Question: The Financial Statements of Harry and Belinda

The Financial Statements of Harry and Belinda

Johnson Suggest Budgeting Problems Harry has worked at a medium-size interior design firm for five years and earns a salary of $4,080 per month. He also receives $3,000 in interest income once a year from a trust fund set up by his deceased father’s estate. Belinda earns a salary of $6,400 per month, and she has many job-related benefits including flexible benefits program, life insurance, health insurance, a 401(k) retirement program, workplace financial education, and a credit union. The Johnsons live in an old apartment located approximately halfway between their places of employment. However, their rent will increase by $100 a month in July. Harry drives about ten minutes to his job, and Belinda travels about 15 minutes via public transportation to reach her downtown job. Harry and Belinda’s apartment is very nice, but small, and it is furnished primarily with furniture given to them by some of his friends. Soon after getting married, Harry and Belinda decided to begin their financial planning. Fortunately each had taken a college course in personal finance. After initial discussion, they worked together for three evenings to develop the financial statements presented below. Note that the cash flow statement covered the first six months of their marriage.

Required:

(a) Briefly describe how Harry and Belinda probably determined the fair market prices for each of their tangible and investment assets.

(b) Using the data from the cash-flow statement developed by Harry and Belinda, calculate a liquidity ratio, asset-to-debt ratio, debt-to-income ratio, debt payments-to-disposable income ratio, and investment assets-to-total assets ratio. What do these ratios tell you about the Johnsons’ financial situation? Should Harry and Belinda incur more debt, such as credit cards or a new vehicle loan?

