Question: The MD&A for the 2013 City

The MD&A for the 2013 City and County of Denver CAFR is included as Appendix B in this chapter. Following are two tables that have been adapted from the statistical section of the CAFR. Use the MD&A and the provided statistical tables to complete this case.

Required:

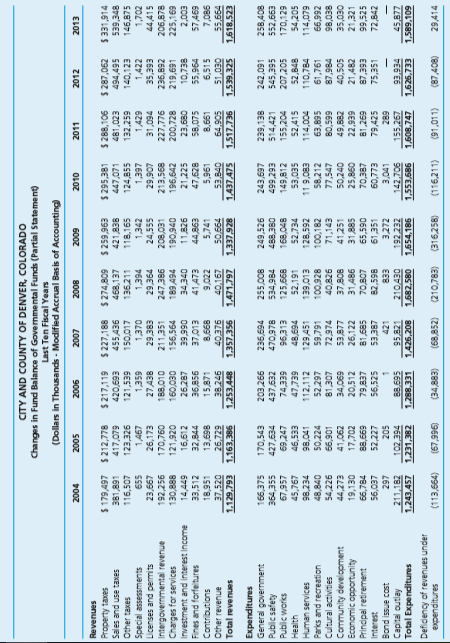

a. What are the three largest sources of governmental funds revenue? What percentage of the governmental funds revenue is from each of these sources?

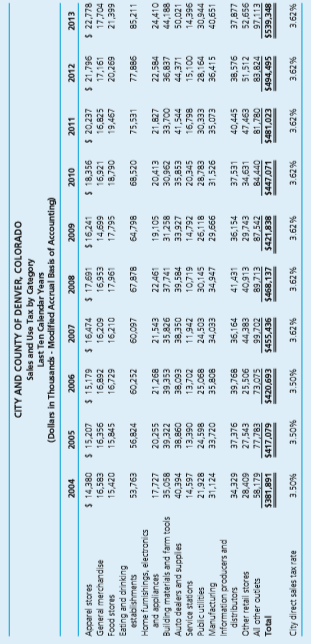

b. Sales tax is a large part of Denver’s tax revenue. Using information from the MD&A and trend information from both statistical tables provided, discuss trends in Denver’s sales tax revenues and your projection for sales tax revenues over the next two to three years.

c. What are the three largest sources of governmental funds expenditures? What percentage of the governmental funds expenditures does each of the three sources represent?

d. Compare the growth in the three largest revenue sources to the growth in the three largest expenditure sources over the past 10years. Using the information from the MD&A and the trend information discuss any changes in the overall expenditure growth patterns you have seen and would expect to see over the next two to three years.

Transcribed Image Text:

CITY AND COUNTY OF DENVER, COLORADO Changes in Fund Balance of Governmental Funds (Partial Statement) Last Ten Fiscal Years (Dollars in Thousands - Modified Accrual Basis of Accounting) 2004 2005 2006 2010 2011 2012 2013 800z 6007 Revenues $ 212,778 417,079 $ 227,188 455,436 $ 287,062 $ 217,119 $ 274,809 468,137 E96 652 S $ 295,381 $ 288,106 $ 331,914 539,348 146,875 Property taxes Sales and use taxes Other taxes Special assessments Licenses and permits Intergovernmental revenue Charges for services Investment and interest Income $ 179,497 381,891 116,507 421,838 118,165 EZO' 187 140,123 123,326 121,539 136,211 124,855 132,259 1,422 1,467 26,173 170,760 121,920 S59 23,667 6SEL 27 A38 1,370 29,383 211,351 44,415 206,878 LO6'62 760' LE EGE'SE 208,031 213,568 227,776 200,728 23,680 236,892 219,691 10,738 192,256 98E LZ 156,564 225,169 888'OEL 16,612 26,287 36,856 15,871 38,246 1,253,448 11,826 21,225 066 6E Fines and forfeitures Contributions Other revenue 32,844 41473 44,863 5,741 v96'SS 6,515 33,512 58,075 ELO LE 697 LS 8,668 40376 1,357,356 5,961 869'EL 26,729 40.167 1,471,797 8,661 64,905 7,086 55,664 1,618.523 53,840 37.520 1.129,793 1.163,385 799 OS 1.337.928 OEO IS 1,437.475 9EL'LISI 1,539,325 senuena jeo1 Expenditures General government Public safety Public works Health 800'SsZ 488,380 243,697 242,091 258,408 552,663 170,129 54,205 114,079 203,266 437,632 249,526 166,375 364,355 239,138 514,421 427,634 470,978 534,984 125,668 545,395 E6Z'667 155,204 207,205 52,848 110,784 61,761 87,984 40,505 67,957 149,812 GEE'DL ELE96 EES'97 98,041 45,767 98,234 48,840 54,226 52,191 52,734 52,415 SEO'ES EBO'6 LL ELO 6EL 100,182 112,112 Human services Parks and recreation 129,451 59,791 72,974 128,592 50,224 52,297 876001 71,143 58,212 77,547 50,240 25,860 SE8'E9 Z66'99 40,826 Cultural activities Community development Economic opportunity Prindpal retirement L06'99 290'L LOE L8 690'vE 665'08 BEO'86 44,273 41,251 49,882 OEO'SE 21,321 LLE'ES 808 LE 20,512 26,122 81,685 31,486 70,807 82,598 588 LE 065's9 LSE 19 21,482 19,130 66,784 81,269 79,425 79,837 70,387 99,525 699'88 EGE"L8 52,227 56,525 75,351 53,387 421 72,842 LEO'9S ELL'09 EEB 210430 3,041 ZEZ Z61 142,706 3,272 682 155,267 1,608,747 1503 anss puog Capital outlay Total Expenditures 95,821 1,426,208 45,877 211.182 1,243,457 1,626,733 1,231,382 1,288,331 1,682,580 1,654,186 1,553,686 60L'68S'L Defidency of revenues under expenditures (113,664) (966'L9) (34,883) (68,852) (210,783) (316,258) (116,211) (91,011) (80 28) 29,414 CITY AND COUNTY OF DENVER, COLORAD0 Sales and Use Tax by Category Last Ten Calendar Years (Dollars in Thousands - Modified Accrual Basis of Accounting) 2004 2008 600z $ 16,241 2010 2011 2012 2013 Sooz 9007 LO0Z $ 14,380 $ 15,207 $ 15,179 $ 16,474 16,209 $ 17,691 $ 18,356 16,921 $ 20,237 Apparel stores General merchandise 96L'IZ S 17,161 BLL'Z2 S 16,356 15,845 16,953 16,825 17,704 Z68'91 669'ri 692'oz 77,886 85,211 15,420 16,729 16,210 17,961 19,467 SaJoIs poo 06L'8L Eating and drinking establishments Home fumishings, electronics and appliances Building materials and farm tocis Auto dealers and supples 53,763 60,252 67,878 68,520 75,531 L60'09 86L'19 17,727 35,058 20,255 39,322 21,268 22 461 20,413 22,584 24,410 44,188 50,021 21,543 19,105 35,826 38,350 37,741 39,584 10,719 31,258 33,700 41,544 ESE'6E 296'0E LEB'9E E60'BE 13,702 ESS'SE 20,345 33,927 44,371 Service stations 098'BE 14,597 21,928 31,124 06E'EL 24,598 11,942 00L'SL 28,164 86L'91 Public utilities Manufacturing Information producers and distributors Other retail stores Al other outiets 24,503 30,145 34,947 26,118 28,783 31,526 EEE'0E ELO'SE 890'SZ 33,720 35,808 29,666 36,415 40,651 EEO'DE 41,431 37,531 34,631 84,440 $447,071 34,329 37,376 39,768 36,164 36,154 40,445 47,463 81,780 $481,023 38,576 51,512 83,824 $494,495 37,877 28,409 58.179 $381,891 27,543 77,783 $417,079 EBE' ZOL'66 89,713 $468,137 29,743 959'zs 97,113 90s'sz ELE'Or SLO'EL $455,436 $421,838 $539,348 E69'OZDS City direct sales tax rate %OS'E % 29'E %OS'E %0S'E % 29'E % 29'E %29'E %29'E %29'E % 29'E

