Question: Pam Corporation owned a 90 percent interest

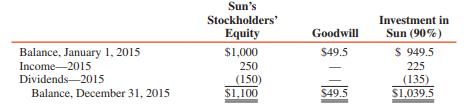

Pam Corporation owned a 90 percent interest in Sun Corporation, and during 2015 the following changes occurred in Sun’s equity and Pam’s investment in Sun (in thousands):

During 2016, Sun’s net income was $280,000, and it declared $40,000 dividends each quarter of the year.

Pam reduced its interest in Sun to 80 percent on July 1, 2016, by selling Sun shares for $120,000.

REQUIRED:

1. Prepare the journal entry on Pam’s books to record the sale of Sun shares as of the actual date of sale.

2. Prepare the journal entry on Pam’s books to record the sale of Sun shares as of January 1, 2016.

3. Prepare a schedule to reconcile the answers to parts 1 and 2.

Transcribed Image Text:

Sun's Stockholders' Investment in Equity Goodwill Sun (90%) Balance, January 1, 2015 $1,000 S49.5 $ 949.5 Income-2015 250 225 Dividends-2015 (150) $1,100 (135) Balance, December 31, 2015 $49.5 S1,039.5

> What are the legal distinctions between a business combination, a merger, and a consolidation?

> Is dissolution of all but one of the separate legal entities necessary in order to have a business combination? Explain.

> What is the accounting concept of a business combination?

> Does current GAAP provide any exceptions to the fair-value measurement principle for business combinations?

> What are the required disclosures related to goodwill included in the consolidated balance sheet?

> Separate-company financial statements for Pop Corporation and its subsidiary, Son Company, at and for the year ended December 31, 2017, are summarized as follows (in thousands): ADDITIONAL INFORMATION: 1. Pop Corporation acquired 13,500 shares of Son C

> Pop Corporation acquired a 75 percent interest in Son Corporation on January 1, 2016, for $720,000 in cash. Financial statements of Pop and Son Corporations for 2016 are as follows (in thousands): REQUIRED: Prepare consolidation work papers for Pop Co

> What special procedures are required to consolidate the statements of a parent that reports on a calendar year basis and a subsidiary whose fiscal year ends on October 31?

> Pop Corporation issued its own common stock for all the outstanding shares of Son Corporation in a pooling of interests business combination on January 1, 2000. The balance sheets of the two companies at December 31, 1999, were as follows (in thousands):

> On January 1, 2000, Pam Corporation held 2,000 shares of Sun Corporation common stock acquired at $15 per share several years earlier. On this date, Pam issued 1.5 of its $10 par value shares for each of the other 98,000 outstanding shares of Sun in a po

> The effect of unrealized profits and losses on sales between affiliated companies is eliminated in preparing consolidated financial statements. When are profits and losses on such sales realized for consolidated statement purposes?

> Consolidation workpaper procedures are usually based on the assumption that any unrealized profit in the beginning inventory of one year is realized through sales in the following year. If the related merchandise is not sold in the succeeding period, wou

> Is the effect of unrealized profit on consolidated cost of goods sold influenced by (a) the existence of a noncontrolling interest and (b) the direction of intercompany sales?

> 1. Pam Corporation owns a 70 percent interest in Sun Corporation, acquired several years ago at book value. On December 31, 2016, Sun mailed a check for $80,000 to Pam in part payment of an $160,000 account with Pam. Pam had not received the check when t

> In eliminating unrealized profit on intercompany sales of inventory items, should gross profit or net profit be eliminated?

> Does noncontrolling interest represent a liability or an equity in the consolidated balance sheet?

> Should the consolidated financial statements include the subsidiary’s retained earnings at the acquisition date?

