Question: Exhibit 6.12 in Chapter 6 provides

Exhibit 6.12 in Chapter 6 provides a simplified statement of cash flows. For each of the transactions that follow, indicate the number(s) of the line(s) in Exhibit 6.12 affected by the transaction and the amount and direction (increase or decrease) of the effect. If the transaction affects net income on line (3) or cash on line (11), be sure to indicate if it increases or decreases the line. Expand the definition of Line (1) to include receipts from other operating revenue sources. Ignore income tax effects. Indicate the effects of each transaction on the Cash Change Equation.

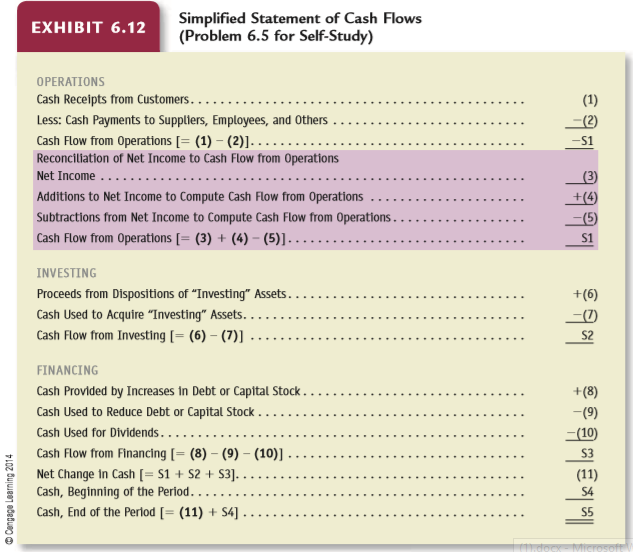

a. A firm declares cash dividends of $15,000, of which it pays $12,000 immediately to its shareholders; it will pay the remaining $3,000 early in the next accounting period.

b. A firm borrows $75,000 from its bank.

c. A firm sells for $20,000 machinery originally costing $40,000 and with accumulated depreciation of $35,000.

d. A firm as lessee records lease payments on operating leases of $28,000 for the period.

e. A firm acquires, with temporarily excess cash, marketable equity securities costing $39,000.

f. A firm writes off a fully depreciated truck originally costing $14,000.

g. A marketable equity security (available for sale) acquired during the current period for $90,000 has a fair value of $82,000 at the end of the period. Indicate the effect of any year-end adjusting entry to apply the market value method.

h. A firm records interest expense of $15,000 for the period on bonds issued several years ago at a discount, comprising a $14,500 cash payment and a $500 addition to Bonds Payable.

i. A firm records an impairment loss of $22,000 for the period on goodwill arising from the acquisition several years ago of an 80% investment in a subsidiary.

Exhibit 6.12:

Transcribed Image Text:

Simplified Statement of Cash Flows (Problem 6.5 for Self-Study) EXHIBIT 6.12 OPERATIONS Cash Recelpts from Customers. .. . (1) Less: Cash Payments to Suppliers, Employees, and Others -(2) Cash Flow from Operations [= (1) – (2)]. ... -S1 Reconciliation of Net Income to Cash Flow from Operations Net Income ... |(3) Additions to Net Income to Compute Cash Flow from Operations Subtractions from Net Income to Compute Cash Flow from Operatlons . . Cash Flow from Operatlons [= (3) + (4) – (5)]... +(4) -(5) S1 INVESTING Proceeds from Dispositions of "Investing" Assets.. +(6) Cash Used to Acquire "Investing" Assets. . -(1) Cash Flow from Investing [= (6) – (7)) S2 FINANCING Cash Provlided by Increases în Debt or Capital Stock . +(8) Cash Used to Reduce Debt or Capital Stock ... -(9) Cash Used for Dividends.... -(10) Cash Flow from Financing [= (8) – (9) – (10)] S3 Net Change in Cash [= S1 + S2 + S3]. . Cash, Beginning of the Period..... Cash, End of the Perlod [= (11) + S4] . (11) ... .. S4 S5 Cengage Learning 2014

> What role does a special purpose entity or variable interest entity serve in achieving off balance-sheet financing involving the sale of receivables?