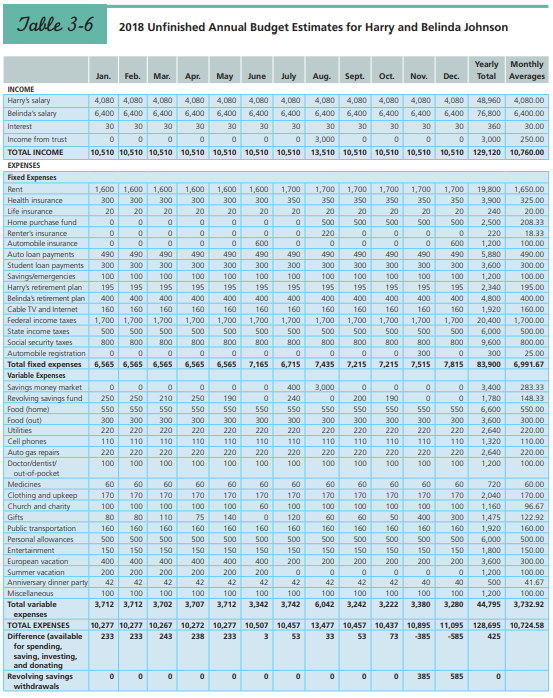

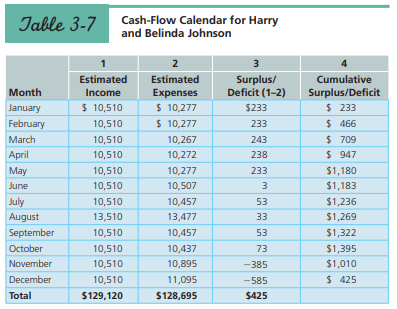

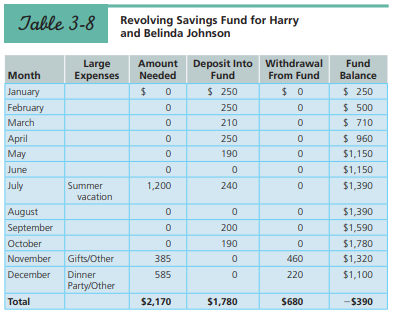

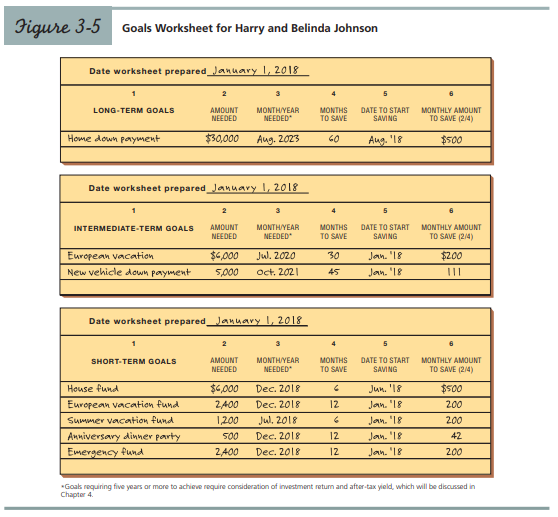

(c) The Johnsons enjoy a high income because both work at well-paying jobs. They have spent parts of three evenings over the past several days discussing their financial values and goals together. As shown in the upper portion of Figure 3-5, they have established three long-term goals: $6,000 for a European vacation to be taken in 2020, $5,000 needed in October 2021 for a down payment on a new automobile, and $30,000 for a down payment on a home to be purchased in December 2023. As shown in the lower portion of the figure, the Johnsons did some calculations to determine how much they had to save for each goal—over the near term—to stay on schedule to reach their long-term goals as well as pay for two vacations and an anniversary party. After developing their balance sheet and cash-flow statement (shown below), the Johnsons made a budget for the year (shown in Table 3-6 on page 97). They then reconciled various conflicting needs and wants until they found that total annual income was close to the total of planned expenses. Next, they created a revolving savings fund (Table 3-8 on page 99) in which they were careful to include enough money each month to meet all of their short-term goals. When developing their cash-flow calendar for the year (Table 3-7 on page 98), they noticed a problem: substantial cash deficits in November and December. Make specific recommendations to the Johnsons on how they could make reductions in their budget estimates. Do not offer suggestions that would alter their new lifestyle drastically, as the couple would reject such ideas.

Table 3-6:

Table 3-7:

Table 3-7:

Figure 3-5:

Transcribed Image Text:

