Question: Pam Corporation paid $1,800,000 cash

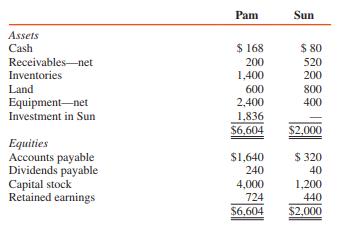

Pam Corporation paid $1,800,000 cash for 90 percent of Sun Corporation’s common stock on January 1, 2016, when Sun had $1,200,000 capital stock and $400,000 retained earnings. The book values of Sun’s assets and liabilities were equal to fair values. During 2016, Sun reported net income of $80,000 and declared $40,000 in dividends on December 31. Balance sheets for Pam and Sun at December 31, 2016, are as follows (in thousands):

REQUIRED:

Prepare consolidated Balance sheet workpapers for Pam Corporation and Subsidiary for December 31, 2016.

Transcribed Image Text:

Pam Sun Assets Cash $ 168 $ 80 Receivables-net 200 520 Inventories 1,400 200 Land 600 800 Equipment-net 2,400 400 Investment in Sun 1,836 $6,604 $2,000 Equities Accounts payable Dividends payable Capital stock Retained earnings $ 320 40 $1,640 240 4,000 1,200 724 440 $6,604 $2,000

> Can the method used by a parent company in accounting for its subsidiary investments be determined by examining the separate financial statements of the parent and subsidiary companies?

> Controlling share of consolidated net income is a measurement of income to the stockholders of the parent, but does a change in cash as reflected in a statement of cash flows also relate to other stockholders of the parent?

> What approach would you use to check the accuracy of the consolidated retained earnings and noncontrolling interest amounts that appear in the balance sheet section of completed consolidation workpapers?

> When is it necessary to adjust the parent’s retained earnings account in the preparation of consolidation workpapers? In answering this question, explain the relationship between parent-retained earnings and consolidated retained earnings.

> The financial statement and trial balance workpaper approaches illustrated in the chapter generate comparable information, so why learn both approaches?

> Are workpaper adjustments and eliminations entered on the parent’s books? The subsidiary’s books? Explain.

> Son Corporation’s outstanding capital stock (and paid in capital) has been $200,000 since the company was organized in 2016. Son’s retained earnings account since 2016 is summarized as follows: Pop Corporation purcha

> If a parent uses the equity method but does not amortize the difference between fair value and book value on its separate books, its net income and retained earnings will not equal its share of consolidated net income and consolidated retained earnings.

> How are the workpaper procedures for the investment in subsidiary, income from subsidiary, and subsidiary’s stockholders’ equity accounts alike?

> Pam Corporation acquired a 70 percent interest in Sun Corporation’s outstanding voting common stock on January 1, 2016, for $980,000 cash. The stockholders’ equity (book value) of Sun on this date consisted of $1,000,0

> How is noncontrolling interest share entered in consolidation workpapers?

> How is reciprocity established between a parent company’s investment account and the equity accounts of its subsidiary when the cost method is used?

> Explain why noncontrolling interest share is added to the controlling share of consolidated net income in determining cash flows from operating activities.

> In what way do the adjustment and elimination entries for consolidation workpapers differ for the financial statement and trial balance approaches?

> If a parent in accounting for its subsidiary amortizes patents on its separate books, why do we include an adjustment for patents amortization in the consolidation workpaper?

> Firms adopting the direct method to prepare the statement of cash flows often include a reconciliation of net income to net cash flows from operating activities. Is this required, and, if so, how should it be presented?

> In preparing a consolidated statement of cash flows, is a firm required to disclose cash flow per share?

> Comparative consolidated financial statements for Pam Corporation and its 80 percent–owned subsidiary at and for the years ended December 31 are summarized as follows: REQUIRED: Prepare a consolidated statement of cash flows for Pam

> 1. In preparing a statement of cash flows, the cost of acquiring a subsidiary is reported: a As an operating activity under the direct method b As an operating activity under the indirect method c As an investing activity d As a financing activity 2. In

> Is noncontrolling interest share an expense? Explain.

> Pop Corporation acquired a 70 percent interest in Son Corporation on January 1, 2016, for $420,000 cash, when Son’s equity consisted of $300,000 capital stock and $200,000 retained earnings. On July 1, 2017, Pop acquired an additional 1

> The consolidated workpaper balances of Pop, Inc., and its subsidiary, Son Corporation, as of December 31 are as follows (in thousands): ADDITIONAL INFORMATION: 1. On January 20, 2016, Pop issued 10,000 shares of its common stock for land having a fair

> Why are reciprocal amounts eliminated in preparing consolidated financial statements?

