Question: PART I The framework created by Professor

PART I

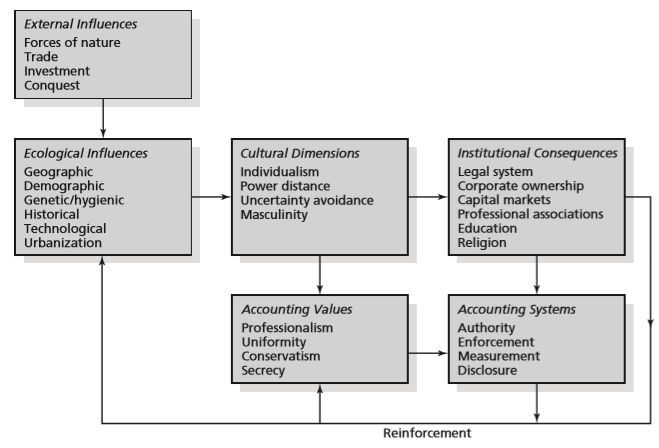

The framework created by Professor Sidney Gray in 1988 to explain the development of a country’s accounting system is presented in the chapter in Exhibit 2.8. Gray theorized that culture has an impact on a country’s accounting system through its influence on accounting values. Focusing on that part of a country’s accounting system comprised of financial reporting rules and practices, the model can be visualized as follows:

In short, cultural values shared by members of a society influence the accounting values shared by members of the accounting subculture. The shared values of the accounting subculture in turn affect the financial reporting rules and practices found within a country.

With respect to the accounting value of conservatism, Gray hypothesized that the higher a country ranks on the cultural dimensions of uncertainty avoidance and long-term orientation, and the lower it ranks in terms of individualism and masculinity, then the more likely it is to rank highly in terms of conservatism. Conservatism is a preference for a cautious approach to measurement. Conservatism is manifested in a country’s accounting system through a tendency to defer recognition of assets and items that increase net income and a tendency to accelerate the recognition of liabilities and items that decrease net income. One example of conservatism in practice would be a rule that requires an unrealized contingent liability to be recognized when it is probable that an outflow of future resources will arise but does not allow the recognition of an unrealized contingent asset under any circumstances.

Required:

Discuss the implications for the global convergence of financial reporting standards raised by Gray’s model.

PART II

Although Gray’s model relates cultural values to the accounting value of conservatism as it is embodied in a country’s financial reporting rules, it can be argued that the model is equally applicable to the manner in which a country’s accountants apply those rules:

Required:

Discuss the implications this argument has for the comparability of financial statements across countries, even in an environment of substantial international accounting convergence. Identify areas in which differences in cultural dimensions across countries could lead to differences in the application of financial reporting rules.

PART III

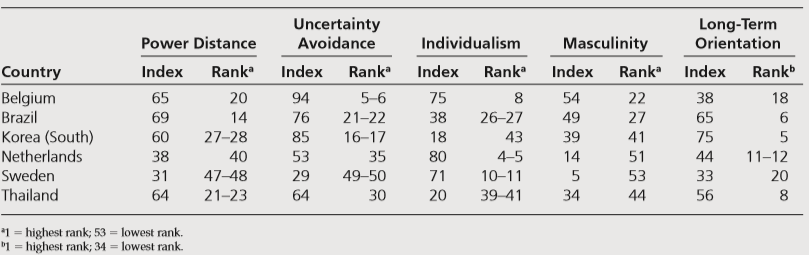

Cancan Enterprises Inc. is a Canadian-based company with subsidiaries located in Brazil, Korea, and Sweden. (Hofstede’s cultural dimension index scores for these countries are presented in Exercise 4.) Cancan Enterprises must apply Canadian GAAP worldwide in preparing consolidated financial statements. Cancan has developed a corporate accounting manual that prescribes the accounting policies based on Canadian GAAP that are to be applied by all the company’s operations. Each year Cancan’s internal auditors have the responsibility of ensuring that the company’s accounting policies have been applied consistently companywide.

Required:

Discuss the implications that the model presented in Part II of this case has for the internal auditors of Cancan Enterprises in carrying out their responsibilities.

Data from Exercise 4:

Cultural dimension index scores developed by Hofstede for six countries are reported in the following table:

Required:

Using Gray’s hypothesis relating culture to the accounting value of secrecy, rate these six countries as relatively high or relatively low with respect to the level of disclosure you would expect to find in financial statements. Explain.