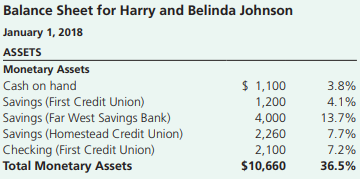

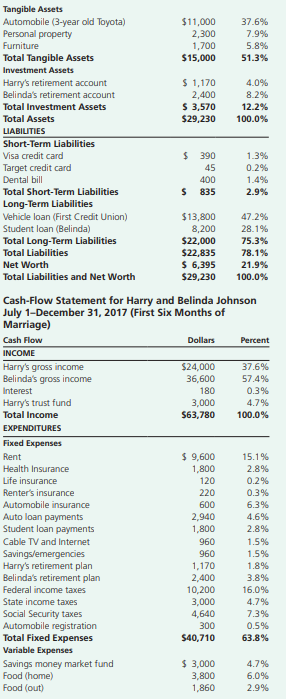

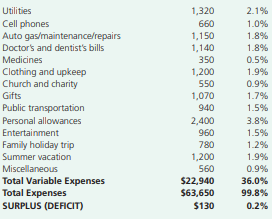

Balance Sheet for Harry and Belinda Johnson January 1, 2018 ASSETS Monetary Assets $ 1,100 1,200 4,000 2,260 2,100 $10,660 Cash on hand 3.8% Savings (First Credit Union) Savings (Far West Savings Bank) Savings (Homestead Credit Union) Checking (First Credit Union) Total Monetary Assets 4.1% 13.7% 7.7% 7.2% 36.5% Tangible Assets Automobile (3-year old Toyota) Personal property $11,000 2,300 1,700 37.6% 7.9% Furniture 5.8% Total Tangible Assets $15,000 51.3% Investment Assets $ 1,170 2,400 S 3,570 $29,230 Harry's retirement account 4.0% Belinda's retirement account 8.2% Total Investment Assets 12.2% Total Assets 100.0% LIABILITIES Short-Term Liabilities Visa credit card $ 390 1.3% Target credit card 45 0.2% Dental bill 400 1.4% $ 835 Total Short-Term Liabilities Long-Term Liabilities Vehicle loan (First Credit Union) Student loan (Belinda) 2.9% $13,800 8,200 $22,000 $22,835 $ 6,395 $29,230 47.2% 28.1% Total Long-Term Liabilities 75.3% Total Liabilities 78.1% 21.9% Net Worth Total Liabilities and Net Worth 100.0% Cash-Flow Statement for Harry and Belinda Johnson July 1-December 31, 2017 (First Six Months of Marriage) Cash Flow Dollars Percent INCOME Harry's gross income Belinda's gross income Interest Harry's trust fund $24,000 36,600 180 3,000 S63,780 37.6% 57.4% 0.3% 4.7% Total Income 100.0% EXPENDITURES Fixed Expenses Rent $ 9,600 1,800 15.1% Health Insurance 2.8% Life insurance 120 0.2% 220 Renter's insurance Automobile insurance Auto loan payments Student loan payments 0.3% 600 6.3% 2,940 1,800 4.6% 2.8% 1.5% 1.5% 1.8% 3.8% 16.0% 4.7% Cable TV and Internet 960 Savings/emergencies Harry's retirement plan Belinda's retirement plan 960 1,170 2,400 10,200 3,000 4,640 Federal income taxes State income taxes Social Security taxes Automobile registration Total Fixed Expenses Variable Expenses 7.3% 300 0.5% $40,710 63.8% Savings money market fund Food (home) Food (out) $ 3,000 3,800 4.7% 6.0% 1,860 2.9% Utilities 1,320 2.1% Cell phones Auto gas/maintenance/repairs Doctor's and dentist's bills 660 1,150 1,140 1.0% 1.8% 1.8% Medicines 350 0.5% 1,200 Clothing and upkeep Church and charity 1.9% 550 1,070 0.9% Gifts 1.7% Public transportation 940 1.5% Personal allowances 2,400 3.8% Entertainment 960 1.5% 780 Family holiday trip Summer vacation 1.2% 1,200 1.9% 0.9% 36.0% Miscellaneous 560 Total Variable Expenses Total Expenses $22,940 $63,650 99.8% SURPLUS (DEFICIT) $130 0.2% Table 3-6 2018 Unfinished Annual Budget Estimates for Harry and Belinda Johnson Yearly Monthly Jan. Feb. Mar. Аpг. May June July Aug. Sept. Oct. Nov. Dec. Total Averages INCOME Harry's salary 4,080 4,080 4,080 4,080 4,080 4,080 4,080 4,080 4,080 4,080 4,080 4,080 48,960 4,080.00 Belinda's salary 6,400 6,400 6,400 6,400 6,400 6,400 6,400 6,400 6,400 6,400 6,400 6,400 76,800 6,400.00 Interest 30 30 30 30 30 30 30 30 30 30 30 30 360 30.00 Income from trust 3,000 3,000 250.00 TOTAL INCOME 10,510 10,510 10,510 10,510 10,510 10,510 10,510 13,510 10,510 10,510 10,510 10,510 129,120 10,760.00 EXPENSES Fixed Expenses Rent 1,600 1,600 1,600 1,600 1,600 300 1,600 1,700 1,700 1,700 350 1,700 350 1,700 1,700 19,800 1,650.00 Health insurance 300 300 300 300 300 350 350 350 350 3,900 325.00 Life insurance 20 20 20 20 20 20 20 20 20 20 20 20 240 20.00 Home purchase fund Renter's insurance Automobile insurance 500 500 500 500 500 2,500 208.33 220 220 18.33 600 600 1,200 100.00 Auto loan payments Student loan payments Savingslemergencies Harry's retirement plan 490 490 490 490 490 490 490 490 490 490 490 490 5,880 490.00 300 300 300 300 300 300 300 300 300 300 300 300 3,600 300.00 100 100 100 100 100 100 100 100 100 100 100 100 1,200 100.00 195 195 195 195 195 195 195 195 195 195 195 195 2,340 195.00 Belinda's retirement plan 400 400 400 400 400 400 400 400 400 400 400 400 4,800 400.00 Cable TV and Internet 160 160 160 160 160 160 160 160 160 160 160 160 1,920 160.00 Federal income taxes 1,700 1,700 1,700 1,700 1,700 1,700 1,700 1,700 1,700 1,700 1,700 1,700 20,400 1,700.00 State income taxes 500 500 