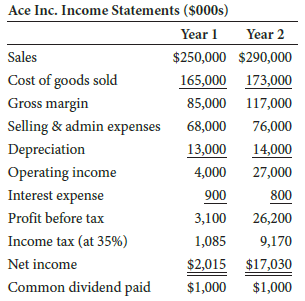

Question: Suppose year 2’s days of receivables

Suppose year 2’s days of receivables were reduced to 35. How much cash would be freed up?

Transcribed Image Text:

Ace Inc. Income Statements ($000s) Year 1 Year 2 Sales $250,000 $290,000 Cost of goods sold 165,000 173,000 Gross margin 85,000 117,000 Selling & admin expenses 68,000 76,000 Depreciation 13,000 14,000 Operating income 4,000 27,000 Interest expense 900 800 Profit before tax 3,100 26,200 Income tax (at 35%) 1,085 9,170 Net income $2,015 $17,030 Common dividend paid $1,000 $1,000 Ace Inc. Balance Sheets at December 31 ($000s) Year 1 Year 2 Cash $2,400 $2,800 Accounts receivable 30,000 32,000 Inventories 18,000 20,000 Total current assets 50,400 54,800 Net property and equipment 20,000 24,000 Total assets $70,400 $78,800 Notes payable: Bank $20,185 $12,555 Accounts payable 14,000 16,000 Total current liabilities 34,185 28,555 Long-term debt Common equity 22,000 20,000 14,215 30,245 Total liabilities and equity $70,400 $78,800

> Briefly define the following terms: dendrogram, icicle plot, agglomeration schedule and cluster membership.

> What is a recursive model? Why is this aspect relevant in SEM?

> How do we determine whether the difference between two structural path coefficients is significant?

> What is a structural theory and how is it different from measurement theory?

> What is a second-order factor model? How is it different from a first-order factor model?

> What is average variance extracted? Why is it useful to calculate this statistic?

> What characteristics distinguish SEM from other multivariate techniques?

> What is the difference between internal and external analysis of preference data?

> Describe the ways in which the reliability and validity of MDS solutions can be assessed.

> What guidelines are used for deciding on the number of dimensions in which to obtain an MDS solution?

> Describe the direct and derived approaches to obtaining MDS input data.

> Describe the factor analysis model.

> Describe the steps involved in conducting MDS.

> What is meant by a spatial map?

> Identify two marketing research problems where MDS could be applied. Explain how you would apply MDS in these situations.

> What procedures are available for assessing the reliability and validity of conjoint analysis results?

> Graphically illustrate what is meant by part-worth functions.

> How can regression analysis be used for analysing conjoint data?

> Describe the pairwise approach to constructing stimuli in conjoint analysis.

> Describe the full-profile approach to constructing stimuli in conjoint analysis.

> What is involved in formulating a conjoint analysis problem?

> What are some of the uses of cluster analysis in marketing?

> What are the major uses of factor analysis?

> How is cluster analysis used to group variables?

> Describe some procedures available for assessing the quality of clustering solutions.

> What role may qualitative methods play in the interpretation of clusters?

> What is involved in the interpretation of clusters?

> How is the fit of the factor analysis model examined?

> What are surrogate variables? How are they determined?

> What guidelines are available for deciding the number of clusters?

> What guidelines are available for interpreting the factors?

> Why is it useful to rotate the factors? Which is the most common method of rotation?

> What is a scree plot? For what purpose is it used?

> How is factor analysis different from multiple regression and discriminant analysis?

> Suppose a preferred share pays perpetual quarterly dividends of $1.00 and has a per annum dividend yield of 8 percent. What is the fair value of this preferred share?

> What is the profitability index for the project in question 6? discount rate = 10.0% initial investment = ($40,000) CF1 = $15,000 CF2 = $20,000 CF3 = $25,000 NPV = $8,948.16 = -$40,000 + $15,000/(1.10) + $20,000/(1.10)2 + $25,000/(1.10)

> What is the internal rate of return for the project in question 6? discount rate = 10.0% initial investment = ($40,000) CF1 = $15,000 CF2 = $20,000 CF3 = $25,000 NPV = $8,948.16 = -$40,000 + $15,000/(1.10) + $20,000/(1.10)2 + $25,000/(1

> What is the net present value of a project with a $40,000 initial investment and expected net cash flows of $15,000, $20,000, and $25,000 in each of the next three years, assuming an appropriate discount rate of 10 percent?

> Wholesale Lumber, Ltd. is a firm that distributes lumber to building supply and home improvement retail stores. The firm’s cost of sales for the most recent year was $45 million, its beginning inventory was $16 million, and its ending inventory was $18 m

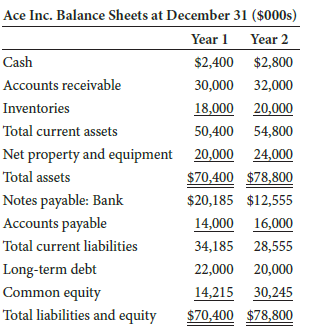

> What are the three methods by which a firm can improve its working capital gap? Ace Inc. Income Statements ($000s) Year 1 Year 2 Sales $250,000 $290,000 Cost of goods sold 165,000 173,000 Gross margin 85,000 117,000 Selling & admin expenses 68,000 7

> IOU Inc. has EBIT of $58,000, depreciation and amortization of $12,000, interest expenses of $21,000, principal repayments of $17,000, and a tax rate of 35 percent. Calculate IOU Inc.’s interest coverage ratio and debt service coverage ratio.

