Question: The following footnote was disclosed at the

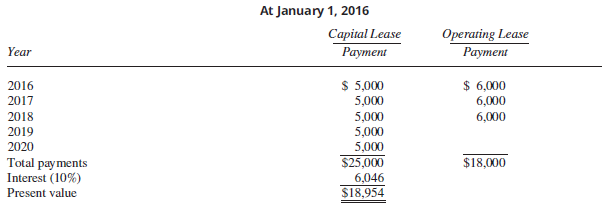

The following footnote was disclosed at the beginning of 2016 (January 1, 2016).

The capital lease began on January 1, 2015 when the fair value of the capital lease was $21,776 (with a six-year life). The operating lease began on January 1, 2016 when the fair value of the operating lease at the inception of the lease was $14,921 (with a three-year lease term). Straight line depreciation is used for all assets. Each lease requires equal annual payments to be made at year-end.

Required:

1. Under existing U.S. GAAP, what is the amount of lease liability recorded on the balance sheet at January 1, 2016?

2. If the proposed changes in accounting for leases become authoritative, what would be the amount of lease liability recorded on the balance sheet at January 1, 2016?

3. Which approach (part 1 or part 2) do you think provides more relevant information to the users of the financial statements? Why?

Transcribed Image Text:

At January 1, 2016 Capital Lease Раутen Operating Lease Раyтent Year $ 5,000 5,000 5,000 5,000 2016 $ 6,000 2017 6,000 2018 6,000 2019 2020 5,000 $25,000 $18,000 Total pay ments Interest (10%) Present value 6,046 $18,954

> In what order must partnership assets be distributed?

> Discuss the three basic assumptions necessary for calculating a safe cash distribution. How is this safe cash distribution computed?

> Following is the preclosing trial balance for the General Fund of the City of Doyle. Note 1: Includes $50,000 of encumbrances from 2015. Required: Prepare in general journal form the closing entries for the General Fund of Doyle City. Doyle City T

> Why are realization gains or losses allocated to partners in their profit and loss ratios?

> Blood River Productions enters into a sale agreement for its recent film. A sale occurs when the entity transfers control of the master copy of a film and all the associated rights that go along with it (that is, an entity sells and gives up all rights t

> Discuss the methods used to record changes in partnership membership.

> What is meant by dissolution and what are its causes?

> List some of the alternative methods of calculating a bonus that may appear in a partnership agreement.

> Explain why a partnership is viewed in accounting as a “separate economic entity.”

> Distinguish between a partner’s interest in capital and his interest in the partnership’s income and losses. Also, make a general distinction between a partner’s capital account and his drawing account.

> How might a partner withdrawing in violation of the partnership agreement and without the consent of the other partners be treated? What about a partner who is forced to withdraw?

> Under what two conditions will the bonus and goodwill methods of recording the admission of a partner yield the same result?

> Describe the methods that might be used to disclose reportable segment information.

> Listed are transactions of the Town of Jackson. 1. A budget consisting of estimated revenues of $1,950,000 and appropriations for expenditures of $1,800,000 was passed by the town council. 2. Property taxes of $1,150,000 were assessed; $1,115,000 are exp

> List the types of information that must be presented for each reportable segment of a company under the rules of SFAS No. 131 [ASC 280].

> What segmental disclosures are required, if any, for interim reports?

> Suppose a not-for-profit entity purchases short-term highly liquid investments using resources that have donor-imposed restrictions that restrict their use to long-term investment purposes. In preparing the statement of cash flows, can these highly liqui

> List the three major types of enterprise wide information disclosures required by SFAS No. 131 [ASC 280], and explain how the firm’s designation of reportable segments affects these disclosures.

> Describe the guidelines to be used in determining (a) what constitutes an operating segment, and (b) whether a specific operating segment is a significant segment.

> Define the following: (a). Operating segment. (b). Reportable segment.

> Why do financial statement users (financial analysts, for example) need information about segments of a firm?

> What are the minimum disclosure requirements established ASC 270 for interim financial reports?

> Describe how changes in estimates should be treated in interim financial statements.

> Describe the basic procedure for computing income tax provisions for interim financial statements.

> Go online and find the City of Atlanta’s Comprehensive Annual Financial Report for the year ended June 30, 2013. Find the footnotes related to defined pensions and other post-employment benefits (OPEB). Required: 1. Determine the amount of unfunded pens

> When must a firm present segmental disclosures for major customers? What is the reason for this requirement?

