Question: A simple trust has the following receipts

A simple trust has the following receipts and expenditures for 2017. The trust instrument is silent with respect to capital gains, and state law concerning trust accounting income follows the Uniform Act. Assume the trustee’s fee is charged equally to income and to principal.

Corporate bond interest……………$40,000

Tax-exempt interest…………………….9,000

Long-term capital gain……………….5,000

trustee’s fee………………………………2,000

Distribution to beneficiary………..48,000

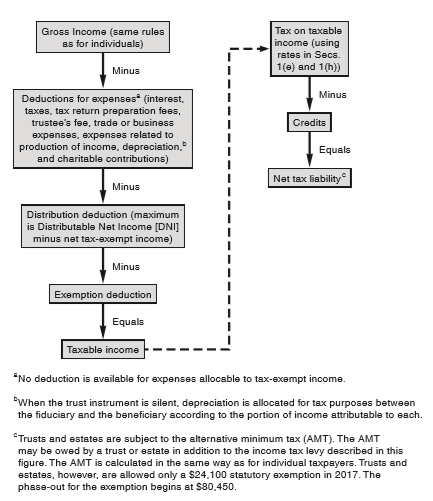

a. What is the trust’s taxable income under the formula approach of Figure C:14-1?

b. What is the trust’s tax liability?

Figure C:14-1?

Transcribed Image Text:

Tax on taxable Gross Income (same rules as for individuals) income (using rates in Secs. 1(e) and 1(h)) Minus Minus Deductions for expenses (interest, taxes, tax return preparation fees, trustee's fee, trade or business Credits expenses, expenses related to production of income, depreciation. and charitable contributions) Equals Net tax liability Minus Distribution deduction (maximum is Distributable Net Income [DNI] minus net tax-axempt income) Minus Exemption deduction Equals Taxable income "No deduction is available for expenses allocable to tax-exempt income. When the trust instrument is silent, depreciation is allocated for tax purposes between the fiduciary and the beneficiary according to the portion of income attributable to each. "Trusts and estates are subject to the alternative minimum tax (AMT). The AMT may be owed by a trust or estate in addition to the income tax levy described in this figure. The AMT is calculated in the same way as for individual taxpayers. Trusts and estates, however, are allowed only a $24,100 statutory exemption in 2017. The phase-out for the exemption begins at $80,450.

> What course(s) of action is (are) available to a taxpayer upon receipt of the following notices: a. The 30-day letter? b. The 90-day letter? c. IRS rejection of a claim for a refund?

> The IRS informs Brad that it will audit his current year employee business expenses. Brad just met with a revenue agent who contends that Brad owes $775 of additional taxes. Discuss briefly the procedural alternatives available to Brad.

> a. Through what programs has the IRS gathered data to develop its DIF statistical models? b. How do these programs differ? c. How has the IRS used these programs to select returns for audit?

> Under the AICPA’s Statements on Standards for Tax Services, what is the tax practitioner’s professional duty in each of the following situations? a. Client erroneously deducts $5,000 (instead of $500) on a previous year’s tax return. b. Client refuses

> List five IRC penalties that can be imposed on tax return preparers. Does the IRC require a CPA to verify the information a client furnishes?

> What is the principal purpose of the innocent spouse provisions?

> In general, when does the limitations period for tax returns expire? List four exceptions to the general rule.

> Explain why the government might bring criminal fraud charges against a taxpayer under Sec. 7206 instead of Sec. 7201. Compare the maximum penalties imposed under Secs. 7201, 7203, and 7206.

> A trust instrument provides that, for life, Irene is entitled to receive distributions of income only and Beth is to receive the remainder interest. The trust sells property at a gain. Income and corpus are classified in accordance with the Uniform Act.

> Distinguish between the circumstances that give rise to the civil fraud penalty and those that give rise to the negligence penalty.

> Upon audit, the IRS determines Maria’s tax liability to be $40,000. Maria agrees to pay a $7,000 deficiency. Will she necessarily have to pay a substantial understatement penalty? Explain.

> Assume that a taxpayer owes additional taxes as a result of an audit. Give two reasons why the IRS might not impose a substantial understatement penalty on the additional amount owed.