> Pam Corporation acquired its 90 percent interest in Sun Corporation at its book value of $3,600,000 on January 1, 2016, when Sun had capital stock of $3,000,000 and retained earnings of $1,000,000. The December 31, 2016 and 2017, inventories of Pam inclu

> Pop Corporation purchased a 90 percent interest in Son Corporation on December 31, 2016, for $5,400,000 cash, when Son had capital stock of $4,000,000 and retained earnings of $1,000,000. All Son’s assets and liabilities were recorded a

> Pop Corporation has owned a 30 percent interest in Son Corporation for ten years, and has properly recorded this investment using the equity method of accounting. On July 1 of the current year Pop purchased an additional 40 percent interest in Son. Is it

> 1. Consolidation workpaper entries normally: a Are posted to the general ledger accounts of one or more of the affiliates b Are posted to the general ledger accounts only when the financial statement approach is used c Are posted to the general ledger ac

> Pop Corporation acquired 100 percent of Son Corporation’s outstanding voting common stock on January 1, 2016, for $660,000 cash. Son’s stockholders’ equity on this date consisted of $300,0

> Pam Corporation purchased a 90 percent interest in Sun Corporation on December 31, 2015, for $2,700,000 cash, when Sun had capital stock of $2,000,000 and retained earnings of $500,000. All Sun’s assets and liabilities were recorded at

> Pop Corporation acquired a 75 percent interest in Son Corporation for $600,000 on January 1, 2016, when Son’s equity consisted of $300,000 capital stock and $100,000 retained earnings. The fair values of Son’s assets a

> Pam Corporation acquired 100 percent of Sun Corporation’s outstanding voting common stock on January 1, 2016, for $660,000 cash. Sun’s stockholders’ equity on this date consisted of $300,000 capital s

> Comparative income statements of Son Corporation for the calendar years 2016, 2017, and 2018 are as follows (in thousands): ADDITIONAL INFORMATION: 1. Son was a 75 percent–owned subsidiary of Pop Corporation throughout the 2016â

> Why is the equity method referred to as a “one-line consolidation”?

> Describe the equity method of accounting.

> How are the accounts of investor and investee companies affected when the investor acquires stock from stockholders of the investee (e.g., a New York Stock Exchange purchase)? Does this differ if the investor acquires previously unissued stock directly f

> Is there any difference in computing goodwill impairment losses for a controlled subsidiary versus an equity method investment?

> Describe the accounting adjustments needed when a 25 percent equity interest in an investee is decreased to a 15 percent equity interest.

> Pop Corporation acquired an 80 percent interest in Son Corporation for $240,000 on January 1, 2016, when Son’s stockholders’ equity consisted of $200,000 capital stock and $25,000 retained earnings. The excess fair val

> Is there a difference between the amount of a parent’s net income under the equity method and the consolidated net income for the same parent and its subsidiaries?

> Pop Corporation purchased 80 percent of the outstanding voting common stock of Son Corporation on January 2, 2016, for $1,200,000 cash. Son’s balance sheets on this date and on December 31, 2016, are as follows: ADDITIONAL INFORMATION

> Under the fair value/cost method of accounting for stock investments, an investor records dividends received from earnings accumulated after the investment is acquired as dividend income. How does an investor treat dividends received from earnings accumu

> Should goodwill arising from an equity investment of more than 20 percent be recorded separately on the books of the investor? Explain.

> A firm sells a part of its investment interest, reducing its holding from 30% to 10%. The firm decides, correctly, that the equity method is no longer appropriate. What is the basis for the investment in applying the new accounting method?

> Pop Corporation owns 300,000 of 360,000 outstanding shares of Son Corporation, and its $8,700,000 Investment in Son account balance on December 31, 2016, is equal to the underlying equity interest in Son. Son’s stockholders’ equity at December 31, 2016,

> The equity method of accounting is often referred to as a one-line consolidation. Since the net impact on the balance sheet and income statement is the same under both consolidation and the equity method, is it acceptable to report a noncontrolling inves

> Pop Corporation acquired a 70 percent interest in Son Corporation on April 1, 2016, when it purchased 14,000 of Son’s 20,000 outstanding shares in the open market at $13 per share. Additional costs of acquiring the shares consisted of $

