Question: The Umbro Company, which is a fitness

The Umbro Company, which is a fitness center, was formed on January 2 of the current year. Transactions completed during the first year of operation are presented below. January 2: Issued 900,000 shares of common stock for $15,000,000, which is the par value of the stock. January 10: Acquired equipment in exchange for $2,500,000 cash and a $6,000,000 note payable. The note is due in 10 years.

February 1: Paid $36,000 for a business insurance policy covering the two-year period beginning on February 1.

February 22: Purchased $930,000 of supplies on account.

March 1: Paid wages of $194,600.

March 23: Billed $2,820,000 for services rendered on account.

April 1: Paid $130,000 of the amount due on the supplies purchased on February 22.

April 17: Collected $190,000 of the outstanding accounts receivable.

May 1: Paid wages of $209,400. May 8: Received bill and paid $96,700 for utilities.

May 24: Paid $45,500 for sales commissions.

June 1: Made the first payment on the note issued on January 10. The payment consisted of $50,000 of interest and $210,000 to be applied against the principal of the note.

June 16: Billed customers for $680,000 of services rendered.

June 30: Collected $450,000 on accounts receivable.

July 10: Purchased $166,000 of supplies on account.

Aug 25: Paid $150,000 for administrative expenses.

Sept 23: Paid $35,000 for warehouse repairs.

October 1: Paid wages of $100,000.

Nov 20: Purchased supplies for $45,000 with cash.

Dec 15: Collected $134,700 in advance for services to be provided in December and January of the following year.

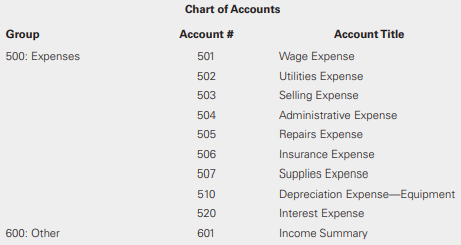

Dec 30: Declared and paid a $50,000 dividend to shareholders. The chart of accounts used by the Umbro Company follows:

a. Journalize the transactions for the year.

b. Post the journal entries to t-accounts.

c. Prepare an unadjusted trial balance as of December 31.

d. Journalize and post adjusting entries to t-accounts based on the following additional information.

i. Eleven months of the insurance policy expired by the end of the year.

ii. Depreciation for the equipment is $420,000.

iii. The company provided a portion of the services related to the advance collection of December 15. The company recognized $72,000 as service revenue for services performed.

iv. There are $501,000 of supplies on hand at the end of the year.

v. An additional $172,000 of interest has accrued on the note by the end of the year.

vi. Umbro accrued wages in the amount of $240,000.

e. Prepare an adjusted trial balance as of December 31.

f. Prepare a single-step income statement and statement of stockholders’ equity for the current year and a classified balance sheet as of the end of the year.

g. Journalize and post-closing entries. h. Prepare a post-closing trial balance as of December 31.

> What is the function of the accounting standard setters?

> What are the roles and responsibilities of an external auditor?

> What is the difference between a point-in-time element and a period-of-time element?

> How is the allocation of capital linked to the demand for financial reporting?

> What is the purpose of generating financial statements and who are the primary users of this information?

> Which items are included in the definition of financial information? Is this concept synonymous with the term financial statements? Explain.

> Are account balances found in the general ledger? Explain.

> Why is the general journal referred to as the “book of original entry”? How are transactions presented in the journal?

> What is meant by the term normal balance? Provide the normal balance for assets, liabilities, and stockholders’ equity.

> What do the terms debit and credit mean?

> Will all transactions have a dual effect on the accounting equation? Explain

> When will retained earnings contain a positive balance? Negative balance?

> What is equity? What are the three components of shareholders’ equity? Explain each component.

> In recent years, what has been the FASB’s approach to standard setting?

> What is the accounting equation and what does it demonstrate?

> What are closing entries? Describe the four closing entries and their effects.

> Which statements can be prepared from the adjusted trial balance? What must be done before preparing the financial statements?