> The following is the pre-closing trial balance for Christina Rehabilitation Hospital as of September 30, 2017. Required a. Prepare a statement of operations and a statement of changes in net assets for the year ended September 30, 2017. Not included

> During 2017, the following selected events and transactions were recorded by Milos County Hospital. 1. Gross charges for hospital services, all charged to accounts and notes receivable, were as follows: Patient service revenues………………………………………….$1,664,90

> During its current fiscal year, Evanston General Hospital, a not-for-profit health care organization, had the following revenue-related transactions (amounts summarized for the year). 1. Services provided to inpatients and outpatients amounted to $9,600,

> The Kyle Sports Medicine facility is a not-for-profit health care facility that is trying to determine what transaction information should be included in its calculation of the performance indicator it uses to report its results of operations. Indicate w

> Following are several unrelated transactions involving a hospital. 1. The hospital has a contractual agreement with a lender requiring that $500,000 in cash be set aside to meet its future debt payment. 2. The hospital accrued $1,500,000 in patient servi

> Choose the best answer. 1. The AICPA Audit and Accounting Guide Health Care Entities is considered category b authoritative guidance that can be used by which of the following? a. A business-type government hospital. b. A not-for-profit hospital. c. A fo

> Information from the 2012 Form 990 and the 2013 annual report for Feeding America , follows. Although the Form 990 indicates it is for 2012, it is actually for the period July 1, 2012, to June 30, 2013, the same time period as the 2013 annual report. Use

> The Silverton Symphony Orchestra Hall is a well-established not-for-profit organization exempt under IRC Sec. 501(c)(3) that owns a facility that is home to the local symphony orchestra. Its mission is to increase access to the arts for the community of

> The Let’s Read organization is a public charity under IRC Sec. 501(c)(3). It had total support of the following: United Way support………………………………………….$ 10,000 Grant from the state……………………………………………25,000 Grant from the city………………………………………………10,000 Con

> You are a governmental accountant for a large municipality, and you have recently been assigned to the budget office and charged with building a better budget document—one that will be of the highest quality, so that citizens and others with an interest

> The midsize City of Orangeville funds an animal control program intended to minimize the danger stray dogs pose to people and property. The program is under scrutiny because of current budgetary constraints and constituency pressure. An animal control wa

> The City of Ashcroft has produced a Service Efforts and Accomplishments report for the past four years in an attempt to answer the question, “How are we doing?” for its citizens. Reproduced here is an excerpt from the

> The City of Manhattan, Kansas, prepares an annual Budget Book, a comprehensive document that includes a citywide budget, as well as departmental budgets. The city has received the GFOA Distinguished Budget Award for more than 25 years. Following are grap

> The police chief of the Town of Meridian submitted the following budget request for the police department for the forthcoming budget year 2017–18. Upon questioning by the newly appointed town manager, a recent masters graduate with

> Choose the best answer. 1. Budgets of government entities: a. Are integrated with the financial accounting system. b. Enable governments to demonstrate compliance with laws and to communicate performance effectiveness. c. Are adopted by governments after

> The United States Office of Management and Budget (OMB) provides guidance on the allow ability of costs under federal grant agreements in Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards. Following is a lis

> The City of Greeley, Colorado’s, fire department, prepares annual Performance Measures. Following are excerpts from the 2013 fire department performance report. Required: a. Examine the following performance report. In what areas did t

> Following is the audit report for the City of Prairie View. Citizens of Prairie View: Split Responsibility for Financial Statements We have audited the accompanying financial statements of the City of Prairie View (the City) as of and for the year ended

> Choose the best answer. 1. Under the hierarchy of GAAP for a state and local government, which of the following has the highest level of authority? a. AICPA Practice Bulletins if specifically made applicable to state and local governments by the AICPA (a

> Collier County had the following federal award activity during the most recent fiscal year: Required: a. Based on size, which programs would be considered Type A programs? Type B programs? b. Based on the information provided above, list any low-risk

> You are the finance director of White Rock City. Your current auditor informs you that he is retiring and selling his auditing practice. When you seek his advice regarding the hiring of the accounting firm that is currently helping to integrate a new acc

