Question: Following is the corporate governance report of

Following is the corporate governance report of Honda Motor Company included in its 2009 Annual Report.

1. Basic Stance Regarding corporate governance

Based on its fundamental corporate philosophy, the Company is working to enhance corporate governance as one of its most important management issues. Our aim is to have our customers and society, as well as our shareholders and investors, place even greater trust in us and to ensure that Honda is “a company that society wants to exist.â€

To ensure objective control of the Company’s management, outside directors and outside corporate auditors are appointed to the Board of Directors and the Board of Corporate Auditors, which are responsible for the supervision and auditing of the Company. Honda has also introduced an operating officer system, aimed at strengthening both the execution of business operations at the regional and local levels and making management decisions quickly and appropriately. The term of office of each director is limited to one year, and the amount of remuneration payable to them is determined according to a standard that reflects their performance in the Company. Our goal in doing this is to maximize the flexibility with which our directors respond to changes in the operating environment.

With respect to business execution, Honda has established a system for operating its organizational units that reflects its fundamental corporate philosophy. For example, separate headquarters have been set up for each region, business, and function, and a member of the Board of Directors or an operating officer has been assigned to each headquarters and main division. In addition, by having the Executive Council and regional operating boards deliberate important matters concerning management, the Company implements a system that enables swift and appropriate decision making.

With respect to internal control, compliance systems and risk management systems have been designed and implemented appropriately following the basic policies for the design of internal controls decided by the Board of Directors.

To enhance even further the trust and understanding of shareholders and investors, Honda’s basic policy emphasizes the appropriate disclosure of Company information, such as by disclosing financial results on a quarterly basis and timely and accurately giving public notice of and disclosing its management strategies. Honda will continue raising its level of transparency in the future.

3. Internal Control System: Fundamental Position and Implementation Status

The Company is designing and implementing internal control systems in accordance with the following basic policies.

• Systems for Ensuring that the Execution of Duties by the Directors and Employees is in Compliance with the Law and the Company’s Articles of Incorporation

To secure compliance of Company management and employees with guidelines for conduct in conformity with applicable laws and internal rules and regulations, the Company has prepared The Honda Conduct Guidelines and implements measures to ensure that all management and employees are made aware of and follow these guidelines.

The Company has appointed a Compliance Officer, who is a director in charge of compliance-related initiatives. Other key elements of our compliance system include the Business Ethics Committee and the Business Ethics Improvement Proposal Line.

• Retention and Management of Information on Execution of Business by Directors

Minutes of the meetings of the Board of Directors and other important meetings as well as information related to the execution of business by the directors will be retained and stored appropriately following the policy for the retention and management of documents.

• Regulations and Other Systems for Management of the Contingencies of Losses

Important items related to management are proposed to the Board of Directors, the Executive Council, and/or Regional Operating boards, risks are assessed, and then, decisions are made, after due consideration according to established deliberation standards.

Regarding risks that are to be dealt with on a departmental basis, each department will work to prevent the emergence of such risk and develop policies for dealing with them. For large-scale disasters requiring Company-level crisis management, the Honda Crisis Response Rules will be applied,………………………………….

Required:

Based on the above,

a. Discuss the way in which Honda Motor Company attempted to establish a high level of corporate governance.

b. Explain the possible link between corporate governance and auditing.

