Question: Your client, Paul, owns a one-third

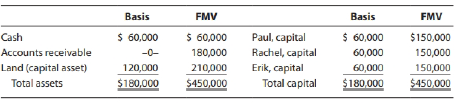

Your client, Paul, owns a one-third interest as a managing (general) partner in the service-oriented PRE LLP. He would like to retire from the lin1ited liability partnership at the end of 2019 and asks your help in structuring the buyout transaction. He expects that his basis in the LLP interest will be about $60,000 at that time.

Based on interim financial data and revenue projections, the LLP's balance sheet is expected to approximate the following at the end of the year.

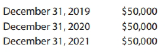

Although the LLP has some cash, the amount is not adequate to purchase Paul's entire interest in the current year. The LLP has proposed to pay Paul, in liquidation of his interest, according to the following schedule.

Paul has agreed to this payment schedule, but the parties are not sure of the tax consequences of the buyout and have temporarily halted negotiations to consult with their tax advisers. Paul has retained you to detern1ine the income tax ramifications of the buyout and to make sure he secures the most advantageous result available. Using the IRS Regulations governing partnerships, answer the following questions.

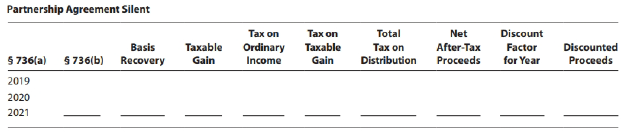

a. If the buyout agreement between Paul and PRE is silent as to the treatment of each payment, how will each payment be treated by Paul and the partnership?

b. As Paul's adviser, what payment schedule should Paul negotiate to minimize his current tax liability?

c. Regarding the LLP, what payment schedule would ensure that the remaining partners receive the earliest possible deductions?

d. Under the three alternatives in parts (a) to (c), what is the present value of Paul's after-tax cash received from the buyout'? Which alternative do you recommend to your client, Paul? Does this change your recommendations in parts (a) through (c)? Paul's Federal and state tax rate for capital gains is 25%, and his marginal combined state and Federal rate for ordinary income is 40%. Assume also that Paul typically earns 6% on his investments (after-tax discount rate), and that the first payment will be received one year from now (with the other payments one year apart). Use the present value tables in Appendix F. Note that each year's after-tax cash flow differs, so the after-tax payment does not constitute an annuity. Create a spreadsheet that summarizes the after-tax cash flows and present values of the three alternatives. You might use the format below for part (a), where the partnership agreement is silent, and then copy and modify the format for parts (b) and (c).

e. What additional planning opportunities might be available to the partnership'

> On July 20, 2017, Lilac Corporation purchased 25% of the Coffee Corporation stock outstanding. Lilac Corporation purchased an additional 40% of the stock in Coffee on March 22, 2018, and an additional 20% on May 2, 2018. On September 25, 2018, Lilac Corp

> Brown Corporation was organized seven years ago by Red Corporation (55%), Blue Corporation (35%), and Yellow Corporation (10%). Brown has been quite successful and now owns assets worth $12 million (basis of $4.4 million) with liabilities of $2 million.

> Through a ''Type A" reorganization, VizslaCo acquires 100% of Puli Corporation by exchanging 30% of its stock for all of Puli 's assets and liabilities. The VizslaCo stock was exchanged for all of the stock of the Puli shareholders. Then Puli liquidated.

> On December 31, 2017, Alpha Corporation, valued at $10 million, acquired BetaCo when BetaCo was valued at $5 n1illion. BetaCo holds a capital loss carryforward of $220,000 and excess business credits of $435,000. At the end of 2018, Alpha reports taxable

> Zeta Corporation is interested in acquiring Tau Corporation through a "Type A" reorganization on January 2 of the current year. Zeta is valued at $50 million and generates taxable incon1e of $5 million per year, whereas Tau is valued at $7 million and ho

> Sinopia completed a corporate restructuring transaction with Cyan on May 31 of the current year. Cyan distributed 30% of Sinopia's stock to its shareholders in exchange for all of their stock in Cyan. At the completion of the reorganization, Cyan's asset

> Assume the same facts as in Problem 56. Assume that Burgundy, Inc.'s annual guaranteed payment is increased to $120,000 starting on January 1, 2019, and the LLC's taxable income for 2018 and 2019 (after deducting Burgundy's guaranteed payment) is the sam

> Burgundy, Inc., and Violet are equal partners in the calendar year BV LLC. Burgundy uses a fiscal year ending April 30, and Violet uses a calendar year. Burgundy receives an annual guaranteed payment of $100,000 for use of capital contributed by Burgundy