500 500 500 500 500 500 500 500 500 500 6,000 500.00 Social security taxes 800 800 800 800 800 800 800 800 800 800 800 800 9,600 800.00 Automobile registration Total fixed expenses Variable Expenses 300 300 25.00 6,565 6,565 6,565 6,565 6,565 7,165 6,715 7,435 7,215 7,215 7,515 7,815 83,900 6,991.67 Savings money market Revolving savings fund Food (home) 400 3,000 3,400 283.33 250 250 210 250 190 240 200 190 1,780 148.33 S50 SS0 S50 S50 S50 S50 S50 S50 S50 S50 550 S50 6,600 550.00 Food (out) 300 300 300 300 300 300 300 300 300 300 300 300 3,600 2,640 300.00 Utilities 220 220 220 220 220 220 220 220 220 220 220 220 220.00 Cell phones Auto gas repairs 110 110 110 110 110 110 110 110 110 110 110 110 1,320 110.00 220 220 220 220 220 220 220 220 220 220 220 220 2,640 220.00 Doctor/dentis 100 100 100 100 100 100 100 100 100 100 100 100 1,200 100.00 out-of-pocket Medicines 60 60 60 60 60 60 60 60 60 60 60 60 720 60.00 Clothing and upkeep Church and charity 170 170 170 170 170 170 170 170 170 170 170 170 2,040 170.00 100 100 100 100 100 60 100 100 100 100 100 100 1,160 96.67 Gifts 80 80 110 75 140 120 60 60 400 300 1,475 122.92 Public transportation 160 160 1,920 6,000 1,800 160 160 160 160 160 160 160 160 160 160 160.00 Personal allowances 500 500 500 500 500 500 500 S00 S00 500 S00 500 500.00 Entertainment 150 150 150 150 150 150 150 150 150 150 150 150 150.00 European vacation 400 400 400 400 400 400 200 200 200 200 200 200 3,600 1,200 300.00 100.00 Summer vacation 200 200 200 200 200 200 Anniversary dinner party 42 42 42 42 42 42 42 42 42 42 40 40 S00 41.67 Miscellaneous 100 100 100 100 100 100 100 100 100 100 100 100 1,200 100.00 Total variable 3,712 3,712 3,702 3,707 3,712 3,342 3,742 6,042 3,242 3,222 3,380 3,280 44,795 3,732.92 expenses TOTAL EXPENSES 10,277 10,277 10,267 10,272 10,277 10,507 10,457 13,477 10,457 10,437 10,895 11,095 128,695 10,724.58 Difference (available 233 233 243 238 233 53 33 53 73 -385 -585 425 for spending. saving, investing. and donating Revolving savings withdrawals 385 585 Jable 3-7 Cash-Flow Calendar for Harry and Belinda Johnson 2 3 Estimated Estimated Surplus/ Deficit (1-2) Cumulative Surplus/Deficit $ 233 Month Еxpenses $ 10,277 $ 10,277 Income January $ 10,510 $233 February 10,510 233 $ 466 March 10,510 10,267 243 $ 709 April 10,510 10,272 238 $ 947 May 10,510 10,277 233 $1,180 June 10,510 10,507 3 $1,183 July 10,510 10,457 53 $1,236 August 13,510 13,477 33 $1,269 September 10,510 10,457 53 $1,322 October 10,510 10,437 73 $1,395 November 10,510 10,895 -385 $1,010 December 10,510 11,095 -585 $ 425 Total $129,120 $128,695 $425 Table 3-8 Revolving Savings Fund for Harry and Belinda Johnson Large Expenses Amount Deposit Into Withdrawal Fund Fund Balance Month Needed From Fund January $ 250 $ 0 $ 250 $ 500 $ 710 $ 960 February 250 March 210 April 250 May 190 $1,150 June $1,150 July Summer 1,200 240 $1,390 vacation August $1,390 September 200 $1,590 October 190 $1,780 November Gifts/Other 385 460 $1,320 December Dinner 585 220 $1,100 Party/Other Total $2,170 $1,780 $680 -$390 Figure 3-5 Goals Worksheet for Harry and Belinda Johnson Date worksheet prepared January 1, 2018 2 LONG-TERM GOALS AMOUNT NEEDED MONTH/YEAR NEEDED MONTHS TO SAVE DATE TO START SAVING MONTHLY AMOUNT TO SAVE (2/4) Home down payment $30,000 Aug. 2023 60 Aug. '18 $500 Date worksheet prepared January 1, 2018 2 AMOUNT MONTH/YEAR NEEDED INTERMEDIATE-TERM GOALS MONTHS DATE TO START MONTHLY AMOUNT NEEDED TO SAVE SAVING TO SAVE (2/4) European vacation $6,000 Jul. 2020 30 Jan. '18 $200 New vehicle down payment 5,000 Oct. 2021 45 Jan. '18 Date worksheet prepared January I, 2018 2 5 AMOUNT NEEDED MONTH/YEAR NEEDED MONTHS DATE TO START SAVING SHORT-TERM GOALS MONTHLY AMOUNT TO SAVE TO SAVE (2/4) House fund $6.000 Dec. 2018 Jun. '18 $S00 European vacation fund 2400 Dec. 2018 12 Jan. '18 200 Summer vacation fund Anniversary dinner party Emergency fund 1,200 Jul. 2018 Jan. '18 200 Dec. 2018 Jan. '18 Jan. '18 S00 12 42 2400 Dec. 2018 12 200 Goaks requiring five years or more to achieve require consideration of investment return and after-tax yield, which will be discussed in Chapter 4.