> What is the purpose of the adjusted trial balance? What items are included in the adjusted trial balance?

> What is a deferred revenue? When will the full amount of the deferred revenue be recorded?

> Why are adjusting journal entries made? When do companies make these entries?

> Under the accrual basis of accounting, when do companies record deferrals and accruals?

> Explain the difference between the accrual basis of accounting and the cash basis of accounting? Which basis is acceptable under U.S. GAAP? Explain.

> What is the purpose of an unadjusted trial balance?

> Describe the accounting cycle.

> How does a principles-based standard differ from a rules-based standard?

> What types of biases are individual decision makers subject to when exercising judgment in addressing accounting issues?

> What types of biases are individual decision makers subject to when exercising judgment in addressing accounting issues?

> What is the difference between the availability and confirmatory biases?

> Does IFRS require that companies disclose their accounting policies? Explain.

> Does U.S. GAAP require that companies disclose their accounting policies? Explain.

> Does IFRS require that companies disclose information about the assumptions and estimates they make in their financial statements? Explain.

> Does U.S. GAAP require that companies disclose information about the assumptions and estimates they make in their financial statements? Explain.

> How can management create an impediment to the exercise of good judgment?

> What is research and when is financial accounting research required?

> Explain how accountants and auditors use judgment as they prepare and audit financial statements.

> Is the promulgation of financial accounting standards a political process? Explain.

> What is the Basis for Conclusions and where can they be found for IFRS?

> What is the Basis for Conclusions and where can they be found for U.S. GAAP?

> What is the purpose of a literature hierarchy?

> What is judgment and when is it used by accountants?

> What is the difference between predictive value and confirmatory value?

> What is predictive value?

> Explain the concept of materiality.

> What are the attributes of relevance?

> Explain the concept of relevance.

> Herman and Sons’ Law Offices opened on January 1, 2018. During the first year of business, the company had the following transactions: • January 2: The owners invested $250,000 (the par value of the stock) into the bu

> Branton Stores began operations on January 1, 2018. Branton had the following transactions in its first year of business: • January 4: Owners invested $400,000 (the par value of the stock) in exchange for 40,000 shares of common stock. • January 31: Bran

> Jester Entertainment Company began operations on January 1, 2018. The company had the following transactions in its first year of business: • January 4: Owners invested $120,000 (the par value of the stock) in exchange for 20,000 shares of common stock.

> The Jiayin Li Corporation, which is a technology company, was formed on January 1 of the current year. Transactions completed during the first year of operation follow. January 1: Issued 1,000,000 shares of common stock for $15,000,000, which is the par

> Who are the primary financial statement user groups identified in the objective of financial reporting?

> Who does the FASB consult in the standard-setting process?

> Sherlock Locksmiths, Inc. has the following adjusted trial balance for the year ended December 31, 2018. Required a. Journalize and post the necessary closing entries. Omit explanations. b. Prepare a post-closing trial balance as of December 31.

> Using the information in P4-6 and P4-7, perform the following steps for Tides Tea Company: Required a. Journalize and post the necessary closing entries. Omit explanations. b. Prepare a post-closing trial balance as of December 31. Data from P4-6 and P

> The post-closing trial balance for Heron Consulting Services, Inc. at December 31 of the prior year is presented here. The company reported the following transactions during the current year: • January 2: Heron took out a 5%, 2-year n

> Using the information provided in P4-6, perform the following steps for Tides Tea Company: Required a. Journalize and post adjusting journal entries based on the following additional information (omit explanations): • At December 31, i

> Tides Tea Company began operations on January 1, 2018. During the first year of business, the company had the following transactions: • January 18: The owners invested $200,000 (the par value of the stock) into the business and acquire

> Using the information in P4-3 and P4-4, perform the following steps for Herman and Sons’: Required a. Journalize and post the necessary closing entries at year-end. Omit explanations. b. Prepare a post-closing trial balance as of Dec

