Question: I thought the Internet would be an

I thought the Internet would be an ideal way to distribute our products. We’ve had a lot of success with our direct sales, but now we can reach a much larger audience. The baskets we make and sell appeal to people everywhere. I thought about opening stores in other towns or maybe even franchising, but the web offers me a way to expand without losing control.

That’s why the results for the first quarter of our web-based unit are so disappointing. We expected a small loss because of marketing and other start-up expenses, but I was not prepared for the beating we took.

Maya McCrum, President and CEO, AGM Enterprises

Organization AGM Enterprises is a small, family-owned and -managed company that produces and sells wooden baskets. The company was founded in 1947 in California by Autumn McCrum as a way of supplementing the family income. The business remained small until 1990, when Maya McCrum took it over from her mother. Until that time, all orders were taken by the senior Ms. McCrum and all baskets were handmade by her. Ten years ago, Maya moved to a model of having “dealers†take orders and opened a small workshop where part-time labor produced the baskets. The dealers were also looking to supplement their incomes and, supplied with a small display inventory, displayed the baskets at home or at parties, and took orders. Order fulfillment was handled directly by AGM Enterprises personnel, who shipped finished baskets directly to customers. Little production inventory was kept.

Last year, Maya McCrum evaluated the costs and benefits of two alternative distribution channels in an attempt to expand the business beyond the West Coast. One alternative was to franchise the business. Maya was concerned that she and the managers of AGM would lose control, especially control over quality, which she felt distinguished AGM baskets. The other alternative was to begin taking orders over the Internet. Maya chose the Internet option. The company added a new managerial position, chief technology officer (CTO), and established a subsidiary, agm-online, to handle the new business. In an unusual move for the company, Maya went outside the small circle of family and friends and hired as the CTO Mary Brown, who had experience on both the technical and management sides of a local Internet start-up. Mary was looking for something new where she could be in charge of an entire operation and was excited that she could combine this with her interest in basket weaving. It was agreed that if she could meet or exceed her budget for the first year of operation, she would be given a substantial piece of agm-online.

The executives of AGM Enterprises considered the initial foray into the Internet to be an experiment to see if the “anonymous†approach would be effective in selling baskets. Until this time, AGM considered its network of dealers to be crucial in the growth it had experienced in the last several years. To this end, a separate workshop (factory) was established in Pennsylvania. One of the reasons for selecting Pennsylvania was the availability of part-time labor at lower costs than in California. Another was to attempt to penetrate the East Coast market by locating a workshop there, taking advantage of more immediate access to local market tastes and trends. It was decided that the Pennsylvania operation would produce exclusively for agm-online business and the California workshop would continue to handle the orders from dealers.

Most of the staff functions for agm-online were provided and controlled by AGM Enterprises. Mary Brown and Donna Cunha, the senior vice president of marketing for the parent company, jointly decided the marketing budget. While the budget was decided jointly, media decisions and advertising campaigns were run directly from the parent organization. Personnel and financial services were also centralized.

Mary contracted with a major telecommunications company to provide web hosting services for the operation. She wanted to go with a telecommunications company rather than a local Internet service provider (ISP) for reasons of reliability. The back office operations (billing, payroll, etc.) would be maintained on personal computers at the agm-online office.

The Initial Plan

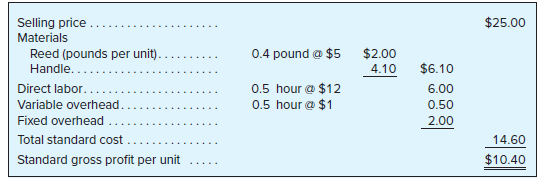

AGM Enterprises (and agm-online) have a July 1 fiscal year, and the launch of agm-online was designed to coincide with the beginning of fiscal year 1. Maya and Mary decided that agmonline would initially offer only one of the company’s many baskets for sale. Company managers believed this would simplify production scheduling and help maintain quality control for the workforce. The basket to be offered was the round basket, one of the company’s most popular. The standard cost sheet for the basket is shown in Exhibit 16.20.

