Question: Horizontal analysis refers to changes of financial

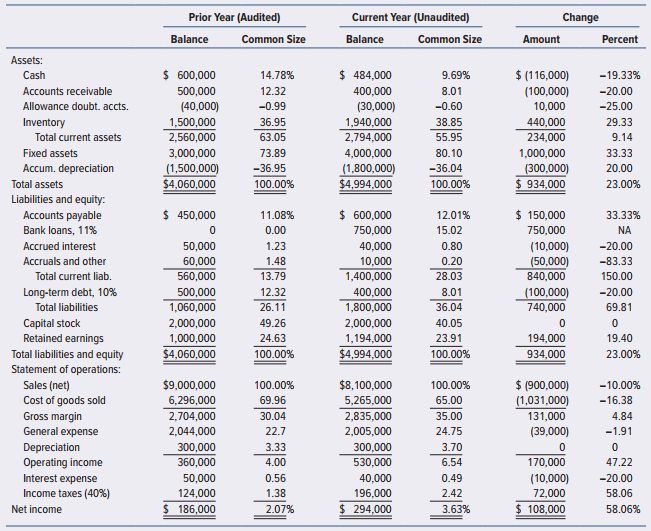

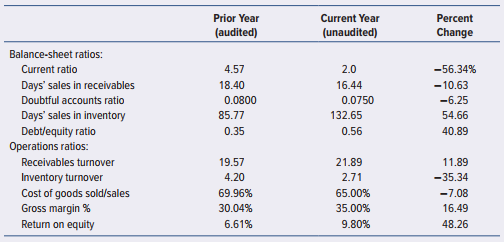

Horizontal analysis refers to changes of financial statement numbers and ratios across two or more years. Vertical analysis refers to financial statement amounts expressed each year as proportions of a base such as sales for the income statement accounts and total assets for the balance-sheet accounts. Exhibit 4.53.1 contains Retail Company’s prior-year (audited) and current-year (unaudited) financial statements, along with amounts and percentages of change from year to year (horizontal analysis) and common-size percentages (vertical analysis). Exhibit 4.53.2 contains selected financial ratios based on these financial statements. Analysis of these data can enable auditors to discern relationships that raise questions about misleading financial statements.

Required:

Study the data in Exhibits 4.53.1 and 4.53.2. Write a memorandum identifying and explaining potential problem areas where misstatements in the current-year financial statements could exist. Additional information about Retail Company is as follows:

The new bank loan, obtained on July 1 of the current year, requires maintenance of a 2:1 current ratio.

Principal of $100,000 plus interest on the 10 percent long-term note obtained several years ago in the original amount of $800,000 is due each January 1.

The company has never paid dividends on its common stock and has no plans for a dividend.

Transcribed Image Text:

Prior Year (Audited) Current Year (Unaudited) Change Balance Common Size Balance Common Size Amount Percent Assets: $ 600,000 $ 484,000 $ (116,000) Cash 14.78% 9.69% -19.33% Accounts receivable 500,000 12.32 400,000 8.01 (100,000) 10,000 -20.00 Allowance doubt. accts. (40,000) -0.99 (30,000) -0.60 -25.00 440,000 234,000 Inventory 1,500,000 2,560,000 36.95 1,940,000 38.85 29.33 Total current assets 63.05 2,794,000 55.95 9.14 3,000,000 73.89 -36.95 Fixed assets 4,000,000 80.10 1,000,000 33.33 Accum. depreciation (1,500,000) $4,060,000 (1,800,000) $4,994,000 -36.04 (300,000) $ 934,000 20.00 Total assets 100.00% 100.00% 23.00% Liabilities and equity: Accounts payable $ 450,000 $ 600,000 $ 150,000 11.08% 12.01% 33.33% Bank loans, 11% 0.00 750,000 15.02 750,000 NA Accrued interest 50,000 1.23 40,000 0.80 (10,000) -20.00 Accruals and other 10,000 60,000 560,000 1.48 0.20 (50,000) 840,000 -83.33 Total current liab. 13.79 1,400,000 28.03 150.00 Long-term debt, 10% 500,000 1,060,000 (100,000) -20.00 12.32 400,000 8.01 Total liabilities 26.11 1,800,000 36.04 740,000 69.81 Capital stock Retained earnings 2,000,000 49.26 2,000,000 40.05 1,000,000 24.63 1,194,000 23.91 194,000 19.40 $4,060,000 $4,994,000 100.00% Total liabilities and equity Statement of operations: Sales (net) Cost of goods sold Gross margin General expense 100.00% 934,000 23.00% $ (900,000) (1,031,000) $9,000,000 100.00% $8,100,000 100.00% -10.00% -16.38 6,296,000 2,704,000 69.96 5,265,000 65.00 30.04 2,835,000 35.00 131,000 4.84 2,044,000 22.7 2,005,000 24.75 (39,000) -1.91 300,000 depreciation Operating income Interest expense Income taxes (40%) 3.33 300,000 3.70 360,000 4.00 530,000 6.54 170,000 47.22 50,000 0.56 40,000 0.49 (10,000) -20.00 124,000 1.38 196,000 2.42 72,000 58.06 Net income $ 186,000 2.07% $ 294,000 3.63% $ 108,000 58.06% Prior Year Current Year Percent (audited) (unaudited) Change Balance-sheet ratios: Current ratio 4.57 2.0 -56.34% Days' sales in receivables 18.40 16.44 -10.63 Doubtful accounts ratio 0.0800 0.0750 -6.25 Days' sales in inventory 85.77 132.65 54.66 Debtlequity ratio Operations ratios: 0.35 0.56 40.89 Receivables turnover 19.57 21.89 11.89 Inventory turnover 4.20 2.71 -35.34 Cost of goods sold/sales Gross margin % Return on equity 69.96% 65.00% -7.08 30.04% 35.00% 16.49 6.61% 9.80% 48.26

> Refer to the internal control questionnaire on a payroll system (Exhibit 5.15). a. Assume that the answer to each question is no. Prepare a table matching the questions to errors or frauds that could occur because of the absence of the control. Your colu

> What are the defining characteristics of (a) white-collar crime, (b) employee fraud, (c) embezzlement, (d) larceny, (e) defalcation, (f) management fraud, and (g) errors?

> What is the auditor’s responsibility regarding fraud risk?

> What is the primary difference between a material misstatement due to fraud or error?

> What is meant by the terms nature, timing, and extent of further audit procedures?

> How is the audit risk model used to plan the audit?

> Which of the following procedures would provide the most reliable audit evidence? a. Inquiries of the client’s internal audit staff. b. Inspection of prenumbered client purchase orders filed in the vouchers payable department. c. Inspection of vendor sal

> What are the components of the risk of material misstatement (RMM)? What are the components of the audit risk model?

> Define audit risk.

> What is the control environment?

> What is the purpose of an audit strategy memorandum? What information should it contain?

> How do the professional audit standards differ for (a) errors, (b) frauds, (c) direct-effect noncompliance, and (d) indirect-effect noncompliance?

> When are analytical procedures required, and when are they optional?

> What are some of the ratios that can be used in preliminary analytical procedures?

> What are the five steps involved with the use of preliminary analytical procedures?

> What is the purpose of performing preliminary analytical procedures in audit planning?

> What are some types of knowledge and understanding about a client’s business and industry that an auditor is expected to obtain? What are some of the methods and sources of information for understanding a client’s business and industry?

> The most reliable evidence regarding the existence of newly acquired computer equipment is a. Inquiry of management. b. Documentation prepared externally. c. Evaluation of the client’s procedures. d. Physical observation.

> What is the major concern for auditors related to evidence obtained from related parties?

> Why should auditors understand their clients’ performance measures when assessing inherent risk?

> If tests of controls induce the audit team to change the assessed level of control risk for fixed assets from 0.4 to 1.0 and audit risk (0.05) and inherent risk remain constant, the acceptable level of detection risk is most likely to a. Change from 0.1

> How does control risk affect the nature, timing, and extent of further audit procedures?

> The auditors assessed risk of material misstatement at 0.50 and said they wanted to achieve a 0.05 risk of failing to express a correct opinion on financial statements that were materially misstated. What detection risk do the auditors plan to use for pl

> The risk of material misstatement is composed of which audit risk components? a. Inherent risk and control risk. b. Control risk and detection risk. c. Inherent risk and detection risk. d. Inherent risk, control risk, and detection risk.