> How are foreign operations defined under SFAS No. 131 [ASC 280]?

> What types of information must be disclosed about foreign operations under SFAS No. 131 [ASC 280–10–50–40]?

> Does the Codification apply to both governmental and nongovernmental entities?

> For what types of companies would segmented financial reports have the most significance? Why?

> Under the current rate method, describe how the various balance sheet accounts are translated (including the equity accounts) and how this translation affects the computation of various ratios (such as debt to equity or the current ratio). In particular,

> What is meant by an entity’s functional currency and what are the economic indicators identified by the FASB to provide guidance in selecting the functional currency?

> Explain the effects on income from hedging a foreign currency exposed net asset position or net liability position.

> Describe a forward exchange contract.

> Explain what is meant by the “two-transaction method” in recording exporting or importing transactions. What support is given for this method?

> Listed are typical financial activities of a local governmental unit. 1. The legislative unit approved the budget for the general operating fund. Estimated revenues are $4,000,000, and appropriations for expenditures are $3,800,000. 2. Statements of prop

> List some of the criteria laid out by the FASB that are required for a gain or loss on forecasted transactions (a cash flow hedge) to be excluded from the income statement. If these criteria are satisfied, where are the gains or losses reported, and when

> Differentiate between forward-based derivatives and option based derivatives.

> Define a derivative instrument, and describe the keystones identified by the FASB for the accounting for such instruments.

> What is a put option, and how might it be used to hedge a forecasted transaction?

> In a limited partnership with multiple general partners, the determination of which, if any, general partner within the group controls and consolidates the limited partnership is based on an analysis of the relevant facts and circumstances. List the righ

> Name the three stages of concern to the accountant in accounting for import–export transactions. Briefly explain the accounting for each stage.

> The FASB classifies forward contracts as those acquired for the purpose of hedging and those acquired for the purpose of speculation. What main differences are there in accounting for these two classifications?

> Define currency exchange rates and distinguish between “direct” and “indirect” quotations.

> List some of the major differences in accounting between IFRS and U.S. GAAP.

> How does the FASB view its role in the development of an international accounting system? Currently, two members of the IASB were previously affiliated with the FASB. Comment on what effect this might have on the likelihood that the U.S. standard-setters

> For each of the items listed below, determine how the amount would be classified in Fund Balance (either nonspendable, restricted, committed, assigned, or unassigned fund balance). 1. Inventory costing $17,000 was purchased to be used for highway repair

> Describe the attitude of the FASB toward the IASB (International Accounting Standards Board).

> Discuss the types of ADRs that non-U.S. companies might use to access the U.S. markets.

> On December 1, 2014, King Company exported equipment that had cost $210,000 to a Brazilian company for 1,000,000 real. The account is to be settled on January 31, 2015. King Company is a calendar-year company and uses a perpetual inventory system. Direct

> The first two lines of Unilever Group’s 2013 consolidated income statement (using IFRS) report the following amounts (in millions of euros): Required: A. On the income statement, the first two lines in Unilever’s inc

> Is a debt restructuring always classified as a troubled debt restructuring if the entity is experiencing some financial difficulties? Explain.

> British Petroleum’s income statement was prepared using IFRS is presented below (in $ millions). ExxonMobil Corporation’s income statement prepared using U.S. GAAP is presented below (in $ millions). Required: A.

> Three funds of the Leukemia Foundation, a nonprofit welfare organization, began an investment pool on January 1, 2016. The costs and fair market values on this date were as follows: During 2016 the investment pool reinvested $20,000 in realized gains a

> The December 31, 2015, statement of financial position for the Blood Donors of America Foundation is presented below. Statement of Financial Position December 31, 2015 Assets Cash ………â

> Preston Library, a nonprofit organization, presented the following statement of financial position and statement of activities for its fiscal year ended February 28, 2014. The following transactions occurred during the fiscal year ended February 28,

> Several independent financial activities of a governmental unit are given below. 1. Revenue from the sale of licenses and permits for the first two months totaled $15,000. 2. Land that had been donated previously was sold for $100,000. 3. An order was pl

> The following transactions of Beltville College transpired during 2015. The funds necessary are the Endowment Fund, the Annuity Fund, the Plant Fund—Unexpended, the Plant Fund Investment in Plant, the Loan Fund, the Unrestricted Current

> A partial statement of financial position of Century University is shown below. Century University Partial Statement of Financial Position June 30, 2014 Assets Current Funds Unrestricted Cash ……â€&brvba

