Question: On February 1, 2020, when the spot

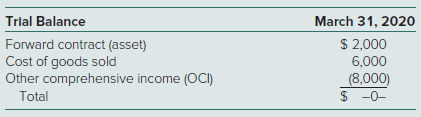

On February 1, 2020, when the spot rate was $1.00 per Swiss franc, Blue Bogey Company (BBC) fore- casted the purchase of component parts on May 1, 2020, at a price of 100,000 Swiss francs. On that date, BBC entered into a forward contract to purchase 100,000 Swiss francs on May 1, 2020, and designated the forward contract as a cash flow hedge of the forecasted transaction. The forward points are excluded from the assessment of hedge effectiveness and are straight-line amortized on a monthly basis. On May 1, 2020, the forward contract was settled, and the component parts were received and paid for. The parts were used in the assembly of finished goods that were sold by June 30, 2020.

BBC’s trial balance at March 31 (end of the first quarter) reported the following amounts related to this cash flow hedge (credit balance in parentheses):

Required

Answer the following questions:

1. On February 1, 2020, was the Swiss franc selling at a discount or at a premium in the three-month forward market?

2. On February 1, 2020, what was the U.S. dollar per Swiss franc forward rate to May 1, 2020?

3. On March 31, 2020, what was the U.S. dollar per Swiss franc forward rate to May 1, 2020?

4. What amount did BBC recognize as Cost of Goods Sold in the second quarter of 2020?

> The following information pertains to the City of Williamson for 2020, its first year of legal existence. For convenience, assume that all transactions are for the general fund, which has three separate functions: general government, public safety, and h

> The County of Maxnell decides to create a waste management department and offer its services to the public for a fee. As a result, county officials plan to account for this activity as an enterprise fund. Prepare journal entries for this operation for th

> On January 1, 2020, the City of Graf pays $60,000 for a work of art to display in the local library. The city will take appropriate measures to protect and preserve the piece. However, if the work is ever sold, the money received will go into unrestricte

> On January 1, 2020, a rich citizen of the Town of Ristoni donates a painting valued at $300,000 to be displayed to the public in a government building. Although this painting meets the three criteria to qualify as an artwork, town officials choose to rec

> AutoNav Company agrees to pay $20 million in cash to the four former owners of Easy-C, Inc., for all of its assets and liabilities. These four owners of Easy-C developed and patented a technology for real- time monitoring of traffic patterns on the natio

> The City of Lawrence opens a solid waste landfill in 2020 that is at 54 percent of capacity on December 31, 2020. City officials had initially anticipated closure costs of $2 million but later that year decided that closure costs would actually be $2.4 m

> On January 1, 2020, the City of Hastings creates a solid waste landfill that it expects to reach capacity gradually over the next 20 years. If the landfill were to be closed at the current time, closure costs would be approximately $1.2 million plus an a

> The City of Raylan has a rather large warehouse that it no longer needs. The city had previously used the warehouse to store supplies and equipment for the school system, police department, and other public service functions. It has a remaining expected

> The City of Leonard decides to lease school desks for its school system rather than buy them because the lessor will do all scheduled maintenance. On January 1, 2020, the school system leases 5,000 school desks for four years. After that, they will be re

> The City of Bacon is located in the County of Pork. The city has a school system that reports buildings at a net $3.6 million although they are actually worth $4.2 million. The county has a separate school system that reports buildings at a net $5.2 mill

> An employment agency for individuals with disabilities works closely with the City of Hanover. The employment agency is legally separate from the city but still depends on the city for financial support. This support creates a potential financial burden

> An accountant is trying to determine whether the school system of the City of Abraham is fiscally independent. Which of the following is not a requirement for the school system to be judged as fiscally independent? a. Holding property in its own name b.

> Which of the following is not necessary for a special-purpose local government to be viewed as a primary government for reporting purposes? a. It must have a separately elected governing body. b. It must have specifically defined geographic boundaries. c

> Which of the following is true about the management’s discussion and analysis (MD&A)? a. It is an optional addition to the comprehensive annual financial report, but GASB encourages its inclusion. b. It adds a verbal explanation for the numbers and trend

> Which of the following statements is true about use of the modified approach? a. It can be applied to all capital assets of a state or local government. b. It is used to adjust depreciation expense either up or down based on conditions for the period. c.