> This year, Ark Corporation acquired substantially all the voting stock of BioTech Consultants, Inc. for cash. Subsequent to the acquisition, Ark’s chief financial officer, Jonathan Cohen, approached Edith Murphy, Ark’s tax advisor, with a question: Could

> A long-time client, Horace Haney, wishes to avoid currently recognizing revenue in a particular transaction. A recently finalized Treasury Regulation provides that, in such a transaction, revenue should be currently recognized. Horace insists that you re

> Your manager advises you that Sam Skinner, a long-time client, died on February 13 of the current year, survived by his wife Sue Skinner and several adult children. The Skinners are residents of a non-community property state. Earlier in the current year

> A client, Sam Curren, established the Curren Trust earlier this year. In addition to stocks and cash, the trust’s assets include a life insurance policy on the life of Mr. Curren. The trust is both the owner and beneficiary of the policy. The insurance p

> Ernest Jacobson created an irrevocable trust in February of last year and designated his friend Eileen Frazier as trustee. Eileen is empowered, for life, to distribute such income as she deems appropriate to herself each year. Any income not distributed

> Roy Ritter died two years ago. Among the assets he owned were Ritter Ranch, a cattle ranch consisting of 12,220 acres in Texas. In accordance with Roy’s will, the ranch along with stocks producing substantial dividends passed to a testamentary trust (the

> You are in the process of doing income tax projections for the Estate of Esther Simmons, who died January 3, 2017. The Estate has paid appraisal fees for having her real estate holdings appraised for estate tax valuation purposes, probate court fees, and

> A client asks about the relevance of state law in classifying items as principal or income. Explain the relevance.

> You are preparing a current year (Year 2) individual tax return for Robert Lucca, a real estate developer and long-time client. While preparing Robert’s individual tax return you learn that last year (Year 1) he received interest income from a trust his

> Arthur Rich, a widower, is considering setting up an irrevocable trust (or trusts) with a bank as trustee for his three minor children. He will fund the trust at $900,000 (or $300,000 each in the case of three trusts). A friend suggested that he might wa

> At what rate is the penalty for underpaying estimated taxes imposed? How is the penalty amount calculated?

> Briefly explain the rules for determining the interest rate charged on tax underpayments. Is this rate the same as that for overpayments? In which months might the rate(s) change?

> A client believes that obtaining an extension for filing an income tax return would give him additional time to pay the tax at no additional cost. Is the client correct?

> Cate Cole died in 2015, and her will left her entire estate in equal shares to her two adult children, Calvin and Corrine. Both children anticipate being in the top income tax bracket for at least ten years. The Cate Cole Estate is a calendar year taxpay

> Carla plans to create a trust and transfer to it oil and gas properties producing royalty income. She will transfer no other properties. The sole income beneficiary of the trust will be Carla’s son, Marshall, who is in the top marginal income tax bracket

> Glorietta Trust is an irrevocable discretionary trust funded by Grant Glorietta. The discretionary income beneficiary for life is Grant’s son, Gordon Glorietta (single). Gordon is a partner in a partnership in which he materially participates, and he has

> Dana Dodson died October 31, 2016, with a gross estate of $6.7 million, debts of $200,000, and a taxable estate of $6.5 million. Dana made no taxable gifts. All of her property passed under her will to her son, Daniel Dodson. The estate chose a June 30 y

> Joan died April 17, 2016. Joan’s executor chose March 31 as the tax year end for the estate. The estate’s only beneficiary, Kathy, reports on a calendar year. The executor of Joan’s estate makes the following distributions to Kathy: June 2016 $ 5,000 Aug

> List some common examples of principal and income items under the Uniform Act.

> In the current year, Maddox Trust, a complex trust, distributed an asset with a $42,000 adjusted basis and a $75,000 FMV to its sole beneficiary, Marilyn Maddox-Mason. The trustee elected to recognize gain on the distribution. Marilyn received no other d

> Julie Brown died on May 27 of the current year. She was employed before her death at a gross salary of $4,000 per month. Her pay day was the last day of each month, and her employer did not pro rate her last monthly salary payment. She owned preferred st

> The following items are relevant for the first income tax return for the Ken Kimble Estate. Mr. Kimble, a cash method of accounting taxpayer, died on July 1, 2017. Dividends………………………………………………………………………………..$10,000 Interest on corporate bonds…………………………………

> Refer to Problem C:14-45. Explain how your answers would change for each independent situation indicated below: a. At the end of the trust term, the property passes instead to Holly’s nephew Nathan. b. Holly creates the trust in October 2017 for a term

> Holly funded the Holly Marx Trust in January 2017. The entire trust income is payable to her adult son, Jack for 20 years. At the end of the twentieth year, the trust assets are to pass to Holly’s husband. In the current year, the trust realizes $30,000

> A revocable trust created by Amir realizes $30,000 of rental income and a $5,000 capital loss. It distributes $22,000 to Ali, its beneficiary. How much income is taxed to the trust, the grantor, and the beneficiary?

