Question: Kellogg Company in its 2004 Annual Report

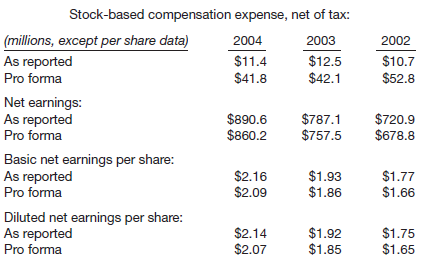

Kellogg Company in its 2004 Annual Report in Note 1—Accounting Policies made the comment on page 962 about its accounting for employee stock options and other stock-based compensation. This was the annual report issued the year before the FASB mandated expensing stock options.

Stock compensation (in part) The Company currently uses the intrinsic value method prescribed by Accounting Principles Board Opinion (APB) No. 25, “Accounting for Stock Issued to Employees,†to account for its employee stock options and other stock-based compensation. Under this method, because the exercise price of the Company’s employee stock options equals the market price of the underlying stock on the date of the grant, no compensation expense is recognized. The following table presents the pro forma results for the current and prior years, as if the Company had used the alternate fair value method of accounting for stock-based compensation, prescribed by SFAS No. 123, “Accounting for Stock-Based Compensation†(as amended by SFAS No. 148).

Under this pro forma method, the fair value of each option grant (net of estimated unvested forfeitures) was estimated at the date of grant using an option-pricing model and was recognized over the vesting period, generally two years. Refer to Note 8 for further information on the Company’s stock compensation programs. In December 2004, the FASB issued SFAS No. 123(Revised), “Share-Based Payment,†which generally requires public companies to measure the cost of employee services received in exchange for an award of equity instruments based on the grant-date fair value and to recognize this cost over the requisite service period. The Company plans to adopt SFAS No. 123(Revised), as of the beginning of its 2005 fiscal third quarter and is currently considering retrospective restatement to the beginning of its 2005 fiscal year. Once this standard is adopted, management believes full-year fiscal 2005 net earnings per share will be reduced by approximately $.08.

Instructions

(a) Briefly discuss how Kellogg’s financial statements were affected by the adoption of the new standard.

(b) Some companies argued that the recognition provisions of the standard are not needed because the computation of earnings per share takes into account dilutive securities such as stock options. Do you agree? Explain, using the Kellogg disclosure provided above.

Transcribed Image Text:

Stock-based compensation expense, net of tax: (millions, except per share data) 2004 2003 2002 As reported Pro forma $11.4 $41.8 $12.5 $42.1 $10.7 $52.8 Net earnings: As reported Pro forma $890.6 $860.2 $787.1 $757.5 $720.9 $678.8 Basic net earnings per share: As reported Pro forma $2.16 $2.09 $1.93 $1.86 $1.77 $1.66 Diluted net earnings per share: As reported Pro forma $2.14 $2.07 $1.92 $1.85 $1.75 $1.65

> Clemson Company had the following stockholders’ equity as of January 1, 2012. Common stock, $5 par value, 20,000 shares issued …………………….. $100,000 Paid-in capital in excess of par—common stock …………………………….. 300,000 Retained earnings ………………………………………………………

> On January 5, 2012, Phelps Corporation received a charter granting the right to issue 5,000 shares of $100 par value, 8% cumulative and nonparticipating preferred stock, and 50,000 shares of $10 par value common stock. It then completed these transaction

> Hagar Company has outstanding 2,500 shares of $100 par, 6% preferred stock and 15,000 shares of $10 par value common. The schedule below shows the amount of dividends paid out over the last 4 years. Instructions Allocate the dividends to each type of st

> Petrenko Corporation has outstanding 2,000 $1,000 bonds, each convertible into 50 shares of $10 par value ordinary shares. The bonds are converted on December 31, 2012. The bonds payable has a carrying value of $1,950,000 and conversion equity of $20,000

> Explain how convertible securities are determined to be potentially dilutive common shares and how those convertible securities that are not considered to be potentially dilutive common shares enter into the determination of earnings per share data.

