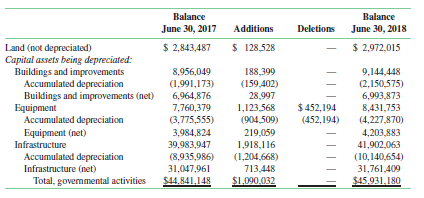

Question: The schedule that follows pertaining to

The schedule that follows pertaining to governmental capital assets was excerpted from the annual report of Urbana, Illinois (with changed dates):

A related schedule indicates the following:

Capital outlays…………………………………………… $ 3,358,611

Depreciation……………………………………………… (2,268,579)

…………………………………………………………………$ 1,090,032

1. As required by GASB Statement No. 34, the annual report includes reconciliations between:

(1) total fund balance, governmental funds (per the funds statements), and net position of governmental activities (per the government-wide statements); and

(2) net change in fund balance, governmental funds (per the funds statements), and change in net position of governmental activities (per the government wide statements). In what way would the data provided in the accompanying schedules be incorporated into the two reconciliations? Be specific.

2. The amount deleted from the equipment account ($452,194) exactly equals the amount deleted from the related accumulated depreciation account. Is this merely a coincidence? Would the amounts always be the same?

3. Based simply on the amount of equipment retired, what would you estimate to be the average useful life of the equipment? Is this reasonable?

Transcribed Image Text:

Balance Balance June 30, 2017 Additions Deletions June 30, 2018 $ 2,843,487 $ 128,528 $ 2,972,015 Land (not depreciated) Capital assets being depreciated: Buildings and improvements Accumulated depreciation Buildings and improvements (net) Equipment 8,956,049 (1,991,173) 6,964,876 7,760,379 (3,775,555) 3,984,824 188,399 (159,402) 28,997 1,123,568 (904,509) 9,144,448 (2,150,575) 6,993,873 8,431,753 (4,227,870) $ 452,194 (452,194) Accumulated depreciation Equipment (net) 219,059 1,918,116 (1,204,668) 4,203,883 41,902,063 (10,140,654) 31,761,409 Infrastructure 39,983,947 (8,935,986) 31,047,961 Accumulated depreciation Infrastructure (net) 713,448 Total, govemmental activities $44.841,148 S1.090.032 $45.931.180

> The accompanying combined statement of revenues, expenditures, and fund balance was drawn from the statements of Plant City, Florida, which, of course, included a general and other funds that are not shown. Suppose, however, that these were the only fund

> As stated in the previous problem, a government issued $8.5 million of special assessment bonds to finance a sewer‐extension project. To service the debt, it assessed property owners $8.5 million. Their obligations are payable over a period of five years

> Upon annexing a recently developed subdivision, a government undertakes to extend sewer lines to the area. The estimated cost is $10.0 million. The project is to be funded with $8.5 million in special assessment bonds and a $1.0 million reimbursement gra

> Vision for Kids, a clinic funded by the Community Health Plan, a not‐for‐profit agency, provides eye examinations, eyeglasses, and eye‐related medical care for children from low‐income families. Children are referred to the clinic by school nurses and te

> The balance sheet and a comparative statement (budget‐to‐actual) of revenues, expenditures, and changes in fund balance of Parkville’s general obligation debt service fund (date changed) is presented

> Durwin County issued $200 million in long‐term debt to fund major improvements to the county’s road and transportation systems. The debt is to be serviced from the proceeds of a specially dedicated property tax. The ac

> Crystal City established a capital projects fund to account for the construction of a new bridge. During the year the fund was established, the city issued bonds, signed (and encumbered) $6 million in contracts with various suppliers and contractors, and

> A city engages in an in‐substance defeasance of long‐term bonds and accordingly invests in, and sets aside, the long‐term securities necessary to make the required interest and principles payments on the debt to be retired. Should, and if so under what c

> A city levies a property tax that is restricted for future period payments of principal and interest on outstanding debt. The tax receipts are recorded in a debt service fund and are invested in interest‐and dividendearning securities. Hence, the amount

> Near the end of its fiscal year a school district issues $80 million of bonds to construct a new high school. By year‐end the district has received the proceeds of the bonds and invested them in short‐term securities. It has not yet incurred any construc

> What is meant by an in-substance defeasance, and how can a government use it to lower its interest costs? How must it recognize a gain or loss on defeasance if it accounts for the debt in a proprietary fund? How do the GASB standards pertaining to in‐sub

> Under what circumstances can a government refund outstanding debt and thereby take advantage of a decline in interest rates?

> What is arbitrage? Why does the Internal Revenue Service place strict limits on the amount of arbitrage that a municipality can earn?