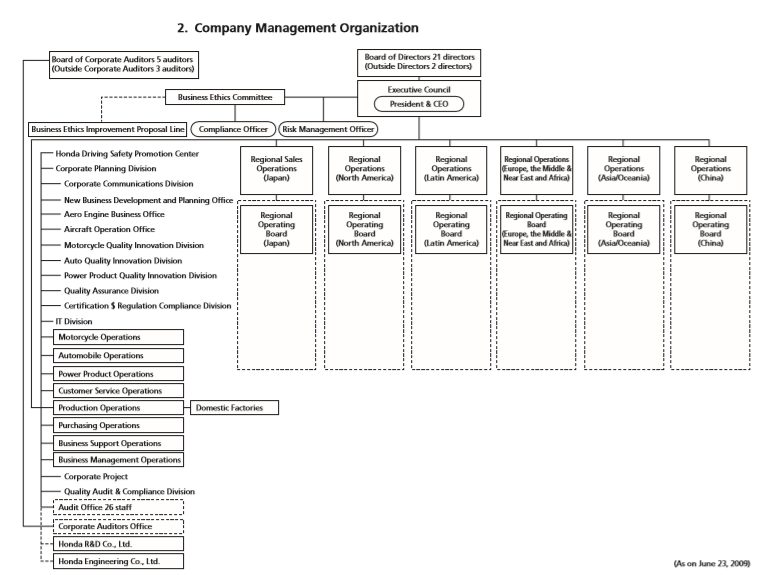

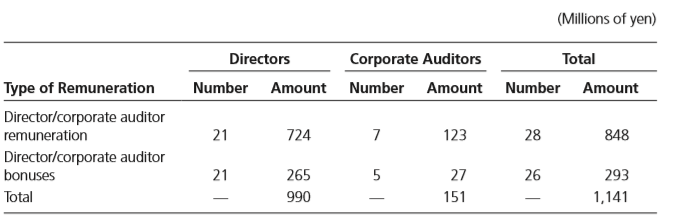

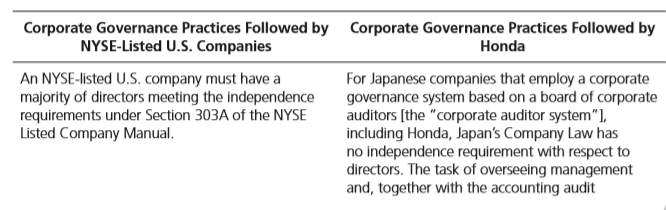

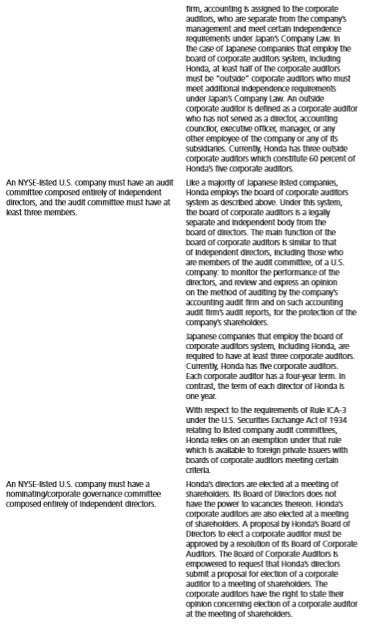

Transcribed Image Text:

