to his independence with respect to Watson, Inc., an audit client. The situation is not addressed by an independence rule or regulation. Using the AICPA Conceptual Framework f

> Sally Adams is an audit manager for the firm of Jones & Smith, CPAs, and is assigned to the audit of Libra Fashions, Inc. Near the middle of the audit, Sally was offered the job of Libra’s chief financial officer. Required: a. Discuss the implications o

> Provide an example in which a data analytics technique applied in financial statement auditing could serve as both a test of a control and a substantive procedure.

> Reed, CPA, accepted an engagement to audit the financial statements of Smith Company. Reed’s discussions with Smith’s new management and the predecessor auditor indicated the possibility that Smith’s financial statements may be misstated due to the possi

> Jane Lee, a director of a nonpublic corporation with a number of stockholders and lines of credit with several banks, suggested that the corporation appoint as controller John Madison, a certified public accountant on the staff of the auditing firm that

> An attitude of independence is a most essential element of an audit by a firm of certified public accountants. Describe several situations in which the CPA firm might find it somewhat difficult to maintain this independent point of view.

> What does an operational audit attempt to measure? Does an operational audit involve more or fewer subjective judgments than a compliance audit or an audit of financial statements? Explain. To whom is the report usually directed after completion of an op

> Various organizations develop standards for audits and regulate CPA firms. Compare and contrast the roles of the AICPA, the PCAOB, and the state boards of accountancy along the following dimensions: Required: a. Standard setting. b. Regulation of CPA fi

> While the AICPA administers a peer review program for CPA firms, the PCAOB staff performs practice inspections. Required: a. Identify the two basic types of peer review. b. On what part of a firm’s practice does the PCAOB staff focus its inspections? c.

> The self-interest of the provider of financial information (whether an individual or a business entity) often runs directly counter to the interests of the user of the information. Required: a. Give an example of such opposing interests. b. What may be

> The Sarbanes-Oxley Act of 2002 created the Public Company Accounting Oversight Board. Explain the major responsibilities of this board.

> A corporation is contemplating issuing debenture bonds to a group of investors. Required: a. Explain how independent audits of the corporation’s financial statements facilitate this transaction. b. Describe the likely effects on the transaction if the c

> As a result of a number of events that caused Congress to doubt the ability of the accounting profession to regulate itself, a number of reforms were made to the accounting profession’s system of self-regulation. Required: a. Provide a brief overview of

> When in the course of an audit might the auditors find it useful to apply analytical procedures?

> Evaluate the following statement: A canceled check is not considered particularly reliable evidence because the check was prepared within the client’s organization.

> As part of the verification of accounts receivable as of the balance sheet date, the auditors might inspect copies of sales invoices. Similarly, as part of the verification of accounts payable, the auditors might inspect purchase invoices. Which of these

> The best means of verification of cash, inventory, office equipment, and nearly all other assets is a physical count of the units; only a physical count gives the auditors complete assurance as to the accuracy of the amounts listed on the balance sheet.”

> In a conversation with you, Mark Rogers, CPA, claims that both the sufficiency and the appropriateness of audit evidence are a matter of judgment in every audit. Do you agree? Explain.

> Contrast the objectives of auditing at the beginning of this century with the objectives of auditing today.

> Distinguish between the component of audit risk that the auditors gather evidence to assess versus the component of audit risk that they collect evidence to restrict.

> Distinguish among routine, non-routine, and estimation transactions. Include an example of each.

> I have finished my testing of footings of the cash journals,” said the assistant auditor to the senior auditor. “Shall I state in the working papers the periods for which I verified footings, or should I just list the totals of the receipts and disbursem

> Describe the relationship between detection risk and audit risk.