> Pam Corporation purchased 40 percent of the voting stock of Sun Corporation on July 1, 2016, for $600,000. On that date, Sun’s stockholders’ equity consisted of capital stock of $1,000,000, retained earnings of $300,00

> Pam Corporation made three investments in Sun during 2016 and 2017, as follows: Sun’s stockholders’ equity on January 1, 2016, consisted of 20,000 shares of $10 par common stock and retained earnings of $100,000. Pam

> Pop Corporation exchanged 40,000 previously unissued no par common shares for a 40 percent interest in Son Corporation on January 1, 2016. The assets and liabilities of Son on that date (after the exchange) were as follows (in thousands): The direct co

> Sun Corporation became a subsidiary of Pam Corporation on July 1, 2016, when Pam paid $1,980,000 cash for 90 percent of Sun’s outstanding common stock. The price paid by Pam reflected the fact that Sun’s inventories we

> Pam Company owns controlling interests in Sun and Toy Corporations, having acquired an 80 percent interest in Sun in 2016, and a 90 percent interest in Toy on January 1, 2017. Pam’s investments in Sun and Toy were at book value equal to

> Pam Corporation paid $170,000 for an 80 percent interest in Sun Corporation on December 31, 2016, when Sun’s stockholders’ equity consisted of $100,000 capital stock and $50,000 retained earnings. A summary of the chan

> Pop Corporation acquired 30 percent of the voting stock of Son Company at book value on July 1, 2016. During 2018, Son paid dividends of $160,000 and reported income of $500,000 as follows: Income from continuing operations....................... $300,0

> Pam Corporation purchased for cash 6,000 shares of voting common stock of Sun Corporation at $16 per share on July 1, 2016. On this date, Sun’s equity consisted of $100,000 of $10 par capital stock, $20,000 retained earnings from prior periods, and $10,0

> Pop Corporation paid $1,680,000 for a 30 percent interest in Son Corporation’s outstanding voting stock on January 1, 2016. The book values and fair values of Son’s assets and liabilities on January 1, along with amort

> Pam Corporation paid $190,000 for 40 percent of Sun Corporation’s outstanding voting common stock on July 1, 2016. Sun’s stockholders’ equity on January 1, 2016, was $250,000, consisting of $150,000 capital stock and $100,000 retained earnings. During 20

> Pop Company acquired a 30 percent interest in the voting stock of Son Company for $331,000 on January 1, 2016, when Son’s stockholders’ equity consisted of capital stock of $600,000 and retained earnings of $400,000. At the time of Pop’s investment, Son’

> Pam Company paid $440,000 for an 80 percent interest in Sun Company on July 1, 2016, when Sun had total equity of $220,000. Sun Company reported earnings of $20,000 for 2016 and declared dividends of $32,000 on November 1, 2016. REQUIRED: Give the entri

> Pop Corporation paid $686,000 for a 30 percent interest in Son Corporation’s outstanding voting stock on April 1, 2016. At December 31, 2015, Son had net assets of $2,000,000 and only common stock outstanding. During 2016, Son declared and paid dividends

> Pam Corporation paid $290,000 for 40 percent of the outstanding common stock of Sun Corporation on January 2, 2017. During 2017, Sun paid dividends of $48,000 and reported net income of $108,000. A summary of Sun’s stockholdersâ&#

> Pop Corporation acquired a 90 percent interest in Son Corporation at book value on January 1, 2016. Intercompany purchases and sales and inventory data for 2016, 2017, and 2018, are as follows: Selected data from the financial statements of Pop and Son

> Pop Corporation paid $780,000 for a 30 percent interest in Son Corporation on December 31, 2016, when Son’s stockholders’ equity consisted of $2,000,000 capital stock and $800,000 retained earnings. The price paid by Pop reflected the fact that Son’s inv

> The stockholders’ equity of Sun Corporation at December 31, 2016, was $380,000, consisting of the following (in thousands): Capital stock, $10 par (24,000 shares outstanding)........... $240 Additional paid-in capital....................................