> Graeter Corporation acquired all of the stock of Lesser Corporation in 2014, and the entities have filed a state and Federal consolidated income tax return ever since. Now an audit notice from the state unemployment tax administration makes it clear that

> Through an acquisitive "Type D" reorganization, Border, Inc., is merged into Collie Corporation on September 2 of the current calendar tax year. The Federal long-term tax-exempt rate for September is 3%. Border shareholders receive 70% of the Collie stoc

> Through a ''Type B" reorganization, Golden Corporation acquired 90% of RetrieverCo stock by October 2 of the current tax year ending December 31. At the time the 90%. was acquired, RetrieverCo was worth $800,000 and the Federal long-term tax-exempt rate

> Midori Corporation is a distiller of fine liqueurs. The market for this specialty product is thin but very lucrative. Midori wants to di versify its product line and is interested in acquiring Verdigris, which specializes in exotic teas and spices. Becau

> PorCo, a foreign corporation not engaged in a U.S. trade or business, received an $800,000 dividend fron1 USCo, a domestic corporation. Porco incurred $75,000 in expenses related to earning the di vidend. All of USCo's income is from U.S. sources. PorCo

> PorCo, a foreign corporation not engaged in a U.S. trade or business, received a $250,000 dividend from USCo, a domestic corporation. ForCo incurred $40,000 in expenses related to earning the di vidend. All of USCo's income is from U.S. sources. Porco is

> Bertha, a single individual, reports taxable income of $177,500, of which Communications $130,000 is attributable to an S corporation that provides consulting services, after paying wages of $72,000 to en1ployees (but not to Bertha). The entity made no a

> At the end of last year, June, a 30% partner in the four-person BJJM Partnership, had an outside basis of $75,000 in the partnership, including a $60,000 share of partnership debt. June's share of the partnership's§ 1245 recapture potential was $40,000.

> Diana, a partner in the cash basis HOA Partnership, has a one-third interest in partnership profits and losses. The partnership's balance sheet at the end of the current year is as follows. Diana sells her interest in the HOA Partnership to Kenneth at

> Assume in Problem 46 that Barry's partnership interest is not sold to another partner. Instead, the partnership makes a liquidating distribution of $90,000 cash to Barry, and the remaining partners assume his share of the liabilities. How much gain or lo

> Carter, Ltd., a Bohen1ia corporation, operates a sales branch in the United States that constitutes a U.S. trade or business. Rather than return the profits fron1 the sales branch to the Bohemia home office, Carter invests the profits in certificates of

> EarthTones, Inc., was a wholly owned subsidiary of Cutlinger Communications Corporation. Several years ago EarthTones acquired numerous oil leases and began exploration activities to determine their suitability for commercial exploitation. The tests were

> Skylar is ready to retire and \Va nts your professional opinion on the most advantageous way to dispose of a 400A. interest in STU LLC. Option # l. Skylar will immediately sell the LLC interest to Partner Tameeka for $300,000 cash. Skylar will then inves

> Continue with the GAB LLP and balance sheet shown in Problem 43, assuming instead that Gina sells her partnership interest to Jess for $140,000 of cash. a. What is the amount and character of Gina's gain? b. What deductions can be claimed by the LLP? c.

> The December 31 balance sheet of the GAB LLP read5 as follows. Capital is not a material income-producing factor for the LLP. Gina is an active (general) partner and owner of a 25% interest in the LLP's profits and capital. On December 31, Gina receive

> Damon owns a 200/o interest as a general partner in the Vermillion Partnership, which provides consulting services. The partnership distributes $60,000 cash to Damon in complete liquidation of his partnership interest. Damon's share of partnership unreal

> In 2015, Adrianna contributed land with a basis of $16,000 and a fair market value of $25,000 to the A&I Partnership in exchange for a 25% interest in capital and profits. In 2018, the partnership distributes this property to Isabel, also a 25% partner,

> Assume the san1e facts as in Problem 39, except that Jamie receives $2,000 cash and a car having a basis of $20,000 to the partnership and a fair market value of $30,000. a. How much loss, if any, may Jamie recognize on the distribution? b. What basis wi

> Jamie's basis in her partnership interest is $52,000. In a proportionate distribution in liquidation of the partnership, Jamie receives $2,000 cash and two parcels of land with bases of $10,000 and $18,000, respectively, to the partnership. The partnersh

> Paula's basis in her partnership interest is $60,000. In liquidation of her Decision Making interest, the partnership makes a proportionate distribution to Paula of $20,000 of cash and inventory (basis of $5,000 and value of $7,000). No •·other property"

> Assume the same fact5 as in Problem 36, except that Jerome's basis in the partnership is $90,000 instead of $50,000. a. How much gain or loss, if any, must Jerome recognize on the distribution? b. What basis will Jerome take in the inventory and land? c.