> On October 18, 2020, Armstrong Auto Corporation ("Armstrong") announced its plan to acquire 80 percent of the outstanding 500,000 shares of Bardeen Electric Corporation’s ("Bardeen") common stock in a business combination following regulatory app

> A city builds sidewalks throughout various neighborhoods at a cost of $2.1 million. Which of the following statements is not true? a. Because the sidewalks qualify as infrastructure, the asset is viewed in the same way as land so that no depreciation is

> Assume in problem 17 that the city reports the work as a capital asset. Which of the following is true? a. Depreciation is not recorded because the city has no cost. b. Depreciation is not required if the asset is viewed as inexhaustible. c. Depreciation

> In problem 17, which of the following statements is true about reporting a revenue in connection with this gift? a. A revenue will be reported. b. Revenue is reported but only if the asset is reported. c. If the asset is not capitalized, the city recogni

> Use the same information as in (8). What amount of deferred lease revenue will Reynolds report on its statement of net position as of December 31, 2020, assuming that the county recognizes revenue on a straight-line method? a. Zero b. $487,419 c. $500,00

> Use the same information as in (8). What amount of depreciation expense will Reynolds report in its government-wide financial statements for 2020? a. Zero b. $52,581 c. $100,000 d. $112,581

> Use the same information as in (8). What is the total amount of expenditures that Webster will report on its fund financial statements for the governmental funds for 2020? a. $112,581 b. $136,954 c. $600,000 d. $712,581

> During 2020, the City of Coyote received $10,000, which was recorded as a general revenue in the general fund. It was actually a program revenue earned by the city’s park program. a. What was the correct overall change for 2020 in the net position report

> In 2020, the City of Coyote receives a $320,000 cash grant from the state to reduce air pollution. Although a special revenue fund could have been set up, the money remains in the general fund. The cash was received immediately but will have to be return

> The City of Coyote mails property tax bills for 2021 to its citizens during August 2020. Payments could be made early to receive a discount. The levy becomes legally enforceable on February 15, 2021. All money the government receives must be spent during

> The City of Coyote mails property tax bills for 2021 to its citizens during August 2020. Property owners could make payments early to receive a discount. The levy becomes legally enforceable on February 15, 2021. All money received by the city must be sp

> A vice president for operations at Poncho Platforms asks for your help on a financial reporting issue concerning goodwill. Two years ago, the company suffered a goodwill impairment loss for its Chip Integration reporting unit. Since that time, however, t

> The City of Coyote records an art display within its general fund. The display generates revenues of $9,000 this year as well as expenditures of $45,000 ($15,000 in expenses and $30,000 to buy land for the display). The CPA firm determines that the city

> On December 30, 2020, the City of Coyote borrows $20,000 for the general fund on a 60-day note. In that fund, the city records Cash and Other Financing Sources. In the general information, this city reports a $30,000 overall increase in the fund balance

> During 2020, the City of Coyote contracts to build a bus stop for schoolchildren costing $10,000 as a special assessments project. The city collects $10,000 from directly affected citizens. The government has no obligation in connection with this project

> Inside the City of Patience, Fund A transfers $20,000 in cash to Fund B. For each of the following, indicate whether the statement is true or false and, if false, explain why. a. If Fund A is the general fund and Fund B is an enterprise fund, nothing is

> The following are transactions of the City of Grayson. Indicate how each of the following transactions affects the fund balance of the general fund, and its classifications, for fund financial statements. Then describe the effect each transaction has on

> On December 1, 2020, a state government awards a city government a grant of $1 million to be used specifically to provide hot lunches for all schoolchildren. No money is received until June 1, 2021. For each of the following, indicate whether the stateme

> Government officials of the City of Johnson expect to receive general fund revenues of $400,000 in 2020 but approve spending only $380,000. Later in the year, as they receive more information, they increase the revenue projection to $420,000. Officials a

> Use the transactions in problem (47) but prepare a statement of net position for the government- wide financial statements. Assume that the general fund held $180,000 in cash on the first day of the year and no other assets or liabilities. No amount of t

> The following transactions relate to the general fund of the city of Lost Angels for the year ending December 31, 2020. Prepare a statement of revenues, expenditures, and other changes in fund balance for the general fund for the period to be included in

> The fiscal year for the City of Havisham ends December 31, Year 5. If the city were to produce financial statements before any adjustments, the following figures would be included: ∙ Governmental activities: Assets = $800,000, Liabilities = $300,000, and

> In this project, you are to provide an analysis of alternative accounting methods for controlling interest investments and subsequent effects on consolidated reporting using Excel. Modeling in Excel helps you quickly assess the impact of alternative acco

> A city has only one activity, its school system. The school system is accounted for within the general fund. For convenience, assume that, at the start of 2020, the school system and the city have no assets. During the year, the city assesses property ta

> The following trial balance is taken from the General Fund of the City of Jennings for the year ending December 31, 2020. Prepare a condensed statement of revenues, expenditures, and other changes in fund balance. Also prepare a condensed balance sheet.

