Question: Karen Johnson, CFO for Raucous Roasters (RR),

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her company’s working capital policy in light of a recent scare she faced when RR’s corporate banker, citing a nationwide credit crunch, balked at renewing RR’s line of credit. Had the line of credit not been renewed, RR would not have been able to make payroll, potentially forcing the company out of business. Although the line of credit was ultimately renewed, the scare has forced Johnson to examine carefully each component of RR’s working capital to make sure it is needed, with the goal of determining whether the line of credit can be eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit, Johnson is well aware that reducing working capital can also add value to a company by improving its EVA (Economic Value Added). In her corporate finance course Johnson learned that EVA is calculated by taking net operating profit after taxes (NOPAT) and then subtracting the dollar cost of all the capital the firm uses: EVA = NOPAT ( Capital costs

= EBIT (1 2 T) ( WACC (Total capital employed)

If EVA is positive, then the firm’s management is creating value. On the other hand, if EVA is negative, then the firm is not covering its cost of capital and stockholders’ value is being eroded. If RR could generate its current level of sales with fewer assets, it would need less capital. This would, other things held constant, lower capital costs and increase its EVA. Historically, RR has done little to examine working capital, mainly because of poor communication among business functions. In the past, the production manager resisted Johnson’s efforts to question his holdings of raw materials, the marketing manager resisted questions about finished goods, the sales staff resisted questions about credit policy (which affects accounts receivable), and the treasurer did not want to talk about the cash and securities balances. However, with the recent credit scare, this resistance became unacceptable and Johnson has undertaken a company-wide examination of cash, marketable securities, inventory, and accounts receivable levels.

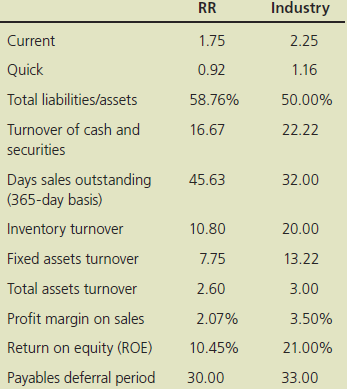

Johnson also knows that decisions about working capital cannot be made in a vacuum. For example, if inventories could be lowered without adversely affecting operations, then less capital would be required, the dollar cost of capital would decline, and EVA would increase. However, lower raw materials inventories might lead to production slowdowns and higher costs, and lower finished goods inventories might lead to stock-outs and loss of sales. So, before inventories are changed, it will be necessary to study operating as well as financial effects. The situation is the same with regard to cash and receivables. Johnson has begun her investigation by collecting the ratios shown below.

a. Johnson plans to use the preceding ratios as the starting point for discussions with RR’s operating team. She wants everyone to think about the pros and cons of changing each type of current asset and how changes would interact to affect profits and EVA. Based on the data, does RR seem to be following a relaxed, moderate, or restricted working capital policy?

b. How can one distinguish between a relaxed but rational working capital policy and a situation in which a firm simply has excessive current assets because it is inefficient? Does RR’s working capital policy seem appropriate?

c. Calculate the firm’s cash conversion cycle given that annual sales are $660,000 and cost of goods sold represents 90% of sales. Assume a 365-day year.

d. What might RR do to reduce its cash without harming operations?

