Question: Gelato Corporation, a private entity reporting

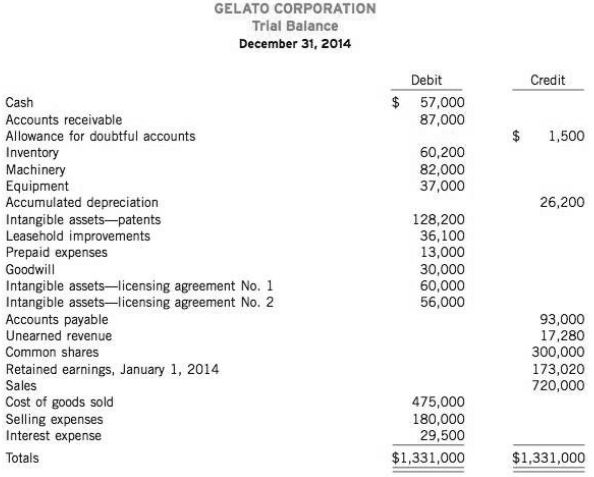

Gelato Corporation, a private entity reporting under ASPE, was incorporated on January 3, 2013. The corporation's financial statements for its first year of operations were not examined by a public accountant. You have been engaged to audit the financial statements for the year ended December 31, 2014, and your audit is almost complete. The corporation’s trial balance is as follows:

The following information is for accounts that may still need adjustment:

1. Patents for Gelato's manufacturing process were acquired on January 2, 2014, at a cost of $87,500. An additional $35,000 was spent in July 2014 and $5,700 in December 2014 to improve machinery covered by the patents and was charged to the Intangible Assets- Patents account. Depreciation on fixed assets was properly recorded for 2014 in accordance with Gelato’s practice, which is to take a full year of depreciation for property on hand at June 30. No other depreciation or amortization was recorded. Gelato uses the straight-line method for all amortization and amortizes its patents over their legal life, which was 17 years when the patent was granted. Accumulate all amortization expense in one income statement account.

2. At December 31, 2014, management determined that the undiscounted future net cash flows that are expected from the use of the patent would be $80,000, the value in use was $75,000, the resale value of the patent was approximately $55,000, and disposal costs would be $5,000.

3. On January 3, 2013, Gelato purchased licensing agreement no. 1, which management believed had an unlimited useful life. Licences similar to this are frequently bought and sold. Gelato could only clearly identify cash flows from agreement no. 1 for 15 years. After the 15 years, further cash flows are still possible, but are uncertain. The balance in the Licenses account includes the agreement’s purchase price of $57,000 and expenses of $3,000 related to the acquisition. On January 1, 2014, Gelato purchased licensing agreement no. 2, which has a life expectancy of five years. The balance in the Licenses account includes its $54,000 purchase price and $6,000 in acquisition expenses, but it has been reduced by a credit of $4,000 for the advance collection of 2015 revenue from the agreement. In late December 2013, an explosion caused a permanent 60% reduction in the expected revenue-producing value of licensing agreement no. 1. In January 2015, a flood caused additional damage that rendered the agreement worthless.

4. The balance in the Goodwill account results from legal expenses of $30,000 that were incurred for Gelato's incorporation on January 3, 2013. Management assumes that the $30,000 cost will benefit the entire life of the organization, and believes that these costs should be amortized over a limited life of 30 years. No entry has been made yet.

5. The Leasehold Improvements account includes the following:

(a) There is a $ 15,000 cost of improvements that Gelato made to premises that it leases as a tenant. The improvements were made in January 2013 and have a useful life of 12 years.

(b) Movable assembly-line equipment costing $ 15,000 was installed in the leased premises in December 2014.

(c) Real estate taxes of$6,100 were paid by Gelato in 2014, but they should have been paid by the landlord under the terms of the lease agreement. Gelato paid its rent in full during 2014. A 10-year non-renewable lease was signed on January 3, 2013, for the leased building that Gelato uses in manufacturing operations. No amortization or depreciation has been recorded on any amounts related to the lease or improvements.

