Question: SKD Limited is a biotechnology company that

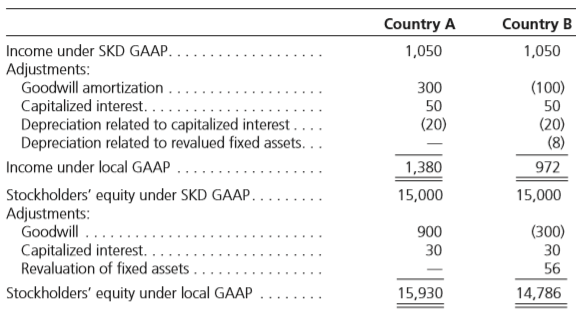

SKD Limited is a biotechnology company that prepares financial statements using internally developed accounting rules (referred to as SKD GAAP). To be able to compare SKD’s financial statements with those of companies in their home country, financial analysts in Country A and Country B prepared a reconciliation of SKD’s current year net income and stockholders’ equity. Adjustments were based on the actual accounting policies and practices followed by biotechnology companies in Country A and Country B. The following table shows the adjustments to income and stockholders’ equity made by each country analyst:

Description of Accounting Differences Goodwill. SKD capitalizes goodwill and amortizes it over a 20-year period. Goodwill is also treated as an asset in Country A and Country B. However, goodwill is not amortized in Country A, but instead is subjected to an annual impairment test. Goodwill is amortized over a 5-year period in Country B.

Interest. SKD expenses all interest immediately. In both Country A and Country B, interest related to self-constructed assets must be capitalized as a part of the cost of the asset.

Fixed assets. SKD carries assets on the balance sheet at their historical cost, less accumulated depreciation. The same treatment is required in Country A. In Country B, companies in the biotechnology industry generally carry assets on the balance sheet at revalued amounts. Depreciation is based on the revalued amount of ï¬xed assets.

Required:

1. With respect to the adjustments related to goodwill, answer the following:

a. Why does the adjustment for goodwill amortization increase net income under Country A GAAP but decrease net income under Country B GAAP?

b. Why does the goodwill adjustment increase stockholders’ equity in Country A but decrease stockholders’ equity in Country B?

c. Why are the adjustments to stockholders’ equity larger than the adjustments to income?

2. With respect to the adjustments made by the analyst in Country A related to interest, answer the following:

a. Why are there two separate adjustments to income related to interest?

b. Why does the adjustment to income for capitalized interest increase income, whereas the adjustment for depreciation related to capitalized interest decreases income?

c. Why is the positive adjustment to stockholders’ equity for capitalized interest smaller than the positive adjustment to income for capitalized interest?

3. With respect to the adjustments made by the analyst in Country B related to fixed assets, answer the following:

a. Why does the adjustment for depreciation related to revalued fixed assets decrease income, whereas the adjustment for revaluation of fixed assets increases stockholders’ equity?

Transcribed Image Text:

Country A Country B Income under SKD GAAP. 1,050 1,050 Adjustments: Goodwill amortization 300 (100) Capitalized interest... Depreciation related to capitalized interest.. Depreciation related to revalued fixed assets... 50 50 (20) (20) (8) Income under local GAAP .... 1,380 972 Stockholders' equity under SKD GAAP.. Adjustments: Goodwill . 15,000 15,000 900 (300) Capitalized interest. Revaluation of fixed assets . 30 30 56 Stockholders' equity under local GAAP 15,930 14,786 ....

> Ultima Company offers its customers discounts to purchase goods and take title before they actually need the goods. The company offers to hold the goods for the customers until they request delivery. This relieves the customers from making room in their

> Mishima Technologies Company introduced Product X to the market on December 1. The new product carries a one-year warranty. In its first month on the market, Mishima sold 1,000 units of the new product for a total of $1,000,000. Customers have an uncondi

> Gotti Manufacturing Inc., a U.S.-based company, operates in three countries in addition to the United States. The following table reports the company’s pretax income and the applicable tax rate in these countries for the year ended Dece

> Updike and Patterson Investments Inc. (UPI) holds equity investments with a cost basis of $250,000. UPI accounts for these investments as available-for sale securities. As such, the investments are carried on the balance sheet at fair value, with unreali

> SC Masterpiece Inc. granted 1,000 stock options to certain sales employees on January 1, Year 1. The options vest at the end of three years (cliff vesting) but are conditional upon selling 20,000 cases of barbecue sauce over the three-year service period

> Bessrawl Corporation is a U.S.-based company that prepares its consolidated financial statements in accordance with U.S. GAAP. The company reported income in 2014 of $1,000,000 and stockholders’ equity at December 31, 2014, of $8,000,000. The CFO of Bess

> On January 2, Year 1, Argy Company’s board of directors granted 12,000 stock options to a select group of senior employees. The requisite service period is three years, with one-third of the options vesting at the end of each calendar year (graded vestin

> White River Company has a defined benefit pension plan in which the fair value of plan assets (FVPA) exceeds the present value of defined benefit obligations (PVDBO). The following information is available at December 31, Year 1 (amounts in millions):

> In what way has the development of accounting and auditing in China differed from that in other countries?