The cost accounting system at AGM Enterprises and the one adopted for agm-online is a full absorption, standard cost system. Overhead is assigned to products (at standard cost) and not recognized in income until the product is sold. Variable overhead is allocated on the basis of direct labor-hours and fixed overhead on the number of units. The fixed overhead rate is based on an estimated production level for the quarter. All variances from standard are recognized in the period recorded.

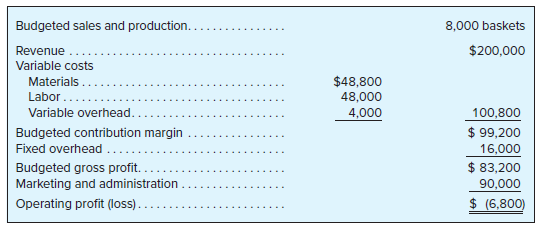

Because of the uncertainty surrounding the demand for baskets using this new channel, the first-quarter budget was designed to be “easy†to meet. In addition, relatively large marketing expenses were budgeted for promoting the new channel at related websites and in craft publications. This was especially important in some of the East Coast publications because AGM had a small share in these markets. The first-quarter operating budget is shown in Exhibit 16.21. The marketing and administration budget included the costs incurred by the parent for providing these services, as well as the cost of the small staff assisting Mary Brown and Jeff Lancaster, the production manager at agm-online.

First-Quarter Results

At first, things went well for agm-online. Sales in July were sufficiently strong that managers thought the initial sales forecast might have been too limiting. Beginning in mid-August, however, events turned against the new operation. Workers at the telecommunications company went on strike. At first, there was little impact. On August 9, however, a phone line leading to the server was damaged. Because of the strike, the site went off the air. It was one week before supervisors were able to get the site back up. Although difficult to estimate, Mary suggested in a message to AGM Enterprises that the company lost about 5 percent in unit sales (i.e., about 400 baskets). She based this estimate on the fact that lines were down 7 days of the quarter (about 7.7 percent) but that some of the customers that were not able to connect would return when service was restored. Others would simply click on the next site their search engine identified.

In order to try and counteract some of the negative publicity that had occurred, agmonline offered some concessions to customers. One concession was free shipping on all orders over $100. (Initially, shipping was billed to the customer at cost.) This added $13,000 to the Marketing and Administration expenses for the quarter. Also, at Mary’s request, additional marketing campaigns costing $32,000 were launched in craft magazines and on cable television. These efforts helped make up for the lost sales.

As sales were falling, the company was also hit by the booming economy in the state when the basket makers were finding better part-time employment in the local industries. As a result, agmonline had to increase the wage rate simply to maintain production.

Not all the news was bad, however. Mary had immediately identified a modification in the production process at the Pennsylvania workshop that reduced the scrap on each basket by 20 percent. This modification was used on all baskets produced in the quarter. (In the original process, scrap occurred in the initial cutting of the material and, therefore, no labor was lost because of the scrap.) In addition, she maintained the level of quality, so the company received no returns and many comments about future purchases. Still, she was concerned that this poor first-quarter showing was going to be difficult to make up.

I came here because I wanted to work at a company that, first, I had a significant ownership stake in and, second, would allow me to pursue my interest in the craft of basket weaving full time. I’m afraid that, because of the strike, I won’t meet the first-year budget and will lose my bonus shares. I think Maya is a fair person, but she has to answer to the other owners. They might not be so willing to assume that these results are because of events out of my control.

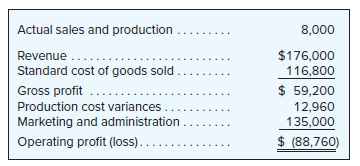

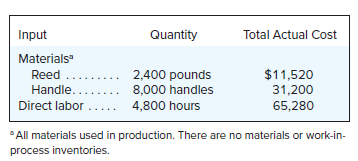

Exhibit 16.22 shows the actual results for the quarter. The actual direct (materials and labor) production inputs are shown in Exhibit 16.23. Actual total variable overhead for the quarter was $5,760 and actual fixed overhead was $16,000.