> The likelihood that material misstatements may have entered the accounting system and not been detected and corrected by the client’s internal control is referred to as a. Inherent risk. b. Control risk. c. Detection risk. d. Risk of material misstatemen

> Which of the following circumstances would most likely cause an audit team to perform extended procedures? a. Supporting documents are produced when requested. b. The client made several large adjustments at or near year-end. c. The company has recently

> One of the typical characteristics of management fraud is a. Falsification of documents in order to misappropriate funds from an employer. b. Victimization of investors through the use of materially misleading financial statements. c. Illegal acts commit

> Auditing standards do not require auditors of financial statements to a. Understand the nature of errors and frauds. b. Assess the risk of occurrence of errors and frauds. c. Design audits to provide reasonable assurance of detecting errors and frauds. d

> Ordinarily, what source of evidence should least affect audit conclusions? a. External documentary evidence. b. Inquiry of management. c. Documentation prepared by the audit team. d. Inquiry of entity legal counsel.

> What is the primary objective of the fraud brainstorming session? a. Determine audit risk and materiality. b. Identify whether analytical procedures should be applied to the revenue accounts. c. Assess the potential for material misstatement due to fraud

> Which of the following matters relating to an entity’s operations would an auditor most likely consider as an inherent risk factor in planning an audit? a. The entity’s fiscal year ends on June 30. b. The entity enters into significant derivative transac

> Which of the following risk types increase when an auditor performs substantive analytical audit procedures for financial statement accounts at an interim date? a. Inherent. b. Control. c. Detection. d. Sampling.

> An auditor’s analytical procedures indicate a lower than expected return on an equity method investment. This situation most likely could have been caused by a. An error in recording amortization of the excess of the investor’s cost over the investment’s

> What are the primary reasons for conducting an evaluation of an audit client’s internal control?

> A primary objective of analytical procedures used in the final review stage of an audit is to a. Identify account balances that represent specific risks relevant to the audit. b. Gather evidence from tests of details to corroborate financial statement as

> Auditors perform analytical procedures in the planning stage of an audit for the purpose of a. Deciding the matters to cover in an engagement letter. b. Identifying unusual conditions that deserve more auditing effort. c. Determining which of the financi

> Which of the following statements best describes auditors’ responsibility for detecting a client’s noncompliance with a law or regulation? a. The responsibility for detecting noncompliance exactly parallels the responsibility for errors and fraud. b. Aud

> When auditors become aware of noncompliance with a law or regulation committed by client personnel, the primary reason that the auditors should obtain a better understanding of the nature of the act is to a. Recommend remedial actions to the audit commit

> An audit committee is a. Composed of internal auditors. b. Composed of members of the audit team. c. Composed of members of a company’s board of directors who are not involved in the day-to-day operations of the company. d. A committee composed of person

> Martin is considering submitting a proposal to conduct the audit examination of Phillip Inc., a manufacturer and distributor of automotive parts to the large automobile manufacturers. Martin learned of this client opportunity through one of its staff acc

> When evaluating whether accounting estimates made by management are reasonable, auditors would be most interested in which of the following? a. Key factors that are consistent with prior periods. b. Assumptions that are similar to industry guidelines. c.

> Under the Private Securities Litigation Reform Act (the Act), independent auditors are required to first a. Report in writing all instances of noncompliance with the Act to the client’s board of directors. b. Report to the SEC all instances of noncomplia

> An audit strategy memorandum contains a. Specifications of auditing standards relevant to the financial statements being audited. b. Specifications of procedures the auditors believe appropriate for the financial statements under audit. c. Documentation

> Auditors are not responsible for accounting estimates with respect to a. Making the estimates. b. Determining the reasonableness of estimates. c. Determining that estimates are presented in conformity with GAAP. d. Determining that estimates are adequate

> Analytical procedures used when planning an audit should concentrate on a. Weaknesses in the company’s internal control activities. b. Predictability of account balances based on individual significant transactions. c. Management assertions in financial

> Define control risk and explain the role of control risk assessment in audit planning.