> Name some reciprocal accounts that might be found in the separate records of a parent and its subsidiaries.

> How should the parent’s investment in subsidiary account be classified in a consolidated balance sheet? In the parent’s separate balance sheet?

> In what general ledger would you expect to find the account “goodwill from consolidation”?

> What is a noncontrolling interest?

> Define or explain the terms parent company, subsidiary company, affiliates, and associates.

> If the fair value of a subsidiary’s land was $100,000 and its book value was $90,000 when the parent acquired its 100 percent interest for cash, at what amount would the land be included in the consolidated balance sheet immediately after the acquisition

> In allocating the excess of investment fair value over book value of a subsidiary, are the amounts assigned to identifiable assets and liabilities (land and notes payable, for example) recorded separately in the accounts of the parent? Explain.

> Does the acquisition of shares held by noncontrolling shareholders constitute a business combination?

> Pam Corporation paid $175,000 for a 70 percent interest in Sun Corporation’s outstanding stock on April 1, 2016. Sun’s stockholders’ equity on January 1, 2016, consisted of $200,000 capital stock and

> Is there a difference in the amounts reported in the statement of retained earnings of a parent that uses the equity method of accounting and the amounts that appear in the consolidated retained earnings statement?

> Comparative consolidated financial statements for Pam Corporation and its 90 percent–owned subsidiary, Sun Corporation, at and for the years ended December 31 are as follows: REQUIRED: Prepare a consolidated statement of cash flows fo

> How does the stockholders’ equity of the parent that uses the equity method of accounting differ from the consolidated stockholders’ equity of the parent and its subsidiaries?

> What amount of capital stock is reported in a consolidated balance sheet?

> Who are the primary users for which consolidated financial statements are intended?

> Describe the circumstances under which the accounts of a subsidiary would not be included in the consolidated financial statements.

> When does a corporation become a subsidiary of another corporation?

> What disclosures are required for a parent company with a less than wholly owned subsidiary?

> Throughout this chapter we typically indicate that acquisitions take place on January 2. At what date should a business combination be recorded?

> A summary of changes in Pam Corporation’s Investment in Sun account from January 1, 2016, to December 31, 2018, follows (in thousands): ADDITIONAL INFORMATION: 1. Pam acquired its 80 percent interest in Sun Corporation when Sun had ca

> Pop Corporation acquired an 80 percent interest in Son Corporation on October 1, 2016, for $82,400, equal to 80 percent of the underlying equity of Son on that date plus $16,000 goodwill (total goodwill is $20,000). Financial statements for Pop and Son C

> Pop Corporation acquired a 70 percent interest in Son Corporation on January 1, 2016, for $2,800,000, when Son’s stockholders’ equity consisted of $2,000,000 capital stock and $1,200,000 retained earnings. On this date

> The consolidated balance sheet of Pam Corporation and its 80 percent subsidiary, Sun Corporation, contains the following items on December 31, 2020 (in thousands): Cash........................................................ $ 160 Inventories...........

> The accountant for Pop Corporation collected the following information that he thought might be useful in the preparation of the company’s consolidated statement of cash flows (in thousands): Cash paid for purchase of equipment..........................

> Pam Corporation purchased 90 percent of Sun Corporation’s outstanding stock for $14,400,000 cash on January 1, 2016, when Sun’s stockholders’ equity consisted of $8,000,000 capital stock and $2,800,00

> On January 1, 2016, Pop Corporation made the following investments: 1. Acquired for cash, 80 percent of the outstanding common stock of Son Corporation at $280 per share. The stockholders’ equity of Son on January 1, 2016, consisted of

> Pop Corporation acquired 80 percent of the outstanding stock of Son Corporation for $1,120,000 cash on January 3, 2016, on which date Son’s stockholders’ equity consisted of capital stock of $800,000 and retained earni

> Adjusted trial balances for Pop and Son Corporations at December 31, 2016, are as follows (in thousands): Pop purchased all the stock of Son for $3,200,000 cash on January 1, 2016, when Son’s stockholders’ equity con

> Pam Corporation purchased a block of Sun Company common stock for $1,040,000 cash on January 1, 2016. Separate-company and consolidated balance sheets prepared immediately after the acquisition are summarized as follows (in thousands): REQUIRED: Recons

> Pam Corporation pays $10,800,000 for an 80 percent interest in Sun Corporation on January 1, 2016, at which time the book value and fair value of Sun’s net assets are as follows (in thousands): REQUIRED: Prepare a schedule to assign t

> Comparative separate-company and consolidated balance sheets for Pam Corporation and its 70 percent–owned subsidiary, Sun Corporation, at year-end 2016, were as follows (in thousands): Sun’s net income for 2017 was $