Next Steps

As Maya contemplates the future of the new distribution channel, she is concerned as well about the effect of the first quarter on her agreement with Mary.

I would really like the answer to just one question: Should we rewrite our agreement? From what I have seen, Mary is really dedicated to the business. On the other hand, an agreement is an agreement. If we revise it now, what kind of problems will we have in the future?

Required

a. What were the factors that caused actual quarterly income to be less than budgeted? Quantify the effect of each of these factors. Be as specific as possible.

b. For which of these factors, if any, should Mary be held responsible?

c. Should Maya rewrite the agreement with Mary?

> The manager of an operating department just received a cost report and has made the following comment with respect to the costs allocated from one of the service departments: “This charge to my division doesn’t seem right. The service center installed eq

> Pallister Medical, Inc. (PMI) produces and sells a single drug. The company is organized into three divisions: Production, Packaging, and Distribution. Production, located in country A, manufactures the drug producing a single-dose capsule. The variable

> Refer to the information in Exercise 14-48. Assume that the company uses a 12 percent cost of capital. As in Exercise 14-48, performance measures are based on beginning-of-year gross book values for the investment base. Required a. What is the residual i

> Refer to the information in Problems 14-63 and 14-64. Looking at the EVA results for year 3, the president of Marine Division complains that the division is evaluated unfairly because a common cost of capital is used. The president believes that the R&am

> Refer to the information in Problems 14-63 and 14-64. The executives at Bentler’s corporate headquarters are intrigued and interested by the EVA findings. They are concerned, however, about the estimated cost of capital that is used (12

> Refer to the information in Problem 14-63. Looking at the ROI results for year 3, the president of Aeronautics Division complains that the division is evaluated unfairly because of the accounting rules that R&D expenditures be expensed in the year in

> Bentler Industries provides high-technology navigation and communication equipment for the aerospace and shipbuilding industries. It is organized into two divisions, Aeronautics and Marine. The division presidents are given wide decision-making authority

> Vermont Automotive is a regional chain of auto parts stores. The managers of the individual stores are evaluated using ROI. Vermont requires managers to earn an ROI of at least 10 percent of assets. The manager of the Erie store estimates revenues in the

> Technology firms, pharmaceutical firms, oil and gas companies, and other ventures inevitably incur costs on unsuccessful investments in new projects (e.g., new technologies or new drugs). For oil and gas firms, a debate continues over whether those costs

> Division managers at Lesure, Inc. are granted a wide range of decision authority. With the exception of managing cash, which is done at corporate headquarters, divisions are responsible for sales, pricing, production, costs of operations, and management

> Refer to the facts in Problem 14-52 through 14-54. Assume that the Leidich Corporation performance measurement and bonus plans are based on residual income instead of ROI. The company uses a cost of capital of 10 percent in computing residual income. Req

> Surveying the accounts payable records, a clerk in the controller’s office noted that expenses appeared to rise significantly within one month of the close of the budget period. The organization did not have a seasonal product or service to explain this

> Refer to the facts in Problem 14-52. Assume that the performance measurement and bonus plans at Leidich Corporation are based on residual income instead of ROI. The company uses a cost of capital of 10 percent in computing residual income. Required a. Wh

> Refer to the information in Problem 14-52. The manager is still assessing the problem of whether to acquire SSM’s assembly machine. SSM tells the manager that the new machine could be acquired next year, but it will cost 20 percent more

> Refer to the data in Problems 14-49 and 14-50. The manager of the Canal Division complains that the calculation of EVA is unfair because a much longer life is assumed for the Lake Division in calculating EVA. The manager of Lake Division responds that EV