> Deb Co. has interest-bearing debt of $122 million, non–interest-bearing debt of $33 million, and equity of $76 million. Calculate Deb Co.’s debt-to-assets, debt-to-equity, and long-term-debt-to-capital ratios.

> Quick-E Inc.’s current assets consist of cash of $5 million, account receivables of $27 million, inventory of $37 million, and it has current liabilities of $48 million. Calculate Quick-E’s current ratio and quick ratio.

> Estimate the working capital gap for each year. Ace Inc. Income Statements ($000s) Year 1 Year 2 Sales $250,000 $290,000 Cost of goods sold 165,000 173,000 Gross margin 85,000 117,000 Selling & admin expenses 68,000 76,000 Depreciation 13,000 14,000

> What is the payback period of a project with average annual cash outflows of $8,000, average annual cash inflows of $10,000, and an initial investment of $13,000?

> Fixem Co. has revenue of $125 million, property and equipment of $42 million, and accumulated depreciation and amortization of $6 million. Estimate the fixed asset turnover ratio.

> BE Enterprises has fixed costs of $50 million. Its gross margin percentage is 18 percent. What sales level must it achieve in order to break even?

> Estimate the age of inventory for each year. Ace Inc. Income Statements ($000s) Year 1 Year 2 Sales $250,000 $290,000 Cost of goods sold 165,000 173,000 Gross margin 85,000 117,000 Selling & admin expenses 68,000 76,000 Depreciation 13,000 14,000 Op

> Suppose year 2’s days of payables were increased to 40. How much cash would be freed up? Ace Inc. Income Statements ($000s) Year 1 Year 2 Sales $250,000 $290,000 Cost of goods sold 165,000 173,000 Gross margin 85,000 117,000 Sellin

> Suppose year 2’s days of inventory were reduced to 35. How much cash would be freed up? Ace Inc. Income Statements ($000s) Year 1 Year 2 Sales $250,000 $290,000 Cost of goods sold 165,000 173,000 Gross margin 85,000 117,000 Selling

> Eeeva Inc. has an EBIT of $1.5 million. The tax rate is 35 percent. Eeeva has a debt of $2.5 million and common equity of $5 million. Eeeva’s cost of capital is estimated to be 11 percent. Calculate Eeeva’s EVA.

> Extra Value Inc. is expected to generate EBIT of $20 million next year, with anticipated depreciation and amortization of $3 million. Extra Value has debt of $40 million. Comparable firms are trading at average forward-looking EV/EBITDA ratios of five ti

> Pepper Inc. is expected to have before-tax earnings of $2.5 million next year. The tax rate is 35 percent. There are 2 million common shares outstanding. Comparable firms in the same industry are estimated to have price-earnings multiples of 10 to 16. Es

> Now suppose BetLev wishes to have a target capital structure of 50 percent debt and 50 percent equity. What will be its levered beta at the target capital structure?

> Suppose BetLev Inc. has a capital structure with 65 percent debt and 35 percent equity, a (levered) beta of 1.3, and a corporate tax rate of 35 percent. Estimate the unlevered beta of BetLev.

> Suppose an all-equity firm has a beta estimated to be 1.2. If the firm changes its capital structure such that its debt-to-equity ratio is now 0.4, what should be the revised beta estimate if it also faces a tax rate of 35 percent?

> Suppose a firm has an EBIT of $5 million, interest expenses of $2 million, depreciation expenses of $1 million, and a tax rate of 35 percent. Its bank agrees to lend up to 4 times its EBITDA. How much debt can the firm borrow from the bank?

> Assume that a firm’s earnings per share (EPS) are expected to be $2.00 next year and that analysts have determined that an appropriate forward-looking multiple is 15 times the projected earnings. What should the stock price be?

> What is the value of an all-equity firm that: a. has a dividend payout ratio of 100 percent b. is expected to generate net income each year (forever) of $1 million, and c. has a required equity return (also the ROE) of 16 percent?

> What is the present value of a perpetual stream of annual cash flows of $100, with the first cash flow to be received in one year, assuming a discount rate of 8 percent?

> How will your answer in question #3 change if we now relax the M&M perfect capital markets assumption and incorporate a corporate tax rate of 35 percent? Ke = Kc + (Kc – Kd) (D/E) Kc = 10.0% Kd = 6.0% D = 1.2 E = 1.0 ( Ke = 14.8% = 10% + (10

> According to Modigliani and Miller (M&M), in a world of perfect capital markets, what will be the expected equity return (or cost of equity) for a firm that has a cost of capital of 10 percent, a cost of debt of 6 percent, debt valued at $1.2 million, an

> Fastest Company’s common shares are currently trading for $30. It is expected that Fastest Company will pay an annual common share dividend of $2 next year. It is also expected that the dividend will grow at a rate of 5 percent each year in perpetuity. B

> How would your answer in question 5 change if Fastest Company’s debt rating deteriorated to BBB and the typical spread between long-term government yields and BBB-rated firms was 3 percent?

