Question: The financial report of Montefiore Medical Center,

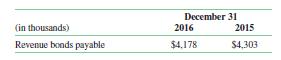

The financial report of Montefiore Medical Center, which operates a major New York City hospital, included the following item in a summary of longâ€term debt outstanding (dates changed):

An explanatory note indicated the following:

The proceeds from the 8.625 percent revenue bonds, dated November 1, 2002, issued by the Dormitory Authority of the State of New York, were used by the Medical Center to construct a parking garage. The fair value of these bonds was estimated to be approximately $5.1 million and $5.4 million on December 31, 2016, and December 31, 2015, respectively, using a discounted cash flow analysis based on the Medical Center’s incremental borrowing rates for similar types of borrowing arrangements. The bonds are payable serially through June 30, 2033, at increasing annual amounts ranging from $130,000 in 2017 to $500,000 in 2033. Bonds may be redeemed before maturity, for which call premiums are 0.5 percent through June 30, 2017, after which call premiums cease. Under the terms of the revenue bond agreement, certain escrow funds are required to be maintained. On December 31, 2016, escrow assets aggregated approximately $1.2 million, which exceeded minimum escrow requirements.

1. Why would the fair value of the bonds, as calculated by the center, be so much greater than their face value?

2. The note states that the “bonds are payable serially.†What does that mean?

3. Assuming that prevailing interest rates remain constant, why would the market price of the bonds be greater before June 30, 2017, than after?

4. Is it likely that the fair value of the bonds is as great as the fair value calculated by the center? Explain.

Transcribed Image Text:

December 31 (in thousands) 2016 2015 Revenue bonds payable $4,178 $4,303

> Prepare general fund journal entries to record the following cash transfers that a city made from its general fund to other funds. Be sure your entry reflects the nature of the transfer. 1. $4,000,000 to provide start‐up capital to a newly established in

> Lemon County permits employees to accumulate any sick leave that they do not take. If employees do not use accumulated sick leave, then they will be paid for those days upon retirement or termination (up to a maximum of 45 days). In 2018 employees earned

> In 2018, employees of Pecos River County earned $5 million in vacation pay. They were paid for $4.2 million but deferred taking the balance of their earned vacations until subsequent years. Also, employees were paid $0.7 million for vacation earned in pr

> In a recent year Ives Township acquired six police cars at a total cost of $200,000. The vehicles are expected to have a useful life of four years. 1. Prepare the journal entries that the township would make in its general fund in the year of acquisition

> The schedule that follows reports the beginning balances and activity during the year in a town’s supplies fund (a governmental fund). The government accounts for supplies on a purchases basis (in thousands). Fund balance (unassigned), January 1………………………

> The following schedule shows the amounts related to supplies that a city debited and credited to the indicated accounts during a year (not necessarily the year‐end balances), excluding closing entries. The organization records its budge

> The Boyd School District began a recent fiscal year with $3,000 of supplies in stock. During its fiscal year, it engaged in the following transactions relating to supplies: • It purchased supplies at a cost of $22,000. • It paid for $19,000 of the suppli

> A city prepares its budget on a cash basis. For each of the following indicate the amount (if any) of an expenditure/expense that the city would be recognize in (1) its budget, (2) its fund statements, and (3) its government‐wide statements. Provide a

> The Eaton School District engaged in the following transactions during its fiscal year ending August 31, 2018. • It established a purchasing department, which would be accounted for in a new internal service fund, to purchase supplies and distribute them

> Select the best answer. Assume that Nolanville’s fiscal year ends on December 31. 1. Nolanville’s payroll for one of its departments is $15,000 per week. It pays its employees on the Thursday of the week following that in which the wages and salaries ar

> A city is weighing the costs and benefits of a new convention center. The center would be accounted for in an enterprise fund. It would cost $20 million and would be funded from the proceeds of 20‐year revenue bonds. Officials estimate that the center wo

> On what basis does the government account for its inventories (purchases or consumption)? Does the City maintain a “fund balance‐nonspendable” amount for inventories?