> Refer to the data in Problem 14-49. R&D is assumed to have a three-year life in Canal Division and an eight-year life in Lake Division. All R&D expenditures are spent at the beginning of the year. Assume there are no current liabilities and (unre

> Navarre Energy Research specializes in developing and commercializing new products. It is organized into two divisions, which are based on the products they produce. Canal Division is smaller, and the lives of the products it produces tend to be shorter

> Refer to the data in Exercise 13-51. Recent economic events in the local area have led the owner of Lamphere Lawncare to revise some estimates in budgeting the operating income for the following year. First, unexpected competition has depressed prices. T

> Norcross Carpet Cleaning (NCC) is a commercial service specializing in maintaining floor coverings in high-traffic areas such as malls and office buildings. The business is highly seasonal, with high demand in the winter and low demand in the summer. In

> Refer to the data in Problem 13-68. Required a. Prepare a cash budget for the year. b. The owners want to ensure that they have cash on hand at the end of the year equal to the current accounts payable balance on December 31. Will the store meet that req

> Owen Surf Sports is an idea of two budding entrepreneurs. Their plan is to sell kiteboards from a store in the local town. Between them, they invest $30,000 in capital and are in the process of applying for a bank loan, also for $30,000. The loan would b

> Refer to the information in Exercise 14-45. Assume that the company uses an 8 percent cost of capital. Required a. Compute residual income, using net book value for each year. b. Compute residual income, using gross book value for each year. Exercise 14

> Accounting is objective and precise. Therefore, performance measures based on accounting numbers must be objective and precise. Do you agree? Explain.

> Lane Products manufactures a popular kitchen utensil. The company recently expanded, and the controller believes that it will need to borrow cash to continue operations. It opened negotiations with the local bank for a one-month loan of $40,000 starting

> Refer to the data in Problem 13-64. The managers of Vernon Cabins are considering different pricing strategies for year 2. Under the first strategy (High Price), they will work to maintain an average price of $260 per night. They realize that this will r

> Vernon Cabins is a small motel chain located near state and national parks. Each property is made up of separate cabins. The chain has 10 properties with an average of 15 cabins at each property. In year 1, the occupancy rate (the number of rooms filled

> Oakley Wholesale Hardware and Supplies (OWHS) sells tools, lumber, and other remodeling supplies to commercial contractors. The company controller is compiling cash and other budget information for July, August, and September. On June 30, the company had

> Leland Pharmaceuticals develops both over-the-counter (OTC) and prescription medicines. It is organized into two divisions, which are evaluated as investment centers. The cost of capital used in evaluating the divisions is 9 percent. A local engineering

> West Partners manufactures metal fixtures. Each fitting requires both steel and an alloy that can withstand extreme temperatures. The following data apply to the production of the fittings for year 1: The machine depreciation and other overhead costs are

> Clairpointe Accessories manufactures products for food preparation at several different manufacturing sites. The following costs and other data apply to unit production from the year just ending: The plant controller at the Norfolk Street facility is pre

> Refer to the data in Problem 13-58. Estimate the cash from operations expected in year 2. Problem 13-58:

> Several years ago, Humboldt Products acquired Crescent Fabrication. Prior to the acquisition, Crescent manufactured and sold metal and plastic components to third-party customers. Since becoming a division of Humboldt, Crescent has manufactured component

> Refer to the data in Problem 13-56. Estimate the cash from operations expected in year 2 for Coyle Manufacturing. Problem 13-56:

> On December 30, a manager determines that income is about $9.9 million. The manager has a compensation plan that calls for a bonus of 25 percent (of salary) if income exceeds $10 million and no bonus if it is below $10 million. What problems might arise

> Burchill Consultants is a global consulting firm. The firm has a travel policy that reimburses employees for the “ordinary and necessary” costs of business travel and reimburses business-class airfare for international

> Manning Systems is a commercial software vendor that sells billing and other financial software to companies around the globe. Manning operates a centralized call center for customer support calls. Costs associated with use of the center are charged to t