> On January 1, 2015, a new Board of Directors was elected for Bradley Hospital. The new board switched to a different accountant. After reviewing the hospital’s books, the accountant decided that the accounts should be adjusted. Effectiv

> The following events were recorded on the books of Mercy Hospital for the year ended December 31, 2015. 1. Revenue from patient services totaled $16,000,000. The allowance for uncollectibles was established at $3,400,000. Of the $16,000,000 revenue, $6,0

> The Village of Oakridge, which was incorporated recently, began financial operations on July 1, 2015, the beginning of its fiscal year. The following transactions occurred during this first fiscal year, July 1, 2015, to June 30, 2016. 1. The Village Coun

> You have been engaged to examine the financial statements of the Town of Bridgeport for the year ended June 30, 2015. Your examination disclosed that, because of the inexperience of the town’s bookkeeper, all transactions were recorded

> Where in the Codification are the conditions listed that allow an entity that sells a product to recognize revenue on an accrual basis?

> The following transactions take place. 1. Bond proceeds of $1,000,000 were received to be used in constructing a firehouse. An equal amount is contributed from general revenues. 2. $800,000 of serial bonds matured. Interest of $120,000 was paid on these

> The following activities and transactions are typical of those that may affect the various funds used by a typical municipal government. Required: Prepare journal entries to record each transaction and identify the fund in which each entry is recorded.

> An administrative section of the County Assessor’s Office of Mecklenburg County serves as the billing and collection agency for all property taxes assessed in Mecklenburg County. A charge of 1% of taxes and penalties collected is apport

> Q, R, S, and T are partners, sharing profits and losses 40%:20%:20%:20%, respectively. After sale of firm assets and payment of the available cash to the partnership creditors, a partnership trial balance and the personal status of each partner are as fo

> Beth, Steph, and Linda have been operating a small gift shop for several years. After an extensive review of their past operating performance, the partners concluded that the business needed to expand in order to provide an adequate return to the partner

> Bill and Jane share profits and losses in a 70:30 ratio. Mike is to be admitted into a partnership upon the investment of $14,000 for a one-third capital interest. Account balances for Bill and Jane on June 30, 2014 just before the admission of Mike are

> Phil Phoenix and Tim Tucson are partners in an electrical repair business. Their respective capital balances are $90,000 and $50,000, and they share profits and losses equally. Because the partners are confronted with personal financial problems, they de

> Hill, Jones, and Vose have been partners throughout 2014. Their average balances for the year and their balances at the end of the year before closing the nominal accounts are as follows: The income for 2014 is $108,000 before charging partnersâ&

> On January 1, 2014, Tony and Jon formed T&J Personal Financial Planning with capital investments of $480,000 and $340,000, respectively. The partners wanted to draft a profit and loss agreement that would reward each individual for the resources invested

> Mary and Nancy invested $80,000 each to form a partnership. Mary has been authorized a salary of $20,000, while Nancy’s salary is $25,000. Each partner is to receive 10% on the original capital investment. The profit and loss agreement stipulates that an

> Jones, Silva, and Thompson form a partnership and agree to allocate income equally after recognition of 10% interest on beginning capital balances and monthly salary allowances of $2,000 to Jones and $1,500 to Thompson. Capital balances on January 1 were

> Tom and Julie formed a management consulting partnership on January 1, 2014. The fair value of the net assets invested by each partner follows: During the year, Tom withdrew $15,000 and Julie withdrew $12,000 in anticipation of operating profits. Net p

> Kazma, Folkert, and Tucker are partners with capital account balances of $30,000, $75,000, and $45,000, respectively. Income and losses are divided in a 4:4:2 ratio. When Tucker decided to withdraw, the partnership revalued its assets from $225,000 to $2

> In the appendix to this chapter, the balance sheet for the General Fund for the City of Atlanta is reported. 1. How is the format used on the balance sheet for the general fund different from the format used by for-profit organizations? Which categories

> The partnership agreement of ABC Associates provides that income should be allocated in the following manner: 1. Each partner receives interest of 20% of beginning capital. 2. Sue receives a salary of $25,000 and Josh receives a salary of $21,000. 3. Jos

> Select the best answer for each of the following. 1. Which of the following is not a characteristic of a partnership? (a) Limited life. (b) Mutual agency. (c) Limited liability. (d) Right to dispose of partnership interest. 2. The articles of partnership

> Select the best answer for each of the following. 1. Jon and Joe formed a partnership on July 1, 2014, and invested the following assets: The realty was subject to a mortgage of $25,000, which was assumed by the partnership. The partnership agreement p

> John, Jeff, and Jane decided to engage in a real estate venture as a partnership. John invested $100,000 cash and Jeff provided office equipment that is carried on his books at $82,000. The partners agree that the equipment has a fair value of $110,000.