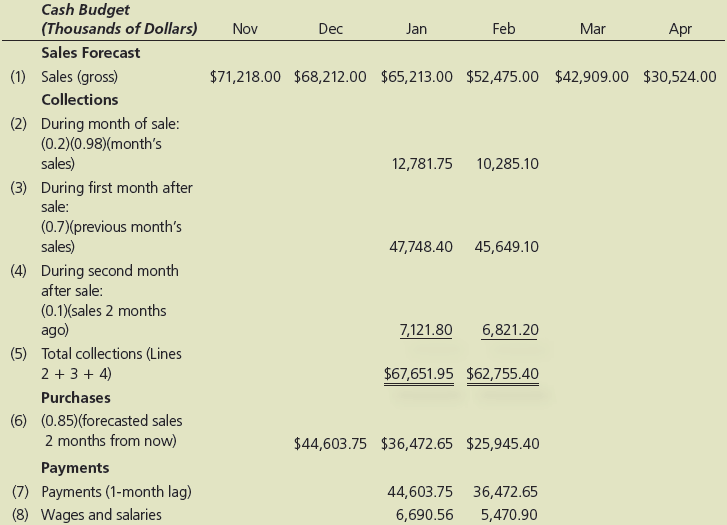

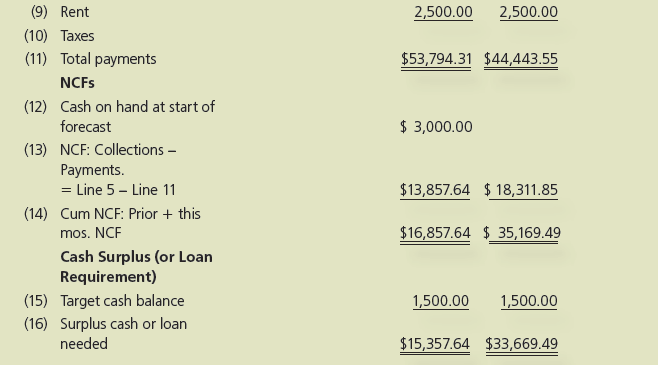

e. In an attempt to better understand RR’s cash position, Johnson developed a cash budget for the first 2 months of the year. This budget appears on the next page. She has the figures for the other months, but they are not shown. Should depreciation expense be explicitly included in the cash budget? Why or why not?

f. In her preliminary cash budget, Johnson has assumed that all sales are collected and thus that RR has no bad debts. Is this realistic? If not, how would bad debts be dealt with in a cash budgeting sense? (Hint: Bad debts will affect collections but not purchases.)

g. Johnson’s cash budget for the entire year, although not given here, is based heavily on her forecast for monthly sales. Sales are expected to be extremely low between May and September but then to increase dramatically in the fall and winter. November is typically the firm’s best month, when RR ships its holiday blend of coffee. Johnson’s forecasted cash budget indicates that the company’s cash holdings will exceed the targeted cash balance every month except for October and November, when shipments will be high but collections will not be coming in until later. Based on the ratios shown earlier, does it appear that RR’s target cash balance is appropriate? In addition to possibly lowering the target cash balance, what actions might RR take to better improve its cash management policies, and how might that affect its EVA?

h. What reasons might RR have for maintaining a relatively high amount of cash?

i. Is there any reason to think that RR may be holding too much inventory? If so, how would that affect EVA and ROE?

j. If the company reduces its inventory without adversely affecting sales, what effect should this have on the company’s cash position:

(1) in the short run and

(2) in the long run? Explain in terms of the cash budget and the balance sheet.

k. Johnson knows that RR sells on the same credit terms as other firms in its industry. Use the ratios presented earlier to explain whether RR’s customers pay more or less promptly than those of its competitors. If there are differences, does that suggest RR should tighten or loosen its credit policy? What four variables make up a firm’s credit policy, and in what direction should each be changed by RR?

l. Does RR face any risks if it tightens its credit policy?

m. If the company reduces its DSO without seriously affecting sales, what effect would this have on its cash position:

(1) in the short run and

(2) in the long run? Answer in terms of the following cases budget and the balance sheet. What effect should this have on EVA in the long run?

n. In addition to improving the management of its current assets, RR is also reviewing the ways in which it finances its current assets. Is it likely that RR could make significantly greater use of accruals?

o. Assume that RR purchases $200,000 (net of discounts) of materials on terms of 1/10, net 30, but that it can get away with paying on the 40th day if it chooses not to take discounts. How much free trade credit can the company get from its equipment supplier, how much costly trade credit can it get, and what is the nominal annual interest rate of the costly credit? Should RR take discounts?

p. RR tries to match the maturity of its assets and liabilities. Describe how RR could adopt either a more aggressive or a more conservative financing policy.

q. What are the advantages and disadvantages of using short-term debt as a source of financing? r. Would it be feasible for RR to finance with commercial paper?