6. Included in selling expenses are the following costs incurred to develop a new product. Gelato hopes to establish the technical, financial, and commercial viability of this project in fiscal 2015.

Salaries of two employees who spend approximately 50% of their time on research and development initiatives (this amount represents their full salary) $110,000

Materials consumed 35,000

Instructions

(a) Prepare an eight-column work sheet to adjust the accounts that require adjustment and include columns for an income statement and a statement of financial position. A separate account should be used for the accumulation of each type of amortization. Formal adjusting journal entries and financial statements are not required.

(b) Prepare Gelato's statement of financial position and income statement for the year ended December 31, 2014, in proper form.

(c) Explain how the accounting would differ if Gelato were reporting under IFRS.

Transcribed Image Text:

GELATO CORPORATION Trial Balance December 31, 2014 Debit Credit $ 57,000 87,000 Cash Accounts receivable Allowance for doubtful accounts $ 1,500 Inventory Machinery Equipment Accumulated depreciation Intangible assets--patents Leasehold improvements Prepaid expenses Goodwill 60,200 82,000 37,000 26,200 128,200 36,100 13,000 30,000 60,000 56,000 Intangible assets-licensing agreement No. 1 Intangible assets-licensing agreement No. 2 Accounts payable Unearned revenue Common shares 93,000 17,280 300,000 173,020 720,000 Retained earnings, January 1, 2014 Sales Cost of goods sold Selling expenses Interest expense 475,000 180,000 29,500 Totals $1,331,000 $1,331,000

> Harper Corporation has the following portfolio of investments at December 31, 2014, that qualify and are accounted for using the fair value through other comprehensive income (FV-OIC) method: Early in 2015, Harper sold all the Frank Inc. shares for $17 p

> Green Thumb Landscaping Limited has determined that its lawn maintenance division is a cash-generating unit under IFRS. The carrying an10unts of the division’s assets at December 31, 2014, are as follows: Land $25,000 Building 50,000 E

> Octavia Corp. prepares financial statements annually on December 31, its fiscal year end. At December 31, 2014, the company has the account Investments in its general ledger that contains the following debits for investment purchases, and no credits: The

> On December 31, 2013, Nodd Corp. acquired an investment in GT Ltd. bonds with a nominal interest rate of I 0% (received each December 31) and the controller produced the following bond amortization schedule based on an effective rate of approximately 15%

> Castlegar Ltd. had the following investment portfolio at January 1, 2014: During 2014, the following transactions took place: 1. On March 1, Josie Corp. paid a $2 per share dividend. 2. On April 30, Castlegar sold 300 shares of Asher Corp. for $10 per sh

> Pascale Corp. has the following securities (all purchased in 2014) in its investment ponfolio on December 31, 2014: (1) 2,500 Anderson Corp. common shares, which cost $48,750 (2) 10,000 Munter Ltd. common shares, which cost $580,000 (3) 6,000 King Corp.

> Access the annual report for British Airways pic for the year ended December 31, 2011, from the company's website. Use the notes to the financial statements to answer the following questions. Instructions (a) Does British Airways pic report any intangib

> NB Corp. purchased a $100,000 face-value bond of Myers Corp. on August 31, 2013, for $104,490 plus accrued interest. The bond pays interest annually each November 1 at a rate of 9%. On November 1, 2013, NB Corp. received the annual interest. On December

> On December 31, 2013, Zurich Corp. provided you with the following pre-adjustment information regarding its portfolio of investments held for short-term profit-taking: During 2014, Bilby Corp. shares were sold for 59,500. The fair values of the securitie

> In early January 2014, Chi Inc., a private enterprise that applies ASPE, purchased 40% of the common shares of Washi Corp. for $410,000. Chi was now able to exercise considerable influence in decisions made by Washi's management. Washi Corp.’s statement

> Refer to the information in E9-3, except assume that Mustafa hopes to make a gain on the bonds as interest rates are expected to fall. Mustafa accounts for the bonds at fair value with changes in value taken to net income, and separately recognizes and r

> On January 1, 2014, Phantom Corp. acquires $300,000 of Spider Products, Inc. 9% bonds at a price of 5278,384. The interest is payable each December 31, and the bonds mature on December 31, 2016. The investment will provide Phantom Corp. with a 12% yield.