> Use Illustration 14–3 as a guide in completing this exercise. ______1. Fredericksburg Chamber of Commerce ______2. American Diabetes Association ______3. American Legion ______4. American Museum of Natural History ______5. American Institute of Certified

> Caring Community Hospital, a not-for-profit hospital, recorded the following transactions. 1. Received $20 as co-pay from a patient for an out-patient visit. Billed $500 to insurance. 2. Gift shop sales amounted to $1,500. 3. Citizen’s Health Insurance p

> Gail McCook, the administrative assistant of a local CPA firm, merged the files listing GAAS standards and GAGAS standards. Because the firm performs both GAAS and GAGAS audits, it is important to identify which standards are applicable to which audits.

> Following is a list of a number of accounts used by federal agencies. Required: For each of the accounts listed indicate in Column A whether the account is a proprietary account (P) or a budgetary account (B). In Column B indicate whether the account

> Access the most recent Financial Report of the U.S. Government at the U.S. Treasury Department Web site, www.fms.treas.gov/fr, and answer the following questions. Required: a. What are amounts of the total budget deficit and net operating cost for eac

> The source of authoritative guidance for federal financial accounting and reporting is the Federal Accounting Standards Advisory Board. To better understand the FASAB, access its Web site at www. fasab.gov to answer the following. Required: a. What is t

> In 2013, 22 of 24 CFO Act agencies received unqualified (unmodified) audit opinions. The Comptroller General disclaimed an opinion on one agency, and one agency received a qualified opinion. The one agency receiving a qualified opinion was HUD (Housing a

> The U.S. Department of Health and Human Services maintains the Web site www.hospitalcompare. hhs.gov, which provides an array of measures that report on individual hospitals and other types of health care providers. Access the Web site for help in co

> In 2010, Congress passed and the President signed into law the Patient Protection and Affordability Act. The act provides for sweeping changes to health care and has been extremely controversial. To learn more about this act, go to www.healthcare.gov

> Custer County receives pass-through funds from the state’s Department of Justice to assist in administering the federally funded Public Safety Partnership and Community Policing Grants program (also referred to as Community Oriented Policing Services [CO

> The Internal Revenue Service (IRS) initiated a study of not-for-profit hospitals in 2006. One purpose of the study was to help the IRS better understand the community benefit provided by not-for-profit hospitals. Community benefit is a critical factor in

> Carol Hernandez has recently been appointed director of the foundation for a private university located in the state of Minnesota. She is intent on learning as much as she can about the foundation’s responsibilities concerning the management and investme

> The chief administrator for a group of not-for profit early education centers and outreach facilities has hired you to conduct an audit. A mission of the organization is to provide child care and early education to children in economically distressed are

> Following is the governmental activities pre-closing trial balance for the Town of Freaz. Freaz is a relatively small town and, as a result, it has only governmental funds (i.e., it uses no proprietary funds). There are no component units. To complete th

> A city has approached you concerning the audit of its 2017 financial statements. State law requires the city to have an audit and submit the audited financial report to the state. New elections at the beginning of the fiscal year resulted in a change in

> Illustration 10–4, adapted from Crawford and Associates, lists several ratios under the heading Financial Position. Which of the ratios listed most closely aligns with the GASB research study definition of financial position provided on page 409? Explain

> Lake View Mental Health Affiliates, a nongovernmental not-for-profit organization, has contacted William Wise, CPA, about conducting an annual audit for its first year of operations. The governing board wishes to obtain an audit of the financial statemen

> The city council members of Laurel City are considering establishing an audit committee as a subset of the council. Several members work for commercial businesses that have such committees. They have asked your advice as a partner in the public accountin

> A federal government initiative to rate public colleges and universities has been undertaken by the U.S. Department of Education. Performance measures for K–12 education have been part of the federal funding initiative for many years with such programs a

> One of the responsibilities of an auditor is to determine the appropriate GAAP for the entity being audited. In December, 2013, GASB issued an exposure draft titled “ The Hierarchy of Generally Accepted Accounting Principles for State and Local Governmen

> The City of St. Cloud, Minnesota, annually prepares a trend report using the ICMA’s Financial Trend Monitoring System. The table presented here captures trend information provided by St. Cloud in its 2013 Annual Financial Trend Report.