> City Segway Tours of Washington DC, LLC (CST) operated tours where customers used Segway personal transportation vehicle to tour the city. Norman Mero and his significant other signed up for such a tour. The contract they signed prior to beginning the to

> FFP Operating Partners, L.P. (FFP Operating), operates a number of convenience stores and gas stations. FFP Operating executed 31 promissory notes in favor of Franchise Mortgage Acceptance Company (FMAC). In connection with the notes, FFP Marketing Compa

> Murray Walter, Inc. (Walter, Inc.), was a general contractor for the construction of a waste treatment plant in New Hampshire. Walter, Inc., contracted with H. Johnson Electric, Inc. (Johnson Electric), to install the electrical system in the treatment p

> Holly Hill Acres, Ltd. (Holly Hill), purchased land from Rogers and Blythe. As part of its consideration, Holly Hill gave Rogers and Blythe a promissory note and mortgage. The note read, in part, “This note with interest is secured by a mortgage on real

> Mr. Higgins operated a used car dealership in the state of Alabama. Higgins purchased a Chevrolet Corvette. He paid for the car with a draft on his account at the First State Bank of Albertville. Soon after, Higgins resold the car to Mr. Holsonback. To p

> Martha M. Carr suffered from schizophrenia and depression. Schizophrenia is a psychotic disorder that is characterized by disturbances in perception, inferential thinking, delusions, hallucinations, and grossly disorganized behavior. Depression is charac

> William H. Bailey, MD, executed a note payable to California Dreamstreet, a joint venture that solicited investments for a cattle breeding operation. Bailey’s promissory note read, “Dr. William H. Bailey hereby promises to pay to the order of California

> Joseph Mitsch purchased a used Chevrolet Yukon SUV vehicle from Rockenbach Chevrolet. The Yukon was manufactured by General Motors Corporation (GMC) and had been driven over 36,000 miles. The purchase contract with Rockenbach Chevrolet contained the foll

> W. Hayes Daughtrey consulted Sidney Ashe, a jeweler, about the purchase of a diamond bracelet as a Christmas present for his wife. Ashe showed Daughtrey a diamond bracelet that he had for sale for $15,000. When Daughtrey decided to purchase the bracelet,

> Kent Nowlin Construction, Inc. (Nowlin), was awarded a contract by the state of New Mexico to pave a number of roads. After Nowlin was awarded the contract, it entered into an agreement with Concrete Sales & Equipment Rental Company, Inc. (C&E). C&E was

> Dr. and Mrs. Sedmak (Sedmaks) were collectors of Chevrolet Corvettes. The Sedmaks saw an article in Vette Vues magazine concerning a new limited-edition Corvette. The limited edition was designed to commemorate the selection of the Corvette as the offici

> Connie R. Grady purchased a new Chevrolet Chevette from Al Thompson Chevrolet (Thompson). Grady gave Thompson a down payment on the car and financed the remainder of the purchase price through General Motors Acceptance Corporation (GMAC). Grady picked up