2. Company Management Organization Board of Corporate Auditors 5 auditors (Outside Corporate Auditors 3 auditors) Board of Directors 21 directors (Outside Directors 2 directors) Executive Council Business Ethics Committee President & CEO Business Ethics Improvement Proposal Line Compliance Officer Risk Management Officer Honda Driving Safety Promotion Center Regional Sales Operations (Japan) Regional Operations (North Amerka) Regional Regional Operations Europe, the Middle & Near East and Africa) Regional Operations (AsialOceania) Regional Operations (China) Corporate Planning Division Operations (Latin America) Corporate Communications Division New Business Development and Planning Office Aero Engine Business Office Regional Орегrating Board Regional Operating Board (North America) Regional Operating Воard (Latin America) Regional Operating Board (AsialOceania) Regional Operating Board Regional Operating Board (China) Aircraft Operation Office Europe, the Middle i Near East and Africa) Motorcycle Quality Innovation Division (lapan) Auto Quality Innovation Division Power Product Quality Innovation Division Quality Assurance Division Certification $ Regulation Compliance Division IT Division Motorcycle Operations Automobike Operations Power Product Operations Customer Service Operations Production Operations Domestic Factories Purchasing Operations Business Support Operations Business Management Operations Сoгporate Projct Quality Audit & Compliance Division Audit Office 26 staff Corporate Auditors Office Honda R&D Co, Ltd. Honda Engineering Co, Ltd. (As on June 23, 2009) - -- (Millions of yen) Directors Corporate Auditors Total Type of Remuneration Number Amount Number Amount Number Amount Director/corporate auditor remuneration 21 724 7 123 28 848 Director/corporate auditor bonuses 21 265 5 27 26 293 Total 990 151 1,141 - - | Corporate Governance Practices Followed by Corporate Governance Practices Followed by NYSE-Listed U.S. Companies Honda An NYSE-listed U.S. company must have a majority of directors meeting the independence requirements under Section 303A of the NYSE Listed Company Manual. For Japanese companies that employ a corporate governance system based on a board of corporate auditors [the "corporate auditor system"], including Honda, Japan's Company Law has no independence requirement with respect to directors. The task of overseeing management and, together with the accounting audit firm, accounting B assigned to the corporate auditors, who are separate from the companys management and meet certan Independence requirements under lapans Company Law. In the case of lapanese companies that employ the board of corporate auditors system, induding Honda, at least half of the corporate auditors must be "outside" corporate auditors who must meet additional independence requirements under lapans Company Law. An outside corporate auditor is defined as a corporate auditor who has not sered as a director acCounting Councior, executive office, manager, or any other employee of the company or any of its subsidianies. Currently, Honda has three outside corporate auditors which constitute 60 percent of Honda's five corporate auditors. An NYSE-Isted U.S. company must have an audit Uke a majority of Japanese Iisted companies, Honda employs the board of corporate auditors directors, and the audit committee must have at system as described above. Under this system, the board of corporate auditors is a egaly separate and independent body from the board of directors. The main function of the committee composed entirely of Independent kast three members. board of corporate auditors s similar to that of Independent directors, Including those who are members of the audit committee, of a US. company: to monitor the performance of the directors, and review and express an opinion on the method of auditing by the companys accounting audit frm and on such acounting audit fims audit reports, for the protection of the company's shareholders. kapanese compankes that employ the board of corporate auditors system, Including Honda, are required to have at least three corporate auditors. Currentiy, Honda has five corporate auditoes. Each corporate auditor has a four year term. In contrast, the term of each director of Honda s one year With respect to the requirements of Rule CA3 under the US. Securities Exchange Act of 1934 relating to Iisted company audit commitees, Honda reles on an exemption under that rule which is avallable to foreign private ksuers with boards of corporate auditors meeting certaln ariterta. An NYSE-Isted U.S. company must have a nominatingcorporate governance committee composed entirely of Independent directors. Honda's directors are elected at a meeting of shareholders. Its Board of Directors does not have the power to vacandes thereon. Honda's corporate auditors are atso elected at a meeting of shareholders. A proposal by Hondas Board of Directors to elect a corporate auditor must be approved by a resolution of its Board of Corporate Auditors. The Board of Corporate Auditors S empowered to request that Hondas directors submit a proposal for election of a corporale auditor to a meeting of shareholders. The corporate auditors have the nght to state their opnion concerning election of a corporate auditor at the meeting of shareholders An NYSE-listed U.S. company must have a compensation committee composed entirely of independent directors. Maximum total amounts of compensation for Honda directors and corporate auditors are proposed to, and voted on, by a meeting of shareholders. Once the proposals for such maximum total amounts of compensation are approved at the meeting of shareholders, each of the Board of Directors and Board of Corporate Auditors determines the compensation amount for each member within the respective maximum total amounts. An NYSE-listed U.S. company must generally obtain shareholder approval with respect to any equity compensation plan. Currently, Honda does not adapt stock option compensation plans. When it does, Honda must obtain shareholder approval for stock options only if the stock options are issued with specifically favorable conditions or price concerning the issuance and exercise of the stock options.

> Moser International, a U.S. corporation, acquired a 100% interest in Gilmore Enterprises, a foreign corporation, which manufactures avionic components. Although Gilmore accounts for its activity using foreign currency A (FCA), it has been determined that

> On October 1, 2013, Kemper International acquired a 90% interest in the equity of Spruco Manufacturing when the subsidiary’s equity was 8,000,000 foreign currency (FC), including retained earnings with a balance of 3,000,000 FC. Kemper

> Due to increasing pressures to expand globally, Pueblo Corporation acquired a 100% interest in Sorenson Company, a foreign company, on January 1, 2016. Pueblo paid 12,000,000 FC, and Sorenson’s equity consisted of the following: Common

> On January 1, one U.S. dollar can be exchanged for eight foreign currencies (FC). The dollar can be invested short term at a rate of 4%, and the FC can be invested at a rate of 5%. 1. Calculate the direct and indirect spot exchange rates as of January 1.

> WTC Manufacturing, Inc., has an 80% interest in a foreign subsidiary, Mofoco Manufacturing. Relevant details regarding WTC’s investment in Mofoco are as follows: Date of acquisition. . . . . . . . . . . . . . . . . . . . . . . . . . .