> Martinez Company’s ledger shows the following balances on December 31, 2012. Preferred Stock (5%; $10 par value, outstanding 20,000 shares) ………….. $ 200,000 Common Stock ($100 par value, outstanding 30,000 shares) ………………. 3,000,000 Retained Earnings …………

> The outstanding capital stock of Pennington Corporation consists of 2,000 shares of $100 par value, 6% preferred, and 5,000 shares of $50 par value common. Instructions Assuming that the company has retained earnings of $70,000, all of which is to be pa

> Presented below is information from the annual report of Potter Plastics, Inc. Operating income ……………………………… $ 532,150 Bond interest expense ………………………….. 135,000 …………………………………………………………… 397,150 Income taxes ………………………………………. 183,432 Net income ……………………………

> Shown below is the liabilities and stockholders’ equity section of the balance sheet for Ingalls Company and Wilder Company. Each has assets totaling $4,200,000. For the year, each company has earned the same income before interest an

> Elizabeth Company reported the following amounts in the stockholders’ equity section of its December 31, 2012, balance sheet. Preferred stock, 8%, $100 par (10,000 shares authorized, 2,000 shares issued) ……. $200,000 Common stock, $5 par (100,000 shares

> Teller Corporation’s post-closing trial balance at December 31, 2012, was as follows. At December 31, 2012, Teller had the following number of common and preferred shares. The dividends on preferred stock are $4 cumulative. In addit

> The following information has been taken from the ledger accounts of Sampras Corporation. Total income since incorporation ……………………………………. $287,000 Total cash dividends paid …………………………………………………… 60,000 Total value of stock dividends distributed ………………………

> The following data were taken from the balance sheet accounts of Wickham Corporation on December 31, 2012. Current assets …………………………………………………………….. $540,000 Debt investments ………………………………………………………….. 624,000 Common stock (par value $10) ………………………………………. 6

> The stockholders’ equity accounts of Lawrence Company have the following balances on December 31, 2012. Common stock, $10 par, 200,000 shares issued and outstanding ……………. $2,000,000 Paid-in capital in excess of par—common stock ………………………………………… 1,200,00

> Teller Corporation’s post-closing trial balance at December 31, 2012, was as follows. At December 31, 2012, Teller had the following number of ordinary and preference shares. The dividends on preference shares are $4 cumulative. In

> The common stock of Warner Inc. is currently selling at $110 per share. The directors wish to reduce the share price and increase share volume prior to a new issue. The per share par value is $10; book value is $70 per share. Five million shares are issu

> What are the principal considerations of a board of directors in making decisions involving dividend declarations? Discuss briefly.

> Addison Corporation has 10 million shares of common stock issued and outstanding. On June 1, the board of directors voted a 60 cents per share cash dividend to stockholders of record as of June 14, payable June 30. Instructions (a) Prepare the journal e

> The following are selected transactions that may affect stockholders’ equity. 1. Recorded accrued interest earned on a note receivable. 2. Declared and distributed a stock split. 3. Declared a cash dividend. 4. Recorded a retained earni

> For a recent 2-year period, the balance sheet of Franklin Company showed the following stockholders’ equity data at December 31 in millions. Instructions (a) Answer the following questions. (1) What is the par value of the common stoc

> Davison Inc. recently hired a new accountant with extensive experience in accounting for partnerships. Because of the pressure of the new job, the accountant was unable to review what he had learned earlier about corporation accounting. During the first

> Weisberg Corporation has 10,000 shares of $100 par value, 6% preferred stock and 50,000 shares of $10 par value common stock outstanding at December 31, 2012. Instructions Answer the questions in each of the following independent situations. (a) If the

> Sanborn Company has outstanding 40,000 shares of $5 par common stock which had been issued at $30 per share. Sanborn then entered into the following transactions. 1. Purchased 5,000 treasury shares at $45 per share. 2. Resold 500 of the treasury shares a

> Loxley Corporation is authorized to issue 50,000 shares of $10 par value common stock. During 2012, Loxley took part in the following selected transactions. 1. Issued 5,000 shares of stock at $45 per share, less costs related to the issuance of the stock