> In 2010 the city had failed to honor its guarantees on The Harrisburg Authority (THA) debt. (THA is a component unit of the city.) In 2011 Harrisburg filed for bankruptcy; however, the bankruptcy petition was denied by the court. The State of Pennsylvani

> You are a new city council person for the City of Columbia, Missouri. You are aware that several cities have been in the news recently because of the financial crises they have faced. The governing bodies have been criticized for not being aware of the n

> Identify some of the characteristics of a government’s citizens that can affect the government’s financial condition. Explain how the characteristics affect financial condition.

> Examine the following tables from the Financial Trend Monitoring Report for the Town of Oakdale that reports on fiscal year 2017. The performance indicators selected are total revenue and revenue per capita. The town provides three reference groups wi

> Throughout Chapters 2-9 reference has been made to the City and County of Denver’s Comprehensive Annual Financial Report (CAFR). In addition to issuing the CAFR the City and County of Denver issues a Popular Annual Financial Report (PAFR). To complete th

> Write the letters a through o on a sheet of paper. Beside each letter, put a plus ( 1 ) if a high or increasing value of the item is generally associated with stronger financial condition, a minus ( 2) if a high or increasing value of the item is ge

> In its notes to the financial statements t he City of St. Petersburg, Florida provided the following information about the amounts and classifications for the St. Petersburg fund balances. Use the information provided by St. Petersburg to complete thi

> Following are the operating statements for a public and private college. The operating statements have been adapted from the annual reports of a public and a private university. As would be expected, the reports are somewhat different. Catherine College

> Following are descriptions of several relationships between primary governments and other organizations.* * Information used in this case is adapted from information provided in the GASB Comprehensive Implementation Guide (Norwalk, CT, 2010). Required:

> *In the 2010 CAFR, Detroit indicated that its general obligation debt rating had been downgraded by Moody’s Investors Services from a Ba2 to a Ba3. Based on its fourth quarter Performance Dashboard 1 Detroit was subsequently downgraded

> Electronic Municipal Market Access (EMMA) provides investors and others interested in state and local government debt and financial information an excellent resource. By accessing EMMA an individual is able to learn about what type of debt is outstanding

> What is an IRC Sec. 527 organization? Are these organizations tax-exempt? What filing requirements have been imposed on 527 organizations by campaign finance laws?

> Discuss what, if any, political activity can be undertaken by a charitable NFP organization.

> What are the distinguishing characteristics between a public charity and a private foundation? What is a public support test and how does it relate to public charities and private foundations?

> What is the purpose of the Form 990? Because there are different types of Form 990, explain how an NFP would know which type it must file.

> Explain a major difference between a 501(c)(3) tax-exempt organization and a 501(c)(7) tax-exempt organization.

> Identify which level(s) of government regulate(s) NFP organizations and identify the source of authority.

> What are articles of incorporation and how do they differ from by-laws of a NFP organization?

> Obtain the most recent copy of the annual report for your college or university (school). Using the annual report, answer the following. Required: a. Does your school follow GASB or FASB standards? Use the financial statements to explain how you can tel

> The financial manager of a not-for-profit child care center wants to improve the monthly report to the board and has decided to include performance measures What are the benefits of providing performance measures? How will board members be able to determ

> What are excessive benefits and what are the consequences of paying/receiving excessive benefits?

> What is a split interest agreement, and why do you believe a donor or a university would enter into such an agreement?

> The NACUBO expense accounts typically used by colleges and universities do not identify the program and support functions. Discuss whether colleges and universities are required to identify program and support expenses and how this is accomplished if the

> A private college has received pledges that are due within one year and pledges that are long-term (that is, due in more than one year). How will the college report the pledges in its financial statements?

> When would receipt of a grant be recorded as revenue rather than a contribution? Give an example of a transaction in which a grant would be recorded as revenue.

> How do private colleges and universities account for bad debts related to tuition and fees? Compare the accounting to that of public and for-profit (corporate) colleges and universities.