> Jeron1e's basis in his partnership interest is $50,000. Jerome receives a pro rata liquidating distribution consisting of $10,000 cash, land with a basis of $40,000 and a fair market value of $60,000, and his proportionate share of inventory with a basis

> The Cardinal Group had filed on a consolidated basis for several years which its wholly owned subsidiary, Swallow, Inc. TI1e group used a calendar tax year. On January 25, 2016, Heron acquired all of the stock of Cardinal, including its ownership in Swal

> In each of the following independent liquidating distributions in which the partnership also liquidates, prepare a Microsoft Excel spreadsheet to determine the amount and character of any gain or loss to be recognized by each partner and the basis of eac

> Use the assets and partners' bases from Problem 31. Assume that the partnership distributes all of its assets in a liquidating distribution. In deciding the allocation of assets, what issues should the partnership consider to minimize each partner's taxa

> Lonergan, Inc., a calendar year S corporation in Athens, Georgia, had a balance in AAA of $200,000 and AEP of $1 10,000 on December 31, 2018. During 2019, Lonergan, Inc., distributes $140,000 to its shareholders, while sustaining an ordinary loss of $120

> Assume the same facts as in Problem 31 , except that TAV distributes $100,000 of cash to Vincent, $50,000 (FMV) of marketable securities to Tyler, and $50,000 (FMV) of account5 receivable to Anita. In general terms, describe the tax result of the distrib

> Bertha, a single individual, reports taxable income of $177,500, of which $130,000 is attributable to an S corporation that provides consulting services, after paying wages of $72,000 to en1ployees (but not to Bertha). The entity made no acquisitions of

> At the beginning of the tax year, Melodie's basis in the MIP LLC was $60,000, including her $40,000 share of the LLC's liabilities. At the end of the year, MlP distributed to Melodie cash of $10,000 and inventory (basis of $6,000, fair market value of $1

> Cari Hawkins is a 50% partner in the calendar year Hawkins-Henry Partnership. On January 1, 2018, her basis in her partnership interest is $160,000. The partnership has no taxable income or loss for the current year. In a current distribution on December

> Assume the facts of Problem 27. For each of parts (a) through (d) considered Decision Making independently, are additional planning opportunities available to the partnership to maximize its inside basis in its assets' If so, by how much can the basis be

> In each of the following independent cases, indicate: • Whether the partner recognizes gain or loss. • Whether the partnership recognizes gain or loss. • The partner's adjusted basis for the property distributed. • The partner's outside basis in the part

> Honk, Inc., a U.S. corporation, purchases weight-lifting equipment for resale from HiDisu, a Japanese corporation, for 6o million yen. On the date of purchase, 110 yen is equal to SI U.S. (¥110:$1). The purchase is made on December 15, 2018, with payment

> Hatvaii Corporation, which is owned equally by two brothers and their younger sister, has been in the business of growing coffee and onions for the last 10 years. Lately, the brothers have been disagreeing regarding the management, operations, and expans

> LearCo, a non-U.S. conglomerate, generates $4 billion in gross receipts annually. Its U.S. subsidiary, KingCo, accounts for $750 million of the annual gross receipts (and its average annual gross receipts for the last three years is $820 million). KingCo

> Nye Tools, incorporated in 2005, makes tools and devices for the automotive industry. The original shareholders were Andre (700 shares) and his brother Roscoe (300 shares). In 2010, Andre transferred 100 shares to his wife and Roscoe sold 50 shares to a

> Shelly Zumaya (2220 East Hennepin Avenue, Minneapolis, MN Communications 55413) is the president and sole shareholder of Kiwi Corporation (stock basis of Critical Thinking $400,000). Incorporated in 2007, Kiwi Corporation's sole business has consisted of

> Your firm has a new individual client, Carla Navarro, who has been assigned to you for preparation of the current year's tax return. Upon review, of Carla's tax returns from prior years, you notice that she reported a large capital gain from a stock rede

> TAN LP was formed as a limited partnership by a corporate general partner and nine individual limited partners to own and operate rental real estate. The LP originally acquired commercial real estate in six locations. In the early years, property values

> The accrual basis Four Winds Partnership owned and operated three storage facilities in Milwaukee, Wisconsin. The partnership did not have a § 754 election in effect on March 1, 2018, when partner Taylor Barnes sold her 25% interest to Patric