Transcribed Image Text:

RR Industry Current 1.75 2.25 Quick 0.92 1.16 Total liabilities/assets 58.76% 50.00% Turnover of cash and 16.67 22.22 securities Days sales outstanding (365-day basis) 45.63 32.00 Inventory turnover 10.80 20.00 Fixed assets turnover 7.75 13.22 Total assets turnover 2.60 3.00 Profit margin on sales 2.07% 3.50% Return on equity (ROE) 10.45% 21.00% Payables deferral period 30.00 33.00 Cash Budget (Thousands of Dollars) Nov Dec Jan Feb Mar Apr Sales Forecast (1) Sales (gross) $71,218.00 $68,212.00 $65,213.00 $52,475.00 $42,909.00 $30,524.00 Collections (2) During month of sale: (0.2)(0.98)(month's sales) 12,781.75 10,285.10 (3) During first month after sale: (0.7)(previous month's sales) 47,748.40 45,649.10 (4) During second month after sale: (0.1)(sales 2 months ago) 7,121.80 6,821.20 (5) Total collections (Lines 2 + 3 + 4) $67,651.95 $62,755.40 Purchases (6) (0.85)(forecasted sales 2 months from now) $44,603.75 $36,472.65 $25,945.40 Payments (7) Payments (1-month lag) 44,603.75 36,472.65 (8) Wages and salaries 6,690.56 5,470.90 (9) Rent 2,500.00 2,500.00 (10) Taxes (11) Total payments $53,794.31 $44,443.55 NCFS (12) Cash on hand at start of forecast $ 3,000.00 (13) NCF: Collections – Payments. = Line 5 – Line 11 $13,857.64 $ 18,311.85 (14) Cum NCF: Prior + this mos. NCF $16,857.64 $ 35,169.49 Cash Surplus (or Loan Requirement) (15) Target cash balance (16) Surplus cash or loan needed 1,500.00 1,500.00 $15,357.64 $33,669.49

> Exchange rates fluctuate under both the fixed exchange rate and floating exchange rate systems. What, then, is the difference between the two systems?

> With the growth in demand for exotic foods, Possum Products’ CEO Michael Munger is considering expanding the geographic footprint of its line of dried and smoked low-fat opossum, ostrich, and venison jerky snack packs. Historically, jer

> Under the fixed exchange rate system, what was the currency against which all other currency values were defined? Why?

> Kimberly MacKenzie—president of Kim’s Clothes Inc., a medium-sized manufacturer of women’s casual clothing—is worried. Her firm has been selling clothes to Russ Brothers Department S

> SafeCo can issue floating-rate debt at LIBOR + 1% or fixed-rate debt at 8%, but it would prefer to use fixed-rate debt. RiskyCo can issue floating- rate debt at LIBOR + 2% or fixed-rate debt at 8.8%, but it would prefer to use floating rate debt. Explain

> Zhao Automotive issues fixed-rate debt at a rate of 7.00%. Zhao agrees to an interest rate swap in which it pays LIBOR to Lee Financial and Lee pays 6.8% to Zhao. What is Zhao’s resulting net payment?

> Are liquidations likely to be more common for public utility, railroad, or industrial corporations? Why or why not?

> Would it be a sound rule to liquidate whenever the liquidation value is above the value of the corporation as a going concern? Discuss.

> Distinguish between operating mergers and financial mergers.

> Why do creditors usually accept a plan for financial rehabilitation rather than demand liquidation of the business?

> a. Informal restructuring; reorganization in bankruptcy b. Assignment; liquidation in bankruptcy; fairness; feasibility c. Absolute priority doctrine; relative priority doctrine d. Bankruptcy Reform Act of 1978; Chapter 11; Chapter 7 e. Priority of claim

> Why do liquidations usually result in losses for the creditors or the owners, or both? Would partial liquidation or liquidation over a period limit their losses? Explain.