> Loretto Outfitters is a retail chain of stores organized into two divisions (East and West) and a corporate headquarters. Corporate planners have prepared financial operating plans (budgets) for the two divisions for the upcoming year (year 2). Selected

> Burwell Manufacturing is organized into two divisions (Agriculture and Mining) and a corporate headquarters. The financial group of the corporate staff prepared financial operating plans (budgets) for the two divisions for the upcoming year (year 1). Sel

> Refer to the information in Problem 12-51 for Elba Consulting Associates. Required Recommend a corporate cost allocation system that would improve the performance measurement system used for the three divisions and would address any issues you may have r

> Elba Consulting Associates (ECA) is organized into three divisions (Manufacturing, Retail, and Entertainment). Many support services, such as human resources, legal, and information technology, are provided by corporate staff. The corporate staff costs a

> Refer to the information in Problem 12-49 for Lilac Group. Required Recommend a corporate cost allocation system that would improve the performance measurement system used for the two divisions and would address any issues you may have raised in Problem

> Lilac Group is organized into two geographic divisions (Americas and Rest of the World, or ROW) and a corporate headquarters. Late last year, the Lilac CFO prepared financial operating plans (budgets) for the two divisions for the current year, shown as

> Racine Chemicals’ division managers have been expressing growing dissatisfaction with the methods the company uses to measure division performance. Division operations are evaluated every quarter by comparing them with a budget prepared during the prior

> Cherrylawn Appliance Stores is a nationwide chain of kitchen appliance stores. The company operates with a widely based retail and distribution system that has led to a highly decentralized management structure. Each area manager is responsible for purch

> Give two reasons why dividing production cost variances into price and efficiency variances is useful for management control.

> Burt Management Consultants (BMC) is a multinational consulting group organized geographically. In the U.S. Division, the managing partner for sales (MPS) is responsible for client acquisition. The MPS negotiates project scopes and budgets with the clien

> The board of directors of the Cortez Beach Yacht Club (CBYC) is developing plans to acquire more equipment for lessons and rentals and to expand club facilities. The board plans to purchase about $50,000 of new equipment each year and wants to begin a fu

> Following several years of tight budgets, administrators at the University of California, Davis, looked for ways “to do more with less.” Janet Hamilton, vice chancellor of administration, researched books and articles,

> I just don’t understand these financial statements at all!” exclaimed Mr. Elmo Knapp. Mr. Knapp explained that he had turned over management of Racketeer, Inc., a division of American Recreation Equipment, Inc., to his

> Keewee Company manufactures a single product for the military. Keewee Company had steady work, but it only had a return on investment of 6 percent. The CEO of Keewee Company did a test flight of Keewee’s product and subsequently had a heart attack and di

> Fargo Industries manufactures and sells snowmobiles. The company has eight business units strategically located near the major markets, each with a sales force and two to four manufacturing plants. These business units operate as autonomous profit center

> Stockton Distributors is a large, privately held warehousing and freight company with managers assigned to each region of the U.S. The company managers are developing Stockton’s sales budget for the following year. The budget department of the CFO’s offi

> Refer to the data in Exercise 15-22. PSC management has disallowed any change in transfer prices for special orders. Required a. Does PSC want to accept this order? b. Will the Assembly Division manager be willing to accept this order? c. Will the Packag

> Philadelphia Supply Corporation (PSC) produces and distributes various products for the hospitality industry. It is organized in two divisions: Assembly and Packaging. The managers of both divisions are evaluated and compensated based on divisional incom

> Pick an organization you know, such as a school, a local firm, a business, an entertainment business, a sports team, and so on. Identify an example of when a favorable cost variance (actual cost relative to a budget) is not good news for the performance

> Post Parts manufactures components used in audio and video systems. The year just ended was Post’s first year of operations and it is preparing financial statements. The immediate issue facing Post is the treatment of the direct labor costs. Post set a s

> Volte Corporation produces small electric appliances. The following information is available for the most recent period of operations: Volte never has any work-in-process inventories and began the year with no finished goods inventory. Required a. What w