> Recognizing rights and obligations embodied in all executory contracts would eliminate a means of off-balance-sheet financing.” How might such an action confuse and possibly mislead financial statement users?

> Compare and contrast the financial statement effects of achieving off-balance-sheet financing through an executory contract versus an asset sale in which the seller of the assets will reimburse the buyer for any shortfall in collections from the purchase

> Of what value is information about the components of deferred tax assets and deferred tax liabilities, given that firms calculate income tax expense on income before taxes and not on individual revenues and expenses?

> The required accounting for deferred taxes delays recognizing in net income the benefits and costs of temporary differences from the period when they originate to the period when they reverse.” Explain.

> Under what circumstances will a firm report a deferred tax asset on the balance sheet? Under what circumstances will a firm report a deferred tax liability on the balance sheet?

> One might view a deferred tax liability as an interest-free loan from the government.” Do you agree? Why or why not?

> Describe the U.S. GAAP rationale for reducing pension expense for the return on pension investments.

> Selected data from the accounts of Seward Corporation appear next; the firm’s fiscal year ends on December 31. The firm makes all sales on account. There were no recoveries during the year of accounts written off in previous years. G

> A retailer leases space in a shopping center, whose buildings have a 30-year life, on a 10-year lease. The lessee pays a small fixed amount per month plus 10% of sales for the previous month. How will the retailer treat this lease under the old/current r

> Refer to the preceding two questions. Describe the circumstances under which a firm would report a net gain from its borrowing activities. Give an example and the general principle. You may find using zero coupon bonds as examples a good way to think abo

> Refer to question 6. Would your answer differ if the firm repaid the bond prior to maturity? Data from question 6: “The total effect on income before income taxes over the life of a bond that a firm repays at maturity will be the same whether the firm

> The total effect on income before income taxes over the life of a bond that a firm repays at maturity will be the same whether the firm accounts for the bond using amortized cost measurement based on the historical market interest rate or fair value meas

> Firm A issues $1,000,000 face value, 9% semiannual coupon bonds at a price to yield 8% compounded semiannually. Firm B issues $1,000,000 face value, 7% semiannual coupon bonds at a price to yield 8% compounded semiannually. Both bond issues mature in 20

> A firm issues two bonds with identical issue prices, market-required yields, and final maturity dates. One bond is a semiannual coupon bond, and the other bond is a serial bond. Will the total interest expense over the life of these two bonds be the same

> Applying the effective interest method using the historical market interest rate gives a constant amount of interest expense on bonds each period.” Do you agree? If not, how would you change the statement to make it accurate?

> Using amortized cost based on the historical market interest rate to account for bonds in periods subsequent to their initial issuance provides a carrying value for bonds that is consistent with using historical, or acquisition, cost measurements for ass

> If permitted, a lessor generally prefers to account for leases using the capital lease method for financial reporting and the operating lease method for tax reporting.” Explain.

> If permitted, a lessee generally prefers to account for leases using the operating lease method for financial reporting and the capital lease method for tax reporting.” Explain.

> Find the interest rate implicit in a loan of $100,000 that the borrower discharges with two annual installments of $55,307 each, paid at the end of each of the next two years.

> The lessor who manufactured the equipment it leases to the lessee recognizes the same amount of income (revenue minus expenses) over the term of a lease as the lessee recognizes as expenses.” Do you agree or disagree? Explain.

> In what ways is a lessee’s capital lease similar to, and different from, purchasing the equipment using the proceeds of a loan repayable in installments?

> Relate the concept of return of capital to the criterion under U.S. GAAP for deciding whether an impairment loss on long-lived assets other than non-amortized intangibles has occurred.

