Question: Financial statements for Pam and Sun Corporations

Financial Statements for Pam and Sun Corporations for 2016 are summarized as follows (in thousands):

Pam owns 90,000 shares of Sun’s outstanding voting common stock at December 31, 2016. These shares were acquired in two lots as follows:

The stockholders’ equity of Sun at year-end 2014, 2015, and 2016 was as follows (in thousands):

Sun’s net income for 2016 is $90,000, earned proportionately throughout the year, and its quarterly dividends of $12,500 are declared on March 15, June 15, September 15, and December 15. (Quarterly dividends of $12,500 include dividends on common stock and preferred stock.) There are no intercompany receivables or payables at December 31, 2016, and there have been no intercompany transactions other than dividends.

REQUIRED:

Prepare a consolidation workpaper for Pam and Subsidiary for 2016.

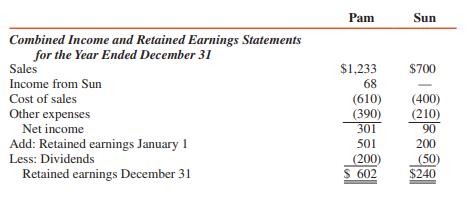

Transcribed Image Text:

Pam Sun Combined Income and Retained Earnings Statements for the Year Ended December 31 Sales $1,233 $700 Income from Sun 68 Cost of sales (610) (390) 301 (400) (210) 90 Other expenses Net income Add: Retained earnings January 1 Less: Dividends 501 200 (200) S 602 (50) $240 Retained earnings December 31 Pam Sun Balance Sheet at December 31 Cash $ 191 $ 50 Other current assets 200 300 Plant assets-net 900 600 Investment in Sun 711 Total assets $2,002 $950 Current liabilities S 200 $ 60 $10 preferred stock Common stock 100 500 50 240 1,200 Other paid-in capital Retained earnings Total equities 602 $2,002 $950

> State in your own words what Little's Law means. Think of an example that you have observed where Little's Law applies.

> Retrieving money from a mechanical slot machine is referred to as the drop process. The drop process begins with a security officer and the slot drop team leader obtaining the slot cabinet keys from the casino cashier’s cage. Getting the keys takes abou

> An engineering firm retains a technical specialist to assist four design engineers working on a project. The help that the specialist gives engineers ranges widely in time consumption. The specialist has some answers available in memory, others require c

> Here is a network with the activity times shown in days: a. Find the critical path. b. The following table shows the normal times and the crash times, along with the associated costs for each activity. If the project is to be shortened by four days, s

> What are the three general factors that determine the fit of a new or revised service process?

> What is the term used to refer to the physical surroundings in which service operations occur and how these surroundings affect customers and employees?

> What are the underlying assumptions of minimum-cost scheduling? Are they equally realistic?

> For each of the following variables, explain the differences (in general) as one moves from a work center to an assembly line environment. a. Throughput time (time to convert raw material into product) b. Capital/labor intensity c. Bottlenecks

> The product–process matrix is a convenient way of characterizing the relationship between product volumes (one-of-a-kind to continuous) and the processing system employed by a firm at a particular location. Characterize the nature of th

> How would you characterize the most important difference for the following issues when comparing a workcenter (job shop) and an assembly line? Issue Workcenter (Job Shop) Assembly Line Number of setups/job changeovers Labor content of product Flexib

> The Goodparts Company produces a component that is subsequently used in the aerospace industry. The component consists of three parts (A, B, and C) that are purchased from outside and cost 40, 35, and 15 cents per piece, respectively. Parts A and B are a

> A firm is selling two products—chairs and bar stools—each at $50 per unit. Chairs have a variable cost of $25, and bar stools $20. The fixed cost for the firm is $20,000. a. If the sales mix is 1:1 (one chair sold for every bar stool sold), what is the b

> Assume a fixed cost of $900, a variable cost of $4.50, and a selling price of $5.50. a. What is the break-even point? b. How many units must be sold to make a profit of $500.00? c. How many units must be sold to average $0.25 profit per unit? $0.50 profi

> A book publisher has fixed costs of $300,000 and variable costs per book of $8.00. The book sells for $23.00 per copy. a. How many books must be sold to break even? b. If the fixed cost increased, would the new break-even point be higher or lower? c. If

> What term is used to mean manufacturing designed to achieve high customer satisfaction with minimum levels of inventory investment?