> Pop Corporation acquired 70 percent of the outstanding common stock of Son Corporation on January 1, 2016, for $350,000 cash. Immediately after this acquisition the balance sheet information for the two companies was as follows (in thousands)

> On December 31, 2016, Pam Corporation purchased 80 percent of the stock of Sun Company at book value. The data reported on their separate balance sheets immediately after the acquisition follow. At December 31, 2016, Pam Corporation owes Sun

> Pam and Sun Corporations’ balance sheets at December 31, 2015, are summarized as follows (in thousands): Pam acquired 80 percent of the voting stock of Sun on January 2, 2016, at a cost of $640,000. The fair values of Sunâ€

> Pam Corporation owns 90 percent of the voting stock of Sun Corporation and 25 percent of the voting stock of Ell Corporation. The 90 percent interest in Sun was acquired for $36,000 cash on January 1, 2016, when Sun’s stockholdersâ

> Pop Corporation acquired an 80 percent interest in Son Corporation on January 2, 2016, for $1,400,000. On this date the capital stock and retained earnings of the two companies were as follows (in thousands): The assets and liabilities of Son were stat

> Summary income statement information for Pam Corporation and its 70 percent–owned subsidiary, Sun, for the year 2017 is as follows (in thousands): REQUIRED: 1. Assume that Pam acquired its 70 percent interest in Sun at book value on J

> Book values and fair values of Son Corporation’s assets and liabilities on December 31, 2015, are as follows (in thousands): On January 1, 2016, Pop Corporation acquires all of Son’s capital stock for $10,000,000 cas

> Pop Corporation paid $3,600,000 for a 90 percent interest in Son Corporation on January 1, 2016; Son’s total book value was $3,600,000. The excess was allocated as follows: $120,000 to undervalued equipment with a three-year remaining u

> 1. Cobb Company’s current receivables from affiliated companies at December 31, 2016, are (1) a $75,000 cash advance to Hill Corporation (Cobb owns 30 percent of the voting stock of Hill and accounts for the investment by the equity met

> 1. Under GAAP, a parent company should exclude a subsidiary from consolidation if: a It measures income from the subsidiary under the equity method b The subsidiary is in a regulated industry c The subsidiary is a foreign entity whose books are recorded

> Pop Corporation purchased a 70 percent interest in Son Corporation on January 2, 2016, for $98,000, when Son had capital stock of $100,000 and retained earnings of $20,000. On June 30, 2017, Pop purchased an additional 20 percent interest for $37,000. Co

> 1. A 75 percent–owned subsidiary should not be consolidated when: a Its operations are dissimilar from those of the parent company b Control of the subsidiary does not lie with the parent company c There is a dominant noncontrolling interest in the subsi

> Comparative income statements of Pop Corporation and Son Corporation for the year ended December 31, 2018, are as follows (in thousands): ADDITIONAL INFORMATION: 1. Son is a 90 percent–owned subsidiary of Pop, acquired by Pop for $1,6

> On December 31, 2016, the separate-company financial statements for Pam Corporation and its 70 percent-owned subsidiary, Sun Corporation, had the following account balances related to dividends (in thousands): REQUIRED: 1. At what amount will dividends

> Briefly outline the steps to calculate a goodwill impairment loss.

> Comparative adjusted trial balances for Pam Corporation and Sun Corporation are given here. Pam Corporation acquired an 80 percent interest in Sun Corporation on January 1, 2016, for $80,000 cash. Except for inventory items that were undervalued by $1,00

> Does cumulative preferred stock in the capital structure of an investee affect the way that an investor accounts for its 30 percent common stock interest? Explain.

> Ordinarily, the income from an investment accounted for by the equity method is reported on one line of the investor’s income statement. When would more than one line of the income statement of the investor be required to report such income?

> What accounting procedures or adjustments are necessary when an investor uses the cost method of accounting for an investment in common stock and later increases the investment such that the equity method is required?

> Cite the conditions under which you would expect the balance of an equity investment account on a balance sheet date subsequent to acquisition to be equal to the underlying book value represented by that investment.

> What is the difference in reporting income from a subsidiary in the parent’s separate income statement and in consolidated financial statements?