Exhibit 2.8:

Transcribed Image Text:

Financial reporting rules and practices Cultural dimensions Accounting values Cultural dimensions Accounting values Accountant's application of financial reporting rules Uncertainty Avoidance Long-Term Orientation Power Distance Individualism Masculinity Country Index Rank Index Rank Index Rank Index Rank Index Rank Belgium 65 20 94 5-6 75 8 54 22 38 18 Brazil 69 14 76 21-22 38 26-27 49 27 65 6. 85 53 Korea (South) 60 27-28 16-17 18 43 39 41 75 Netherlands 38 40 35 80 4-5 14 51 44 11-12 Sweden 31 47–48 29 49-50 71 10-11 53 33 20 Thailand 64 21-23 64 30 20 39-41 34 44 56 8 *1 = highest rank; 53 = lowest rank. "1 = highest rank; 34 = lowest rank. External Influences Forces of nature Trade Investment Conquest Ecological Influences Cultural Dimensions Institutional Consequences Geographic Demographic Genetic/hygienic Historical Technological Urbanization Individualism Power distance Uncertainty avoidance Masculinity Legal system Corporate ownership Capital markets Professional associations Education Religion Accounting Values Professionalism Uniformity Conservatism Secrecy Accounting Systems Authority Enforcement Measurement Disclosure Reinforcement

> This exercise consists of three parts. Part A. On January 1, Year 1, Complete Company acquired 60 percent of the outstanding shares of Partial Company by paying $1,200,000 in cash. The fair value of Partial’s identifiable assets and liabilities is $2,000

> Sinto Bem Company issues a two-year note paying 5 percent interest on January 1, Year 1. The note sells for its par value of $1,000,000, and the company incurs issuance costs of $22,000. Which of the following amounts best approximates the amount of int

> Manometer Company sells accounts receivable of $10,000 to Eck Bank for $9,000 in cash. The sale does not qualify for de recognition of a financial asset. As a result, Manometer’s balance sheet will be different in which of the following ways? a. $1,000 m

> Halifax Corporation has a December 31 fi scal year-end. As of December 31, Year 1, the company has a debt covenant violation that results in a 10-year note payable to Nova Scotia Bank becoming due on March 1, Year 2. Halifax will be required to classify

> Recently the IASB revised IFRS 1. Required: What is the main reason for this revision?

> On December 31, Year 1, Airways Corp. issued $1 million in bonds at 5 percent annual interest, due December 31, Year 6, at a discount of $100,000. Airways incurred bank fees of $100,000, legal fees of $50,000, and salaries of $25,000 for its employees in

> An entity can justify a change in accounting policy if a. The change will result in a reliable and more relevant presentation of the financial statements. b. The entity encounters new transactions that are substantively different from existing or previou

> Which companies might Ford Motor Company include in a benchmarking study of the automobile industry, and in which countries are those companies located?

> In selecting an accounting policy for a transaction, which of the following is the first level within the hierarchy of guidance that should be considered? a. The most recent pronouncements of other standard-setting bodies to the extent they do not confli

> An entity must adjust its financial statements for an event that occurs after the end of the reporting period if a. The event occurs before the financial statements have been approved for issuance and it provides evidence of conditions that existed at th

> Which of the following best describes the accounting for goodwill subsequent to initial recognition? a. Goodwill is amortized over its expected useful life, not to exceed 20 years. b. Goodwill is tested for impairment whenever impairment indicators are p

> An entity incurs the following costs in connection with the purchase of a trademark: Purchase price of the trademark…………………………………………………………………………$80,000 Nonrefundable value added tax paid on the purchase of the trademark…………………..4,000 Training sales dep

> This exercise consists of two parts. Part A. T he following table summarizes the assets of the Rocker Division (a separate cash-generating unit) at December 31, Year 5, prior to testing goodwill for impairment. Property, Plant, and Equipment and Other I

> Which of the following is a criterion that must be met in order for an item to be recognized as an intangible asset? a. The item’s fair value can be measured reliably. b. The item is part of the entity’s activities aimed at gaining new scientific or tech

> Under IFRS, an entity that acquires an intangible asset may use the revaluation model for subsequent measurement only if a. The useful life of the intangible asset can be reliably determined. b. An active market exists for the intangible asset. c. The co

> An asset is considered to be impaired when its carrying amount is greater than its a. Net selling price. b. Value in use. c. Undiscounted future cash flows. d. Recoverable amount.

> Which of the following is not a criterion that must be met before an entity recognizes a provision related to a restructuring program? a. The entity has a detailed formal plan for the restructuring. b. The entity has begun implementation of the restructu

> When an entity chooses the revaluation model as its accounting policy for measuring property, plant, and equipment, which of the following statements is correct? a. When an asset is revalued, the entire class of property, plant, and equipment to which th

> Why might individual investors wish to include foreign companies in their investment portfolio?