> A government issues bonds at a discount. Where would the government report the discount on its (a) fund statements and (b) government‐wide statements?

> The following are selected measures of service efforts and accomplishments that might be appropriate for a university. For each, indicate whether it is an input, output, or outcome, and state the objective with which it would most likely be associated. I

> How should governments report their capital projects and debt service activities in their governmentwide statements?

> Special assessment debt may be, in economic substance and/or legal form, an obligation of the assessed property owners rather than a government. Should the government, therefore, report it in its statements as if it were its own debt? What are the curren

> At one time governments maintained a unique type of fund to account for special assessments. This fund recorded the construction in process, the long‐term debt, and the assessments receivable. Explain briefly how governments account for special assessmen

> It is sometimes said that in debt service funds the accounting for interest revenue is inconsistent with that for interest expenditure. Explain. What is the rationale for this seeming inconsistency?

> When bonds are issued for capital projects, premiums are generally not accounted for as the mirror image of discounts. Why not?

> Does the government own any “unusual” securities such as derivatives? If so, does the report contain an explanation of these transactions?

> Judging from the disclosures pertaining to investments, does the entity have any investments that appear to be especially risky? In your judgment, to which risk (e.g., credit risk, interest rate risk, foreign currency risk) is the exposure of the entity

> Did the government capitalize collections of art or historical treasures? Did it depreciate such collections?

> Did the government capitalize infrastructure assets acquired during the year? Did it account for infrastructure assets using the “standard” or the “modified” approach?

> How much depreciation did the government charge in its government-wide statements on capital assets used in governmental activities?

> Access the website of the American Red Cross (www.redcross.com) and the American Diabetes Association (www.diabetes.org) and obtain the audited financial statements and Form 990 for the latest fiscal years available. Form 990 can also be obtained from ww

> What is the city’s threshold policy on capitalizing general capital assets and intangible assets?

> What was the total amount of capital assets used in governmental activities added during the year? What was the amount retired?

> What are the principal classes of capital assets associated with governmental activities that the city reports in its financial statements?

> A government holds the following investments. For each, indicate the category in which it should most likely be classified. 1. A 20-year, 4 percent corporate bond rated AA by a leading rating agency. The bond is not widely traded in a market. 2. Shares i

> A city acquired general capital assets as follows: 1. It purchased new construction equipment. List price was $400,000, but the city was granted a 10 percent “government discount.” The city also incurred $12,000 in transportation costs and paid $4,000 to

> Refer to the transactions in the previous exercise. 1. Prepare journal entries that the city would make in its governmental funds (e.g., its general fund or a capital projects fund). 2. How would you recommend that the city maintain accounting control ov

> The following summarizes the history of the Sharp City Recreation Center. 1. In 1990, the city constructed the building at a cost of $1,500,000. Of this amount, $1,000,000 was financed with bonds and the balance from unrestricted city funds. 2. In the 10

> A city engaged in the following transactions during a year: 1. It acquired computer equipment at a cost of $40,000. 2. It completed construction of a new jail, incurring $245,000 in new costs. In the previous year the city had incurred $2.5 million in co

> Select the best answer. 1. A government repaves a section of highway every four years at a cost of $2 million to preserve it at a specific condition level. How much should it report in depreciation charges under the modified approach to accounting for i

> Select the best answer. 1. Which of the following would be least likely to be classified as a city’s general capital assets? a. Roads and bridges b. Electric utility lines c. Computers used by the police department d. Computers used by the department th

> Select the best answer. 1. A key determinant as to whether, under Circular A133, a program is considered major or nonmajor is a. The overall size of the program as measured by total revenues, regardless of source b. The overall size of the program as me

> Northstate University had constructed a theater at a cost of $20 million. It anticipated a useful life of 30 years. After 18 years (with the building 60 percent depreciated), the university dropped its drama program; it no longer had need for a theater.

> Clarkstown State University acquired specialized laboratory equipment with the expectation that it would be used to perform approximately 3,000 tests per year over a 10-year period. The cost was $600,000. After the equipment had been used for only three

> The Middleville School district has discovered mold in one of its schools. The school was constructed 10 years ago at a cost of $30 million. It had an expected useful life of 50 years and hence was 20 percent depreciated. The cost to replace the school t

> Bear County maintains an investment pool for school districts and other governments within its jurisdiction. Participating governments contribute cash to the pool, which is operated like a mutual fund, and receive in return a proportionate share of all d

> A government holds as investments the assets set forth below and determines its fair value as described. For each, indicate the level (1, 2, or 3) within the hierarchy of inputs to valuation techniques in which the investment should be classified and how