> A firm expects to use a delivery truck for five years. At the end of three years, the transmission wears out and requires replacement at a cost of $4,000. The firm argues that it should capitalize the expenditure because without it the useful life is zer

> An airline has depreciated its new aircraft in the past over 25 years. New fuel usage and safety standards indicate that a shorter useful life is now appropriate for all of its existing aircraft. Depending on the circumstances, the airline might (a) spre

> When Thames acquires another firm, it allocates a portion of the purchase price to brand names, some of which it amortizes and some of which it does not amortize. How does Thames likely justify this different treatment of brand names?

> Contrast the terms finite life and indefinite life as they apply to depreciation of tangible long-lived assets and amortization of intangible assets.

> What is the effect of capitalizing interest costs associated with self-constructed assets on reported income summed over all the periods of the life of a given self-constructed asset, from building through use until eventual retirement? Contrast with a p

> If Merck, a pharmaceutical firm, makes expenditures to research new drugs, it must treat the expenditures as an expense. If it acquires a patent for a new drug from its creator, it must treat the expenditure as an asset. If it acquires another firm with

> A firm that makes expenditures to self-construct a building treats the expenditures as an asset. When that same firm makes research and development expenditures to create a new patented technology, it must treat the expenditures as an expense. When that

> Dove Company’s accounts receivable show the following balances by age: Age of Accounts……………………………………….Balance Receivable Not yet due……………………………………………………………….$1,200,000 0–30 Days…………………………………………………………………….400,000 31–60 Days………………………………………………………………………90,0

> Suppose that competition among acquiring firms to make a corporate acquisition results in a valuation error, such that the acquiring firm overpays for the acquired firm. The acquiring firm will allocate the excess purchase price to goodwill, along with a

> The use of undiscounted, instead of discounted, cash flows for identifying asset impairment losses under U.S. GAAP seems to lack a conceptual basis. Explain why discounted cash flows are preferred to undiscounted cash flows in this scenario.

> Why does the cash recoverability criterion apply to impairment losses on amortized intangibles but not on non-amortized intangibles under U.S. GAAP?

> The Francis W. Parker School, a private lower school, has a reporting year ending June 30. It hires teachers for a 10-month period: September of one year through June of the following year. It contracts to pay teachers in 12 monthly installments over the

> Firms should obtain as much financing as possible from suppliers through accounts payable because it is a free source of funds.” Do you agree? Why or why not?

> Compare and contrast the Merchandise Inventory account of a merchandising firm and the Finished Goods Inventory account of a manufacturing firm.

> Describe the similarities and differences between the allowance method for un collectibles (see Chapter 8) and the allowance method for warranties.

> A noted accountant once remarked that the optimal number of faulty TV sets for Sony to sell is “not zero,” even if Sony promises to repair all faulty Sony sets that break down, for whatever reason, within two years of purchase. Why could the optimal numb

> Under what circumstances will the Allowance for Uncollectible Accounts have a debit balance during the accounting period? The balance sheet figure for the Allowance for Uncollectible Accounts at the end of the period should never show a debit balance. Wh

> a. An old wisdom in tennis holds that if your first serves are always good, you are not hitting them hard enough. An analogous statement in business might be that if you have no uncollectible accounts, you probably are not selling enough on credit. Comme

> York Company’s accounts receivable show the following balances: Age of Accounts………………………………………………..Balance Receivable 0–30 Days…………………………………………………………………..$1,200,000 31–60 Days………………………………………………………………………255,000 61–120 Days………………………………………………………………………..75,

> Conceptually, what kind of account is the Deferred Gross Margin account that arises under the installment method of accounting? How is this account typically classified on balance sheets?

> Both bad debt expense and expected returns reduce income in the period of sale. How does the accounting for these two items differ and how is it similar?