> Hartman Inc. issues 500 shares of $10 par value common stock and 100 shares of $100 par value preferred stock for a lump sum of $100,000. Instructions (a) Prepare the journal entry for the issuance when the market price of the common shares is $168 each

> Cordero Corporation has an employee share-purchase plan which permits all full-time employees to purchase 10 ordinary shares on the third anniversary of their employment and an additional 15 shares on each subsequent anniversary date. The purchase price

> Fogelberg Corporation is a regional company which is an SEC registrant. The corporation’s securities are thinly traded on NASDAQ (National Association of Securities Dealers Quotes). Fogelberg has issued 10,000 units. Each unit consists of a $500 par, 12%

> Twenty-five thousand shares reacquired by Pierce Corporation for $48 per share were exchanged for undeveloped land that has an appraised value of $1,700,000. At the time of the exchange, the common stock was trading at $60 per share on an organized excha

> What are the computational guidelines for determining whether a convertible security is to be reported as part of diluted earnings per share?

> Abernathy Corporation was organized on January 1, 2012. It is authorized to issue 10,000 shares of 8%, $50 par value preferred stock, and 500,000 shares of no-par common stock with a stated value of $2 per share. The following stock transactions were com

> During its first year of operations, Sitwell Corporation had the following transactions pertaining to its common stock. Jan. 10 Issued 80,000 shares for cash at $6 per share. Mar. 1 Issued 5,000 shares to attorneys in payment of a bill for $35,000 for se

> Nottebart Corporation has outstanding 10,000 shares of $100 par value, 6% preferred stock and 60,000 shares of $10 par value common stock. The preferred stock was issued in January 2012, and no dividends were declared in 2012 or 2013. In 2014, Nottebart

> Use the information from BE15-13, but assume Green Day Corporation declared a 100% stock dividend rather than a 5% stock dividend. Prepare the journal entries for both the date of declaration and the date of distribution. In BE15-13 Green Day Corporatio

> Green Day Corporation has outstanding 400,000 shares of $10 par value common stock. The corporation declares a 5% stock dividend when the fair value of the stock is $65 per share. Prepare the journal entries for Green Day Corporation for both the date of

> Graves Mining Company declared, on April 20, a dividend of $500,000 payable on June 1. Of this amount, $125,000 is a return of capital. Prepare the April 20 and June 1 entries for Graves.

> Cole Inc. owns shares of Marlin Corporation stock classified as available-for-sale securities. At December 31, 2012, the available-for-sale securities were carried in Cole’s accounting records at their cost of $875,000, which equals their fair value. On

> Ravonette Corporation issued 300 shares of $10 par value ordinary shares and 100 shares of $50 par value preference shares for a lump sum of $13,500. The ordinary shares have a market price of $20 per share, and the preference shares have a market price

> Woolford Inc. declared a cash dividend of $1.00 per share on its 2 million outstanding shares. The dividend was declared on August 1, payable on September 9 to all stockholders of record on August 15. Prepare all journal entries necessary on those three

> Hinges Corporation issued 500 shares of $100 par value preferred stock for $61,500. Prepare Hinges’s journal entry.

> Arantxa Corporation has outstanding 20,000 shares of $5 par value common stock. On August 1, 2012, Arantxa reacquired 200 shares at $80 per share. On November 1, Arantxa reissued the 200 shares at $70 per share. Arantxa had no previous treasury stock tra

> Indicate how each of the following accounts should be classified in the equity section. (a) Share Capital—Ordinary (b) Retained Earnings (c) Share Premium—Ordinary (d) Treasury Shares (e) Share Premium—Treasury (f) Share Capital—Preference (g) Accumulate

> Explain each of the following terms: authorized ordinary shares, unissued ordinary shares, issued ordinary shares, outstanding ordinary shares, and treasury shares.

> Mary Tokar is comparing a GAAP-based company to a company that uses IFRS. Both companies report equity investments. The IFRS company reports unrealized losses on these investments under the heading “Reserves” in its equity section. However, Mary can find

> Briefly discuss the implications of the financial statement presentation project for the reporting of stockholders’ equity.