> Lamphere Lawn Care provides lawn and gardening services. The price of the service is fixed at a flat rate for each service, and most costs of providing the service are the same, given the similarity in the lawns and lots. The owner budgets income by esti

> The director of marketing for Marbud Hardware is responsible for, among other things, identifying new geographic regions for the company to enter. As part of the company’s zero-based budgeting process, the director submitted the followi

> Avery Equipment Rental is a regional firm servicing agricultural and construction clients in the northern plains states. The CFO of Avery is preparing next quarter’s budget and has two forecasts for sales in the Western Branch. The market research group

> Refer to the information in Exercise 13-47. For November, Lambie Custodial Services has budgeted profit of $1,620 based on 50 commercial clients. All information about unit costs for cleaners and supplies, about fixed monthly costs, and about hourly clea

> Lambie Custodial Services (LCS) offers residential and commercial janitorial services. Clients are billed monthly but can cancel the service at the end of any month. In addition to the employees who do the actual cleaning, the firm employs two managers w

> Curtis Party Rentals offers party equipment such as tents, tables, chairs, and so on for outdoor events. The rental fees average $750 per event. Curtis receives a 15 percent deposit two months before the event, 60 percent the month before, and the remain

> Hackett Produce Supply is preparing its cash budget for April. The following information is available: Required What is the estimated amount of cash receipts from accounts receivable collections in April?

> Commonly in many organizations, including corporations, universities, and government agencies, when more than one employee from the organization is having a business meal paid by the organization, the most senior person (in terms of authority, not age) p

> What are the advantages and disadvantages of starting the budgeting process early in the year versus later in the year prior to the budget year?

> One of the authors of this book has a favorite sandwich shop where one person makes the sandwich and another person rings up the sale and takes the customer’s cash. At first, this author thought that having two people involved had something to do with hi

> Cornwall Mobile Detailing (CMD) is a service that washes and details a customer’s vehicle at their home or office. It operates on a membership basis. Members pay $200 dues per month, which entitle them to a complete wash and detail serv

> Dill Shipyards operates a dry dock on the East Coast, where it builds and repairs ships. The company’s Payroll Department supports its two divisions, Naval and Private. The Naval division has contracts with the Department of Defense and

> All sales at Alaska Company are on credit. The company is preparing a cash budget for November. The following information on accounts receivable collections is available from customer payment history: The remaining 2 percent is not collected and is writt

> Kentfield Advisory Services (KAS) is a large management consulting firm organized into two groups: Governmental Services (GS) and Commercial Support (CS). Corporate information technology (IT) services support both groups. The cost of computer support is

> Montrose Instrumentation produces measurement equipment. One component, used in a variety of the company’s products, is critical, and the supply chain often breaks. For that reason, Montrose has a policy to hold in inventory enough of t

> Giardin Outdoors is a recreational goods retailer with two divisions: Online and Stores. The two divisions both use the services of the corporate Finance and Accounting (F&A) Department. Annual costs of the F&A Department total $5.2 million a yea

> Equipment is a specialty nozzle. The budgeting team is now determining the purchase requirements and monthly cash disbursements for this part. Eliot wishes to have in stock enough nozzles to use for the coming month. On August 1, the company has 16,800 n

> Benham Foundries manufactures metal components. The inventory policy at Benham is to hold inventory equal to 150 percent of the average monthly sales for its main product. Sales for the main product for the following year are expected to be 480,000 units

> Cherboneau Novelties produces drink coasters (among many other products). During the current year (year 0), the company sold 520,000 units (packages of 6 coasters). In the coming year (year 1), the company expects to sell 540,000 units, and, in year 2, i

> What is the link between flexible budgeting and management control?