> A magazine publisher offers a reduced annual subscription fee if customers pay for three years in advance. Under this subscription program, the magazine publisher receives from customers $45,000, which it credits to Advances from Customers. The estimated

> The perpetuity with growth formula involves several assumptions. Which one seems least plausible?

> Both the installment method and the cost recovery method recognize revenue when a firm collects cash. Why, then, does the pattern of income (that is, revenues minus expenses) over time differ under these two methods?

> Construction companies often use the percentage-of-completion method. Why doesn’t a typical manufacturing firm use this method of income recognition?

> Exhibit 6.12 in Chapter 6 provides a simplified statement of cash flows. For each of the transactions that follow, indicate the number(s) of the line(s) in Exhibit 6.12 affected by the transaction and the amount and direction (increase or decrease) of th

> Exhibit 15.9 presents the changes in common shareholders’ equity of Monk Corporation for 2013 through 2015. Monk regularly purchases shares of its common stock and reissues them in connection with stock option plans. It will usually iss

> Exhibit 15.8 presents a portion of the statement of changes in shareholders’ equity for Busch Corporation for 2013. Prepare journal entries for each of the eight transactions listed in Exhibit 15.8. Record the effect of items affecting

> Diversified Technologies opened for business on January 1, 2013. Sales on account during 2013 were $126,900. Collections from customers from sales on account during 2013 were $94,300. Diversified Technologies estimates that it will ultimately not collect

> Exhibit 15.7 presents a portion of the statement of changes in shareholders’ equity for Sirens, Inc., for 2013. Prepare journal entries for each of the six listed transactions in Exhibit 15.7. Transactions (4) and (5) were not with empl

> Exhibit 15.6 reproduces a portion of the statement of changes in shareholders’ equity for Microtel Corporation for 2013. When Microtel repurchases its common stock, it cancels the outstanding shares. Prepare journal entries for each of

> Pramble Company grants stock options to its managerial employees on December 31 of each year. Employees may acquire one share of common stock with each stock option. Pramble sets the exercise price equal to the market price of its common stock on the dat

> Lowen Corporation grants stock options to its managerial employees on December 31 of each year. Employees may acquire one share of common stock with each stock option. Lowen sets the exercise price equal to the market price of its common stock on the dat

> Shea Company began business on January 1. Its balance sheet on December 31 contained the shareholders’ equity section shown in Exhibit 15.3. During the year, Shea Company engaged in the following transactions: (1) Issued shares for $30

> Fisher Company began business on January 1. Its balance sheet on December 31 contained the shareholders’ equity section in Exhibit 15.2. During the year, Fisher Company engaged in the following transactions: (1) Issued shares for $15 ea

> The following events relate to shareholders’ equity transactions of Wilson Supply Company during the first year of its existence. Present journal entries for each of the transactions. a. January 2: The firm files articles of incorporation with the State

> Prepare journal entries to record the issuance of capital stock in each of the following independent cases. You may omit explanations for the journal entries. A firm does the following: a. Issues 20,000 shares of $10 par value common stock in the acquisi

> Prepare journal entries under U.S. GAAP to record the issuance of capital stock in each of the following independent cases. You may omit explanations for the journal entries. A firm does the following: a. Issues 50,000 shares of $5 par value common stock

> Ganton follows a policy of holding less than a 50% ownership interest in the corporations that bottle its beverages. Exhibit 14.17 presents selected balance sheet data for Ganton and for its bottling affiliates on December 31, 2013. The first column show

> Abson Corporation began business on January 1, 2013, selling copiers. It also sells service contracts to maintain and repair copiers for $600 per year. When a customer signs a service contract, Abson collects the $600 fee and credits Service Contract Fee

> The first two columns of Exhibit 14.16 present information from the accounting records of Parent Company and Sub Company on December 31 of the current year. Parent Company acquired 80% of the common stock of Sub Company on January 1 of the current year f