> Chesterfield County had the following transactions. Prepare the entries first for fund financial statements and then for government-wide financial statements. a. A budget is passed for all ongoing activities. Revenue is anticipated to be $834,000, with a

> Following are descriptions of transactions and other financial events for the City of Tetris for the year ending December 2020. Not all transactions have been included here. Only the general fund formally records a budget. No encumbrances were carried ov

> Prepare journal entries for a local government to record the following transactions, first for fund financial statements and then for government-wide financial statements. a. The government sells $900,000 in bonds at face value to finance the constructio

> Prepare journal entries for the City of Pudding’s governmental funds to record the following transactions, first for fund financial statements and then for government-wide financial statements. a. A new truck for the sanitation department was ordered at

> A local government has the following transactions during the current fiscal period. Prepare journal entries without dollar amounts, first for fund financial statements and then for government-wide financial statements. a. The budget for the police depart

> A city transfers cash of $90,000 from its general fund to start construction on a police station. The city issues a bond at its $1.8 million face value. The police station is built for a total cost of $1.89 million. Prepare all necessary journal entries

> The board of commissioners of the City of Hartmoore adopts a general fund budget for the year ending June 30, 2020. It includes revenues of $1,000,000, bond proceeds of $400,000, appropriations of $900,000, and operating transfers out of $300,000. If thi

> A city transfers cash of $20,000 from its general fund to an enterprise fund to pay for work done by the enterprise fund for the school system. What is reported on the city’s fund financial statements? a. No reporting is made. b. Other Financing Sources

> On January 1, 2020, Hi-Speed.com acquired 100 percent of the common stock of Wi-Free Co. for cash of $730,000. The consideration transferred was allocated among Wi-Free’s net assets as follows: At the acquisition date, the computer soft

> A city transfers cash of $20,000 from its general fund to an enterprise fund to pay for work per- formed by the enterprise fund for the school system. How does the city report this transfer on its government-wide financial statements? a. No reporting is

> A county transfers cash of $60,000 from its general fund to a debt service fund. What is reported on the county’s fund financial statements? a. No reporting is made. b. Other Financing Sources increase by $60,000. Other Financing Uses increase by $60,000

> Which of the following is an example of an interactivity transaction? a. A city transfers money from the general fund to a debt service fund. b. A city transfers money from a capital projects fund to the general fund. c. A city transfers money from a spe

> The partnership of Hendrick, Mitchum, and Redding has the following account balances: This partnership is being liquidated. Hendrick and Mitchum are each entitled to 40 percent of all profits and losses with the remaining 20 percent going to Redding. a.

> The Simpson, Hart, Bobb, and Reidel partnership has terminated operations and is undergoing liquidation. Sales commissions and other liquidation expenses are expected to total $19,000. The partnership’s balance sheet prior to the commen

> A partnership has the following account balances at the date of termination: Cash, $80,000; Noncash Assets, $660,000; Liabilities, $320,000; Bell, capital (50 percent of profits and losses), $200,000; Mann, capital (30 percent), $120,000; Scott, capital

> When a partnership is liquidated, how is the final distribution of partnership cash made to the partners? a. Equally b. According to the profit and loss ratio c. According to the final capital account balances d. According to the initial investment made

> Patrick has a capital balance of $120,000 in a local partnership, and Caitlin has a $90,000 balance. These two partners share profits and losses by a ratio of 60 percent to Patrick and 40 percent to Caitlin. Camille invests $60,000 in cash in the partner

> A partnership has the following capital balances with partners’ profit and loss percentages indicated parenthetically: Ranzilla agrees to pay a total of $245,000 directly to these three partners to acquire a 25 percent ownership interes

> A partnership has the following capital balances with partners’ profit and loss percentages indicated parenthetically: Anne is going to invest $125,000 into the business to acquire a 40 percent ownership interest. Goodwill is to be reco