> Pam Corporation purchased 9,000 shares of Sun Corporation’s $50 par common stock at $90 per share on January 1, 2016, when Sun had capital stock of $500,000 and retained earnings of $300,000. During 2016, Sun Corporation had net income of $50,000 but dec

> Pam Corporation acquired a 90 percent interest in Sun Corporation on July 1, 2017, for $675,000. The stockholders’ equity of Sun at December 31, 2016, was as follows (in thousands): Capital stock..................... $500 Retained earn

> The stockholder’s equity of Son Corporation at December 31, 2015, 2016, and 2017, is as follows (in thousands): Son reported income of $80,000 in 2016 and paid no dividends. In 2017, Son reported net income of $80,000 and declared and

> Pam Corporation owns two-thirds (600,000 shares) of the outstanding $1 par common stock of Sun Company on January 1, 2016. In order to raise cash to finance an expansion program, Sun issues an additional 100,000 shares of its common stock for $5 per shar

> The stockholders’ equities of Pop Corporation and its 80 percent–owned subsidiary, Son Corporation, on December 31, 2016, appear as follows (in thousands): Pop’s Investment in Son account on this da

> The stockholders’ equities of Pam Corporation and its 80 percent–owned subsidiary, Sun Corporation, on December 31, 2016, are as follows (in thousands): Pam’s Investment in Sun account balance on De

> Pop Corporation paid $2,548,000 cash for 70 percent of the common stock of Son Corporation on June 1, 2016. The assets and liabilities of Son were fairly valued, and any fair value/book value differential is goodwill. Data related to the stockholders’ eq

> The balance of Pam Corporation’s investment in Sun Company account at December 31, 2015, was $436,000, consisting of 80 percent of Sun’s $500,000 stockholders’ equity on that date and $36,000 goodwill. On May 1, 2016, Pam sold a 20 percent interest in Su

> Pam Corporation acquired a 75 percent interest in Sun Corporation on January 1, 2016. Financial statements of Pam and Sun Corporations for the year 2016 are as follows (in thousands): REQUIRED: Prepare consolidation workpapers for Pam Corporation and S

> Pop Corporation owns 100 percent (300,000 shares) of the outstanding shares of Son Corporation’s common stock on January 1, 2016. Its Investment in Son account on this date is $4,400,000, equal to Son’s $4,000,000 stockholders’ equity plus $400,000 goodw

> On January 1, 2016, Pam Corporation purchased a 40 percent interest in Sun Corporation for $1,600,000, when Sun’s stockholders’ equity consisted of $2,000,000 capital stock and $2,000,000 retained earnings. On September 1, 2016, Pam purchased an addition

> Pop Corporation increases its ownership interest in its subsidiary, Son Corporation, from 70 percent on January 1, 2016, to 90 percent at July 1, 2016. Son’s net income for 2016 is $200,000, and it declares $60,000 dividends on March 1 and $60,000 on Sep

> Calculate the parent’s income from its 75 percent–owned subsidiary if the reported net income of the subsidiary for the period is $100,000 and the consolidated entity has a constructive loss of $8,000 from the parent’s acquisition of subsidiary bonds.

> Prepare a journal entry (or entries) to account for the parent’s investment income for the current year if the reported income of its 80 percent–owned subsidiary is $50,000 and the consolidated entity has a $4,000 constructive gain from the subsidiary’s

> The following information related to intercompany bond holdings was taken from the adjusted trial balances of a parent and its 90 percent–owned subsidiary four years before the bond issue matured: Construct the consolidation workpaper

> If a subsidiary purchases parent bonds at a price in excess of recorded book value, is the gain or loss attributed to the parent or the subsidiary? Explain.

> Describe the process by which constructive gains on intercompany bonds are realized and recognized on the books of the affiliates. Does recognition of a constructive gain in consolidated financial statements precede or succeed recognition on the books of

> Compare a constructive gain on intercompany bonds with an unrealized gain on the intercompany sale of land.

> A company has a $1,000,000 bond issue outstanding with unamortized premium of $10,000 and unamortized issuance cost of $5,300. What is the book value of its liability? If an affiliate purchases half the bonds in the market at 98, what is the gain or loss

> Pop Corporation acquired 70 percent of the outstanding voting stock of Son Corporation for $182,000 cash on January 1, 2016, when Son’s stockholders’ equity was $260,000. All the assets and liabilities of Son were stat

> What are constructive gains and losses? Describe a transaction having a constructive gain.

> Do direct lending and borrowing transactions between affiliates give rise to unrealized gains or losses and unrecognized gains or losses?

> If a parent reports interest expense of $4,300 with respect to bonds held intercompany and the subsidiary reports interest income of $4,500 for the same bonds: (a) Was there a constructive gain or loss on the bonds? (b) Is the gain or loss attributed to

> What reciprocal accounts arise when one company borrows from an affiliate?

> A firm issues mandatorily redeemable preferred stock. Should this be classified as debt or equity in the consolidated financial statements?

> How should a company determine the fair value of long-term debt?