> The Jacob Hartz Seed Company, Inc. (Hartz), bought soybeans for use as seed from E. R. Coleman. Coleman certified that the seed had an 80 percent germination rate. Hartz paid for the beans and picked them up from a warehouse in Card, Arkansas. After the

> All America Export-Import Corp. (All America) placed an order for several thousand pounds of yarn with A. M. Knitwear (Knitwear). On June 4, All America sent Knitwear a purchase order. The purchase order stated the terms of the sale, including language t

> Fuqua Homes, Inc. (Fuqua), is a manufacturer of prefabricated houses. MMM, a dealer of prefabricated homes, was a partnership created by two men named Kirk and Underhill. On seven occasions before the disputed transactions occurred MMM had ordered homes

> Big Knob Volunteer Fire Company (Fire Co.) agreed to purchase a fire truck from Hamerly Custom Productions (Hamerly), which was in the business of assembling various component parts into fire trucks. Fire Co. paid Hamerly $10,000 toward the price two day

> Lindsey Stroupes was 16 years old and a sophomore in high school. Anthony Bradley, the manager of a Finish Line, Inc.’s store in a mall, offered Lindsey a position as a sales associate that she accepted. Lindsey signed an employment contract that require

> Numismatic Funding Corporation (Numismatic), with its principal place of business in New York, sells rare and collector coins by mail throughout the United States. Frederick R. Prewitt, a resident of St. Louis, Missouri, responded to Numismatic’s adverti

> Frances Hector entered CedarsSinai Medical Center (Cedars-Sinai), Los Angeles, California, for a surgical operation on her heart. During the operation, a pacemaker was installed in Hector. The pacemaker, which was manufactured by American Technology, Inc

> Alvin Cagle was a potato farmer in Alabama who had had several business dealings with the H. C. Schmieding Produce Co. (Schmieding). Several months before harvest, Cagle entered into an oral sales contract with Schmieding. The contract called for Schmied

> Dan Miller was a commercial photographer who had taken a series of photographs that appeared in The New York Times. Newsweek magazine wanted to use the photographs. When a Newsweek employee named Dwyer phoned Miller, Dwyer was told that 72 images were av

> Mr. Gulash lived in Shelton, Connecticut. He wanted an above-ground swimming pool installed in his backyard. Gulash contacted Stylarama, Inc. (Stylarama), a company specializing in the sale and construction of pools. The two parties entered into a contra

> David Abacus uses the internet to place an order to license software for his computer from Inet.License, Inc. (Inet) through Inet’s electronic website ordering system. Inet’s web page order form asks David to type in his name, mailing address, telephone

> Little Steel Company is a small steel fabricator that makes steel parts for various metal machine shop clients. When Little Steel Company receives an order from a client, it must locate and purchase 10 tons of a certain grade of steel to complete the ord

> Someone secretly took video cameras into the locker room and showers of the Illinois State University football team. Video recordings showing these undressed players were displayed at the website http://univ.youngstuds.com, operated by Franco Productions

> Ernest & Julio Gallo Winery (Gallo) is a famous maker of wines located in California. The company registered the trademark “Ernest & Julio Gallo” in 1964 with the U.S. Patent and Trademark Office. The company has spent more than $500 million promoting it

> Ptarmigan Investment Company (Ptarmigan), a partnership, entered into a contract with Gundersons, Inc. (Gundersons), a South Dakota corporation in the business of golf course construction. The contract provided that Gundersons would construct a golf cour

> Andrew Parente had a criminal record. He and Mario Pirozzoli Jr., formed a partnership to open and operate the Speak Easy Café in Berlin, Connecticut, which was a bar that would serve alcohol. The owners were required to obtain a liquor license from the

> Hawaiian Telephone Company entered into a contract with Microform Data Systems, Inc. (Microform), for Microform to provide a computerized assistance system that would handle 15,000 calls per hour with a one-second response time and with a “nonstop” featu

> California and Hawaiian Sugar Company (C&H), a California corporation, is an agricultural cooperative owned by 14 sugar plantations in Hawaii. It transports raw sugar to its refinery in Crockett, California. Sugar is a seasonal crop, with about 70 percen