> Perez Corp., a mining company, owns a significant mineral deposit in a northern territory. Included in the asset is a road system that was constructed to give company personnel access to the mineral deposit for maintenance and mining activity. The road s

> On January 1, 2014, Mustafa Limited paid $537,907.40 for 12% bonds with a maturity value of $500,000. The bonds provide the bondholders with a 10% yield. They are dated January 1, 2014, and mature on January 1, 2019, with interest receivable on December

> On January 1, 2014, Kenn Corp. purchased at par 10% bonds having a maturity value of $300,000. They are dated January 1, 2014, and mature on January 1, 2019, with interest receivable on December 31 of each year. The bonds are accounted for using the amor

> Each of the following investments is independent of the others. 1. A bond that will mature in four years was bought one month ago when the price dropped. As soon as the value increases, which is expected next month, it will be sold. 2. Ten percent of the

> The following are two independent situations. Situation 1: Lauren Inc. received dividends from its common share investments during the year ended December 31, 2014, as follows: • A cash dividend of $12,250 is received from Peel Corporation. Lauren owns a

> On January 1, 2014, Rae Corporation purchased 30% of the common shares of Martz Limited for $196,000. Martz Limited shares are not traded in an active market. The carrying amount of Martz's net assets was $520,000 on that date. Any excess of the purchase

> Instructions Read the article "Recognizing Assets" by John Browne, CA Magazine, December 2008. Answer the following questions. (a) What are regulatory assets? Which types of companies have these assets? (b) What are the current accounting issues with res

> Harnish Inc. acquired 25% of the outstanding common shares of Gregson Inc. on December 31, 2013. The purchase price was $1,250,000 for 62,500 shares, and is equal to 25% of Gregson's carrying amount. Gregson declared and paid a $0.75 per share cash divid

> Fox Ltd. invested 51 million in Gloven Corp. early in the current year, receiving 25% of its outstanding shares. At the time of the purchase, Gloven Corp. had a carrying amount of $3.2 million. Gloven Corp. pays out 35% of its net income in dividends eac

> Holmes, Inc. purchased 30% of Nadal Corporation's 30,000 outstanding common shares at a cost of515 per share on January 3, 2014. The purchase price of515 per share was based solely on the book value of Nadal's net assets. On September 21, Nadal declared

> Weekly Corp., a December 31 year-end company that applies IFRS, acquired an investment in 1,000 shares of Credence Corp. in mid-2010 for $29,850. Between significant volatility in the markets and in the business prospects of Credence Corp., the accountin

> The management of Luis Inc., a small private company that uses the cost recovery impairment model, was discussing whether certain equipment should be written down as a charge to current operations because of obsolescence. The assets had a cost of $900,00

> On January 1, 2012, Mamood Ltd. paid $322,744.44 for 12% bonds of Variation Ltd. with a maturity value of$300,000. The bonds provide the bondholders with a 10% yield. They are dated January 1, 2012, mature on January 1, 2018, and pay interest each Decemb

> In early 2014, for the first time, HTSM Corp. invested in the common shares of another Canadian company. It acquired 5,000 shares of Toronto Stock Exchange-traded Bayscape Ltd. at a cost of $68,750. Bayscape is projected to reach a value of $ 15.50 per s

> Niger Corp. provided you with the following information about its investment in Fahad Corp. shares purchased in May 2014 and accounted for using the FV-OCI method: Cost………………………………………………………………………………. $39,900 Fair value, December 31, 2014………………………………………….