> A company determined the following values for its inventory as of the end of its fiscal year: Historical cost……………………………………………………………………………….$50,000 Current replacement cost…………………………………………….…………………..35,000 Net realizable value……………………………………………………………….…

> A company incurred the following costs related to the production of inventory in the current year: Cost of materials…………………………………………………………….…..…………………..$100,000 Cost of direct labor……………………………………………………………………………………. 60,000 Allocation of variable overhea

> What is an advance pricing agreement?

> Under what conditions would a company apply for a correlative adjustment from a foreign tax authority? What effect do tax treaties have on this process?

> According to U.S. tax regulations, what are the five methods to determine the arm’s-length price in a sale of tangible property? How does the best-method rule affect the selection of a transfer pricing method?

> Bartholomew Corporation acquired 80 percent of the outstanding shares of Samson Company in Year 1 by paying $5,500,000 in cash. The fair value of Samson’s identifiable net assets is $5,000,000. Bartholomew uses the proportionate share of the acquired fir

> How can transfer pricing be used to reduce the amount of withholding taxes paid to a government on dividends remitted to a foreign stockholder?

> What is the performance evaluation objective of transfer pricing?

> What are the costs and benefits associated with entering into an advance pricing agreement?

> What is the maximum amount of foreign tax credit that a company will be allowed to take with respect to the income earned by a foreign operation?

> To which specific type of business combination does the concept of a group relate?

> Under what circumstances is it advantageous to take a deduction rather than a credit for taxes paid in a foreign country?

> What are the mechanisms used by countries to provide relief from double taxation?

> What are the different ways in which income earned in one country becomes subject to double taxation?

> What is the difference between the worldwide and territorial approaches to taxation?

> What is a tax haven? How might a company use a tax haven to reduce income taxes?

> Why might the effective tax rate paid on income earned within a country be different from that country’s national corporate income tax rate?

> Philosopher Stone Inc. incurred costs of $20,000 to develop an intranet Web site for internal use. The intranet will be used to store information related to company policies, customers, and products. Access to the intranet is password-protected and is re

> What procedures are used to translate the foreign currency income of a foreign branch into U.S. dollars for U.S. tax purposes? What procedures are used to translate the foreign currency income of a foreign subsidiary?

> What are the four factors that will determine the manner in which income earned by a foreign operation of a U.S. taxpayer will be taxed by the U.S. government?

> Under what circumstances will the income earned by a foreign subsidiary of a U.S. taxpayer be taxed as if it had been earned by a foreign branch?

> What is a group? Compare and contrast the different concepts of a group.

> What is a controlled foreign corporation? What is Subpart F income?

> What is a tax treaty? What is one of most important benefits provided by most tax treaties?

> How does the foreign tax credit basket system used in the United States affect the excess foreign tax credits generated by a U.S.-based company?

> What are excess foreign tax credits? How are they created and how can companies use them?

> How can a country’s tax system affect the manner in which an operation in that country is financed by a foreign investor?

> What are the advantages and disadvantages of using measures such as operating income before depreciation (OIBD) or earnings before interest, taxes, depreciation, and amortization (EBITDA) rather than net income in comparing profitability across foreign c

> In what ways does the timeliness of the publication of financial information differ across countries?

> During Year 1, Reforce Company conducted research and development on a new product. By March 31, Year 2, the company had determined the new product was technologically feasible, and the company obtained a patent for the product in April, Year 2. The comp

> How can more disclosure in the notes to the financial statements facilitate the analysis of foreign financial statements?

> Which balance sheet accounts give rise to purchasing power gains, and which accounts give rise to purchasing power losses?

> A foreign company prepares its financial statements in a foreign language and does not provide any convenience translations. How might this affect an analyst’s decision to invest in this company?

> Why should the fact that a foreign company presents its financial statements in a foreign currency present no significant problems in analyzing those statements?

> What are potential problems in using commercial databases as the source of financial statement information for foreign companies?

> A foreign company did not capitalize any interest in the current or past years, although such capitalization is required under U.S. GAAP. Why does an adjustment to reconcile this item to U.S. GAAP affect assets, expenses, and beginning retained earnings?

> How might differences across countries in the extent to which debt versus equity is the major source of financing affect profit margins, debt-to-equity ratios, and return on equity?

> How might differences in the extent to which countries apply the accounting concept of conservatism (some countries are more conservative than others) affect profit margins, debt-to-equity ratios, and returns on equity?