> a. Derivatives b. Enterprise risk management c. Financial futures; forward contract d. Hedging; natural hedge; long hedge; short hedge; perfect hedge; symmetric hedge; asymmetric hedge e. Swap; structured note f. Commodity futures

> How can swaps be used to reduce the risks associated with debt contracts?

> Explain how the futures markets can be used to reduce interest rate risk and contracts?

> Explain how the EOQ inventory model can be modified and used to help determine the optimal size of a firm’s cash balances. Do you think the EOQ approach to cash management is more or less relevant today than it was in precomputer, preelectronic communica

> Explain briefly what the EOQ model is and how it can be used to help establish an optimal inventory policy. Is the EOQ concept consistent with just-in-time procedures for managing inventories?

> The Gentry Garden Center sells 90,000 bags of lawn fertilizer annually. The optimal safety stock (which is on hand initially) is 1,000 bags. Each bag costs the firm $1.50, inventory carrying cost is 20%, and the cost of placing an order with its supplier

> Barenbaum Industries projects that cash outlays of $4.5 million will occur uniformly throughout the year. Barenbaum plans to meet its cash requirements by periodically selling marketable securities from its portfolio. The firm’s marketable securities are

> Firm a wants to acquire Firm B. Firm B’s management agrees that the merger is a good idea. Might a tender offer be used? Why or why not?

> Indicate by a (+), (_), or (0) whether each of the following events would probably cause average annual inventory holdings to rise, fall, or be affected in an indeterminate manner: a. Our suppliers change from delivering by trainto air freight. ________

> a. Baumol model b. Total carrying cost; total ordering cost; total inventory costs c. Economic Ordering Quantity (EOQ); EOQ model; EOQ range d. Reorder point; safety stock e. Red-line method; two-bin method; computerized inventory control system f. Just-

> Explain how each of the following factors would probably affect a firm’s target cash balance if all other factors were held constant. a. The firm institutes a new billing procedure that better synchronizes its cash inflows and outflows. b. The firm devel

> Malone Feed and Supply Company buys on terms of 1/10, net 30, but it has not been taking discounts and has actually been paying in 60 rather than 30 days. Assume that the accounts payable are recorded at full cost, not net of discounts. Maloneâ

> The Russ Fogler Company, a small manufacturer of cordless telephones, began operations on January 1. Its credit sales for the first 6 months of operations were as follows: Throughout this entire period, the firm’s credit customers maint

> Yonge Corporation must arrange financing for its working capital requirements for the coming year. Yonge can: (a) borrow from its bank on a simple interest basis (interest payable at the end of the loan) for 1 year at a 12% nominal rate; (b) borrow on a

> Kim Mitchell, the new credit manager of the Vinson Corporation, was alarmed to find that Vinson sells on credit terms of net 90 days while industry-wide credit terms have recently been lowered to net 30 days. On annual credit sales of $2.5 million, Vinso

> The Boyd Corporation has annual credit sales of $1.6 million. Current expenses for the collection department are $35,000, bad-debt losses are 1.5%, and the days sales outstanding is 30 days. The firm is considering easing its collection efforts such that

> Gifts Galore Inc. borrowed $1.5 million from National City Bank. The loan was made at a simple annual interest rate of 9% a year for 3 months. A 20% compensating balance requirement raised the effective interest rate. a. The nominal annual rate on the lo

> Del Hawley, owner of Hawley’s Hardware, is negotiating with First City Bank for a 1-year loan of $50,000. First City has offered Hawley the alternatives listed below. Calculate the effective annual interest rate for each alternative. Which alternative ha

> Four economic classifications of mergers are: (1) horizontal, (2) vertical, (3) conglomerate, and (4) congeneric. Explain the significance of these terms in merger analysis with regard to (a) the likelihood of governmental intervention and (b) possibi

> Mary Jones recently obtained an equipment loan from a local bank. The loan is for $15,000 with a nominal interest rate of 11%. However, this is an installment loan, so the bank also charges add-on interest. Mary must make monthly payments on the loan, an

> Suncoast Boats Inc. estimates that, because of the seasonal nature of its business, it will require an additional $2 million of cash for the month of July. Suncoast Boats has the following four options available for raising the needed funds. 1. Establis