> At December 31, 2014, the equity investments of Wang Inc. that were accounted for using the fair value through other comprehensive income model without recycling (application of IFRS 9) were as follows: Because of a change in relationship with Ahn Inc.,

> Arantxa Corporation made the following purchases of investments during 2014, the first year in which Arantxa invested in equity securities: 1. On January 15, purchased 9,000 shares of Nirmala Corp.'s common shares at $33.50 per share plus commission of $

> The following information is available about Kao Corp.'s investments at December 31, 2014. This is the first year Kao has purchased securities for investment purposes. Assume that Kao Corp. follows IFRS and applies IAS 39. Instructions (a) Prepare the

> L'Oreal is the world's largest cosmetic company, with brands such as its own name, Redken, Mayhelline, Lancome, and Ralph Lauren, just to name a few. Instructions Access L'Oreal’s annual financial statements for the year ended December 31, 2011, from

> Activet Corporation, a Canadian-based international company that follows IFRS, including IAS 39, has the following securities in its portfolio of investments acquired for trading purposes and accounted for using the fair value through net income method o

> On January 3, 2014, Mega Limited purchased 3,000 shares (30%) of the common shares of Sonja Corp. for $438,000. The following information is provided about the identifiable assets and liabilities of Sonja at the date of acquisition: During 2014, Sonja re

> Both ASPE and IFRS require disclosures about an enterprise's investments that include the carrying amount of each type of investment by the accounting method used and the income, gains, or losses classified in a sin1ilar way. Identify the disclosure obje

> Finlay Limited constructed a building at a cost of $2.8 million and has occupied it since January 1994. It was estimated at that time that its life would be 40 years, with no residual value. In January 2014, a new roof was installed at a cost of $370,000

> Beckett Corp. is facing a decision of whether to purchase 40% of Kyla Corp.'s shares for $1.6 million cash, giving Beckett significant influence over the investee company, or 60% of Kyla's shares for $2.4 million cash, making Kyla a subsidiary company. T

> Use the information from BE9-19 except thatJulip Corporation is a private enterprise that applies ASPE. Prepare Julip’s 2014 entries to record all transactions and events related to its significant influence investment in Krov Corporation assuming (a) Kr

> Julip Corporation purchased a 25% interest in Krov Corporation on January 2, 2014, for $1,000. At that time, the carrying amount of Krov's net assets was $3,600. Any excess of the cost of the investment over Julip's share of Krov's carrying amount can be

> Poot Corporation purchased a 40% interest in Moss, Inc. for $100. This investment gave Poot significant influence over Moss. During the year, Moss earned net income of $15 and paid dividends of $5. Assuming the purchase price was equal to 40% of Moss's n

> Kolber Manufacturing Limited designs, manufactures, and distributes safety boots. In January 2014, Kolber purchased another business that manufactures and distributes safety shoes, to complement its existing business. The total purchase price was to be $

> Ramirez Company has an investment in 6%, 10-year bonds of Soto Company. The investment was originally purchased at par for $100 in 2013 and it is accounted for at amortized cost. Early in 2014, Ramirez recorded an impairment on the Soto investment due to

> Write a brief essay highlighting the differences between IFRS and ASPE noted in this chapter, discussing the conceptual justification for each.

> Echo Corp., a retail propane gas distributor, has increased its annual sales volume to a level that is three times greater than the annual sales of a dealer that it purchased in 2014 in order to begin operations. The board of directors of Echo Corp. rece

> On June 30, 2014, your client, Bearcat Limited, was granted two patents for plastic cartons that it had been producing and marketing profitably for the past three years. One patent covers the manufacturing process and the other covers related products. B

> Weaver Limited is a company that is a distributor of hard-to-find computer supplies such as hardware parts and cables. It sells and ships products all over the world. Recently the board of directors approved the plan and a budget for the company to desig

> In 1985, Lincoln Limited completed the construction of a building at a cost of $ 1.8 million; it occupied it in January 1986. It was estimated that the building would have a useful life of 40 years and a residual value of $400,000. Early in 1996, an add