> The first two columns of Exhibit 14.14 present information from the accounting records of Peak Company and Valley Company on December 31 of the current year. Peak Company acquired 100% of the common stock of Valley Company on January 1 of this year for $

> The first two columns of Exhibit 14.13 present information from the accounting records of Company P and Company S on December 31, 2014. Company P acquired 100% of the common stock of Company S on January 1, 2013, Exhibit 14.13: when the balance in Co

> The first two columns of Exhibit 14.12 present information from the accounting records of Ely Company and Sims Company at the end of the current year. Ely Company acquired 100% of the common stock of Sims Company Exhibit 14.12: on January 1 of the cur

> Avery Corporation issues a note payable on January 1, 2013, to a supplier in return for equipment. The note has a face value of $50,000 and bears interest at a variable interest rate; the variable interest rate is 6% on January 1, 2013. Interest is payab

> Sandretto Corporation issues a note payable on January 1, 2013, to a supplier in return for equipment. The note has a face value of $50,000 and bears interest at 6% each year. Interest is payable annually on December 31, and the note matures on December

> On July 1, 2013, Owens Corporation places an order with a European supplier for manufacturing equipment for delivery on June 30, 2014. The purchase is denominated in euros in the amount of €60,000. Owens Corporation purchases a forward c

> Refer to Examples 15 and 19 in the chapter. Delmar holds 10,000 gallons of whiskey in inventory on October 31, 2013, that costs $225 per gallon. Delmar contemplates selling the whiskey on March 31, 2014. Uncertainty about the selling price of whiskey on

> Shiraz Company wants to raise $50 million cash but, for various reasons, does not want to do so in a way that results in a newly recorded liability. It is sufficiently solvent and profitable that its bank will lend up to $50 million at the prime interest

> Exhibit 12.24 presents information from the income tax note of Dime Store, a discount retailer, for its fiscal years ending January 31, 2013, 2012, and 2011. Dime Store applies U.S. GAAP. a. Present the journal entry to recognize Dime Storeâ€&

> Morrison’s Cafeteria sells coupons that customers may use later to purchase meals. Each coupon book sells for $25 and has a face value of $30; that is, the customer can use the book to purchase meals with menu prices of $30. On January

> Indicate the accounting principle or procedure apparently used to record each of the following independent transactions. Also, describe the transaction or event recorded in each case.

> Exhibit 12.23 presents information from the income tax note to the financial statements for E-Drive, a European computer manufacturer, for the years ending December 31, 2013, 2012, and 2011. E-Drive applies IFRS. a. Present the journal entry to recognize

> Exhibit 12.22 presents selected information from the notes to the financial statements of Catiman Limited, a manufacturer of farming equipment, for the years ending October 31, 2013, 2012, and 2011. Catiman applies U.S. GAAP. a. Present the journal entr

> Exhibits 12.20 and 12.21 present selected information from the notes to the financial statements of Tread away, Inc., a tire manufacturing company, regarding its U.S. pension and health care retirement plans. a. Refer to Exhibit 12.20. Why does the inter

> Exhibits 12.18 and 12.19 present selected information from the notes to the financial statements of Juicy-Juice, a U.S. based beverage company, regarding its pension and health care retirement plans. a. What is the likely reason for the actuarial gains i

> Lewis Corporation sold certain timber assets and received cash and notes receivable from the purchaser. Lewis then engaged in a transaction to convert the notes receivable into cash without recognizing a liability on the balance sheet. Exhibit 12.17 pres

> GSB Corporation issued semiannual coupon bonds with a face value of $110,000 several years ago. The annual coupon rate is 8%, with two coupons due each year, six months apart. The historical market interest rate was 10% compounded semiannually when GSB C

> Excerpts from the notes to the financial statements of Northern Airlines for two recent years reveal the following (amounts in millions). Northern Airlines uses the current/old rules of accounting for its leases. Future minimum commitments under leases