> T he Baton Rouge Company compiled the following information for the current year related to its defined benefit pension plan: Present value of defined benefit obligation, beginning of year……………………..$1,000,000 Fair value of plan assets, beginning of year…

> In January 1, Year 1, the Hoverman Corporation made amendments to its defined benefit pension plan, resulting in $150,000 of past service costs. The plan has 100 active employees with an average expected remaining working life of 10 years. There currentl

> The Kissel Trucking Company Inc. has a defined benefit pension plan for its employees. At December 31, Year 1, the following information is available regarding Kissel’s plan: Fair value of plan assets……………………………………………………$30,000,000 Present value of defi

> T he board of directors of Chestnut Inc. approved a restructuring plan on November 1, Year 1. On December 1, Year 1, Chestnut publicly announced its plan to close a manufacturing division in New Jersey and move it to China, and the company’s New Jersey e

> On June 1, Year 1, Charley Horse Company entered into a contract with Good Feed Company to purchase 1,000 bales of organic hay on January 30, Year 2, at a price of $30 per bale. The hay will be grown especially for Charley Horse and is needed to feed the

> In Year 1, Better Sleep Company began to receive complaints from physicians that patients were experiencing unexpected side effects from the company’s sleep apnea drug. The company took the drug off the market near the end of Year 1. During Year 2, the c

> On January 1, Year 1, an entity acquires a new machine with an estimated useful life of 20 years for $100,000. The machine has an electrical motor that must be replaced every fi ve years at an estimated cost of $20,000. Continued operation of the machine

> Iptat International Ltd. provided the following reconciliation from IFRS to U.S. GAAP in its most recent annual report (amounts in thousands of CHF): Required: a. Explain why U.S. GAAP adjustment (a) results in an addition to net income. Explain why U

> With its broad portfolio of market-leading businesses, the Jardine Matheson Group is an Asian-based conglomerate with extensive experience in the region. Its business interests include Jardine Pacific, Jardine Motors Group, Hongkong Land, Dairy Farm, Man

> Madison Company acquired a depreciable asset at the beginning of Year 1 at a cost of $12 million. At December 31, Year 1, Madison gathered the following information related to this asset: Carrying amount (net of accumulated depreciation) ……………………………$10

> Briefly describe the current requirement for companies in Mexico to account for the effect of inflation in their annual financial statements.

> Jefferson Company acquired equipment on January 2, Year 1, at a cost of $10 million. The equipment has a five-year life, no residual value, and is depreciated on a straight-line basis. On January 2, Year 3, Jefferson Company determines the fair value of

> Godfrey Company constructed a new, highly automated chemical plant in Year 1, which began production on January 1, Year 2. The cost to construct the plant was $5,000,000: $1,500,000 for the building and $3,500,000 for machinery and equipment. The useful

> Quick Company acquired a piece of equipment in Year 1 at a cost of $100,000. The equipment has a 10-year estimated life, zero salvage value, and is depreciated on a straight-line basis. Technological innovations take place in the industry in which the co

> Stevenson Corporation acquires a one-year-old building at a cost of $500,000 at the beginning of Year 2. The building has an estimated useful life of 50 years. However, based on reliable historical data, the company believes the carpeting will need to be

> In what way does the fair value model for investment property differ from the revaluation model for property, plant, and equipment?

> How are the Anglo and less developed Latin cultural areas expected to differ with respect to the accounting values of conservatism and secrecy?

> How is depreciation determined for an item of property, plant, and equipment that is comprised of significant parts, such as an airplane?

> In accounting for post-employment benefits, when are past service costs and actuarial gains and losses recognized in income?

> Steffen-Zweig Company exchanges two used printing presses with a total net book value of $24,000 ($40,000 cost less accumulated depreciation of $16,000) for a new printing press with a fair value of $24,000 and $3,000 in cash. The fair value of the two u

> What is the arm’s-length range of transfer pricing, and how does it affect the selection of a transfer pricing method?