> Dell Computers’ primary consumer business takes orders from customers for specific configurations of desktop and laptop computers. Customers must select from a certain model line of computer, and choose from available parts, but within those constraints

> Which characteristics must a project have for critical path scheduling to be applicable? What types of projects have been subjected to critical path analysis?

> What is it about service processes that makes their design and operation so different from manufacturing processes?

> Pop Corporation is the primary beneficiary in a VIE, even though Pop owns only 10 percent of the outstanding voting shares. In the year following the initial consolidation, the VIE earns net income of $2,000,000. Included in income is a fee paid by Pop f

> Sun Corporation is a corporate joint venture that is jointly controlled and operated by five investor-venturers, four with 15 percent interests each and one with a 40 percent interest. Each of the five venturers is active in venture management. Land sale

> On January 1, 2016, Pam Corporation acquired a 90 percent interest in Sun Corporation for $1,260,000. The book values and fair values of Sun’s assets and equities on this date are as follows (in thousands): REQUIRED: 1. Prepare the jo

> Pop Corporation acquired an 80 percent interest in Son Company at book value a number of years ago. Separate incomes of Pop and Son for 2016 were $120,000 and $60,000, respectively. The only transactions between Pop and Son during 2016 were as follows:

> Pam Company acquired an 80 percent interest in Sun Corporation at book value equal to fair value on January 1, 2016. During the year, Sun sold $50,000 inventory items to Pam, and at December 31, 2016, unrealized profits amounted to $15,000. Separate inco

> Son Corporation’s recorded assets and liabilities are equal to their fair values on July 1, 2017, when Pop Corporation purchases 36,000 shares of Son common stock for $900,000. Identifiable net assets of Son on this date are $855,000, and Son’s stockhold

> On January 1, 2017, Pam Corporation pays $600,000 for an 80 percent interest in Sun Company, when Sun’s net assets have a book value of $550,000 and a fair value of $700,000. The $150,000 excess fair value is due to undervalued equipment with a five-year

> Balance sheet information of Pop and Son Corporations at December 31, 2015, is summarized as follows (in thousands): On January 2, 2016, Pop purchases 80 percent of Son’s outstanding shares for $500,000 cash. REQUIRED: 1. Determine g

> Do investments in nonconsolidated subsidiaries and 20 to 50 percent–owned investees affect the nature of the investor’s EPS calculations?

> How does controlling share of consolidated earnings per share differ from parent earnings per share?

> Pan Corporation owns an 80 percent interest in Sol Company and Sol owns a 30 percent interest in Pan, both acquired at a fair value equal to book value. Separate incomes (not including investment income) of the two affiliates for 2016 are: Pan..........

> Describe the computation of noncontrolling interest share for an 80 percent–owned subsidiary with both preferred and common stock outstanding.

> Refer to the information in question 1. Assume that Son pays two years’ preferred dividend requirements during the current year. Would this affect your computation of Pop’s investment income for the current year? If so, recompute Pop’s investment income.

> When do unrealized and constructive gains and losses create temporary differences for a consolidated entity?

> Does a parent/investor provide for income taxes on the undistributed earnings of a subsidiary by adjusting investment and investment income accounts? Explain.

> Describe the nature of the tax effect of temporary differences that arise from use of the equity method of accounting.

> Some or all of the dividends received by a corporation from domestic affiliates may be excluded from federal income taxation. When are all of the dividends excluded?

> Can a consolidated entity that is classified as an “affiliated group” under the IRS code elect to file separate tax returns for each affiliate?

> Are consolidated income tax returns required for all consolidated entities? Discuss.

> It may be necessary to compute the earnings per share for subsidiaries and equity investees before parent (and consolidated) earnings per share can be determined. When are the subsidiary EPS computations used in calculating parent earnings per share?