> Using the information provided in P4-3, perform the following steps: Data From P4-3: Required a. Journalize and post adjusting journal entries for Herman and Sons’ based on the following additional information: • Of

> Gates Accounting Services (GAS), a sole proprietorship, entered into a new 18-month office space contract on September 15, Year 1, paying the full $36,000 rent contract to the real estate company on that day (lease expiration March 15, Year 3). Assuming

> Jefferson, CPAs provides accounting services for a client at a flat contract rate of $10,000 a month. The terms of the contract include a required payment on the 15th day of each month for the prior month’s accounting services. Assuming Jefferson, CPAs p

> Choco-Delite Cookies Company (Choco) declared a $1,600,000 cash dividend on December 15, Year 2, payable to all stockholders on record the following month. On December 31, Year 2, the company completed a two-for-one stock split (Note: Prior to the split

> Why is a conceptual framework of accounting necessary and justifiable?

> The Cougars football team sells season tickets in advance for $480 each. The season consists of 16 games. Half of these games are home games, and half of them are away games. For Year 3, the team has sold and collected payment for 10,000 season tickets.

> Embree Corp. purchased a four-year insurance policy on May 1, Year 2, for $12,000, effective immediately. The company expensed the full cost of the policy in Year 2. The correct journal entry for Year 2 (ending December 31) will include a: a. Debit to p

> On July 15, Year 1, Southeastern University hired an associate professor for its Math Department at an annual (12-month) salary of $150,000. The salary is effective for its new school year, which commences August 16, and is payable in four quarterly cale

> Sampson Manufacturing Company (SMC) has an empty warehouse that it rents out to a local beer distributor for a monthly rental fee of $6,000. Terms of the rental agreement include a 10-day payment grace period and an additional $200 monthly utility expens

> During the fourth quarter ended December 31, Year 1, Lighting Fixtures Inc. (LFI) had average outstanding revolving bank loans of $1.2 million. Assume that the quarterly interest charges associated with these loans was $7,500. If LFI makes the interest p

> State University sold all of its basketball tickets to its students for 15 home games on September 30 for $1,200,000 (basketball season starts November 1). Assuming the college basketball team played six home games prior to year-end, what adjusting journ

> Windy Harbor Boat Company pays its employees on a weekly basis each Friday. During the week ended Friday, January 3, Year 2, the company had a weekly payroll of $125,750. Assuming that the company is on a calendar basis, has a five-day workweek, and that

> Vikram Patel, one of your friends from high school who is a finance major, is surprised that you are learning about international accounting. Explain why it is important for an accountant in the United States to learn International Financial Reporting St

> Alicia O’Malley, a sociology major, is considering changing her major to accounting. Alicia is having some doubts because she fears that accounting and financial reporting are concerned only with numbers and are isolated from society. Convince Alicia to

> Define financial accounting and describe the four main elements in that definition.

> Are the FASB and IASB conceptual frameworks fully converged? Explain.

> G&S Auto Body, Inc. started 2018 with the following balances: The following transactions occurred during the current year: a. On January 1, the owners invested a total of $150,000 (the par value of the stock) as an additional capital contribution. I

> Using the information provided in E4-7, prepare CC&C’s t-accounts for all relevant accounts for the year ended December 31, 2018. Post journal entries in E4-7 to the general ledger Data from E4-7: Assets 100 Cash 101 Accounts Receivable 102 Supplies 1

> Cookies, Cakes & Crumbs Bakery (CC&C) ended its first year of operations on December 31, 2018. During 2018, the following transactions occurred: CC&C uses the following chart of accounts: Assets 100 Cash 101 Accounts Receivable 102 Supplies

> Using the information provided in E4-5, post Dover Direct Insurance Agency’s journal entries to the general ledger for all relevant accounts for the month ended June 30, 2018. You do not need to provide explanations. Data From E4-5:

> The Dover Direct Insurance Agency began operations on June 1, 2018. In the month of June, the following transactions occurred: June 2: Dover Direct’s owner invested $80,000 (the par value of the stock) cash and acquired 4,000 shares of

> Using the information provided in E4-3, prepare Master Mind’s t-accounts for each transaction.