> Pop Corporation acquired 80 percent of Son Corporation’s common stock on January 1, 2016, for $420,000 cash. The stockholders’ equity of Son at this time consisted of $300,000 capital stock and $100,000 retained earnin

> Summary balance sheet and income information for Son Company for two years is as follows (in thousands): On January 2, 2016, Pop Company purchases 10 percent of Son Company for $25,000 cash, and it accounts for its investment (classified as an availabl

> Pam Corporation acquired 25 percent of Sun Corporation’s outstanding common stock on October 1, for $300,000. A summary of Sun’s adjusted trial balances on this date and at December 31 follows (in thousands): Pam use

> Pop Corporation purchased 480,000 shares of Son Corporation’s common stock (an 80 percent interest) for $10,600,000 on January 1, 2016. The $1,000,000 excess of investment fair value over book value acquired was attributed to goodwill.

> Son Company had net income of $400,000 and paid dividends of $200,000 during 2017. Son’s stockholders’ equity on December 31, 2016, and December 31, 2017, is summarized as follows (in thousands): On January 2, 2017,

> Pam Corporation owns a 40 percent interest in the outstanding common stock of Sun Corporation, having acquired its interest for $2,400,000 on January 1, 2016, when Sun’s stockholders’ equity was $4,000,000. The fair value/book value differential was assi

> 1. On January 3, 2016, Pop Company purchases a 15 percent interest in Son Corporation’s common stock for $50,000 cash. Pop accounts for the investment using the cost method. Son’s net income for 2016 is $20,000, but it declares no dividends. In 2017, Son

> Pop Company acquired a 30 percent interest in Son on January 1 for $500,000 cash. Assume the cost of the investment equals the fair value of Son’s net assets. Pop assigned the $125,000 excess of fair value over book value of the interest acquired to the

> 1. Intercompany profit elimination entries in consolidation workpapers are prepared in order to: a Nullify the effect of intercompany transactions on consolidated statements b Defer intercompany profit until realized c Allocate unrealized profits between

> 1. Pam Company owns 25 percent of Sun Corporation. During the year, Sun had net earnings of $450,000 and paid dividends of $28,000. Pam mistakenly recorded these transactions using the cost method rather than the equity method. What effect would this hav

> 1. GAAP provides indicators of an investor’s inability to exercise significant influence over an investee. Which of the following is not included among those indicators? a Surrender of significant stockholder rights by agreement b Concentration of majori

> Pop Corporation recorded goodwill in the amount of $200,000 in its acquisition of Son Company in 2016. Pop paid a total of $700,000 to acquire Son. In preparing its 2017 financial statements, Pop estimates that identifiable net assets still have a fair v

> Pam, Inc. has two primary business reporting units: Alfa and Beta. In preparing its 2017 financial statements, Pam conducts the required annual impairment review of goodwill. Alfa has recorded goodwill of $35,000 that has an estimated fair value of $30,0

> Pam Corporation acquired 80 percent of Sun Corporation’s common stock on January 1, 2016, for $840,000 cash. The stockholders’ equity of Sun at this time consisted of $600,000 capital stock and $200,000 retained earnin

> Pam Corporation purchased a 40 percent interest in Sun Corporation for $2,000,000 on January 1, at book value, when Sun’s assets and liabilities were recorded at fair values. During the year, Sun reported net income of $1,200,000 as follows (in thousands

> A summary of changes in the stockholders’ equity of Sun Corporation from January 1, 2016, to December 31, 2017, appears as follows (in thousands): Pam Corporation purchases 40,000 shares of Sun’s outstanding stock on

> Pam Corporation pays $300,000 for a 30 percent interest in Sun Corporation on July 1, 2016, when the book value of Sun’s identifiable net assets equals fair value. Information relating to Sun follows (in thousands): REQUIRED: Calculat

> Son Corporation’s stockholders’ equity at December 31, 2015, consisted of the following (in thousands): Capital stock, $10 par, 60,000 shares issued and outstanding ..............$600 Additional paid-in capital ..........................................