> A state government provided several grants to school districts and local governments during its fiscal year ending August 31. 1. On August 1, 2018, it announced a $2 million grant to a local school district for the purchase of computers. The district can

> As indicated in Chapter 2, the GASB defines assets as “resources with present service capacity that the government presently controls.” It explains that present service capacity of an asset is its capability to enable the government to provide services a

> Highbridge County imposes a motor fuel tax to finance road maintenance. It therefore accounts for all road maintenance in a special revenue fund, the entire fund balance of which is legally restricted. The fund’s statement of revenues,

> The following information was abstracted from a note, headed “Interfund Transactions,” to the financial statements of Independence, Missouri. Interfund Charges for Support Services Interfund charges for support servi

> A town plans to borrow about $10 million and is considering three alternatives. A town official requests your guidance on the economic cost of each of the arrangements and advice as to how they would affect the town’s reported expenditures. 1. For each o

> The Mainor School District is about to establish a 30‐machine computer lab. It is considering six alternative means of acquiring and financing the machines: 1. Buy the machines outright; cost will be $60,000. 2. Buy the machines and finance them with a $

> A city is having fiscal problems in 2018. It expects to report a deficit in its general fund, the only fund that is statutorily required to be balanced. To eliminate the anticipated deficit, the city opts to “sell” its city hall—to itself—for $5 million.

> The following is an excerpt from a note to the financial statements of the city of Dallas (dates changed): The city prepares its annual appropriated general fund, debt service fund, and proprietary operating funds budgets on a basis (budget basis) which

> The following schedule indicates selected accounts from a city’s preclosing 2018 and postclosing 2017 general fund trial balances: All the amounts shown relate only to supplies. All purchases during the year were paid in cash. 1. Assume

> To enhance security in Riverside Park, a city is considering whether it should install a high‐tech security system. The system would not only reduce the cost of police patrols but would also deter crime. The city has received offers from two contractors

> The Allendale School District recently signed a contract with its teachers’ union. The contract provides that all teachers will receive a one‐semester sabbatical leave after seven continuous years of employment. The preamble to the contract provision str

> A city has adopted the following plan for compensated time off: • City employees are entitled to a specified number of days each year for holidays and vacation. The number depends on length of service (20 days for employees with fewer than 5 years of ser

> A city on the coast of Florida has incurred losses (including impairment of assets, clean‐up costs, additional public safety costs, etc.) of $50 million owing to a recent hurricane. This was the third time in as many years in which the city was hit by ma

> A city acquires $1 million of public safety emergency communication equipment by entering into a capital lease. The city divides its first rent payment of $135,868 between lease interest and lease principal as follows: Lease interest……………………………………………. $6

> A state’s department of human resources is responsible for providing certain training courses for various agencies within the state. The department does not actually conduct the training itself. Instead it contracts with outside consultants. The departme

> Per GASB standards if a government gives a cash advance to a grantee and the grantee has not yet satisfied all eligibility requirements, the government would offset its credit to cash with a debit to an asset. By contrast, if the grantee has satisfied al

> A government’s unassigned fund balance in the general fund at year‐end should be indicative of the amount that the government has available for appropriation in future years. Explain and provide an example to support your answer.

> A city’s electric utility transfers $40 million to its general fund. Of this amount, $30 million is a return of the general fund’s initial contribution of “start‐up capital.” The balance is a payment in lieu of property taxes that a private utility opera

> A school district accounts for its pension costs in a governmental fund. In a particular year the district’s actuary recommends that it contribute $18 million for the year. The district, however, had only budgeted $15 million and chooses to contribute on

> Governments are not required to accrue interest on long‐term debt in governmental funds even if the interest is applicable to a current period and will be due the first day of the following year. Explain and justify the standards that permit this practic

> A public school district recently converted its budget from an object to a program format. The district is organized into three instructional divisions: elementary school (kindergarten through grade 6); middle school (grades 7 and 8); and high school (gr

> Many accountants note that for most governments the reported “bottom line” of their financial statements (i.e., revenues less expenditures/expenses and other charges that affect fund balance/net position) will not greatly differ between their fund statem

> A government accounts for inventory on the purchases basis. Why must it offset its year‐end inventory balance with an addition to fund balance?