> What is the significance of Bulletin A-8 of the Mexican Institute of Public Accountants?

> Why is there often a conflict between the performance evaluation and cost minimization objectives of transfer pricing?

> What are possible cost-minimization objectives that a multinational company might wish to achieve through transfer pricing?

> What are the various types of intercompany transactions for which a transfer price must be determined?

> What is a constructive obligation

> Were the EU directives effective in generating comparability of financial statements across companies located in member nations? Why or why not?

> To determine the amount at which inventory should be reported on the December 31, Year 1, balance sheet, Monroe Company compiles the following information for its inventory of Product Z on hand at that date: • Historical cost……………………………………………………………..$2

> How are convertible bonds measured initially on the balance sheet?

> What are the four classes of financial assets?

> How is an exchange of goods that are similar in nature and value accounted for?

> What is the accounting treatment for debt extinguishment costs? Debt modification costs?

> How are foreign branch income and foreign subsidiary income taxed differently by a company’s home country?

> How are costs associated with the issuance of bonds payable accounted for?

> What happens if a significant amount of held-to-maturity investments is reclassified as available- for-sale?

> How are deferred taxes classified on the balance sheet?

> What is the cutoff date for the occurrence of events after the reporting period requiring adjustment to the financial statements?

> What are the rules related to the recognition of a deferred tax asset?

> What is a gain on bargain purchase?

> As a result of a downturn in the economy, Optiplex Corporation has excess productive capacity. On January 1, Year 3, Optiplex signed a special order contract to manufacture custom-design generators for a new customer. The customer requests that the gener

> What are the types of differences that exist between IFRS and U.S. GAAP?

> How is goodwill measured in a business combination with a non-controlling interest?

> How does an individual taxpayer qualify for the foreign earned income exclusion?

> Which intangible assets are subject to annual impairment testing?

> What is the current treatment with respect to borrowing costs?

> As expressed in IAS 1, what is the overriding principle that should be followed in preparing IFRS-based financial statements?

> To what extent have IFRS been adopted by countries around the world?

> Under what conditions should a firm claim to prepare financial statements in accordance with IFRS?

> What are the alternative methods used internationally to present fixed assets on the balance sheet subsequent to acquisition?

> What is a provision, and when must a provision be recognized?

> When a previously recognized impairment loss is subsequently reversed, what is the maximum amount at which the affected asset may be carried on the balance sheet?

> Indicate whether each of the following describes an accounting treatment that is acceptable under IFRS, U.S. GAAP, both, or neither, by checking the appropriate box. Acceptable Under IFRS U.S. GAAP Both Neither • A company takes out a loan to finan

> What are the different ways in which financial statements differ across countries?

> What is the benefit provided to an individual taxpayer through the foreign earned income exclusion?

> What are the two most common methods used internationally for the order in which assets are listed on the balance sheet? Which of these two methods is most common in North America? In Europe?

> Why might a company want its stock listed on a stock exchange outside of its home country?

> What financial reporting issues arise as a result of making a foreign direct investment?

> What accounting issues arise for a company as a result of engaging in international trade (imports and exports)?

> Which group has negotiated the greatest number of advance pricing agreements with the U.S. Internal Revenue Service (IRS)? a. Foreign parent companies with branches and subsidiaries in the United States. b. U.S. parent companies with branches and subsidi

> U.S. Treasury Regulations require the use of one of five specified methods to determine the arm’s-length price in a sale of tangible property. Which of the following is not one of those methods? a. Cost-plus method. b. Market-based method. c. Profit spli

> Market-based transfer prices lead to optimal decisions in which of the following situations? a. When interdependencies between the related parties are minimal. b. When there is no advantage or disadvantage to buying and selling the product internally rat

> Which of the following is not a method commonly used for establishing transfer prices? a. Cost-based transfer price. b. Negotiated price. c. Market-based transfer price. d. Industry wide transfer price.

> Which of the following types of transaction is most likely to be audited? a. Sales of tangible property. b. Licenses of intangible property. c. Intercompany loans. d. Intercompany services.

> Bridget’s Bakery Inc. enters into a new operating lease for a 10-year term at a monthly rental of $2,500. To induce Bridget’s Bakery into the lease, the lessor agreed to a free-rent period for the first three months. Required: Determine the amount of le

> How are the estimated costs of removing and dismantling an asset handled upon initial recognition of the asset?

> Which international organization has developed transfer pricing guidelines that are used as the basis for transfer pricing laws in several countries? a. World Bank. b. Organization for Economic Cooperation and Development. c. United Nations. d. Internati

> Which of the following methods does U.S. tax law always require to be used in pricing intercompany transfers of tangible property? a. Comparable uncontrolled price method. b. Comparable profits method. c. Cost-plus method. d. Best method.