> Analytical procedures can be used in which of the following ways? a. As a means of overall review near the end of the audit. b. As “attention-directing” methods when planning an audit at the beginning. c. As substantive audit procedures to obtain evidenc

> Which of the following relationships between types of analytical procedures and sources of information are most logical? Type of Analytical Procedure Source of Information a. Comparison of current account balances with prior periods b. Comparison of

> Which of the following is a specific audit procedure that would be completed in response to a particular fraud risk in an account balance or class of transactions? a. Exercising more professional skepticism. b. Carefully avoiding conducting interviews wi

> An important principle for auditors is the need to maintain an appropriate level of professional skepticism. Required: a. Define professional skepticism. b. During which stages of the audit are auditors required to exhibit professional skepticism? c. Ho

> Oak Industries, a manufacturer of radio and cable TV equipment and an operator of subscription TV systems, had a multitude of problems. Subscription services in a market area, or which $12 million of cost had been deferred, were being terminated, and the

> An auditor must identify the relevant assertions about each significant financial statement account and disclosure and then gather evidence to conclude whether a material misstatement exists for each assertion. The nature of each financial statement acco

> Johnson & Company, CPAs, audited Guaranteed Savings & Loan Company. M. Johnson had the assignment of evaluating the collectability of real estate loans. Johnson was working on two particular loans: (1) a $4 million loan secured by Smith Street Apartments

> Weyman Z. Wannamaker is the chief financial officer of Cogburn Company. He prides himself on being able to manage the company’s cash resources to minimize the interest expense. Consequently, on the second business day of each month, Wey

> Audit standards distinguish auditors’ responsibility for planning procedures for detecting noncompliance with laws and regulations having a direct effect on financial statements versus planning procedures for detecting noncompliance with laws and regulat

> Give an example of an error or fraud that would misstate financial statements to affect the accounts as follows, taking each case independently. (Note: “Overstate” means the account has a higher value than would be appropriate under GAAP and “understate”

> What are management’s and auditors’ respective responsibilities regarding internal control?

> The auditor should establish an overall audit strategy that sets the scope, timing, and direction of the audit and guides the development of the audit plan. In establishing the overall audit strategy, the auditor should develop and document an audit plan

> The following situations represent errors and frauds that could occur in financial statements. Required: State how the ratio in question would compare (higher, equal, or lower) to what the ratio should have been had the error or fraud not occurred. a. T

> Management fraud (fraudulent financial reporting) is not the expected norm, but it happens from time to time. In the United States, several cases have been widely publicized. They happen when motives and opportunities overwhelm managerial integrity. a. W

> What is management’s responsibility for reporting on internal control over financial reporting?

> This question consists of a number of items pertaining to an auditor’s risk analysis for a company. Your task is to tell how each item affects overall audit risk—that is, the probability of issuing an unmodified audit report on materially misleading fina

> Suppose management estimated the market valuation of some obsolete inventory at $99,000; this inventory was recorded at $120,000, which resulted in recognizing a loss of $21,000. The auditors obtained the following information: The inventory in question

> Audit risks for particular accounts and disclosures can be conceptualized in the model: Audit risk (AR) = Inherent risk (IR) × Control risk (CR) × Detection risk (DR). Use this model as a framework for considering the following situations and deciding wh

> Dunder-Mifflin Inc. wanted to expand its manufacturing and sales facilities. The company applied for a loan from First Bank, presenting the prior-year audited financial statements and the forecast for the current year shown in Exhibit 4.56.1. (Dunder-Mif

> Kelly Griffin, an audit manager, had begun preliminary analytical procedures of selected statistics related to the Majestic Hotel. Her objective was to obtain an understanding of the hotel’s business in order to draft a preliminary audi

> As part of your regular year-end audit of a public client, you must estimate the probability of success of its proposed new product line. The client has experienced financial difficulty during the last few years and, in your judgment, a successful introd

> For a typical audit engagement, describe the people and skills that are normally assigned to a full service audit team.

> What are the three goals of an internal control system according to the COSO report? Which of the three is most important to auditors?

> What is meant by the information and communications component of an effective internal control system? How can an auditor evaluate whether a client’s internal control system is functioning properly for this component?

> What must external auditors do to use the work of audit specialists in the audit of an entity’s financial statements?

> Generally accepted auditing standards require auditors to be independent. Included within this standard are the concepts of independence in fact and independence in appearance. Required: a. Define independence in fact and independence in appearance. b.

> What must external auditors do to use the work of internal auditors in the audit of an entity’s financial statements?

> List some items normally documented in a planning memorandum.

> What is the purpose of a planning memorandum?

> What benefits are obtained by having an engagement letter? What is a termination letter?