> What is the cash conversion cycle (CCC)? Why it better, other things held constant, to have a shorter rather than a longer CCC? Suppose you know a company’s annual sales, average inventories, average accounts receivable, average accounts payable, and ann

> Define the terms aggressive and conservative when applied to financing, give examples of each, and then discuss the pros and cons of each approach. Would you expect to find entrenched firms in monopolistic (or oligopolistic) industries leaning more towar

> What are some advantages of matching the maturities of claims against assets with the lives of the assets financed by those claims? Is it feasible for a firm to match perfectly the maturities of all assets and claims against assets? Why might a firm deli

> Differentiate between free and costly trade credit. What is the formula for determining the nominal annual cost rate associated with a credit policy? What is the formula for the effective annual cost rate? How would these cost rates be affected if a firm

> What is a cash budget, and how is this statement used by a business? How is the cash budget affected by the CCC? By credit policy?

> Lewis Securities Inc. has decided to acquire a new market data and quotation system for its Richmond home office. The system receives current market prices and other information from several online data services and then either displays the information o

> Define each of the following terms: a. Cash discounts b. Seasonal dating c. Aging schedule; days sales outstanding (DSO) d. Payments pattern approach; uncollected balances schedule e. Simple interest; discount interest; add-on interest

> Indicate by a (1), (2), or (0) whether each of the following events would most likely cause accounts receivable (AR), sales, and profits to increase, decrease, or be affected in an indeterminate manner: AR Sales Profits The firm tightens its credit s

> a. Synergy; merger b. Horizontal merger; vertical merger; congeneric merger; conglomerate merger c. Friendly merger; hostile merger; defensive merger; tender offer; target company; breakup value; acquiring company d. Operating merger; financial merger e.

> What are the two principal reasons for holding cash? Can a firm estimate its target cash balance by summing the cash held to satisfy each of the two reasons?

> Discuss this statement: “Firms can control their accruals within fairly wide limits.”

> Is it true that, when one firm sells to another on credit, the seller records the transaction as an account receivable while the buyer records it as an account payable and that, disregarding discounts, the receivable typically exceeds the payable by the

> What is a convertible? If a company decides to raise capital by issuing convertible bonds, how would the terms on the bond be set? Consider specifically the maturity, coupon rate, and call features of the bond, as well as the conversion price (or convers

> What is a warrant? If a company decides to raise capital by issuing bonds with warrants, how would the terms on both the bond and the warrant be set? Consider in particular how the coupon rate and maturity of the bond would be related to the exercise pri

> If a company is thinking about issuing preferred stock to raise capital, what are some factors that it should consider? What factors should an investor consider before buying preferred stock?

> Suppose you just bought a convertible bond at its par value. Your broker gives you information on the bond’s conversion ratio, coupon rate, maturity, years of call protection, and the yield on nonconvertible bonds of similar risk and maturity. The compan

> Paul Duncan, financial manager of EduSoft Inc., is facing a dilemma. The firm was founded 5 years ago to provide educational software for the rapidly expanding primary and secondary school markets. Although EduSoft has done well, the firm’s founder belie

> Define each of the following terms: a. Lessee; lessor b. Operating lease; financial lease; sale-and-leaseback; combination lease; synthetic lease; SPE c. Off–balance sheet financing; capitalizing d. FASB Statement 13 e. Guideline lease f. Residual value

> Distinguish between the APV, FCFE, and corporate valuation models.

> What is interest rate parity? How might the treasurer of a multinational firm use the interest rate parity concept: (a) when deciding how to invest the firm’s surplus cash and (b) when deciding where to borrow funds on a short-term basis?

> In our Anderson Company example, we assumed that the lease could not be canceled. What effect would a cancellation clause have on the lessee’s analysis? On the lessor’s analysis?

> Suppose Congress enacted new tax law changes that would: (1) permit equipment to be depreciated over a shorter period, (2) lower corporate tax rates, and (3) reinstate the investment tax credit. Discuss how each of these potential changes would affect

> Suppose there were no IRS restrictions on what constituted a valid lease. Explain, in a manner a legislator might understand, why some restrictions should be imposed. Illustrate your answer with numbers.