> On January 1, 2020, Innovus, Inc., acquired 100 percent of the common stock of ChipTech Company for $670,000 in cash and other fair-value consideration. ChipTech’s fair value was allocated among its net assets as follows: The December 3

> Steve Reese is a well-known interior designer in Fort Worth, Texas. He wants to start his own business and convinces Rob O’Donnell, a local merchant, to contribute the capital to form a partnership. On January 1, 2019, O’Donnell invests a building worth

> A partnership of attorneys in the St. Louis, Missouri, area has the following balance sheet accounts as of January 1, 2021: According to the articles of partnership, Athos is to receive an allocation of 50 percent of all partnership profits and losses, w

> Kimble, Sykes, and Gerard open an accounting practice on January 1, 2019, in Chicago, Illinois, to be operated as a partnership. Kimble and Sykes will serve as the senior partners because of their years of experience. To establish the business, Kimble, S

> Gorman and Morton form a partnership on May 1, 2019. Gorman contributes cash of $50,000; Morton conveys title to the following properties to the partnership: The partners agree to start their partnership with equal capital balances. No goodwill is to be

> In the early part of 2021, the partners of Hugh, Jacobs, and Thomas sought assistance from a local accountant. They had begun a new business in 2020 but had never used an accountant’s services. Hugh and Jacobs began the partnership by contributing $150,0

> On January 1, 2020, the dental partnership of Angela, Diaz, and Krause was formed when the partners contributed $30,000, $58,000, and $60,000, respectively. Over the next three years, the business reported net income and (loss) as follows: During this pe

> Purkerson, Smith, and Traynor have operated a bookstore for a number of years as a partnership. At the beginning of 2021, capital balances were as follows: Due to a cash shortage, Purkerson invests an additional $8,000 in the business on April 1, 2021. E

> The partnership agreement of Jones, King, and Lane provides for the annual allocation of the business’s profit or loss in the following sequence: ∙ Jones, the managing partner, receives a bonus equal to 20 percent of t

> The Prince-Robbins partnership has the following capital account balances on January 1, 2021: Prince is allocated 80 percent of all profits and losses with the remaining 20 percent assigned to Robbins after interest of 10 percent is given to each partner

> A partnership begins its first year with the following capital balances: The articles of partnership stipulate that profits and losses be assigned in the following manner: ∙ Each partner is allocated interest equal to 5 percent of the b

> On January 1, 2020, James Company purchased 100 percent of the outstanding voting stock of Nolan, Inc., for $1,000,000 in cash and other consideration. At the purchase date, Nolan had common stock of $500,000 and retained earnings of $185,000. James attr

> Use the trial balance presented for Lynch, Inc., in problem (51). Assume that the company will be liquidated and the following transactions will occur: ∙ Accounts receivable of $18,000 are collected with remainder written off. ∙ All of the company’s inve

> Lynch, Inc., is a hardware store operating in Boulder, Colorado. Management recently made some poor inventory acquisitions that have loaded the store with unsalable merchandise. Because of the drop in revenues, the company is now insolvent. The entire in

> Becket Corporation’s accountant has prepared the following balance sheet as of November 10, 2020, the date on which the company is to release a plan for reorganizing operations under Chapter 11 of the Bankruptcy Reform Act: The company

> The following balance sheet has been produced for Litz Corporation as of August 8, 2020, the date on which the company is to begin selling assets as part of a corporate liquidation: The following events occur during the liquidation process: âˆ

> The following balance sheet has been prepared by the accountant for Limestone Company as of June 3, 2020, the date on which the company is to file a voluntary petition of bankruptcy: Additional Information ∙ If the company is liquidated

> Smith Corporation has gone through bankruptcy and is ready to emerge as a reorganized entity on December 31, 2020. On this date, the company has the following assets (fair value is based on dis- counting the anticipated future cash flows): The company ha

> Ristoni Company is in the process of emerging from a Chapter 11 bankruptcy. It will apply fresh start accounting as of December 31, 2020. The company currently has 30,000 shares of common stock outstanding with a $240,000 par value. As part of the reorga

> Shi Company is going through a Chapter 7 bankruptcy. All assets have been liquidated, and the company retains only $26,200 in free cash. The following debts, totaling $43,050, remain: Indicate how much money will be paid to the creditor associated with e

> Which of the following statements is true? a. The Securities Exchange Act of 1934 regulates intrastate stock offerings made by a company. b. The Securities Act of 1933 regulates the subsequent public trading of securities through brokers and markets. c.