> In this simulation, you are asked to address questions related to the accounting for stock options and earnings per share computations. Prepare responses to all parts. KWW_Professional_Simulation Stock Options and EPS Time Remaining 3 hours 50 minut

> Richardson Company is contemplating the establishment of a share-based compensation plan to provide long-run incentives for its top management. However, members of the compensation committee of the board of directors have voiced some concerns about adopt

> On January 1, 2011, Garner issued 10-year, $200,000 face value, 6% bonds at par. Each $1,000 bond is convertible into 30 shares of Garner $2 par value common stock. The company has had 10,000 shares of common stock (and no preferred stock) outstanding th

> Sepracor, Inc., a drug company, reported the following information. The company prepares its financial statements in accordance with GAAP. __________________________2007 (,000) Current liabilities …………………………………… $ 554,114 Convertible subordinated debt ……

> Briggs and Stratton recently reported unamortized debt issue costs of $5.1 million. How should the costs of issuing these bonds be accounted for and classified in the financial statements?

> Go to the book’s companion website and use information found there to answer the following questions related to The Coca-Cola Company and PepsiCo, Inc. (a) What employee stock-option compensation plans are offered by Coca-Cola and PepsiCo? (b) How many o

> Over what period of time should compensation cost be allocated?

> The financial statements of P&G are presented in Appendix 5B or can be accessed at the book’s companion website, www.wiley.com/college/kieso. Instructions Refer to P&G’s financial statements and accompanying notes to answer the following questions. (a)

> Brad Dolan, a stockholder of Rhode Corporation, has asked you, the firm’s accountant, to explain why his stock warrants were not included in diluted EPS. In order to explain this situation, you must briefly explain what dilutive securities are, why they

> Chorkina Corporation, a new audit client of yours, has not reported earnings per share data in its annual reports to stockholders in the past. The treasurer, Beth Botsford, requested that you furnish information about the reporting of earnings per share

> “Earnings per share” (EPS) is the most featured, single financial statistic about modern corporations. Daily published quotations of stock prices have recently been expanded to include for many securities a “times earnings” figure that is based on EPS. S

> The following two items appeared on the Internet concerning the GAAP requirement to expense stock options. WASHINGTON, D.C.—February 17, 2005 Congressman David Dreier (R–CA), Chairman of the House Rules Committee, and Congresswoman Anna Eshoo (D–CA) rein

> For various reasons a corporation may issue warrants to purchase shares of its common stock at specified prices that, depending on the circumstances, may be less than, equal to, or greater than the current market price. For example, warrants may be issue

> The executive officers of Rouse Corporation have a performance-based compensation plan. The performance criteria of this plan is linked to growth in earnings per share. When annual EPS growth is 12%, the Rouse executives earn 100% of the shares; if growt

> Sprinkle Inc. has outstanding 10,000 shares of $10 par value common stock. On July 1, 2012, Sprinkle reacquired 100 shares at $87 per share. On September 1, Sprinkle reissued 60 shares at $90 per share. On November 1, Sprinkle reissued 40 shares at $83 p

> Incurring long-term debt with an arrangement whereby lenders receive an option to buy common stock during all or a portion of the time the debt is outstanding is a frequent corporate financing practice. In some situations, the result is achieved through

> Agassi Corporation is preparing the comparative financial statements to be included in the annual report to stockholders. Agassi employs a fiscal year ending May 31. Income from operations before income taxes for Agassi was $1,400,000 and $660,000, respe

> The information below pertains to Barkley Company for 2013. Net income for the year ……………………………………………………………………………………. $1,200,000 8% convertible bonds issued at par ($1,000 per bond); each bond is convertible into 30 shares of common stock ………………………………………

> Assume the bonds in IFRS14-3 were issued for $644,636 and the effective-interest rate is 6%. Prepare the company’s journal entries for (a) The January 1 issuance, (b) The July 1 interest payment, and (c) The December 31 adjusting entry In IFRS14-3 On Ja