> What is a bargain purchase? Describe the accounting procedures necessary to record and account for a bargain purchase.

> The consolidated income statement of Pop and Son for 2016 was as follows (in thousands): Sales........................................................................................... $5,520 Cost of sales...............................................

> Pam Corporation owns an 80 percent interest in Sun Corporation acquired several years ago. Sun regularly sells merchandise to Pam at 125 percent of Sun’s cost. Gross profit data of Pam and Sun for 2017 are as follows: During 2017, Pam

> Pop Corporation owns an 80 percent interest in Son Corporation and at December 31, 2016, Pop’s investment in Son on an equity basis was equal to 80 percent of Son’s stockholders’ equity. During 2017,

> 1. The separate incomes of Pop Corporation and Son Corporation, a 100 percent–owned subsidiary of Pop, for 2017 are $2,000 and $1,000, respectively. Pop sells all of its output to Son at 150 percent of Pop’s cost of pr

> Pam Corporation acquired an 85 percent interest in Sun Corporation on August 1, 2016, for $522,750, equal to 85 percent of the underlying equity of Sun on that date. In August 2016, Sun sold inventory items to Pam for $60,000 at a gross profit of $15,000

> 1. Pop, Inc., owns 80 percent of Son, Inc. During 2016, Pop sold goods with a 40 percent gross profit to Son. Son sold all of these goods in 2016. For 2016 consolidated financial statements, how should the summation of Pop and Son income statement items

> Can the method used by a parent company in accounting for its subsidiary investments be determined by examining the separate financial statements of the parent and subsidiary companies?

> Controlling share of consolidated net income is a measurement of income to the stockholders of the parent, but does a change in cash as reflected in a statement of cash flows also relate to other stockholders of the parent?

> What approach would you use to check the accuracy of the consolidated retained earnings and noncontrolling interest amounts that appear in the balance sheet section of completed consolidation workpapers?

> When is it necessary to adjust the parent’s retained earnings account in the preparation of consolidation workpapers? In answering this question, explain the relationship between parent-retained earnings and consolidated retained earnings.

> The financial statement and trial balance workpaper approaches illustrated in the chapter generate comparable information, so why learn both approaches?

> Are workpaper adjustments and eliminations entered on the parent’s books? The subsidiary’s books? Explain.

> Son Corporation’s outstanding capital stock (and paid in capital) has been $200,000 since the company was organized in 2016. Son’s retained earnings account since 2016 is summarized as follows: Pop Corporation purcha

> If a parent uses the equity method but does not amortize the difference between fair value and book value on its separate books, its net income and retained earnings will not equal its share of consolidated net income and consolidated retained earnings.

> How are the workpaper procedures for the investment in subsidiary, income from subsidiary, and subsidiary’s stockholders’ equity accounts alike?

> Pam Corporation acquired a 70 percent interest in Sun Corporation’s outstanding voting common stock on January 1, 2016, for $980,000 cash. The stockholders’ equity (book value) of Sun on this date consisted of $1,000,0

> How is noncontrolling interest share entered in consolidation workpapers?

> How is reciprocity established between a parent company’s investment account and the equity accounts of its subsidiary when the cost method is used?

> Explain why noncontrolling interest share is added to the controlling share of consolidated net income in determining cash flows from operating activities.

> In what way do the adjustment and elimination entries for consolidation workpapers differ for the financial statement and trial balance approaches?

> If a parent in accounting for its subsidiary amortizes patents on its separate books, why do we include an adjustment for patents amortization in the consolidation workpaper?

> Firms adopting the direct method to prepare the statement of cash flows often include a reconciliation of net income to net cash flows from operating activities. Is this required, and, if so, how should it be presented?

> In preparing a consolidated statement of cash flows, is a firm required to disclose cash flow per share?

> Comparative consolidated financial statements for Pam Corporation and its 80 percent–owned subsidiary at and for the years ended December 31 are summarized as follows: REQUIRED: Prepare a consolidated statement of cash flows for Pam