> Why should analysts be careful in comparing financial ratios across companies in different countries?

> What are the different features of financial statements that a foreign company might “translate” in a convenience translation?

> Define control. When does control exist in accordance with IAS 27?

> Stratosphere Company acquires its only building on January 1, Year 1, at a cost of $4,000,000. The building has a 20-year life, zero residual value, and is depreciated on a straight-line basis. The company adopts the revaluation model in accounting for b

> How does a company determine whether sales or noncurrent assets located in an individual foreign country are material?

> In what ways do International Financial Reporting Standards (IFRS) address the issue of accounting for changing prices (inflation)?

> Why is return on assets (net income/total assets) generally smaller under current cost accounting than under historical cost accounting?

> What are the major differences in the calculation of income between the historical cost (HC) model and the current cost (CC) model of accounting?

> What are the major differences in the calculation of income between the historical cost (HC) model and the general purchasing power (GPP) model of accounting?

> What types of entity-wide disclosures are required by IFRS 8?

> What are the major differences in the segment information required to be reported in accordance with IFRS and in accordance with U.S. GAAP?

> In accordance with IFRS 8, how does a company determine which operating segments to report separately?

> What are the circumstances under which a subsidiary could, and perhaps should, be excluded from consolidation?

> Why is it important that, in countries with high inflation, financial statements be adjusted for inflation?

> Why might a company want to hedge its balance sheet exposure? What is the paradox associated with hedging balance sheet exposure?

> Explain why the legal concept of control may be appropriate in some countries, such as Japan.

> Quantacc Company began operations on January 1, Year 1, and uses IFRS to prepare its financial statements. Quantacc reported net income of $100,000 in Year 5 and had stockholders’ equity of $500,000 at December 31, Year 5. The company wishes to determine

> Which translation method does U.S. GAAP require for operations in highly inflationary countries? What is the rationale for mandating use of this method?

> What does the term functional currency mean? How is the functional currency determined under IFRS and under U.S. GAAP?

> What are the major differences between IFRS and U.S. GAAP in the translation of foreign currency financial statements?

> How does a parent company determine the appropriate method for translating the financial statements of a foreign subsidiary?

> What are the major procedural differences in applying the current rate and temporal methods of translation?

> What is the concept underlying the current rate method of translation? What is the concept underlying the temporal method of translation? How does balance sheet exposure differ under these two methods?

> What factors create a balance sheet (or translation) exposure to foreign exchange risk? How does balance sheet exposure compare with transaction exposure?

> How are gains and losses on foreign currency borrowings used to hedge the net investment in a foreign subsidiary reported in the consolidated financial statements?

> What are the two major conceptual issues that must be resolved in translating foreign currency financial statements?

> How is the fair value of a foreign currency forward contract determined? How is the fair value of an option determined?

> On January 1, Year 1, Holzer Company hired a general contractor to begin construction of a new office building. Holzer negotiated a $900,000, five-year, 10 percent loan on January 1, Year 1, to finance construction. Payments made to the general contracto

> Why might a company prefer a foreign currency option rather than a forward contract in hedging a foreign currency firm commitment? Why might a company prefer a forward contract over an option in hedging a foreign currency asset or liability?

> How does the timing of hedges of the following differ? a. Foreign-currency-denominated assets and liabilities. b. Foreign currency firm commitments. c. Forecasted foreign currency transactions.

> What does the word hedging mean? Why do companies hedge foreign exchange risk?

> What factors create a foreign exchange gain on a foreign currency transaction? What factors create a foreign exchange loss?

> A company makes an export sale denominated in a foreign currency and allows the customer one month to pay. Under the two-transaction perspective, accrual approach, how does the company account for fluctuations in the exchange rate for the foreign currenc

> In what way is the accounting for a foreign currency borrowing more complicated than the accounting for a foreign currency account payable?

> How are changes in the fair value of an option accounted for in a cash flow hedge? In a fair value hedge?

> What are the differences in accounting for a forward contract used as a cash flow hedge of (a) a foreign-currency-denominated asset or liability and (b) a forecasted foreign currency transaction?

> How are foreign currency derivatives such as forward contracts and options reported on the balance sheet?

> What is an onerous contract? How are onerous contracts accounted for?

> Why is the principle of prudence clearly established in the German law?

> What is the Tokyo agreement?

> What was the accounting Big Bang in Japan?

> How have cultural factors influenced accounting practices in Japan?

> Identify three features of the Chinese accounting profession that are different from its counterparts in Anglo-American countries.