> Fastest Company has a debt rating of A and a tax rate of 35 percent. The current long-term government bond yield is 2 percent. Suppose the typical spread between long-term government yields and A-rated firms is about 2 percent. Estimate Fastest Company’s

> Suppose Fastest Company is offered accounts payable terms of “2 percent, 10 days, net 30 days” but its suppliers actually allow it to repay in 45 days. Estimate the annualized opportunity cost for not taking advantage of the 2 percent discount for the qu

> Suppose Fastest Company, a new start-up firm, initially has $50 million in common equity and its common shareholders require or expect a return of 14 percent on this investment. After the first year, Fastest Company makes an after-tax profit of $6 millio

> Suppose Fastest Company’s current balance sheet showed book value weights of 32 percent debt, 11 percent preferred shares, and 57 percent common equity. Assuming its cost of debt was 3 percent, the cost of preferred shares was 5 percent, and the cost of

> How would your answer in question 13 change if the current long-term government bond yield was 3 percent and Fastest Company’s beta was 1.5? Ke (CAPM method) = Rf + β x MRP = 2.00% + 1.15 x 5.00% = 7.75%

> Suppose the current long-term government bond yield is 2 percent and the estimated market risk premium is 5 percent. Fastest Company’s beta is estimated to be 1.15. Using CAPM, estimate Fastest Company’s cost of common equity.

> How would your answer in question 9 change if the dividend was expected to be $1.80 and the perpetual growth of the dividend 4 percent? Based on the constant growth dividend discount model: Ke = DIV1/Po + g DIV1 = $2.00 P0 = $30.00 g = 5%

> Consider the same estimated costs as in question 15. Fastest Company is not planning to issue preferred shares in the future but anticipates a target capital structure of 40 percent debt and 60 percent common equity. Reestimate Fastest Companyâ

> What is the internal rate of return for the project in question 2? discount rate = 8.0% initial investment = ($12,000) CF1 = $15,000 NPV = $1,889 = -$12,000 + $15,000/(1.08) = -$12,000 + $13,888.89

> What is the fair value today of a common share with expected annual dividends of $1.00, $1.05, and $1.10 in each of the next three years and an expected share price of $20 in three years, assuming a required return of 9 percent?

> Calculate the present value (PV) of a cash inflow of $500 in one year and a cash inflow of $1,000 in five years, assuming a discount rate of 15 percent.

> Consider two bonds, Bond C and Bond D, both with a yield to maturity of 10 percent and with 5 years to maturity. These are standard bonds with semiannual coupon payments. Bond C has a coupon rate of 10 percent (with semiannual coupon payments); Bond D do

> Jesters-R-Us, Inc. is a publicly traded company that has assets on its balance sheet of $125 million and liabilities of $75 million. The firm also has 4 million common shares that are currently trading for $21 per share. Estimate the firm’s market-to-boo

> Bigco’s balance sheet one year ago indicated retained earnings of $450 million. This year, Bigco’s net income was $35 million. It paid its preferred shareholders a dividend of $5 million and paid its common shareholders a regular dividend of $6 million,

> Explain why a company may have deferred income taxes on its balance sheet.

> If a firm has goodwill on its balance sheet, what, if anything, does this imply about the firm’s previous acquisition activities?

> Why do we refer to depreciation and amortization as “noncash items”?

> Consider the bonds in question 5. Suppose interest rates decline, causing the yield to maturity for each bond to immediately decline to 9 percent. What is the new price of each bond? (Consider the semiannual yield to maturity.)

> Explain why equity is not the same as cash.

> Describe the two hypotheses that explain the shape of the yield curve.

> What is deflation?

> Why is low and steady inflation important?

> What are the three goals of the Federal Reserve?

> What are the four key components of gross domestic product?

> Describe the four stages of the business cycle.

> What information would need to be gathered in order to assess the economy’s current position within the business cycle?

> Develop a list of factors that would result in a firm having high supply risk and high demand risk.

> Develop a list of key success factors in the auto manufacturing industry.

> Wally Wholesale has revenue of $487,000, end-of year receivables of $112,000, account payables of $70,000, and inventory of $91,000. Assume purchases equal cost of sales of $372,000. Estimate Wally Wholesale’s age of inventory, age of receivables, and ag

> Describe Porter’s Five Forces that govern the competition within an industry. Compare and contrast the Porter analysis for the utilities industry and for the jewelry industry (part of the consumer discretionary industry).

> Compare the typical profitability of a stage 2 firm versus a stage 3 firm.

> Describe the three shapes of the yield curve that tend to be associated with different business cycle stages.

> What are the two key drivers of value?

> What is the primary goal of an enterprise?

> How do sole proprietorships, general partnerships, limited liability companies, S corporations, and C corporations differ?

> How is a recession typically measured?