> In order to demonstrate the use of the re measurement process, assume that at the beginning of the year a U.S. parent company invested 100,000 foreign currency B (FCB) to form a 100% owned subsidiary. The subsidiary immediately invested the foreign curre

> In the process of preparing a budget for the second quarter of the current fiscal year, Anderson Welding, Inc., has forecasted foreign sales of 1,200,00 foreign currency (FC). The company is concerned that the dollar will strengthen relative to the FC an

> On March 1, a company committed to acquire 10,000 units of inventory to be delivered on May 31. The purchase price is to be paid in foreign currency (FC) in the amount of 200,000 FC. Assume that the commitment’s negative values are $7,9

> Medical Distributors, Inc., is a U.S. company that buys and sells used medical equipment throughout the United States and Canada. During the month of June, the company had the following transactions with Canadian parties: 1. Purchased used equipment on J

> Kaiser Exporters buys used medical equipment and sells it to various foreign health care institutions. On June 15, the company committed to sell medical equipment to a foreign hospital for 800,000 FC. The equipment, with a cost of $325,000, was shipped t

> Jarvis Corporation transacts business with a number of foreign vendors and customers. These transactions are denominated in FC, and the company uses a number of hedging strategies to reduce the exposure to exchange rate risk. Several such transactions ar

> Hauser Corporation has $20,000,000 of outstanding debt that bears interest at a variable rate and matures on June 30, 2018. At inception of the debt, the company had a lower credit rating, and most available financing carried a variable rate. The company

> During the third quarter of the current year, Beamer Manufacturing Company invested in derivative instruments for a variety of reasons. The various investments and hedging relationships are as follows: a. Call Option A—This option was p

> Industrial Plating Corporation coats manufactured parts with a variety of coatings such as Teflon, gold, and silver. The company intends to purchase 100,000 troy ounces of silver in September. The purchase is highly probable, and the company has become c

> Williams Corporation imports, from a number of German manufacturers, large machining equipment used in the tooling industry. On June 1, the company received delivery of a piece of machinery with a cost of 450,000 euros when the spot rate was 1 euro equal

> Pasu International purchased a plant in Louisiana on December 31, 2015, and financed $20,000,000 of the purchase price with a 5-year note. The note bears interest at the fixed rate of 5%, and payments on the note are made quarterly in the amount of $1,13

> Clayton Industries sells medical equipment worldwide. On March 1 of the current year, the company sold equipment, with a cost of $160,000, to a foreign customer for 200,000 euros payable in 60 days. At the same time, the company purchased a forward contr

> Custom Brand Bakeries, Inc. (CBBI), located in Erie, Pennsylvania, bakes a variety of products for various parties on a contract basis. For example, a food company may contract with CBBI to make energy bars that are then sold under the food companyâ

> On March 17, Kennedy Baking, Inc., committed to buy 1,000 tons of commodity A for delivery in May at a cost of $118 per ton. Concerned that the price of commodity A might decrease, on March 29 the company purchased a May put option for 1,000 tons of comm

> Each of the following is an independent fact situation involving an extinguishment or restructuring of debt. Debt A—On January 1, 2015, the company borrowed $3,000,000 after incurring $100,000 of related debt issuance costs. The note had a term of three

> St. John Corporation is barely solvent and has been seeking an equity investor that would be interested in making a capital contribution so that the company would hopefully return to performance levels it had experienced in the past. At the end of the pr

> Matmart Corporation is contemplating seeking a voluntary liquidation under Chapter 7 of the Bankruptcy Reform Act. There are a large number of partially secured creditors who are opposed to the possibility of a liquidation and favor a restructuring of th

> Marshall Tool and Die Company has been experiencing significant foreign competition and a declining market. Annual net losses from operations have averaged $250,000 over the last three years. The company’s balance sheet as of December 3

> A partially completed statement of realization and liquidation is as follows: The following additional transactions have occurred through August 12 of the current year: a. Receivables collected amounted to $39,000. Receivables with a book value of $15,

> Casper Blueprinting, Inc., has filed under Chapter 7 of the Bankruptcy Code. The estimated net realizable value of its assets is as follows: Cash and cash equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. $ 23,

> A major cattle feeding operation has entered into a firm commitment to buy 100,000 bushels of corn to be delivered to its feed lot in Kansas. The corn is expected to be delivered in 90 days. The company is committed to pay $1.50 per bushel. If corn yield

> Peltzer Manufacturing is experiencing financial difficulties. Rather than entering into a lengthy bankruptcy proceeding, the company has reached an agreement with its long-term creditors to restructure various loans. The restructured loans are described

> Howard Manufacturing has two debts outstanding with a creditor. Howard is experiencing financial difficulties, and the creditor has granted a concession. Therefore, accounting for the debt in question qualifies as a troubled debt restructuring. At the da

> Ridgeway Builders, Inc., is in the residential construction industry and has been experiencing a business downturn. As a result of these economic conditions, the company is having difficulty serving its outstanding debt and is seeking relief outside of t