> Biofuel Inc. (BI) is a private company that just started up this year. The company's owner, Sarah Biorini, created a process whereby carbon dioxide (CO2) emissions are converted into biofuel. Specifically, the C02 is pumped into a pond where algae is gro

> Dr. Gary Morrov’s a former surgeon, is the president and owner of Morrow Medical (MM), a private Ontario company that focuses on the design and implementation of various medical and pharmaceutical products. 'With the recent success of various products pu

> Monsecours Corp., a public company incorporated on June 28, 2013, setup a single account for all of its intangible assets. The following summary discloses the debit entries that were recorded during 2013 and 2014 in that account: The new business started

> Information for Canberra Corporation's intangible assets follows: 1. On January 1, 2014, Canberra signed an agreement to operate as a franchisee of Hsian Copy Service, Inc. for an initial franchise fee of $75,000. Of this amount, $35,000 was paid when t

> Guiglano Inc. is a large, publicly held corporation. The following are six selected expenditures that were made by the company during the current fiscal year ended April 30, 2014. The proper accounting treatment of these transactions must be determined i

> The standard setters identify three approaches to accounting for the impairment of financial asset investments: an incurred loss model, an expected loss model, and a fair value model. Identify which models are required to be used by enterprises applying

> The president of Plain Corp., Joyce Lima, is thinking of purchasing Balloon Bunch Corporation. She thinks that the offer sounds fair but she wants to consult a professional accountant to be sure. Balloon Bunch Corporation is asking for $85,000 in excess

> Macho Inc. has recently become interested in acquiring a South American plant to handle many of its production functions in that market. One possible candidate is De Fuentes SA, a closely held corporation, whose owners have decided to sell their business

> On September 1, 2014, Madonna Lisa Corporation, a public company, acquired Jaromil Enterprises for a cash payment of $763,000. At the time of purchase, Jaromil's statement of financial position showed assets of $850,000, liabilities of $430,000, and owne

> Carras Corporation purchased $60,000 of five-year, 6% bonds of Hu Inc. for $55,133 to yield an 8% return, and classified the purchase as an amortized cost method investment. The bonds pay interest semi-annually. (a) Assum1ing Carras Corporation applies I

> In late July 2014, Mona Ltd., a private company, paid $2 million to acquire all of the net assets of Lubello Corp., which then became a division of Mona. Lubello reported the following statement of financial position at the time of acquisition: Current a

> Six examples follow of purchased intangible assets. They are reported on the consolidated statement of financial position of Phelp Enterprises Limited and include information about their useful and legal lives. Phelp prepares financial statements in acco

> Use the data provided in P1l2-7. Assume instead that Meridan Golf and Sports is a public company. The relevant information for the impairment test on December 31, 2016, is as follows: Data Provided in P12-7 Meridan Golf and Sports was formed on July 1,

> Meridan Golf and Sports was formed on July 1, 2014, when Steve Powerdriver purchased Old Master Golf Corporation. Old Master provides video golf instruction at kiosks in shopping malls. Powerdriver's plan is to make the instruction business part of his g

> In 2013, Aquaculture Incorporated applied for several commercial fishing licences for its commercial fishing vessels. The application was successful and on January 2, 2014, Aquaculture was granted 22 commercial fishing licences for a registration fee of

> During 2012, Medicine Hat Tools Ltd., a Canadian public company, purchased a building site for its product development laboratory at a cost of $61,000. Construction of the building was started in 2012. The building was completed in late December 2013 at

> Institute Limited organized late in 2013 and set up a single account for all intangible assets. The following summary shows the entries in 2014 (all debits) that have been recorded in intangible Assets since then: Instructions (a) Prepare the necessary e

> Tsui Corporation owns corporate bonds at December 31, 2014, accounted for using the amortized cost model. These bonds have a par value of $800,000 and an amortized cost of $788,000. After an impairment review was triggered, Tsui determined that the disco

> Instructions Go to the SEDAR website (www.sedar.com) and choose two companies from each of four different industry classifications. Choose from a variety of industries such as real estate and construction, food stores (under merchandising), biotechnology