> Carom Sports Collectibles Shop plans to acquire, as of January 1, 2013, a computerized cash register system that costs $100,000 and has a five-year life and no salvage value. The company considers two plans for acquiring the system: (1) Outright purchase

> IBM manufactures a particular computer for $6,000 and sells it for $10,000. Adair Corporation needs this computer in its operations and contemplates three ways of acquiring it on January 1, 2013. The computer has a three year estimated useful life and ze

> Exhibit 11.15 presents excerpts from the notes to the financial statements of Home Supply Company. a. The amounts shown for Debentures, Notes, and the Medium-Term Notes appear as the same amounts on February 1, 2012 and 2013. What is the likely interpret

> Assume that Lentiva Group Limited provided the following description of its revenue recognition policies in the notes to its financial statements. ■ Lentiva recognizes revenue from the sale of goods (such as sales of hardware and software) when it effect

> Exhibit 11.14 presents a bond table for 8%, semiannual bonds for various market yields and years to maturity. Don’t overlook that this table presents values for semiannual coupon bonds, the most usual kind. The amounts in the table give

> When Time Warner Inc. announced its intention to borrow about $500 million by issuing 20-year zero coupon (single payment) notes, The Wall Street Journal reported the following: New York—Time Warner announced an offering of debt that could yield the comp

> The notes to the financial statements of Aggarwal Corporation for 2013 reveal the following information with respect to long-term debt. All interest rates in this problem assume semiannual compounding and the effective interest method of amortization usi

> Exhibit 10.4 presents a partial balance sheet for HP3, a creator and manufacturer of computer hardware and software and related services, for its fiscal years ending October 31, 2012 and 2013. a. HP3 uses the straight-line method to depreciate its buildi

> The notes to the financial statements of Bayer Group, a German pharmaceutical company, report a balance of €154 million for Restructuring Provisions on December 31; for the prior year, the ending balance in this liability account was €196 million. During

> Assume that Central Appliance sells appliances, all for cash. It debits all acquisitions of appliances during a year to the Merchandise Inventory account. The company provides warranties on all its products, guaranteeing to make required repairs, within

> Refer to the information in Problem 40 concerning Sedan Corporation’s inventory for the years ended March 31, 2013 and 2012. The notes to Sedan’s financial statements for the year ended March 31, 2013, state that some

> Wilson Company sells chemical compounds made from expensium. The company has used a LIFO inventory flow assumption for many years. The inventory of expensium on December 31, 2012, comprised 4,000 pounds from 2003 through 2012 at prices ranging from $30 t

> Burch Corporation began a merchandising business on January 1, 2010. It acquired merchandise costing $100,000 in 2010, $125,000 in 2011, and $135,000 in 2012. Information about Burch Corporation’s inventory as it would appear on the bal

> Hanover Oil Products (HOP) operates a gasoline outlet. It commenced operations on January 1. It prices its gasoline at 10% above its average purchase price for gasoline. Purchases of gasoline during January, February, and March appear next: Sales for e

> Marks and Spencer Group, Plc., a U.K. retailer, applies IFRS and reports its results in millions of pounds sterling (£). The notes to its financial statements provide the following information: ■ Revenue comprises sales of goods to customers less an appr

> Burton Corporation commenced retailing operations on January 1, 2011. Purchases of merchandise inventory during 2011 and 2012 appear next: Burton Corporation sold 1,000 units during 2011 and 1,500 units during 2012. a. Calculate the cost of goods sold

> Good Luck Brands reported a carrying value of its total inventory as of December 31, 2013, of $2,047.6 million; the corresponding figure for December 31, 2012, was $1,937.8. Good Luck Brands applies U.S. GAAP and reports its results in millions of U.S. d

> The Minevik Group is a Swedish-based, high-technology engineering firm. It follows IFRS and reports its results in millions of Swedish kronor (SEK). For the years ended December 31, 2013 and 2012, Minevik reported the following information pertaining to