> Why do predecessor auditors need to obtain the client’s consent to give information to prospective auditors? What information should prospective auditors try to obtain from predecessor auditors?

> What sources of information can auditors use in connection with deciding whether to accept a new client?

> What are the documentation retention requirements of AS 1215?

> What is considered the most important content of the auditor’s current audit documentation files?

> What information would you expect to find in a current audit file?

> What is the Committee of Sponsoring Organizations (COSO)? Briefly describe the original COSO framework from 1992 and the improvements made in the updated COSO framework from 2013.

> You are meeting with executives of Cooper Cosmetics Corporation to arrange your firm’s engagement to audit the corporation’s financial statements for the year ending December 31. One executive suggests the audit work be divided among three staff members.

> What purposes are served by a dual-purpose test?

> What is the difference between preventive controls and detective controls? Give an example of each.

> Boulder Mines paid $425,000 for the right to extract ore from a 250,000-ton mineral deposit. In addition to the purchase price, Boulder Mines also paid a $110 fi ling fee, a $2,000 license fee to the state of West Virginia, and $55,390 for a geologic sur

> National Truck Company is a large trucking company that operates throughout the United States. National Truck Company uses the units-of-production (UOP) method to depreciate its trucks. National Truck Company trades in trucks often to keep driver morale

> Assume that on January 2, 2012, Vincent of Vermont purchased fixtures for $8,700 cash, expecting the fixtures to remain in service for five years. Vincent has depreciated the fixtures on a double-declining-balance basis, with $1,800 estimated residual va

> Assume Z-1 Software Consultants purchased a building for $445,000 and depreciated it on a straight-line basis over 40 years. The estimated residual value was $90,000. After using the building for 20 years, Z-1 realized that the building will remain usefu

> Assume that in early January 2012, a Sunshine Bakery restaurant purchased a building, paying $53,000 cash and signing a $103,000 note payable. The restaurant paid another $66,000 to remodel the building. Furniture and fixtures cost $59,000, and dishes an

> During fiscal year 2012, Capitol Cupcakes reported a net income of $132.4 million. Capitol received $1.4 million from the sale of other businesses. Capitol made capital expenditures of $10.5 million and sold property, plant, and equipment for $6.8 millio

> Wilcox Financial paid $530,000 for a 45% investment in the common stock of Hornet, Inc. For the first year, Hornet reported net income of $240,000 and at year-end declared and paid cash dividends of $125,000. On the balance-sheet date, the fair value of

> Refer to the RadioShack Corporation Consolidated Financial Statements in Appendix B at the end of this book. This case leads you through an analysis of the activity in Radioshack’s long-term assets, as well as the calculation of its rate of return on tot

> Refer to Amazon.com, Inc.’s Consolidated Financial Statements in Appendix A at the end of the book, and answer the following questions: 1. Refer to Note 1 and Note 3 of the Notes to Consolidated Financial Statements. What kinds of assets are included in

> Ralph’s Pizza bought a used Toyota delivery van on January 2, 2012, for $18,600. The van was expected to remain in service for four years (35,000 miles). At the end of its useful life, Ralph’s officials estimated that the van’s residual value would be $2

> North Mark (NM) owns vast amounts of corporate bonds. Suppose that on June 30, 2012, NM buys $800,000 of CitiSide bonds at a price of 102. The CitiSide bonds pay cash interest at the annual rate of 7% and mature at the end of five years. 1. How much did

> United Jersey Bank of Princeton purchased land and a building for the lump sum of $6 million. To get the maximum tax deduction, the bank’s managers allocated 80% of the purchase price to the building and only 20% to the land. A more realistic allocation

> Assume Shoe Mania Corporation completed the following transactions: a. Sold a store building for $620,000. The building had cost Shoe Mania $1,400,000, and at the time of the sale, its accumulated depreciation totaled $780,000. b. Lost a store building i

> The European Press (TEP) is a major telecommunication conglomerate. Assume that early in year 1, TEP purchased equipment at a cost of 20 million euros (€20 million). Management expects the equipment to remain in service for four years and estimated resid

> Lowe’s Companies, Inc., the second-largest home improvement retailer, reported the following information (adapted) for its fiscal year ended January 31, 2011: Requirements 1. Compute profit margin for the year ended January 31, 2011.