> Charles Austin of the controller’s office of Thompson Corporation was given the assignment of determining the basic and diluted earnings per share values for the year ending December 31, 2013. Austin has compiled the information listed below. 1. The comp

> Melton Corporation is preparing the comparative financial statements for the annual report to its shareholders for fiscal years ended May 31, 2012, and May 31, 2013. The income from operations for each year was $1,800,000 and $2,500,000, respectively. In

> Amy Dyken, controller at Fitzgerald Pharmaceutical Industries, a public company, is currently preparing the calculation for basic and diluted earnings per share and the related disclosure for Fitzgerald’s financial statements. Below is selected financial

> Assume that Amazon has a stock-option plan for top management. Each stock option represents the right to purchase a share of Amazon $1 par value common stock in the future at a price equal to the fair value of the stock at the date of the grant. Amazon h

> Berg Company adopted a stock-option plan on November 30, 2011, that provided that 70,000 shares of $5 par value stock be designated as available for the granting of options to officers of the corporation at a price of $9 a share. The market price was $12

> Volker Inc. issued $2,500,000 of convertible 10-year bonds on July 1, 2012. The bonds provide for 12% interest payable semiannually on January 1 and July 1. The discount in connection with the issue was $54,000, which is being amortized monthly on a stra

> Moonwalker Corporation issued 2,000 shares of its $10 par value common stock for $60,000. Moonwalker also incurred $1,500 of costs associated with issuing the stock. Prepare Moonwalker’s journal entry to record the issuance of the company’s stock.

> The stockholders’ equity section of Martino Inc. at the beginning of the current year appears below. Common stock, $10 par value, authorized 1,000,000 shares, 300,000 shares issued and outstanding ……………………………………………………………………………………………………. $3,000,000 Paid-i

> Derrick Company establishes a stock-appreciation rights program that entitles its new president, Dan Scott, to receive cash for the difference between the market price of the stock and a pre-established price of $30 (also market price) on January 1, 2011

> On December 31, 2009, Flessel Company issues 120,000 stock-appreciation rights to its officers entitling them to receive cash for the difference between the market price of its stock and a pre-established price of $10. The fair value of the SARs is estim

> Werth Corporation earned $260,000 during a period when it had an average of 100,000 shares of common stock outstanding. The common stock sold at an average market price of $15 per share during the period. Also outstanding were 30,000 warrants that could

> On January 1, 2012, JWS Corporation issued $600,000 of 7% bonds, due in 10 years. The bonds were issued for $559,224, and pay interest each July 1 and January 1. Prepare the company’s journal entries for (a) The January 1 issuance, (b) The July 1 interes

> Brooks Inc. recently purchased Donovan Corp., a large midwestern home painting corporation. One of the terms of the merger was that if Donovan’s income for 2013 was $110,000 or more, 10,000 additional shares would be issued to Donovan’s stockholders in 2

> Zambrano Company’s net income for 2012 is $40,000. The only potentially dilutive securities outstanding were 1,000 options issued during 2011, each exercisable for one share at $8. None has been exercised, and 10,000 shares of common were outstanding dur

> On January 1, 2012, Lindsey Company issued 10-year, $3,000,000 face value, 6% bonds, at par. Each $1,000 bond is convertible into 15 shares of Lindsey common stock. Lindsey’s net income in 2013 was $240,000, and its tax rate was 40%. The company had 100,

> The Ottey Corporation issued 10-year, $4,000,000 par, 7% callable convertible subordinated debentures on January 2, 2012. The bonds have a par value of $1,000, with interest payable annually. The current conversion ratio is 14:1, and in 2 years it will i

> On June 1, 2011, Bluhm Company and Amanar Company merged to form Davenport Inc. A total of 800,000 shares were issued to complete the merger. The new corporation reports on a calendar-year basis. On April 1, 2013, the company issued an additional 600,000

> On February 1, 2012, Buffalo Corporation issued 3,000 shares of its $5 par value common stock for land worth $31,000. Prepare the February 1, 2012, journal entry.