> A government accounts for inventory on the consumption basis. Why do some accountants believe that it should offset the year‐end inventory balance with a fund balance—nonspendable when no comparable fund balance is required for cash, taxes receivable, or

> A school district grants teachers a sabbatical leave every seven years. Yet, consistent with GAAP, it fails to accrue a liability for such leave over the period in which the leave is earned—not even in its government‐wide statements. How can you justify

> A government permits its employees to accumulate all unused vacation days and sick leave. Whereas (in accord with current standards) it may have to “book” a liability for the unused vacation days, it may not have to record an obligation for the unused si

> Under pressure to balance their budgets, governments at all levels have resorted to fiscal gimmicks, such as delaying the wages and salaries of government employees from the last day of the month to the first day of the following month. In the year of th

> A government expects to pay its electric bill relating to its current fiscal year sometime in the following year. An official of the government requests your advice as to whether the anticipated payment should be charged as an expenditure of the current

> What is the distinction between expenditures and expenses as the terms are used in governmental accounting?

> During 2018 Luling Township engaged in the following transactions related to modernizing the bridge over the Luling River. The township accounts for long‐term construction projects in a capital projects fund. • On July 1 it issued 10‐year, 4 percent bond

> Select the best answer. 1. Which of the following items is least likely to appear on the balance sheet of a capital projects fund? a. Cash b. Investments c. Construction in process d. Reserve for encumbrances 2. The fund balance of a debt service fund

> The Education Agency of one of the nation’s most populous states evaluates public elementary schools on the basis of the following inputs and outcomes: Outcomes • Total campus attendance • Average student scores on standardized tests in math, reading, an

> In what way do the GAO standards impose more rigorous continuing professional education requirements than those of the AICPA?

> Select the best answer. 1. A government opts to set aside $10 million of general‐fund resources to finance a new city hall. Construction is expected to begin in several years, when the city has been able to accumulate additional resources. a. The govern

> A debt service fund reports both routine principal and interest payments as well as an in-substance defeasance. The revenue and expenditure statement that follows is from an annual report of the City of Fort Worth, Texas. It was accompanied by the notes

> A hospital has outstanding $100 million of bonds that mature in 20 years (40 periods). The debt was issued at par and pays interest at a rate of 6 percent (3 percent per period). Prevailing rates on comparable bonds are now 4 percent (2 percent per perio

> Colgate County issued $1 million of 30‐year, 8 percent term bonds to finance improvements to its electric utility plant. The bonds, accounted for in an enterprise fund, were issued at par. After the bonds were outstanding for 10 years, interest rates fel

> A city agrees to extend water and sewer lines to an outlying community. To cover the cost, the affected property owners agree to special assessments of $12 million. The assessments are to be paid over five years, with interest at the rate of 6 percent pe

> Charter City issued $100 million of 6 percent, 20‐year general obligation bonds on January 1, 2017. The bonds were sold to yield 6.2 percent and hence were issued at a discount of $2.27 million (i.e., at a price of $97.73 million). Interest on the bonds

> The accompanying combined statement of revenues, expenditures, and fund balance was drawn from the statements of Plant City, Florida, which, of course, included a general and other funds that are not shown. Suppose, however, that these were the only fund

> As stated in the previous problem, a government issued $8.5 million of special assessment bonds to finance a sewer‐extension project. To service the debt, it assessed property owners $8.5 million. Their obligations are payable over a period of five years

> Upon annexing a recently developed subdivision, a government undertakes to extend sewer lines to the area. The estimated cost is $10.0 million. The project is to be funded with $8.5 million in special assessment bonds and a $1.0 million reimbursement gra