> A company must prepare IFRS financial statements for the first time on December 31, 2022. According to IFRS 1, what is the date of transition to IFRS for this company? a. January 1, 2020 b. January 1, 2021 c. December 31, 2021 d. December 31, 2022

> Prior to the creation of government-wide financial statements, the City of Loveland did not report the cost of its infrastructure assets. Now city officials are attempting to determine reported values for major infrastructure assets that were obtained pr

> Hirsch Company acquired equipment at the beginning of 2020 at a cost of $135,000. The equipment has a five-year life with no expected salvage value and is depreciated on a straight- line basis. At December 31, 2020, Hirsch compiled the following informat

> Trecek Corporation incurs research and development costs of $650,000 in 2020, 30 percent of which relate to development activities subsequent to IAS 36 criteria having been met that indicate an intangible asset has been created. The newly developed produ

> Parnell Company acquired construction equipment on January 1, 2020, at a cost of $78,400. The equipment was expected to have a useful life of six years and a residual value of $10,000 and is being depreciated on a straight-line basis. On January 1, 2021,

> Harrington Company was sued by an employee in late 2020. General counsel concluded that there was an 80 percent probability that the company would lose the lawsuit. The range of possible loss is estimated to be $20,000 to $70,000, with no amount in the r

> Tapatio S.A. de C.V. acquired a new piece of manufacturing equipment on January 1, 2019, for a cash price of 500,000 pesos. The equipment was expected to have a useful life of 10 years and no residual value, and is being depreciated on a straight-line ba

> Sapporo K.K. was sued by a competitor in late 2020, and company management concluded that there was a 55 percent probability that the company would lose the lawsuit. The best estimate of the loss on December 31, 2020, was 4,000,000 yen. In 2021, the laws

> Llungby AB spent 1,000,000 krone in 2020 on the development of a new product. The company determined that 25 percent of this amount was incurred after the criteria in IAS 36 for capitalization as an intangible asset had been met. The newly developed prod

> Mikkeli OY acquired a brand name with an indefinite life in 2021 for 40,000 markkas. At December 31, 2020, the brand name could be sold for 35,000 markkas, with zero costs to sell. Expected cash flows from the continued use of the brand are 42,000 markka

> On January 1, 2020, Xiamen Company made amendments to its defined benefit pension plan that resulted in 60,000 yuan of past service cost. The plan has 5,000 active employees with an average expected remaining working life of 15 years. There currently are

> Surat Limited paid cash to acquire an aircraft on January 1, 2020, at a cost of 30,000,000 rupees. The aircraft has an estimated useful life of 40 years and no salvage value. The company has deter- mined that the aircraft is composed of three significant

> The City of Bainland has been undergoing financial difficulties because of a decrease in its tax base caused by corporations leaving the area. On January 1, 2020, the city has a fund balance of only $400,000 in its governmental funds. In 2016, the city h

> Izmir A.S. issued convertible bonds at their face value of 100,000 lira on December 31, 2020. The bonds have a 10-year life with interest of 10 percent payable annually. At the date of issue, the pre- vailing interest rate for similar debt without a conv

> What amount does Newberry’s consolidated income statement report for cost of goods sold for the year ending December 31, 2021? a. $16,000 b. $17,000 c. $18,000 d. $19,000

> What amount does Newberry’s consolidated balance sheet report for this inventory at December 31, 2020? a. $16,000 b. $17,000 c. $18,000 d. $19,000

> Millager Company is a U.S.-based multinational corporation with the U.S. dollar (USD) as its reporting currency. To prepare consolidated financial statements for 2020, the company must trans- late the accounts of its subsidiary in Mexico, Cadengo S.A. On

> Diekmann Company, a U.S.-based company, acquired a 100 percent interest in Rakona A.S. in the Czech Republic on January 1, 2019, when the exchange rate for the Czech koruna (Kčs) was $0.05. Rakona’s financial statements as of

> On January 1, 2019, Cayce Corporation acquired 100 percent of Simbel Company for consideration transferred with a fair value of $126,000. Cayce is a U.S.-based company headquartered in Buffalo, New York, and Simbel is in Cairo, Egypt. Cayce accounts for

> Sendelbach Corporation is a U.S.-based organization with operations throughout the world. One of its subsidiaries is headquartered in Toronto. Although this wholly owned company operates primarily in Canada, it engages in some transactions through a bran