> Barber Technologies designs and develops software to be used for the management of inventory by both retailers and manufacturing firms. Over the past three years, the company has experienced significant competition and a declining market resulting in a s

> Frankton Corporation has experienced difficult financial times for the past five years resulting in serious cash flow problems, negative earnings, and increasing deficits in retained earnings. The negative cash flows from operations have been managed in

> Cutler Manufacturing manufactures and distributes specialty piping used in the construction industry. Due to the recent contraction in the commercial construction market, the company has had difficulty servicing its outstanding debt. In particular, debt

> Jason Jackson was killed in a mountain-climbing accident in British Columbia. As Jason’s trusted friend and CPA, you have been named executor of his estate and guardian to his minor child, Cody Jackson. Jason’s estate consists of the following assets sub

> Jack Mason is a single parent with three minor children. His will provides for the creation of a trust for the benefit of his three children. His entire net estate is to be placed into the trust, and the trustee is authorized to approve disbursements to

> Edith Leppert and her husband, Gerald Leppert, have net assets with market values of $4,300,000 and $2,400,000, respectively. The Lepperts have begun to do some estate tax planning and are developing various strategies based on the following assumptions:

> Charles Kamp, a divorced person, died in February of the current year with an estate consisting of assets valued at $7,008,000 and liabilities of $380,000. Charles’s will have contained the following provisions: a. Robert Sullivan would serve as executor

> On July 1, 2016, Hargrove Corporation issued a 2-year note with a face value of $4,000,000 and a fixed interest rate of 9%, payable on a semiannual basis. On January 15, 2017, the company entered into an interest rate swap with a financial institution in

> One of your clients has recently read about the goal of converging to International Accounting Standards and they are concerned about what impact it may have on their company. 1. Discuss some of the costs that a company might incur as part of its converg

> Sometimes an MNC may decide to use local currency to evaluate a foreign subsidiary. Required: Explain the circumstances under which it may be appropriate for an MNC to use local currency to evaluate a foreign subsidiary.

> It is impossible to separate the performance of a foreign subsidiary from that of its managers, and there is no need for it. Required: Critically comment on the preceding statement.

> There is no agreement internationally on how to address the issue of auditor liability. Required: Describe the approach taken in your own country in addressing the issue of auditor liability, and explain the rationale behind that approach.

> This chapter refers to the concept of accounting infrastructure, which encompasses the various environmental factors affecting the issues concerning auditing in a particular country. Required: Explain the environmental factors that affect the issues con

> Identify five key terms used in assessing the impact of climate change on a firm.

> Exhibit 15.10 provides an example of a company, Toyota, which has clearly stated its CSR policy in its annual report of 2010. Required: Identify another company which has stated its CSR policy in its 2012 annual report, and compare the main points highl

> The concept of the balanced scorecard is becoming increasingly popular among firms internationally. Required: Explain the possible reasons for the popularity of the balanced scorecard.

> Exhibit 15.7 provides an extract from the 2009 CSR report of a company in the IT industry, IBM Corporation. Required: Discuss the motivations for a company in another industry of your choice to prepare a CSR report, and identify the nature of the inform

> Exhibit 15.4 provides an example of an audit report of a Brazilian company for 2011, which refers to GRI-G3 sustainability guidelines. Required: Identify a 2012 audit report for a U.S. company which refers to GRI-G3 sustainability guidelines and compare

> The Corporate Responsibility Report 2010 of Coca-Cola Amatil Company is at http://ccamatil.com/InvestorRelations/AnnualReports/2009/2010%20 Sustainability%20Report.pdf. It mentions four global pillars. Required: Discuss the strategies, programs, and tar

> Following is the report of the Supervisory Board included in Daimler company’s 2009 Annual Report. REPORT OF THE SUPERVISORY BOARD Dear Shareholders, In eight meetings during the 2009 financial year, the Supervisory Board diligently fulfilled its duties

> What is the PCAOB? What is its role in audit regulation?

> What is audit quality? What determines audit quality in a given country?

> What determines the primary role of external auditing in a particular country?

> What are the provisions in the Sarbanes-Oxley Act 2002 and the New York Stock Exchange listing requirements that are aimed at improving corporate governance and are directly related to audit committees?

> What are the main differences between the OECD Principles of Corporate Governance issued in 1999 and the revised version issued in 2004?