> Select the best answer for each of the following. 1. Which of the following is not a consideration in segment reporting for diversified companies? (a) Consolidation policy. (b) Defining the segments. (c) Transfer pricing. (d) Allocation of joint costs. 2

> Spur Company’s actual earnings for the first two quarters of 2014 and its estimate during each quarter of its annual earnings are: Actual first-quarter earnings ………………………………………………….. $ 400,000 Actual second-quarter earnings …………………………………………………. 510,000

> Day Company, which uses the FIFO inventory method, had 254,000 units in inventory at the beginning of the year at a FIFO cost per unit of $30. No purchases were made during the year. Quarterly sales information and two sets of end-of-quarter replacement

> The following information concerns the operations of Blane Company for the year ended December 31, 2014. Required: Determine the operating profit (loss) for each of Blane’s two segments for 2014. (In Thousands of Dollars) General

> Twodor Company is involved in four separate industries. Selected financial information concerning Twodor’s involvement in each of the four industries is presented below: Required: Using all tests, determine which of the industry segme

> Pong Industries’ operations involve four operating segments, A, B, C, and D. During the past year, the operating profit (loss) of each segment was Segment Operating Profit (Loss) A ……………………………………………………………………………… $(600) B ………………………………………………………………………

> On April 19, 2011, IBM announced first-quarter 2011 earnings of $2.31 per share (compared to earnings of $1.97 per share in the first quarter of 2010), an increase of 17%. First-quarter net income was $2.9 billion, compared to $2.6 billion in the first q

> In its 10-K amended filing on April 30, 2010, Bronco Drilling reported the financial statements of Challenger Limited (an unconsolidated subsidiary) for its year ending December 31, 2009. The balance sheet and the income statement are reported as follows

> You have purchased a put option on Kimberly Clark common stock. The option has an exercise price of $95.00 and Kimberly Clark’s stock currently trades at $96.18. The option premium is $1.25 per contract. a. Calculate your net profit on the option if Kimb

> You have purchased a call option contract on Johnson & Johnson common stock. The option has an exercise price of $89.00 and J & J’s stock currently trades at $90.43. The option premium is quoted at $2.17 per contract. a. Calculate your net profit on the

> Refer to Table 10–6. a. How many ExxonMobil October 2016 $90.00 put options were outstanding at the open of trading on August 3, 2016? b. What was the closing price of a 10-year Treasury note December 13300 futures call option on August

> You have written a put option on Diebold Inc. common stock. The option has an exercise price of $28 and Diebold’s stock currently trades at $30.50. The option premium is $0.75 per contract. a. What is your net profit if Diebold’s stock price increases to

> Refer to Table 10–4. a. What was the settlement price on the December 2017 Eurodollar futures contract on August 3, 2016? b. How many five-year Treasury note futures contracts traded on August 2, 2016? c. What is the face value on a Swi

> Jones Bank has been borrowing in the U.S. markets and lending abroad, thereby incurring foreign exchange risk. In a recent transaction, it issued a one-year $5 million CD at 4 percent and is planning to fund a loan in yen at 6 percent for a 2 percent exp

> North Bank has been borrowing in the U.S. markets and lending abroad, thereby incurring foreign exchange risk. In a recent transaction, it issued a one-year $2 million CD at 6 percent and is planning to fund a loan in British pounds at 8 percent for a 2

> East Bank has purchased a 5 million one-year Swiss franc (Sf) loan that pays 6 percent interest annually. The spot rate of U.S. dollars for Swiss francs (CHF/USD) is 1.0175. It has funded this loan by accepting a Canadian dollar (C$)– denominated deposit

> Sun Bank USA has purchased a 16 million one-year Australian dollar loan that pays 12 percent interest annually. The spot rate of U.S. dollars for Australian dollars (AUD/USD) is $0.757/ A$1. It has funded this loan by accepting a British pound (BP)– deno

> Bankone issued $200 million worth of one-year CD liabilities in Brazilian reals at a rate of 6.50 percent. The exchange rate of U.S. dollars for Brazilian reals at the time of the transaction was $0.305/Br 1. a. Is Bankone exposed to an appreciation or d