> As the recently appointed auditor for Daleara Corporation, you have been asked to examine selected accounts before the six-month financial statements of June 30, 2014, are prepared. The controller for Daleara Corporation mentions that only one account is

> Machinery purchased for $56,000 by Wong Corp. on January 1, 2009, was originally estimated to have an eight-year useful life with a residual value of $4,000. Depreciation has been entered for five years on this basis. In 2014, it is determined that the t

> Selected information follows for Mount Olympus Corporation for three independent situations: 1. Mount Olympus purchased a patent from Bakhshi Co. for $1.8 million on January 1, 2012. The patent expires on January 1, 2022, and Mount Olympus is amortizing

> Berrie Inc. has the following amounts included in its general ledger at December 31, 2014: Organization costs ………………………………………………………………….…………….. $34,000 Purchased trademark ………………………………………………………….……..………….. 17,500 Discount on bonds payable ………………………………………

> Selected account information follows for Richmond Inc. as at December 31, 2014. All the accounts have debit balances. Instructions Identify which items should be classified as intangible assets. For the items that are not classified as intangible assets,

> The following is a list of items that could be included in the intangible assets section of the statement of financial position: 1. An investment in a subsidiary company 2. Timberland 3. The cost of an engineering activity that is required to advance a p

> Louvre Inc. bought a business that is expected to give a 25% annual rate of return on the investment. Of the total amount paid for the business, $75,000 was deemed to be goodwill, and the rest was attributed to the identifiable net assets. Louvre Inc. es

> As the president of Victoria Recording Corp., you are considering purchasing Moose Jaw CD Corp., whose statement of financial position is summarized as follows: Current assets $400,000 Plant and equipment (net) 750,000 Other assets

> Aswan Corporation is interested in acquiring Richmond Plastics Limited. Richmond has determined that its excess earnings have averaged approximately $17 5,000 and feels that such an amount should be capitalized over an unlimited period at a 15% rate. Asw

> Net income figures for Belgian Ltd. are as follows: 2010 ………………………………. $75,000 2011 ………………………………. $53,000 2012 ………………………………. $84,000 2013 ………………………………. $87,000 2014 ………………………………. $69,000 Future income is expected to continue at the average amount of the

> Rotterdam Corporation's pre-tax accounting income of $725,000 for the year 2014 included the following items: Amortization of identifiable intangibles $147,000 Depreciation of building 115,000 Loss from discontinued operations 44,000

> The following information relates to Cortez Corp. for 2014: net income of $672,683; unrealized loss of $20,830 related to investments accounted for at fair value through other comprehensive income during the year; and accumulated other comprehensive inco

> At the beginning of 2014, Kao Company, a small private company, acquired a mine for $850,000. Of this amount, $100,000 was allocated to the land value and the remaining portion to the minerals in the mine. Surveys conducted by geologists found that appro

> Gamma Corp. invested in a three-year, $ 100 face value 6% bond, paying $ 105.55. At this price, the bond will yield a 4% return. Interest is payable annually. (a) Prepare a bond premiun1 amortization table for Gamma Corp. assuming Gamma uses the effectiv

> Since 1996, Nike, Inc. has had endorsement contracts with Tiger Woods and some of the world's best known athletes. For example, Nike has been able to gain the rights to use Tiger Woods's name in advertising promotions and on Nike Golf apparel, footwear,

> Topaz Inc. has accounts receivable terms of 2/10, n/30. In the past, 50% of Topaz's customers have taken advantage of the discount and paid within 10 days of the invoice date, and the remaining 50% of customers have paid in full within 30 days of the inv

> Chessman Corporation factors $600,000 of accounts receivable with Liquidity Financing, Inc. on a with recourse basis. Liquidity Financing will collect the receivables. The receivable records are transferred to Liquidity Financing on August 15, 2014. Liqu

> Landstalker Enterprises sold $750,000 of accounts receivable to Leander Factors, Inc. on a without recourse basis under IFRS, as the risks and rewards have been transferred to Leander. The transaction meets the criteria for a sale, and no asset or liabil