> According to Exhibit 13.8 , the top-three budget goals for divisional managers of Japanese companies are sales volume, net profit, and production cost, in that order, whereas those of U.S. companies are return on investment, controllable profit, and net

> What is the oversight role of an audit committee?

> What are the main factors that complicate the issue of auditor independence?

> What are some of the strategies adopted internationally to limit the auditor’s liability?

> What determines whether or not to issue an unqualified audit opinion on the compliance of a set of financial statements with IFRS?

> What are the main benefits of international harmonization of auditing standards?

> Why should MNCs be concerned about auditing issues?

> What are the problems caused by inflation in evaluating the performance of a foreign subsidiary?

> What issues are associated with the calculation of profit for a foreign subsidiary?

> Do you think it is important to separate the evaluation of the performance of a subsidiary from that of its manager? Why?

> What are the factors that influence the decision regarding the manner in which a particular subsidiary should be treated for purposes of performance evaluation (e.g., as a cost center or a profit center or an investment center)?

> Visit the Web site of Nokia Company (www.Nokia.com). Required: Comment on Nokia’s risk management activities as reported in the company’s 2009 annual report.

> What are the nonfinancial measures available to MNCs for evaluating foreign subsidiary performance?

> What differences can you identify between performance evaluation measures adopted by Japanese and U.S. MNCs?

> What are the main issues that need to be considered in designing and implementing a successful performance evaluation system for a foreign subsidiary?

> Explain the role of accounting in implementing multinational business strategy

> How do differences in cultural values across countries influence strategy implementation within an MNC?

> How does the organizational structure of an MNC influence its strategy implementation?

> Compare and contrast NPV and IRR as capital budgeting techniques.

> Explain the role of accounting in strategy formulation within an MNC.

> What are the external factors that influence strategy formulation within an MNC?

> What are the internal factors that influence strategy formulation within an MNC?

> Sedona Electronics of Arizona exports 25,000 Disc Drive Controllers (DDCs) per year to China under an agreement that covers the period 2009–2013. In China, the DDCs are sold for the RMB (Chinese currency) equivalent of $50 per unit. The total costs in th

> What are some of the problems of trying to regulate CSR practices through legislation?

> Identify five mechanisms for regulating CSR practices at the international level.

> Why is it necessary to regulate the CSR practices of firms?

> What are the implications of climate change for CSR?

> What motivates firms to engage in CSR practices?

> What is the conceptual basis for CSR?

> What are the theories often used to explain the CSR practices of firms?

> What is the Global Reporting Initiative?

> What is the Kyoto Protocol?

> What are the items often included in CSR reports?

> There is no clear definition of corporate social reporting (CSR). The European Commission defines CSR as “the responsibility of enterprises for their impacts on society.” In the United States, there is no governmental regulation regarding CSR. Companies

> What is corporate social reporting (CSR)?

> In what ways do company audit reports vary in different countries?

> What was the impact of the European Union’s Eighth Directive on the regulation of auditing in the United Kingdom?

> What is the PIOB? What is its role in audit regulation?

> On January 1, 2009, a U.S. firm made an investment in Germany that will generate $5 million annually in depreciation, converted at the current spot rate. Projected annual rates of inflation in Germany and in the United States are 5 percent and 2 percent,

> Refer to Exhibit 13.6. Required: Briefly explain the operating environment of a developing country of your choice using the framework that identifies the social, political, economic, and technological influences. Exhibit 13.6:

> A U.S. company is considering an investment project proposal to extend its operations in Germany. As part of the proposed project, the German operation is required to pay an annual royalty of €500,000 to the parent company. Required: Explain the cash fl

> The establishment of the Public Company Accounting Oversight Board (PCAOB) in 2002 was a major step toward strengthening the auditing function in the United States. Required: What can the PCAOB do to strengthen the auditing function in the United States

> This chapter refers to a unique ownership structure of many former state owned enterprises in China, which have been redefined to create new economic entities. Required: Describe the uniqueness of the ownership structure of the entities mentioned above,

> Some commentators argue that the two-tiered corporate structure, with a management board and a supervisory board, prevalent in many Continental European countries, is better suited for addressing corporate governance issues, including the issue of audito

> We’re in the business of satisfying thirst. We do it very well. We’re also thirsty ourselves. Thirsty for continued profitable growth. Every gain delivers more for our shareholders. We’re thirsty for

> Internationally, legislators and professional bodies have focused on corporate governance issues in making recommendations for restoring investor confidence, and auditing is an essential part of corporate governance. Required: Explain the link between a