> One advantage of leasing voiced in the past is that it kept liabilities off the balance sheet, thus making it possible for a firm to obtain more leverage than it otherwise could have. This raised the question of whether or not both the lease obligation a

> Commercial banks moved heavily into equipment leasing during the early 1970s, acting as lessors. One major reason for this invasion of the leasing industry was to gain the benefits of accelerated depreciation and the investment tax credit on leased equip

> Are lessees more likely to be in higher or lower income tax brackets than lessors?

> Distinguish between operating leases and financial leases. Would you be more likely to find an operating lease employed for a fleet of trucks or for a manufacturing plant?

> Is it true that most firms are able to obtain some free trade credit and that additional trade credit is often available, but at a cost? Explain.

> From the standpoint of the borrower, is long-term or short-term credit riskier? Explain. Would it ever make sense to borrow on a short-term basis if short-term rates were above long-term rates?

> What are the advantages of matching the maturities of assets and liabilities? What are the disadvantages?

> What is a futures contract, and how are futures used to manage risk? What are you protecting against if you buy Treasury futures contracts? What if you sell Treasury futures short?

> What are the four elements of a firm’s credit policy? To what extent can firms set their own credit policies as opposed to accepting policies that are dictated by its competitors?

> Define each of the following terms: a. Working capital; net working capital; net operating working capital b. Relaxed policy; restricted policy; moderate policy c. Permanent operating current assets; temporary operating current assets d. Moderate (maturi

> What kinds of firms use commercial paper?

> The Thompson Corporation projects an increase in sales from $1.5 million to $2 million, but it needs an additional $300,000 of current assets to support this expansion. Thompson can finance the expansion by no longer taking discounts, thus increasing acc

> Suppose a firm makes purchases of $3.65 million per year under terms of 2/10, net 30, and takes discounts. a. What is the average amount of accounts payable net of discounts? (Assume the $3.65 million of purchases is net of discounts—that is, gross purc

> Dorothy Koehl recently leased space in the Southside Mall and opened a new business, Koehl’s Doll Shop. Business has been good, but Koehl frequently runs out of cash. This has necessitated late payment on certain orders, which is beginn

> Payne Products had $1.6 million in sales revenues in the most recent year and expects sales growth to be 25% this year. Payne would like to determine the effect of various current assets policies on its financial performance. Payne has $1 million of fixe

> Strickler Technology is considering changes in its working capital policies to improve its cash flow cycle. Strickler’ss sales last year were $3,250,000 (all on credit), and its net profit margin was 7%. Its inventory turnover was 6.0 times during the ye

> Negus Enterprises has an inventory conversion period of 50 days, an average collection period of 35 days, and a payables deferral period of 25 days. Assume that cost of goods sold is 80% of sales. a. What is the length of the firm’s cash conversion cycle

> Grunewald Industries sells on terms of 2/10, net 40. Gross sales last year were $4,562,500 and accounts receivable averaged $437,500. Half of Grunewald’s customers paid on the 10th day and took discounts. What are the nominal and effective costs of trade

> What types of risks are interest-rate and exchange rate swaps designed to mitigate? Why might one company prefer fixed-rate payments while another company prefers floating-rate payments, or payments in one currency versus another?

> a. If a firm buys under terms of 3/15, net 45, but actually pays on the 20th day and still takes the discount, what is the nominal cost of its nonfree trade credit? b. Does it receive more or less credit than it would if it paid within 15 days?

> Snider Industries sells on terms of 2/10, net 45. Total sales for the year are $1,500,000. Thirty percent of customers pay on the 10th day and take discounts; the other 70% pay, on average, 50 days after their purchases. a. What is the days sales outstan

> What is the nominal and effective cost of trade credit under the credit terms of 3/15, net 30?