> Under what conditions will the procedures used in computing a parent’s EPS be the same as those for a company without equity investments?

> Pat Corporation owns an 80 percent interest in Sam Corporation and a 70 percent interest in Ten Corporation. Ten owns a 10 percent interest in Sam. These investment interests were acquired at fair value equal to book value. The net incomes of the affilia

> Potentially dilutive securities of a subsidiary may be converted into parent common stock or subsidiary common stock. Describe how these situations affect the parent’s EPS procedures.

> How should preferred stock of a subsidiary be shown in a consolidated balance sheet in each case? a. If it is held 100 percent by the parent b. If it is held 50 percent by the parent and 50 percent by outside interests c. If it is held 100 percent by out

> Son Corporation has 100,000 outstanding shares of $10 par common stock and 5,000 outstanding shares of $100 par, cumulative, 10 percent preferred stock. Son’s net income for the year is $300,000, and its stockholders’ equity at year-end is as follows: 1

> What are the primary advantages of filing a consolidated tax return?

> In computing diluted earnings for a parent, it may be necessary to replace the parent’s equity in subsidiary’s realized income with the parent’s equity in the subsidiary’s diluted earnings. Does this replacement calculation involve unrealized profits tha

> What are the required disclosures related to EPS calculations when preparing consolidated financial statements?

> Your CEO called you into his office to discuss an article he had read over the weekend. The article stated that the FASB had changed accounting for deferred taxes such that all deferred tax assets and liabilities would be treated as noncurrent items. The

> Pam Corporation has $108,000 income from its own operations for 2016, and $42,000 income from Sun Corporation, its 70 percent–owned subsidiary. Sun’s net income of $60,000 consists of $66,000 operating income less $6,000 net-of-tax interest on its outsta

> Pop Corporation acquired an 80 percent interest in Son Corporation common stock for $240,000 on January 1, 2015, when Son’s stockholders’ equity consisted of $200,000 common stock, $100,000 preferred stock, and $25,000

> The affiliation structure for a group of interrelated companies is diagrammed as follows: The investments were acquired at fair value equal to book value in 2016, and there are no unrealized or constructive profits or losses. Separate incomes and divid

> Pop Corporation acquired 80 percent of Son Corporation’s preferred stock for $175,000 and 90 percent of Son’s common stock for $630,000 on July 1, 2016. Son’s stockholders’ equity on December 31, 2016, was as follows (in thousands): Stockholders’ Equity

> Pam Corporation paid $7,200,000 for 360,000 shares of Sun Corporation’s outstanding voting common stock on January 1, 2016, when the stockholders’ equity of Sun consisted of (in thousands): 10% cumulative, preferred stock, $100 par. Liquidation.........

> On January 3, 2016, Pam Corporation purchased a 90% interest in Sun Corporation at a price $120,000 in excess of book value and fair value. The excess is goodwill. During 2016, Pam sold inventory items to Sun for $100,000, and $15,000 in profit from the

> The pretax operating incomes of Pop Corporation and Son Corporation, its 70 percent–owned subsidiary, for 2016 are as follows (in thousands): ADDITIONAL INFORMATION: 1. Pop received $280,000 dividends from Son during 2016. 2. Goodwill

> Pop Corporation acquired all the stock of Son Corporation on January 1, 2016, for $280,000 cash, when the book values and fair values of Son’s assets and liabilities were as follows (in thousands): Son’s buildings ha

> Pam Corporation acquired a 90 percent interest in Sun Corporation in a taxable transaction on January 1, 2016, for $900,000, when Sun had $500,000 capital stock and $400,000 retained earnings. The $100,000 excess cost over book value is due to goodwill.