> A note from the annual report of a city includes the following: As of September 30, the utility fund had the following investments: Credit risk. As of September 30, the U.S. Treasuries and the U.S. Agency Bonds were rated AAA by Standard & Poorâ

> On August 2, 30 days prior to the end of its August 31 fiscal year, a government issues $3 million of general obligation bonds. The proceeds are being accounted for in a capital projects fund (a governmental fund). To earn a return on the bond proceeds b

> A government held the securities shown in the following table in one of its investment portfolios. All the securities are either stocks or bonds that mature in more than one year. 1. Ignoring dividends and interest, how much gain or loss should the gover

> The City of Allentown recently received a donation of two items: 1. A letter written in 1820 from James Allen, the town’s founder, in which he sets forth his plan for the town’s development. Independent appraisers have valued the letter at $24,000. 2. A

> In 2017 Bantham County incurred $80 million in costs to construct a new highway. Engineers estimate that the useful life of the highway is 20 years. 1. Prepare the entry that the county should make to record annual depreciation (straight-line method) to

> Select the best answer. 1. Government Auditing Standards must be adhered to in all financial audits of a. State and local governments b. Federal agencies c. Federally chartered banks d. All of the above 2. “Generally accepted government auditing standa

> A school district constructs a new elementary school at a cost of $24 million. It finances the project by issuing 30-year general obligation serial bonds, payable evenly over the outstanding term ($800,000 per year). District officials estimate that the

> In the management discussion and analysis accompanying its 2018 financial statements, Tiber County reported that “for the fifth consecutive year revenues exceeded expenditures.” However, a note included in required sup

> The following totals were drawn from Independence City’s “Schedule of Changes in Capital Assets by Function and Activity,” included in the city’s financial statements for the year en

> A city’s road maintenance department received “donations” of two types of assets: 1. From the county in which the city is located it received earthmoving equipment. The equipment had cost the county $800,000 when it was acquired five years earlier. Accou

> In the year a road maintenance district was established, it engaged in the transactions that follow involving capital assets (all dollar amounts in thousands). The district maintains only a single governmental fund (a general fund). 1. Received authority

> A city maintains botanical gardens that contain valuable plants. Should these plants be considered “collectibles,” such as museum pieces, or infrastructure, such as parks?

> A state acquired a large parcel of forest land, which at some time in the future, it expects to license to timber companies so that they can harvest and sell the trees. For now, however, the land is used primarily for recreation. The state maintains hiki

> Per the GASB, held-to-maturity securities, such as bonds, must be reported at fair value, even if they will be eventually redeemed at stated or face value. Thus gains and losses on changes in fair value must be periodically recognized, even if such losse

> The GASB establishes a hierarchy of inputs to determine the fair values of investments. What are the three levels of the hierarchy?

> What are the advantages of “monetizing” the value of human lives (often said to be “priceless”) in assessing the costs and benefits of a proposed project or activity? What is the most widely used basis for valuing human lives? What are the limitations of

> How can governments use derivatives as a means of reducing investment or borrowing risks?

> What are derivatives? Why can they be especially high-risk securities?

> What are the differences between market risk, credit risk, and legal risk? Suppose that a local government invests in 20-year U.S. government bonds. Assess each of the three risks, and discuss the disclosures required by a government on its financial sta

> Per the provisions of Statement No. 34, governments must report their capital assets similar to businesses in their government-wide statements. Yet the information provided is still inadequate to facilitate the major types of decisions and judgments made

> What are deferred maintenance costs, and when and how must a government report them (as they relate to infrastructure) in its financial statements?

> Why have many government officials objected to Statement No. 34’s requirement that infrastructure assets be accounted for similar to other capital assets?

> Although Statement No. 34 requires that infrastructure assets be accounted for similar to other capital assets, it allows for a major exception with regard to depreciation. What is that exception?

> A city establishes an art museum. What options does it have in accounting for its collection of paintings?

> How should governments report their long-lived assets in their government-wide financial statements?

> Although many governments prepare budgets for both capital projects and debt service funds and integrate them into their accounts, budgetary control over these funds is not as essential as it is for other governmental funds. Do you agree? Explain. If bud

> The following descriptions relate to an independent CPA firm that includes among its audit clients municipalities, school districts, and not‐for‐profit organizations, all of which receive federal financial assistance. Each description presents a possible

> Does the city have outstanding any conduit debt?

> Compute the total amount of the city’s direct and overlapping debt?

> Does the city have any lease obligations outstanding? Are these accounted for as operating or capital leases? Can you determine if any of these leases were initiated during this year? What is the amount of payments related to capital leases?