> Which of the following would be an acceptable transfer price under the comparable profits method? a. $700 b. $750 c. $795 d. $825

> Which of the following would be an acceptable transfer price under the cost plus method? a. $700 b. $750 c. $795 d. $825

> Which of the following would be an acceptable transfer price under the resale price method? a. $700 b. $750 c. $795 d. $825

> Which of the following objectives is not achieved through the use of lower transfer prices? a. Improving the competitive position of a foreign operation. b. Minimizing import duties. c. Protecting foreign currency cash flows from currency devaluation. d.

> Jordan Inc., a U.S. company, is required to translate the foreign income generated by its foreign operation. To determine U.S. taxable income, what must Jordan use to translate the income of its foreign branch into U.S. dollars? a. The exchange rate at t

> What are the two most common methods of eliminating the double taxation of income earned by foreign corporations? a. Exempting foreign source income and deducting all foreign taxes paid. b. Deducting all foreign taxes paid and providing a foreign tax cre

> Poole Corporation is a U.S. company with a branch in China. Income earned by the Chinese branch is taxed at the Chinese corporate income tax rate of 25 percent and at the rate of 35 percent in the United States. What is this an example of? a. Capital-exp

> Kerry is a U.S. citizen residing in Portugal. Kerry receives some investment income from Spain. Why might Kerry be expected to pay taxes on the investment income to the United States? a. The United States taxes its citizens on their worldwide income. b.

> In what way did both the domestic international sales corporation and the foreign sales corporation violate international trade agreements?

> This problem is comprised of three parts. Part A. Fields Company sells a building to Victory Finance Company. The selling price of the building is $500,000, which approximates its fair value, and the carrying amount is $400,000. Fields then leases the bu

> Why might companies have an incentive to finance their foreign operations with as much debt as possible? a. Interest payments are generally tax deductible. b. Withholding rates are lower for dividends. c. Withholding rates are lower for interest. d. Both

> Which of the following item(s) might provide an MNC with a tax-planning opportunity as it decides where to locate a foreign operation? a. Differences in corporate tax rates across countries. b. Differences in local tax rates across countries. c. Whether

> Which of the following items is not a tax benefit provided by Congress to U.S. citizens working abroad? a. Foreign earned income exclusion. b. Foreign tax credit. c. Dividend income exclusion. d. Foreign housing exclusion.

> Why might a company involved in international business find it beneficial to establish an operation in a tax haven? a. The OECD recommends the use of tax havens for corporate income tax avoidance. b. Tax havens never tax corporate income. c. Tax havens a

> In Year 3, how much excess foreign tax credit can Powell carry back? a. $7,500. b. $6,000. c. $1,000. d. $0.

> For Year 3, what is the net U.S. tax liability? a. $35,000. b. $0. c. $1,000. d. $6,000.

> For Year 1, Year 2, and Year 3, what is the foreign tax credit allowed in the United States? a. $7,500, $6,000, and $0. b. $18,750, $29,000, and $36,000. c. $75,000, $100,000, and $100,000. d. $18,750, $29,000, and $35,000.

> In deciding whether to establish a foreign operation, which factor(s) might a multinational corporation (MNC) consider? a. After-tax returns from competing investment locations. b. The tax treatments of branches versus subsidiaries. c. Withholding rates

> The functional currency of Garland Inc.’s Japanese subsidiary is the Japanese yen. Garland borrowed Japanese yen as a partial hedge of its investment in the subsidiary. How should the transaction gain on the foreign currency borrowing be reported in Garl

> What is treaty shopping?

> In accordance with U.S. generally accepted accounting principles (GAAP), which translation combination would be appropriate for a foreign operation whose functional currency is the U.S. dollar? Method Treatment of Translation Adjustment Temporal Te

> Atlanta Tours Company entered into a five-year lease on January 1, Year 1, with Duck Boats Inc. for a customized duck boat. Duck Boats Inc. will provide a vehicle to Atlanta Tours Company with the words “Gone with the Wind” carved into the sides. Followi

> Which method of translation maintains, in the translated financial statements, the underlying valuation methods used in the foreign currency financial statements? a. Current rate method; income statement translated at average exchange rate for the year.

> Which of the following best explains how a translation loss arises when the temporal method of translation is used to translate the foreign currency financial statements of a foreign subsidiary? a. The foreign subsidiary has more monetary assets than mon