> Which of the following statements is not true for tax years beginning after 2017? a. Affiliated corporations that file consolidated returns can take a l00% dividends received deduction. b. The dividends received deduction for a small investment in an unr

> The dividends received deduction (ORD) is a tax deduction that may be taken by which of the following? a. An individual b. An S corporation c. A partnership d. A C corporation

> Determine whether the following transactions are taxable. If a transaction is not taxable, indicate what type of reorganization is effected, if any. a. AlphaPsi Corporation owns two lines of business that it has conducted for the last eight years. For li

> Before the provision for Federal income tax, Karas Corporation had book income of $400,000 for the current year. The book income included $100,000 of dividends received from a 15% owned domestic corporation. What was Karas Corporation's taxable income fo

> Parent Corp. owns 40% of Sub Corp. In the current year, Parent has gross income of $43,000 and allowable deductions of $30,000 before considering any dividends received deduction (ORD). Included in the $43,000 gross income is $8,000 of dividends from Sub

> Provide the information required to complete the following chart.

> Indicate whether each of the following would make good consolidated return partners in computing the affiliated group's Federal income tax. Explain why or why not. a. ParentCo would like to file on a consolidated basis with SubOne because the subsidiary

> Indicate whether each of tl1e following would make good consolidated return partners in computing the affiliated group's Federal income tax. Explain why or why not. a. SubCo has a number of appreciated assets that it wants to sell to its parent, Huge Cor

> Describe the various types of event5 that can cause a partnership termination.

> Who makes the optional adjustment-to-basis election? How is the election made? What is its effect on future years? Are there situations in which the partnership would not make the election?

> What tax consequences result from the death of a partner? What collateral issues might arise?

> When a partnership interest is sold during the partnership's taxable year, how is the income allocated between the buying partner and selling partner? When is the income reported?

> Distinguish between the treatment of§ 736 income and property payments. What are the tax consequences of such payments to the retiring partner, the remaining partners, and the partnership?

> Use a timeline to diagram the gain/ loss recognition by this affiliated group. • Year 1: SubCo purchases an asset for $400. • Year 3: SubCo sells the asset to Parent for $300. • Year 4: Parent sells the asset to Stranger (not an affiliate) for $240.

> What issues arise if a partner contributes appreciated property to a partnership and other appreciated property is later distributed to that partner?

> In working as the tax consultant for LargeCo, Megan discovers that for the first time, the corporation is eligible to form a consolidated group for filing its Federal corporate income tax returns. List two or more of the events that likely have occurred

> Which of these taxes may be incurred by an S corporation? a. Corporate income tax. b. Tax on certain built-in gains. c. Property tax assessed by the county.

> The Pelican Group cannot decide whether to start to file on a consolidated basis for Federal income tax purposes, effective for its tax year beginning January 1, 2018. Its computational study of die effects of consolidation is taking longer than expected

> You are making a presentation to the board of directors of HugeCo about the merits of acquiring Bitty, Ltd., an important supplier. One board member, knowing that you are a tax specialist, asks you to list some of the nontax reasons to make the acquisiti

> Continue with the facts presented in Question 7. In addition, assume that Critical Thinking Brown Corporation has a history of making large, continuous charitable contributions that are important in its community. In the next three years, Brown's largest

> Black, Brown, and Red corporations are considering a corporate restructuring that would allow them to file Federal income tax returns on a consolidated basis. Black holds significant NOL carryforwards from several years ago. Brown always has been profita

> List the structural and compliance requirements under Federal income tax law that must be met before a parent and its affiliates are allowed to file on a consolidated basis. Consider only the requirements for the group to file its first consolidated retu

> The local CPA Society is presenting its annual tax conference. Most of the Communications attendees will be career tax professionals who work with smaller clients. You have been asked to submit an outline for your talk "When to Use a Consolidated Tax Ret

> Financial accounting n1les do not always match the tax treatment of transactions involving groups of U.S. corporations. List at least two areas where tax and accounting rules differ when groups of affiliated corporations are involved.

> Use a timeline to diagram the gain/ loss recognition by this affiliated group. • Year 1: SubCo purchases a nondepreciable asset for $400. • Year 3: SubCo sells the asset to Parent for $575. • Year 4: Parent sells the asset to Stranger (not an affiliate)

> The tax rules governing the Federal consolidated tax return elections are largely in the form of Treasury Regulations and IRS n 11ings. Why' When is the split between the legislative and executive branches in tax-writing responsibilities: a. Appropriate?