> Master Mind Games, Inc. is a new corporation started on January 1, 2018. The following transactions occurred during the first year of operations. a. On January 1, the owners invested a total of $50,000 (the par value of the stock) to start the company. I

> Using the adjusted trial balance for Diane’s Dairy Sales & Delivery in E4-22, prepare a single-step income statement, a statement of shareholders’ equity, and a balance sheet. Data from E4-22:

> Diane’s Dairy Sales & Delivery finished its first year of operations on December 31, 2018. After adjusting journal entries, the company presented the following adjusted trial balance. Using this trial balance, prepare Dianeâ&#

> Using the information provided in E4-18, prepare a worksheet including the columns for the unadjusted trial balance, adjustments, the adjusted trial balance, income statement, and balance sheet. Data From E4-18:

> When is financial information considered “understandable”?

> Using the information provided in E4-18: Required a. Prepare the necessary closing entries for Magic Cleaning Services at year-end. Omit explanations. b. Prepare the post-closing trial balance for Magic Cleaning Services at year-end. Data from E4-18:

> Using the information given in E4-1, prepare the journal entry for each transaction for Miller Manufacturing. Omit explanations. Data from E4-1: a. Bought office equipment with cash, $30,000. b. Bought supplies on credit from a vendor, $15,000. c. Sold

> Using the adjusted trial balance for Magic Cleaning Services in E4-18, prepare a single-step income statement, a statement of shareholders’ equity, and a balance sheet. Data from E4-18:

> Magic Cleaning Services (MCS) has a fiscal year-end of December 31. It is the first year of operations. As of year-end, MCS has the following unadjusted trial balance: In addition, it has not adjusted for the following transactions: •

> Using the information provided in E4-14, prepare a worksheet including the columns for the unadjusted trial balance, adjustments, the adjusted trial balance, income statement, and balance sheet. Data from E4-14: • Cash: $430,000 • Accounts Receivable: $

> Using the information provided in E4-14: Required a. Prepare the necessary closing entries for MPS, Inc. at December 31, 2018. Omit explanations. b. Prepare the post-closing trial balance for MPS, Inc. at December 31, 2018. Data from E4-14: • Cash: $430

> Using the information provided in E4-14: Required a. Prepare an unadjusted trial balance for MPS, Inc. as of December 31, 2018. b. Prepare an adjusted trial balance for MPS, Inc. as of December 31, 2018. Data From E4-14: • Cash: $430,000 • Accounts Rec

> MPS, Inc. has the following unadjusted account balances as of December 31, 2018, the company’s year-end: • Cash: $430,000 • Accounts Receivable: $2,000 • Prepaid Insurance: $14,000 • Prepaid Rent: $22,000 • Equipment: $60,000 • Accumulated Deprecia

> Using the information provided in E4-12, prepare an adjusted trial balance for Fanatical Fashions as of December 31, 2018. Data From E4-12:

> Fanatical Fashions, a department store, has the following unadjusted account balances as of December 31, 2018, the company’s year-end: At year-end, Fanatical Fashions makes necessary adjusting journal entries to properly record revenues

> What is the conceptual framework for financial reporting?

> Using the information provided in E4-6, prepare Dover Direct Insurance Agency’s unadjusted trial balance at June 30, 2018. Data from E4-6:

> Hartman Housewares Company began the current year with the following account balances: The following transactions were completed during the current year. a. Bought office equipment with cash, $10,000. b. Bought supplies on credit from a vendor, $5,000.

> The following transactions are taken from the books of Miller Manufacturing. a. Bought office equipment with cash, $30,000. b. Bought supplies on credit from a vendor, $15,000. c. Sold goods for cash, $40,000 (ignore the inventory and cost of goods sold

> Using the information in E4-22, prepare the post-closing trial balance for Diane’s Dairy Sales & Delivery. Data from E4-22:

> What is the objective of the statement of cash flows? Provide the Codification reference.