> For each of the following situations explain how a private and a public university would record the transaction (assume the grants are non exchange): notification of a grant to be received in the next fiscal year; receipt of a grant with a purpose restri

> Discuss whether colleges and universities are subject to audits under Government Auditing Standards (GAS).

> Identify the financial statements that must be prepared by a private college or university and those that must be prepared by a public college or university.

> You are considering making a contribution to the Conservation Fund . However, as an accountant you decide to conduct “due diligence” related to the efficiency and effectiveness of the Conservation Fund before making your contribution. You are aware of

> What are some ways an audit report for a government differs from an audit report for a for-profit organization?

> As a newly hired staff auditor, you have been assigned to a governmental engagement that includes a single audit. Your supervisor asks you to familiarize yourself with OMB’s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for

> In the context of a government audit, what is an opinion unit, and of what significance is an opinion unit to the auditor?

> What are the three types of auditor services described in the Government Accountability Office’s Government Auditing Standards, and how do they differ?

> What is the purpose of a financial audit? Who is responsible for setting standards for financial audits of government and not-for-profit organizations?

> What is EMMA and when would someone want to use EMMA?

> Identify factors that the rating agencies use in determining bond ratings. Which of the factors identified is beyond management control and how could this factor affect the government’s finances?

> Government Auditing Standards specifically outline an auditor’s responsibilities with respect to ethics and independence. What are the ethical principles and primary considerations with regard to independence, as identified in GAGAS? How do ethical princ

> In 2013, the Tampa Bay Times published a series of four articles uncovering some of the worst charities in America. Read the articles ( www.tampabay.com/topics/specials/ worst-charities. page ) and answer the following questions. Required: a. What

> Should citizens be concerned if the funded ratio for pension plans decreases over time? Why?

> When conducting a financial analysis, ratios based solely on governmental fund financial statements would not be considered sufficient for assessing economic condition. Explain why this statement would be true.

> Explain the difference between a blended and discretely presented component unit, and explain how each is reported.

> Under the hierarchy of GAAP, what sources of accounting principles have the most authority for state and local governments, federal government entities, and nongovernmental entities? Where do accountants and auditors look when a particular item is not co

> The GASB indicates that economic condition is composed of three components. Identify and define the three components of economic condition.

> State and general purpose local governments are considered primary governments. Under what circumstances a special purpose government would be considered a primary government?

> Under GASB guidance when should an item be recognized on the face of the financial statements? Under what conditions, would the GASB indicate that a note disclosure should accompany an item that has been recognized on the financial statements?

> W hat are the two tracks in the dual-track accounting system? Explain the purpose of each track. Relate each track to state and local governmental “dual track” accounting.

> What are stewardship assets? How does the accounting for a stewardship asset differ from that for general property, plant, and equipment?

> The federal government uses two groups of funds. Identify the two fund groups, and the funds associated with each group. Compare the funds to those used by state and local governments.

> Go to the Internet Web sites of any five of the charitable organizations listed in Illustration 14–7 and search for financial information and performance measures they may disclose on their Web sites. Required: a. For the most recent year provided on t

> Defining the reporting entity at the federal level is complicated by different perspectives from which the federal government can be viewed. What are the three perspectives? How are they defined? How do they interrelate?

> Explain the differences among these accounts: (1) Estimated Revenues used by state and local governments, (2) Other Appropriations Realized used by federal agencies in their budgetary track, and (3) Fund Balance with Treasury used by federal agenci

> According to the FASAB conceptual framework, there are four objectives for federal financial reporting. Discuss the four objectives and explain why the focus of the FASAB objectives differs from that of the FASB or the GASB.

> Compare the GAAP hierarchy for the federal government to that for state and local governments (see Chapter 11).

> What are the components of the PAR and where would a federal agency go to find out the requirements for preparing a PAR?

> Explain the role of the Government Accountability Office (GAO), the Department of the Treasury, and the Office of Management and Budget (OMB) in the financial accounting and reporting of the federal government.

> What is the Patient Protection Affordability Act, and what impact has it had on NFP hospitals’ financial reporting and tax filing?

> What is premium revenue, and when is it recognized? Discuss the recognition of revenue relative to the revenue recognition and matching concepts in accounting.