> The following information is for the inventory of mini kettles at Funnell Company Limited for the month of May: Instructions (a) Assuming that the periodic inventory method is used, calculate the inventory cost at May 31 under each of the following cost

> On October 1, 2014, Alpha Inc. assigns $2 million of its accounts receivable to Alberta Provincial Bank as collateral for a $1.6-million loan evidenced by a note. The bank's charges are as follows: a finance charge of 4% of the assigned receivables and a

> The Patchwork Corporation manufactures sweaters for sale to athletic-wear retailers. The following information was available on Patchwork for the years ended December 31, 2013, and 2014: During 2014, Patchwork had the following transactions: 1. On June

> The Cormier Corporation sells office equipment and supplies to many organizations in the city and surrounding area on contract terms of 2/10, n/30. In the past, over 75% of the credit customers have taken advantage of the discount by paying within 10 day

> In 2014, Ibran Corp. required additional cash for its business. Management decided to use accounts receivable to raise the additional cash and has asked you to determine the income statement effects of the following transactions: l. On July 1, 2014, Ibr

> Logo Limited follows ASPE. It manufactures sweatshirts for sale to athletic-wear retailers. The following summary information was available for Logo for the year ended December 31, 2013: Part 1 1. Total sales were $465,000. Of the total sales amount, $21

> Boyko Company received an order from Lister Inc. on May 15, 2014, valued at 52,200. Boyko shipped the goods to Lister on May 31, 2014, with terms f.o.b. shipping point, and credit terms 2/10, n/30. Assuming Boyko uses the gross method of recording sales;

> Desrosiers Ltd. had the following long-term receivable account balances at December 31, 2013: Notes receivable $1,800,000 Notes receivable-Employees 400,000 Transactions during 2014 and other information relating to Desrosiers' long-term recei

> On December 31, 2014, Zhang Ltd. rendered services to Beggy Corp. at an agreed price of $91,844.10. In payment, Zhang accepted $36,000 cash and agreed to receive the balance in four equal installments of $18,000 that are due each December 31. An interest

> On October 1, 2014, Healy Farm Equipment Corp. sold a harvesting machine to Homestead industries. Instead of a cash payment, Homestead Industries gave Healy Farm Equipment a $150,000, two-year, 10% note; 10% is a realistic rate for a note of this type. T

> The statement of financial position of Reynolds Corp. at December 31, 2013, includes the following: Transactions in 2014 include the following: 1. Accounts receivable of $138,000 were collected. This amount includes gross accounts of $40,000 on which 2%

> On June 3, Arnold Limited sold to Chester Arthur merchandise having a sale price of $3,000 with terms 3/10, n/60, f.o.b. shipping point. A $90 invoice, terms n/30, was received by Chester on June 8 from John Booth Transport Service for the freight cost.

> By December 31, 2013, Clearing Corp. had performed a significant amount of environmental consulting services for Rank Ltd. Rank was short of cash, and Clearing agreed to accept a $200,000, non- interest-bearing note due December 31, 2015, as payment in f

> At December 31, 2014, Ichor Ltd. has outstanding non-cancellable purchase commitments for 45,500 litres of raw material at S3.25 per litre. The material will be used in Ichor's manufacturing process, and the company prices its raw materials inventory at

> Information from Salini Computers Ltd. follows: Instructions (a) Prepare the entries for Salini Computers Ltd., assuming the gross method is used to record sales and cash discounts. (b) Prepare the entries for Salini Computers Ltd., assuming the net met

> Your accounts receivable clerk, Mitra Adams, to whom you pay a salary of $1,500 per month, has just purchased a new Cadillac. You have decided to test the accuracy of the accounts receivable balance of $86,500 shown in the general ledger. The following i

> Theriault Inc. shows a balance of $420,289 in the Accounts Receivable account on December 31, 2014. The balance consists of the following: Instructions Show how the information above should be presented on the statement of financial position of Theriaul