> Taxable incomes for Pop Corporation and Son Corporation, its 70 percent–owned subsidiary, for 2016 are as follows (in thousands): ADDITIONAL INFORMATION: 1. Pop acquired its interest in Son at a fair value equal to book value on Decem

> Pam Corporation paid $1,155,000 cash for a 70 percent interest in Sun Corporation’s outstanding common stock on January 2, 2016, when the equity of Sun consisted of $1,000,000 common stock and $600,000 retained earnings. The excess fair

> Pop Corporation and its 100 percent–owned subsidiary, Son Corporation, are members of an affiliated group with pretax accounting incomes as follows (in thousands): The gain reported by Pop relates to land sold to Son during the curren

> Pam Corporation’s net income for 2016 consists of the following: ADDITIONAL INFORMATION: 1. Pam has 100,000 shares of common stock, and Sun has 50,000 shares of common and 10,000 shares of $10 cumulative, convertible, preferred stock

> Pet Company owns 90 percent of the stock of Man Corporation and 70 percent of the stock of Nun Company. Man owns 70 percent of the stock of Oak Corporation and 10 percent of the stock of Nun Company. Nun Company owns 20 percent of the stock of Oak Corpor

> Pop Company owns 40,000 of 50,000 outstanding shares of Son Company, and during 2016, it recognizes income from Son as follows: Share of Son net income ($500,000 × 80%)............................ $ 400,000 Patent amortization...........................

> Pam Corporation owns 80 percent of Sun Corporation’s outstanding common stock. The 80 percent interest was acquired in 2016 at $40,000 in excess of book value due to undervalued equipment with an eight-year remaining useful life. Outsta

> Pop Corporation owns an 80 percent interest in Son Corporation. Throughout 2016, Pop had 20,000 shares of common stock outstanding. Son had the following securities outstanding: â– 10,000 shares of common stock â– Option

> 1. A parent company and its 100 percent–owned subsidiary have only common stock outstanding (10,000 shares for the parent and 3,000 shares for the subsidiary), and neither company has issued other potentially dilutive securities. The equation to compute

> Pam Corporation purchased 60 percent of Sun Corporation’s outstanding preferred stock for $6,500,000 and 70 percent of its outstanding common stock for $35,000,000 on January 1, 2017. Sun’s stockholders’ equity on December 31, 2016, consisted of the foll

> The stockholders’ equity of Son Corporation on December 31, 2016, was as follows (in thousands): 15% preferred stock, $100 par, cumulative, nonparticipating, with..............$1,000 one year’s dividends in arrears Common stock, $10 par.................

> Pam Corporation owns 80 percent of Sun Corporation’s common stock, having acquired the interest at a fair value equal to book value on December 31, 2016. During 2017, Pam’s separate income is $6,000,000 and Sun Corpora

> The stockholders’ equity of Son Corporation at December 31, 2015, was as follows (in thousands): 12% preferred stock, cumulative, nonparticipating,............................ $1,200 $100 par, callable at $105 Common stock, $10 par......................

> The stockholders’ equity of Sun Corporation at December 31, 2016, was as follows (in thousands): 10% cumulative preferred stock, $100 par, callable at $105,..................... $2,000 20,000 shares issued and outstanding, with one year’s dividends in a

> 1. During 2017, Pop Corporation owns 20 percent of Son Corporation’s preferred stock and 80 percent of its common stock. Son’s stock outstanding on December 31, 2017, is as follows: 10% cumulative preferred stock.....

> Pal Corporation owns 80 percent each of the voting common stock of Sal and Tea Corporations. Sal owns 60 percent of the voting common stock of Won Corporation and 10 percent of the voting stock of Tea. Tea owns 70 percent of the voting stock of Val and 1

> Pop Corporation recognizes a deferred tax asset (benefit) of $150,000 related to its acquisition of Son Company. Pop has determined that the tax position qualifies for recognition and should be measured. Pop has determined the amounts and the probabiliti

> Pam Corporation recognizes a deferred tax asset (benefit) of $1,000,000 related to its acquisition of Sun Company. Pam has determined that the tax position qualifies for recognition and should be measured. Pam has determined the amounts and the probabili

> Son Corporation, an 80 percent–owned subsidiary of Pop Corporation, sold equipment with a book value of $600,000 to Pop for $1,000,000 at December 31, 2016. Separate income tax returns are filed, and a 34 percent income tax rate is applicable to both Pop