> Vision for Kids, a clinic funded by the Community Health Plan, a not‐for‐profit agency, provides eye examinations, eyeglasses, and eye‐related medical care for children from low‐income families. Children are referred to the clinic by school nurses and te

> The balance sheet and a comparative statement (budget‐to‐actual) of revenues, expenditures, and changes in fund balance of Parkville’s general obligation debt service fund (date changed) is presented

> Durwin County issued $200 million in long‐term debt to fund major improvements to the county’s road and transportation systems. The debt is to be serviced from the proceeds of a specially dedicated property tax. The ac

> Crystal City established a capital projects fund to account for the construction of a new bridge. During the year the fund was established, the city issued bonds, signed (and encumbered) $6 million in contracts with various suppliers and contractors, and

> A city engages in an in‐substance defeasance of long‐term bonds and accordingly invests in, and sets aside, the long‐term securities necessary to make the required interest and principles payments on the debt to be retired. Should, and if so under what c

> A city levies a property tax that is restricted for future period payments of principal and interest on outstanding debt. The tax receipts are recorded in a debt service fund and are invested in interest‐and dividendearning securities. Hence, the amount

> Near the end of its fiscal year a school district issues $80 million of bonds to construct a new high school. By year‐end the district has received the proceeds of the bonds and invested them in short‐term securities. It has not yet incurred any construc

> What is meant by an in-substance defeasance, and how can a government use it to lower its interest costs? How must it recognize a gain or loss on defeasance if it accounts for the debt in a proprietary fund? How do the GASB standards pertaining to in‐sub

> Under what circumstances can a government refund outstanding debt and thereby take advantage of a decline in interest rates?

> What is arbitrage? Why does the Internal Revenue Service place strict limits on the amount of arbitrage that a municipality can earn?

> A government issues bonds at a discount. Where would the government report the discount on its (a) fund statements and (b) government‐wide statements?

> The following are selected measures of service efforts and accomplishments that might be appropriate for a university. For each, indicate whether it is an input, output, or outcome, and state the objective with which it would most likely be associated. I

> How should governments report their capital projects and debt service activities in their governmentwide statements?

> Special assessment debt may be, in economic substance and/or legal form, an obligation of the assessed property owners rather than a government. Should the government, therefore, report it in its statements as if it were its own debt? What are the curren

> At one time governments maintained a unique type of fund to account for special assessments. This fund recorded the construction in process, the long‐term debt, and the assessments receivable. Explain briefly how governments account for special assessmen

> It is sometimes said that in debt service funds the accounting for interest revenue is inconsistent with that for interest expenditure. Explain. What is the rationale for this seeming inconsistency?

> When bonds are issued for capital projects, premiums are generally not accounted for as the mirror image of discounts. Why not?

> Does the government own any “unusual” securities such as derivatives? If so, does the report contain an explanation of these transactions?

> Judging from the disclosures pertaining to investments, does the entity have any investments that appear to be especially risky? In your judgment, to which risk (e.g., credit risk, interest rate risk, foreign currency risk) is the exposure of the entity

> Did the government capitalize collections of art or historical treasures? Did it depreciate such collections?

> Did the government capitalize infrastructure assets acquired during the year? Did it account for infrastructure assets using the “standard” or the “modified” approach?

> How much depreciation did the government charge in its government-wide statements on capital assets used in governmental activities?

> Access the website of the American Red Cross (www.redcross.com) and the American Diabetes Association (www.diabetes.org) and obtain the audited financial statements and Form 990 for the latest fiscal years available. Form 990 can also be obtained from ww

> What is the city’s threshold policy on capitalizing general capital assets and intangible assets?

> What was the total amount of capital assets used in governmental activities added during the year? What was the amount retired?

> What are the principal classes of capital assets associated with governmental activities that the city reports in its financial statements?