> Friar Corporation is the parent entity in a Federal consolidated group for corporate income tax purposes. It has a $3 million basis in the stock of its wholly owned subsidiary, Abbey, Ltd. This year Abbey reports a $4 million taxable loss. a. What is Fri

> Explain how the earnings and profits (E & P) of the acquired corporation are treated by the successor corporation when the E & P balance is positive. When the E & P balance is negative. How are earnings and profits treated in a divisive "Type D" reorgani

> Explain what a corporation is trying to accomplish when using a "Type E" Critical Thinking reorganization. When using a "Type F" reorganization.

> Briefly describe the judicial doctrines of sound business purpose, continuity of business enterprise, and the step transaction doctrine.

> What is the difference between a split-up, a split-off, and a spin-off?

> What advantage does a '·Type C" reorganization have over a "Type A" reorganization with regard to transferred liabilities? What disadvantage does a "Type C" reorganization have over a "Type A" reorganization with regard to transferred liabilities?

> Explain the stock and control requirements in a "Type B" reorganization. After a '·Type B" reorganization, what is the relationship between the corporations participating in the restructuring'

> What is the difference between a "Type A" merger and a '·Type A" consolidation?

> In general, what are the tax consequences surrounding the sale of§ 306 stock?

> Intercompany transactions of a consolidated group can be subject to a Decision Making "matching rule" and an "acceleration rule." a. Define both terms. b. As a tax planner structuring an intercompany transaction, when would it be beneficial to use either

> Donna and Steven own all the stock in Pink Corporation (E & P of Critical Thinking $2 million). Each owns 1,000 shares and has a basis of $75,000 in the shares. Donna and Steven are married and have two n1inor children. Pink Corporation has had considera

> Lauren owns 600 shares in Viridian Corporation. The remaining 400 shares of Viridian are owned by Lauren's son, Brett. Currently, Lauren is both president and chair of the board of directors of Viridian Corporation. If Viridian redeems Lauren's 600 share

> To qualify as a partial liquidation, a distribution must not be essentially equivalent to a dividend. Discuss how this requirement is satisfied.

> Brown Corporation operates several trades and businesses. In the current year, Brown discontinues the operation of one of its trades and businesses. Brown is considering distributing to its shareholders either the assets of the discontinued business or t

> Why should the acquiring corporation perform present value calculations when it is planning to merge with a target holding business credit carryforwards?

> The computational method of Exhibit 8.2 indicates that consolidated taxable Communications income includes a number of group items where limitations are applied on an aggregate basis. In no more than two slides, list as many group items as you can.

> The consolidated return Regulations employ the "SRLY" rules to limit the losses a parent can claim with respect to a newly acquired subsidiary. Explain the tax policy behind the SRLY rules. Describe how they affect the timing of loss deductions after an

> Mini Corporation brought a $7 million NOL carryforward into the Mucho Group of corporations that elected to file on a consolidated basis as of the beginning of this year. Combined results for the year generated $15 million taxable income, $2 million of w

> Oudine the process by which a consolidated group computes its Federal taxable income. Your description should match the approach taken in Exhibit 8.2.

> Ryce contributes non-depreciable property with an adjusted basis of $60,000 and a fair market value of $95,000 to the Montgomery Partnership in exchange for a one-half interest in profits and capital. In the next tax year, when the property's fair market

> Spinone Corporation directs its sole shareholder, James, to exchange all of his common stock valued at $200,000 (basis of $50,000) for $100,000 of common stock, $70,000 of preferred stock, and $30,000 in cash. In addition, Spinone directs its sole bondho

> The Parent consolidated group reports the following results for the tax year. a. What is the group's consolidated taxable income and consolidated tax liability' b. If the Parent group has consented to the relative taxable income method, how will the co

> Penguin LLC operates a large apparel store with several employees and substantial debt. Each LLC member is active in the business and receives compensation from the LLC. The LLC invests it5 excess cash in government and corporate bonds, blue chip stocks,

> LO.S Park Corporation distributes its shoe manufacturing line of business to the newly created ShoeBiz Corporation in a transaction qualifying as a '"Type D" spin-off reorganization. Before the distribution, Park is worth $4,000,000 and its E & P balance

> Blush Corporation owns long-term bonds (basis of $1.3 million) of its subsidiary, Brass Corporation, that were acquired at a discount. Upon liquidation of Brass pursuant to § 332, Blush receives a distribution of $1.5 million, the face amount of the bond

> The stock of Quail Corporation is held as follows: 85% by Pheasant Corporation and 15% by Gisela, an individual. Quail Corporation is liquidated in December of the current year pursuant to a plan adopted earlier in the year. At the time of its liquidatio