> Sun Corporation is a 100 percent–owned subsidiary of Pam Corporation. During the current year, Pam sold merchandise that cost $200,000 to Sun for $400,000. A 34 percent income tax rate is applicable, and 80 percent of the merchandise remains unsold by Su

> Pop Corporation and its 70 percent–owned subsidiary, Son Corporation, have pretax operating incomes for 2016 as follows (in thousands): Pop received $280,000 dividends from Son during 2016. A previously unrecorded patent from Pop&acir

> The pretax accounting incomes of Pam Corporation and its 100 percent–owned subsidiary, Sun Company, for 2016 are as follows (in thousands): The only intercompany transaction during 2016 was a gain on land sold to Sun. Assume a 34 perc

> 1. When Pop Corporation acquired its 100 percent interest in Son Corporation in a tax-free reorganization, Son’s equipment had a fair value of $12,000,000 and a book value and tax basis of $8,000,000. If Pop’s effective tax rate is 34 percent, how much o

> 1. Income taxes are currently due on intercompany profits when: a Profits originate from upstream sales b Separate-company tax returns are filed c Consolidated tax returns are filed d Affiliates are accounted for as consolidated subsidiaries 2. The righ

> Pow Corporation owns an 80 percent interest in Soy Corporation. Pow does not have common stock equivalents or other potentially dilutive securities outstanding, so it calculated its EPS for 2016 as follows: An examination of Pow’s inc

> The income statements of Pop Corporation and its 80 percent–owned subsidiary, Son Corporation, for 2016 are as follows: Note: Income from Son is computed as [($26,400 reported income × 80%) - $2,000 patent amortization -$

> The affiliation structure for Pin Corporation and its subsidiaries is as follows: Separate incomes of Pin, Son, and Tan Corporations for 2016 are $360,000, $160,000, and $100,000, respectively. 1. The equation for determining Pin’s i

> The following information is available regarding Pam Corporation and its 80 percent–owned subsidiary, Sun Corporation, at and for the year ended December 31, 2016: REQUIRED: Determine consolidated earnings per share (both basic and di

> Pop Corporation’s net income for 2016 is $316,000, including $160,000 income from Son Corporation, its 80 percent– owned subsidiary. The income from Son consists of $176,000 equity in income less $16,000 patent amortization. Pop has 300,000 shares of $10

> In using the schedule approach for allocating income of subsidiaries to controlling and noncontrolling stockholders in an indirect holding affiliation structure, why is it necessary to begin with the lowest subsidiary in the affiliation tier?

> P owns a 60 percent interest in S, and S owns a 40 percent interest in T. Should T be consolidated? If not, how should T be included in the consolidated statements of P and Subsidiaries?

> If companies in an affiliation structure account for investments on an equity basis, how can noncontrolling interests be determined without the use of simultaneous equations?

> How do consolidation procedures for mutual holdings involving the father-son-grandson type of affiliation structure differ from those for mutually held parent stock?

> What is the right of offset rule? How does it affect the amount to be distributed to partners in liquidation?

> If a partnership is insolvent, how is the amount of cash distributed to individual partners determined?

> How do safe payments computations affect partnership ledger account balances?

> What assumptions are made in determining the amount of distributions (or safe payments) to individual partners prior to the recognition of all gains and losses on liquidation?

> UPA specifies a priority ranking for distribution of partnership assets in liquidation. What is the ranking?

> What is simple partnership liquidation, and how are distributions to partners computed?

> How does partnership liquidation differ from partnership dissolution?

> P’s separate earnings are $100,000, and S’s separate earnings are $40,000. P owns an 80 percent interest in S, and S owns a 10 percent interest in P. What is the controlling share of consolidated net income?

> When all partnership assets have been distributed in the liquidation of a partnership, some partners may have debit capital balances and others may have credit capital balances. How are such balances eliminated if the partners with debit balances are per

> What are vulnerability ranks? How are they used in the preparation of cash distribution plans for partnership liquidations?

> A partnership in liquidation has satisfied all of its nonpartner liabilities and has cash available for distribution to partners. Under what circumstances would it be permissible to divide available cash in the profitand loss-sharing ratios of the partne