> The Trump World Tower is a 72-story luxury condominium building constructed at 845 United Nations Plaza in Manhattan, New York. Before the building was constructed, 845 UN Limited Partnership (845 UN) began selling condominiums at the building. The condo

> Shumann Investments, Inc. (Shumann) hired Pace Construction Corporation (Pace), a general contractor, to build Outlet World of Pasco Country. In turn, Pace hired OBS Company, Inc. (OBS), a subcontractor, to perform the framing, drywall, insulation, and s

> C.W. Milford owned a registered quarter horse named Hired Chico. Milford sold the horse to Norman Stewart. Recognizing that Hired Chico was a good stud, Milford included the following provision in the written contract that was signed by both parties: “I,

> William John Cunningham, a professional basketball player, entered into a contract with Southern Sports Corporation, which owned the Carolina Cougars, a professional basketball team. The contract provided that Cunningham was to play basketball for the Co

> Eugene H. Emmick hired L. S. Hamm, an attorney, to draft his will. The will named Robert Lucas and others (Lucas) as beneficiaries. When Emmick died, it was discovered that the will was improperly drafted, violated state law, and was therefore ineffectiv

> The Phillies, L.P., the owner of the Philadelphia Phillies professional baseball team (Phillies), decided to build a new baseball stadium called Citizens Bank Park (the Project). The Phillies entered into a contract (Agreement) with Driscoll/Hunt Joint V

> Irving Levin and Harold Lipton owned the San Diego Clippers Basketball Club, a professional basketball franchise. Levin and Lipton met with Philip Knight to discuss the sale of the Clippers to Knight. After the meeting, they all initialed a 3-page handwr

> David Brown met with Stan Steele, a loan officer with the Bank of Idaho (now First Interstate Bank), to discuss borrowing money from the bank to start a new business. After learning that he did not qualify for the loan on the basis of his own financial s

> Harun Fountain, a minor, was shot in the back of the head at point-blank range by a playmate. Fountain required extensive lifesaving medical services from a variety of medical service providers, including Yale Diagnostic Radiology. The expense of the ser

> Define the cash-flow statement and explain what it does.

> Define the balance sheet and give two examples of how to increase one’s net worth.

> Give some examples of legal employment rights.

> How does one put a market value on an employee benefit?

> Is college worth the cost? Why or why not?

> Give an example of how inflation affects income and consumption.

> Describe two statistics that help predict the future direction of the economy

> Summarize the phases of the business cycle.

> What is identity theft?

> Distinguish between the APR (annual percentage rate) and the finance charge on a debt.

> Summarize how financial goals follow from one’s values.

> What is the biggest financial worry of most individuals, and what can they do about it?

> Summarize the content in Figure 3-1, the overview of effective personal financial planning. Figure 3-1: Figure 3-1 Overview of Effective Financial Planning Economic Data Living Еxpenses Advertising Standards of Comparison Earnings Values MANAGERIAL

> What are the building blocks to achieving financial success?

> Summarize what you will accomplish studying personal finance.

> Distinguish among financial success, financial security, and financial happiness

> Explain the five fundamental steps in the financial planning process.

> Summarize your insurance protections when you have funds on deposit in a depository institution as opposed to other financial services providers.

> Give three examples of depository institutions where one could open a checking account.

> Explain the circumstances when it would be appropriate to have funds in a checking account.

> After completing his associate of arts degree four months ago from a community college in Oklahoma City, Oklahoma, Juan Ramirez has answered more than three dozen advertisements and interviewed three times in his effort to get a sales job, but he has had

> Identify the primary goals of monetary asset management.

> Explain why some taxpayers have an effective marginal tax rate as high as 40 percent.

> What is a marginal tax bracket, and how does it impact taxpayers making tax advantaged contributions to their retirement plans?

> Distinguish between a progressive and a regressive tax.

> Is the gig economy, freelancing, or entrepreneurship for you? Why or why not?

> What can be done to enhance your abilities, experiences and education without working in a job situation?

> How do your values and interests impact your life-style trade-offs in career planning?

> What is career planning and why is it important?