> Williams & Sons last year reported sales of $10 million and an inventory turnover ratio of 2. The company is now adopting a new inventory system. If the new system is able to reduce the firm’s inventory level and increase the firm’s inventory turnover ra

> The Raattama Corporation had sales of $3.5 million last year, and it earned a 5% return (after taxes) on sales. Recently, the company has fallen behind in its accounts payable. Although its terms of purchase are net 30 days, its accounts payable represen

> Why do companies use so many different types of instruments to raise capital? Why not just use debt and common stock?

> Define each of the following terms: a. Preferred stock b. Cumulative dividends; arrearages c. Warrant; detachable warrant d. Stepped-up price e. Convertible security f. Conversion ratio; conversion price; conversion value g. Sweetener

> Suppose a company simultaneously issues $50 million of convertible bonds with a coupon rate of 10% and $50 million of straight bonds with a coupon rate of 14%. Both bonds have the same maturity. Does the convertible issue’s lower coupon rate suggest that

> Evaluate the following statement: “Issuing convertible securities is a means by which a firm can sell common stock for more than the existing market price.”

> How does a firm’s dividend policy affect each of the following? a. The value of its long-term warrants b. The likelihood that its convertible bonds will be converted c. The likelihood that its warrants will be exercised

> What does it mean to “manage” risk? Should its stockholders want a firm to “manage” all of the risks it faces?

> If a firm expects to have additional financial requirements in the future, would you recommend that it use convertibles or bonds with warrants? What factors would influence your decision?

> What effect does the trend in stock prices (subsequent to issue) have on a firm’s ability to raise funds through: (a) convertibles and (b) warrants?

> Is preferred stock more like bonds or common stock? Explain.

> The Howland Carpet Company has grown rapidly during the past 5 years. Recently, its commercial bank urged the company to consider increasing its permanent financing. Its bank loan under a line of credit has risen to $250,000, carrying an 8% interest rate

> Fifteen years ago, Roop Industries sold $400 million of convertible bonds. The bonds had a 40-year maturity, a 5.75% coupon rate, and paid interest annually. They were sold at their $1,000 par value. The conversion price was set at $62.75, and the common

> The Tsetsekos Company was planning to finance an expansion. The principal executives of the company all agreed that an industrial company such as theirs should finance growth by means of common stock rather than by debt. However, they felt that the curre

> Maese Industries Inc. has warrants outstanding that permit the holders to purchase 1 share of stock per warrant at a price of $25. a. Calculate the exercise value of the firm’s warrants if the common sells at each of the following prices: (1) $20, (2) $2

> Neubert Enterprises recently issued $1,000 par value 15-year bonds with a 5% coupon paid annually and warrants attached. These bonds are currently trading for $1,000. Neubert also has outstanding $1,000 par value 15-year straight debt with a 7% coupon pa

> Niendorf Incorporated needs to raise $25 million to construct production facilities for a new type of USB memory device. The firm’s straight nonconvertible debentures currently yield 9%. Its stock sells for $23 per share, has an expected constant growth

> Stohs Semiconductor Corporation plans to issue $50 million of 20-year bonds in 6 months. The interest rate would be 9% if the bonds were issued today. How can Stohs set up a hedge against an increase in interest rates over the next 6 months? Assume that

> Big Sky Mining Company must install $1.5 million of new machinery in its Nevada mine. It can obtain a bank loan for 100% of the purchase price, or it can lease the machinery. Assume that the following facts apply. 1. The machinery falls into the MACRS 3

> Two companies, Energen and Hastings Corporation, began operations with identical balance sheets. A year later, both required additional fixed assets at a cost of $50,000. Energen obtained a 5-year, $50,000 loan at an 8% interest rate from its bank. Hasti

> Consider the data in Problem 19-1. Assume that Reynolds’ tax rate is 40% and that the equipment’s depreciation would be $100 per year. If the company leased the asset on a 2-year lease, the payment would be $110 at the beginning of each year. If Reynolds

> Reynolds Construction needs a piece of equipment that costs $200. Reynolds can either lease the equipment or borrow $200 from a local bank and buy the equipment. If the equipment is leased, the lease would not have to be capitalized. Reynoldsâ€