> A government holds the following investments. For each, indicate the category in which it should most likely be classified. 1. A 20-year, 4 percent corporate bond rated AA by a leading rating agency. The bond is not widely traded in a market. 2. Shares i

> A city acquired general capital assets as follows: 1. It purchased new construction equipment. List price was $400,000, but the city was granted a 10 percent “government discount.” The city also incurred $12,000 in transportation costs and paid $4,000 to

> Refer to the transactions in the previous exercise. 1. Prepare journal entries that the city would make in its governmental funds (e.g., its general fund or a capital projects fund). 2. How would you recommend that the city maintain accounting control ov

> The following summarizes the history of the Sharp City Recreation Center. 1. In 1990, the city constructed the building at a cost of $1,500,000. Of this amount, $1,000,000 was financed with bonds and the balance from unrestricted city funds. 2. In the 10

> A city engaged in the following transactions during a year: 1. It acquired computer equipment at a cost of $40,000. 2. It completed construction of a new jail, incurring $245,000 in new costs. In the previous year the city had incurred $2.5 million in co

> Select the best answer. 1. A government repaves a section of highway every four years at a cost of $2 million to preserve it at a specific condition level. How much should it report in depreciation charges under the modified approach to accounting for i

> Select the best answer. 1. Which of the following would be least likely to be classified as a city’s general capital assets? a. Roads and bridges b. Electric utility lines c. Computers used by the police department d. Computers used by the department th

> Select the best answer. 1. A key determinant as to whether, under Circular A133, a program is considered major or nonmajor is a. The overall size of the program as measured by total revenues, regardless of source b. The overall size of the program as me

> Northstate University had constructed a theater at a cost of $20 million. It anticipated a useful life of 30 years. After 18 years (with the building 60 percent depreciated), the university dropped its drama program; it no longer had need for a theater.

> Clarkstown State University acquired specialized laboratory equipment with the expectation that it would be used to perform approximately 3,000 tests per year over a 10-year period. The cost was $600,000. After the equipment had been used for only three

> The Middleville School district has discovered mold in one of its schools. The school was constructed 10 years ago at a cost of $30 million. It had an expected useful life of 50 years and hence was 20 percent depreciated. The cost to replace the school t

> Bear County maintains an investment pool for school districts and other governments within its jurisdiction. Participating governments contribute cash to the pool, which is operated like a mutual fund, and receive in return a proportionate share of all d

> A government holds as investments the assets set forth below and determines its fair value as described. For each, indicate the level (1, 2, or 3) within the hierarchy of inputs to valuation techniques in which the investment should be classified and how

> A note from the annual report of a city includes the following: As of September 30, the utility fund had the following investments: Credit risk. As of September 30, the U.S. Treasuries and the U.S. Agency Bonds were rated AAA by Standard & Poorâ

> On August 2, 30 days prior to the end of its August 31 fiscal year, a government issues $3 million of general obligation bonds. The proceeds are being accounted for in a capital projects fund (a governmental fund). To earn a return on the bond proceeds b

> A government held the securities shown in the following table in one of its investment portfolios. All the securities are either stocks or bonds that mature in more than one year. 1. Ignoring dividends and interest, how much gain or loss should the gover

> The City of Allentown recently received a donation of two items: 1. A letter written in 1820 from James Allen, the town’s founder, in which he sets forth his plan for the town’s development. Independent appraisers have valued the letter at $24,000. 2. A

> In 2017 Bantham County incurred $80 million in costs to construct a new highway. Engineers estimate that the useful life of the highway is 20 years. 1. Prepare the entry that the county should make to record annual depreciation (straight-line method) to

> Select the best answer. 1. Government Auditing Standards must be adhered to in all financial audits of a. State and local governments b. Federal agencies c. Federally chartered banks d. All of the above 2. “Generally accepted government auditing standa

> A school district constructs a new elementary school at a cost of $24 million. It finances the project by issuing 30-year general obligation serial bonds, payable evenly over the outstanding term ($800,000 per year). District officials estimate that the