> What is the city’s legal debt margin?

> What is the percentage of total net bonded debt to assessed value of property? What is the amount of net debt per capita?

> Did the city increase or decrease its long-term borrowings during the year? What was the effect on total long-term liabilities at year end? Explain.

> The Cleveland Historical Society issues $40 million of 6 percent, 15-year bonds at a price of $36,321,000 to finance the construction of a new museum. The price reflects an annual yield of 7.0 percent. 1. Prepare the journal entry to record the issuance

> Has the city entered into any service concession arrangements? Which specific ones, and why?

> What was the total operating income? What was total net cash provided by operating activities? What accounts for the largest difference between these two amounts?

> Do the financial statements include a statement of cash flows for proprietary funds? Is the statement on a direct or an indirect basis? In how many categories are the cash flows presented? Which of these categories resulted in net cash inflows? Which res

> The City on the Lake Convention Center was constructed at a cost of $250 million with the aim of attracting visitors to the area. Taxpayers were assured that the convention center would be self‐supporting: that convention center revenue would be sufficie

> Does the government have revenue bonds outstanding that are related to business-type activities? If so, for what activities?

> Were any of the government’s enterprise funds “profitable” during the year? If so, what has the government done with the “earnings”? Has it transferred them to the general fund?

> Did any of the internal service funds report significant operating surpluses or deficits for the year? Were any accumulated significant net asset balances over the years not invested in capital assets?

> How are the internal service fund activities reported in the government-wide statement of net position? How are they reported in the proprietary funds statement of net position?

> Indicate the activities accounted for in both internal service funds and major enterprise funds. Comment on whether any of these activities could also have been accounted for in a general or other governmental fund.

> Why are bond ratings of vital concern to bond issuers?

> In 2017 Marquette County opened a landfill that was expected to accept waste for four years. The following table indicates the estimates county officials made at the end of each of the four years: Determine the total expected closure costs ($10 million)

> The water and wastewater utility (enterprise) funds of three cities each paid $1 million in casualty insurance premiums. City A is insured by a small independent insurance company. City B is self-insured and accounts for its insurance activities in an in

> The following list of cash flows was taken from the statement of cash flows of Grand Junction’s internal service fund (with all amounts expressed in thousands): Cash on hand at beginning of year………………………… $ 122 Interest from investments………………………………………..

> The following data relate to the City of Spicewood’s data processing internal service fund: Billings to police and fire departments……………………………….……. $ 800,000 Billings to water utility department……………………………………..…… $ 200,000 Year-end receivable from police

> The chairman of a state legislature’s finance committee has charged that the Division of Taxation’s computer systems are in chaos and, as a consequence, the state is failing to collect hundreds of millions in income taxes to which it is entitled. Accordi

> The Louisville City bus system engaged in the following transactions: 1. It issued $10,000,000 in 8 percent revenue bonds. It used the proceeds to acquire new buses. The bonds were issued at par. 2. Consistent with a bond covenant, the system set aside 1

> William County opted to account for its duplication service center in an internal service fund. Previously the center had been accounted for in the county’s general fund. During the first month in which it was accounted for as an internal service fund th

> Select the best answer. 1. A city’s general fund has an outstanding payable to its electric utility, which is accounted for in an enterprise fund. The utility has a corresponding receivable from the general fund. In the city’s government-wide statement

> The city of Tribville recently centralized its mobile technology (phones, computers, and tablets) functions for the government in a single internal service fund. City officials want the fund to break even, so they need rates to be set appropriately. The

> The City Electric Utility (CEU), which a city accounts for in its enterprise fund, provides cash rebates to customers who install insulation, storm windows, or energy-saving appliances. The payments are intended to reduce the demand for electricity and t

> What follows are the statement of revenues, expenses, and changes in net position, and the statement of cash flows for Tucson, Arizona’s fleet services internal service fund. 1. How do you account for the difference between net operating income of $105 a

> In Year 1, as a result of routine testing, a city discovers that local wells are polluted. Investigation reveals that the source of the contamination is an abandoned waste dump that the city owns. At a cost of $25,000, the county conducts a feasibility s

> In 2018, a city opens a municipal landfill, which it will account for in an enterprise fund. It estimates capacity to be 6 million cubic feet and usable life to be 20 years. To close the landfill, the municipality expects to incur labor, material, and eq

> A municipality expects to use a landfill evenly throughout the 25 years from January 1, 2017, to December 31, 2041. Upon closing the landfill it estimates that it will incur closing costs of $300,000. Thereafter, it anticipates it will have to monitor th