> Now that you have read this chapter on building and maintaining good credit, what would you recommend to Julia Grace regarding: 1. How might Julia go about establishing a debt limit? 2. What two or three things can she do help keep her student debt under

> Now that you have read the chapter on the importance of career planning, what do you recommend to Nicole Linkletter in the case at the beginning of the chapter regarding: 1. Clarifying her values and lifestyle trade-offs in career planning? 2. Enhancing

> Victor is somewhat satisfied with his sales career and has always wondered about a career as a teacher in a public school. He would have to take a year off work to go back to college to obtain his teaching certificate, and that would mean giving up his $

> Now that you have read the chapter on managing checking and savings accounts, what would you recommend to Nathan Rosenberg and Avigai Abramovitz in the case at the beginning of the chapter regarding: 1. Where they can obtain the monetary asset managemen

> Now that you have read the chapter on managing income taxes, what advice can you offer Ace and Florence in the case at the beginning of the chapter regarding: 1. Using tax credits to help pay for Ace’s college expenses? 2. Determining how much money Flor

> Now that you have read the chapter on financial planning, what do you recommend to Austin Patterson for his talk with Emily on the subject of financial planning regarding: 1. Setting financial goals? 2. Determining what they own and owe? 3. Using the inf

> Now that you have read the chapter on the importance of personal finance, what do you recommend to Jing Wáng in the case at the beginning of the chapter regarding: Participating in her employer’s 401(k) retirement plan? Understanding the effects of her

> Is it too easy for college students to get credit cards? Who do you know who has gotten into financial difficulty because of overuse of credit cards, and what happened?

> Use the information on pages 185, 186 and 187 to discuss how best to deal with student loan debt Page No. 185, 186,187: CHAPTER 6 Building and Maintaining Good Credit 185 6.2a Method 1: Continuous-Debt Method A useful approach for determining your d

> How might students judge whether they are taking on too high a level of student loan debt?

> What aspects of your financial life make you creditworthy? What aspects might make it difficult for you to obtain credit?

> Have you ever had a disagreement with a friend or family member over a money issue? How might you communicate differently now?

> Lost/Stolen Debit Cards. What should you do if your ATM or debit card is lost or stolen? Why?

> Harry has started out fine in his career as his responsibilities have increased since he began working there about five years ago. Belinda recently attended a conference for those in her stock brokerage field and by chance she dropped in at the “career s

> When might it be appropriate for you to save via a certificate of deposit versus a money market account?

> Many people desire protection from the possibility of overdrawing their checking account. Banks make it easy by allowing you to opt into overdraft protection. Explain how this and other overdraft protections work and why the true cost of opting in may ex

> When would you recommend using an individual account, a joint tenancy with right of survivorship account, and a tenancy by the entirety account for your monetary assets?

> You know someone who recently had $90 in overdraft fees for two small debit card transactions. Explain to him why such high fees resulted from such small transactions and the relative benefits of having an automatic funds transfer agreement versus an aut

> List two examples of checking account transactions that result in assessment of fees that are avoidable?

> Identify three strategies to reduce income tax liability that you may take advantage of in the future.

> Name three tax credits that a college student might take advantage of while still in school or during the first few years after graduation.

> Some college students earn money that is paid to them in cash and then do not include this as income when they file their tax returns. What are the pros and cons of this practice?

> Many college students choose not to file a federal income tax return, assuming that the income taxes withheld by employers “probably” will cover their tax liability. Is such an assumption correct? What are the negatives of this practice if the employers

> What can a person try to do to genuinely control spending to better achieve financial success?

> You have been asked to give a brief speech on how to achieve financial success and financial security. Use the five steps in the financial planning process and the building blocks to achieving financial success in your speech. Outline your speech.

> Do you have a budget or spending plan? Why or why not? What do you think are the two major reasons why people do not make formal written budgets?

> Of the financial ratios described in this chapter, which two might be most revealing for the typical college student?

> College students often have little income and many expenses. Does this reduce or increase the importance of completing a cash-flow statement on a monthly basis? Why or why not?

> What are two of your most important personal values? Give an example of how each of those values might influence your financial plans.

> What is the biggest budget-related mistake that you have made? What would you do differently now?

> During slow economic times, the federal government’s budgeting priority often is to borrow so it can spend more money than it takes in. What happens to families that try that, and why?

> People regularly make decisions in career planning that have trade-offs. Identify some benefits and costs people are faced with as well as two lifestyle trade-offs.