> Sauer Instruments manufactures a surgical tool used in cardiovascular procedures. The demand for the instrument has been strong after a competitor’s instrument was deemed defective and is currently off the market. Sauer management is developing the produ

> Consider the Business Application, “Centralizing as a Cost-Cutting Approach.” Required What best describes the benefits that the companies cited that chose not to centralize likely hoped to receive by keeping certain s

> Zender Fabrication is a long-established manufacturer of various industrial products located in the United States. This company’s products have a well-respected brand name and receive a premium price in the market. The unionized workforce is well paid an

> Shadownook Industries is a multinational firm operating in many businesses, including manufacturing, mining, and agriculture. Top management focuses on the annual earnings in evaluating the performance of sector managers. (Sector managers include a mix o

> Wreford Components produces testing equipment for hospitals and other health care facilities. The vice president for operations (VP-Ops) and vice president for sales (VP-Sales) are paid a flat salary. The base salary is $200,000 for the VP-Ops and $300,0

> Westphalia Corporation produces audio equipment for home, office, and vehicles. The production manager (PM) and marketing manager (MM) are both are paid a flat salary and are eligible for a bonus. The bonus is equal to 2 percent of company profit that is

> Lamont Copy Centers (LCC) operates several stores in the upper midwest. The company is decentralized. At the corporate level, there are two operating managers: chief personnel officer (CPO) and chief operating officer (COO). The CPO’s p

> Bramell Park is an amusement park with an entrance fee that allows unlimited rides. Last year, the company sold 88,000 one-day admission tickets with an average price of $125 and 30,000 three-day admission tickets with an average price of $280. The park

> Emmons Lawn Maintenance (ELM) provides lawn and garden care for residential properties. In the current year, ELM maintains 75 properties and earns an average of $5,000 annually for each property. The owner of ELM is planning for the coming year. New buil

> Write a memo to Megan Okoye outlining how you would recommend measuring “correct orders” for Silo Coffee and Tea. Be sure to discuss the advantages and disadvantages of your proposed measure.

> What is the advantage of preparing the flexible budget? The period is over and the actual results are known. Is this just extra work for the staff?

> Trombly Fabrication has three production facilities located in the state, each producing the same basic mix of products. Facility 1 was the original plant and the only one for several years. Facilities 2 and 3 were added recently to handle the increased

> Ternes Manufacturing produces metal products primarily used in the construction industry. The three main inputs in production are materials (metal), labor, and overhead. Data for the previous three reporting periods follow: Required a. Compute the total

> Cahalan is a network of clinics performing laser surgery for vision correction. Each clinic tracks the number of patients treated and the number of professional-hours spent on the laser patient procedure. Consultations, follow-up visits, and so on are tr

> Canfield Transition Centers is a not-for-profit organization to teach new technical skills to individuals looking to change careers. Canfield operates four campuses (Construction, Electrical, Plumbing, and Carpentry). Because the programs require all-day

> The controller’s staff at McNichols Lubricants is responsible for preparing quarterly performance reports. One report evaluates quarter-to-quarter improvement in partial productivity of the two main inputs in the production process: bas

> Top management at Reisener Corporation are looking to improve productivity in corporate staff functions. One area targeted for the initiative is the Human Resources (HR) department. The following data were collected for three relatively routine actions f

> RST Airlines operates call centers for customer service in four locations: Minneapolis, Phoenix, Boise, and Singapore. Although all four call centers can handle any inquiries, calls from elite customers are generally routed to the Boise center, and inter

> For each category of functional measures listed in Exhibit 18.9, add one additional specific measurement that is not already listed.

> Gordon Industries has the following mission statement: To be the low-cost leader in package delivery services. Gordon’s CEO tells you that the financial staff has developed the following initial balanced scorecard: Required Comment on t

> Romeyn Food Markets has decided to adopt a balanced scorecard to monitor performance. The company’s strategy is to be a provider of premium foods, sourced from local farms and nationally known organic suppliers. The initial scorecard re

> What is the advantage of recognizing materials price variances at the time of purchase rather than at the time of use?

> What are the advantages of the contribution margin format based on variable costing compared to the traditional format based on full absorption costing?