> In 2012, Buraka Enterprises issued, at par, 75 $1,000, 8% bonds, each convertible into 100 shares of common stock. Buraka had revenues of $17,500 and expenses other than interest and taxes of $8,400 for 2013. (Assume that the tax rate is 40%.) Throughout

> At January 1, 2012, Cameron Company’s outstanding shares included the following. 280,000 shares of $50 par value, 7% cumulative preferred stock 800,000 shares of $1 par value common stock Net income for 2012 was $2,830,000. No cash dividends were declare

> On January 1, 2012, Bailey Industries had stock outstanding as follows. 6% Cumulative preferred stock, $100 par value, issued and outstanding 10,000 shares …………….……………………….. $1,000,000 Common stock, $10 par value, issued and outstanding 200,000 shares ……

> A portion of the statement of income and retained earnings of Pierson Inc. for the current year follows. Note 1. During the year, Pierson Inc. suffered a major casualty loss of $1,340,000 after applicable income tax reduction of $1,200,000. At the end

> Kendall Inc. presented the following data. Net income ……………………………………..…………………. $2,200,000 Preferred stock: 50,000 shares outstanding, $100 par, 8% cumulative, not convertible ………………. 5,000,000 Common stock: Shares outstanding 1/1 ……………………. 600,000 Issued

> Briefly explain the accounting requirements for stock compensation plans under GAAP.

> Ott Company had 210,000 shares of common stock outstanding on December 31, 2012. During the year 2013, the company issued 8,000 shares on May 1 and retired 14,000 shares on October 31. For the year 2013, Ott Company reported net income of $229,690 after

> On January 1, 2012, Chang Corp. had 480,000 shares of common stock outstanding. During 2012, it had the following transactions that affected the Common Stock account. February 1 ……………………………. Issued 120,000 shares March 1 ……………………….. Issued a 20% stock di

> Gogean Inc. uses a calendar year for financial reporting. The company is authorized to issue 9,000,000 shares of $10 par common stock. At no time has Gogean issued any potentially dilutive securities. Listed below is a summary of Gogean’s common stock ac

> Tweedie Company issues 10,000 shares of restricted stock to its CFO, Mary Tokar, on January 1, 2012. The stock has a fair value of $500,000 on this date. The service period related to this restricted stock is 5 years. Vesting occurs if Tokar stays with t

> Ravonette Corporation issued 300 shares of $10 par value common stock and 100 shares of $50 par value preferred stock for a lump sum of $13,500. The common stock has a market price of $20 per share, and the preferred stock has a market price of $90 per s

> Derrick Company issues 4,000 shares of restricted stock to its CFO, Dane Yaping, on January 1, 2012. The stock has a fair value of $120,000 on this date. The service period related to this restricted stock is 4 years. Vesting occurs if Yaping stays with

> On January 1, 2011, Scooby Corporation granted 10,000 options to key executives. Each option allows the executive to purchase one share of Scooby’s $5 par value common stock at a price of $20 per share. The options were exercisable within a 2-year period

> On January 1, 2012, Magilla Inc. granted stock options to officers and key employees for the purchase of 20,000 shares of the company’s $10 par common stock at $25 per share. The options were exercisable within a 5-year period beginning January 1, 2014,

> On November 1, 2011, Olympic Company adopted a stock-option plan that granted options to key executives to purchase 40,000 shares of the company’s $10 par value common stock. The options were granted on January 2, 2012, and were exercisable 2 years after

> On May 1, 2012, Barkley Company issued 3,000 $1,000 bonds at 102. Each bond was issued with one detachable stock warrant. Shortly after issuance, the bonds were selling at 98, but the fair value of the warrants cannot be determined. Instructions (a) Pre

> On September 1, 2012, Jacob Company sold at 104 (plus accrued interest) 3,000 of its 8%, 10-year, $1,000 face value, nonconvertible bonds with detachable stock warrants. Each bond carried two detachable warrants. Each warrant was for one share of common

> What are stock rights? How does the issuing company account for them?

> Prior Inc. has decided to raise additional capital by issuing $175,000 face value of bonds with a coupon rate of 10%. In discussions with investment bankers, it was determined that to help the sale of the bonds, detachable stock warrants should be issued