> Refer to Problem C:14-42. How would your answer change if instead the trust were a complex trust that makes no distributions in 2016 and 2017? Assume the trust earns $8,000 of corporate bond interest income each year. From problem 42: A simple trust had

> A simple trust had a long-term capital loss of $10,000 for 2016 and a long-term capital gain of $15,000 for 2017. Its net accounting income and DNI are equal. Explain the tax treatment for the 2016 capital loss assuming the trust is in existence at the e

> The George Grant Trust reports the receipts and expenditures listed below. What are the trust’s deductible expenses? U.S. Treasury interest…………………..$25,000 Rental income………………………………..9,000 Interest from tax-exempt bonds……..6,000 Property taxes on rental

> Refer to Problem C:14-39. How would your answers change if the trust were a discretionary trust that distributes $12,000 to its beneficiary, Julio? From problem 39: Assume the trustee must pay out all of its income currently to its beneficiary, Julio. a

> Explain to a client the significance of the income and principal categorization scheme used for fiduciary accounting purposes.

> Refer to Problem C:14-38. Assume the trustee must pay out all of its income currently to its beneficiary, Julio. a. What is the deductible portion of the trustee’s fee? b. What is the trust’s taxable income exclusive of the distribution deduction? c.

> The Trotter Trust has the receipts and expenditures listed below for the current year. Assume the Uniform Act governs an item’s classification as principal or income. The trustee’s fee is charged one half to principal and one-half to income. What is the

> A complex trust is required to distribute $20,000 and $30,000 annually to its beneficiaries, Bart and Thelma, respectively. In addition, it can distribute other amounts at its discretion. In Year 1, it had DNI of $62,000 and distributed $20,000 to Bart a

> Refer to Problem C:14-35. How would your answer change if the trust instrument required that $10,000 per year be distributed to Sandy, and the trustee also made discretionary distributions of $60,000 to Roy and $30,000 to Sandy with separate shares not r

> A complex trust is authorized to make discretionary distributions of income and principal to its two beneficiaries, Roy and Sandy. Separate shares are not required. For the current year, it has DNI and net accounting income of $80,000, all from taxable s

> A trust has net accounting income of $24,000 and incurs a trustee’s fee of $1,000 in its principal account. What is its distribution deduction under the following situations: a. It distributes $24,000, and all of its income is from taxable sources. b.

> During the current year, a simple trust has the following receipts and expenditures. The Uniform Act governs the accounting classification. Corporate bond interest…………..$60,000 Long-term capital gain……………..20,000 Trustee’s fees…………………………….3,000 a. What

> Refer to Problem C:14-30. How would your answer to Part a change if the trust in addition received $8,000 interest from tax-exempt bonds, and it distributed $28,000 instead of $20,000? Data From problem 30: A simple trust has the following receipts and

> A simple trust has the following receipts and expenditures for the current year. The trust instrument classifies gains, losses, and trustee’s fees as part of principal. Dividends……â€&b

> List some major differences between the taxation of individuals and trusts.

> Suellen Symmes died on January 15, 2017. Her estate elected a November 30 year end. The executor projects that the estate will receive interest income of $50,000 by November 30, 2017, and will have no other gross income. In addition, it will have no dedu

> A complex trust has taxable income of $29,900 in 2017. The $29,900 includes $5,000 of rental income and $25,000 of taxable interest income, reduced by the $100 personal exemption. The trust makes no distributions during the year. What is the trust’s tota

> Raj Kothare funded an irrevocable simple trust in May of last year. The trust benefits Raj’s son for life and grandson upon the son’s death. One of the assets he transferred to the trust was Webbco stock, which had a $35,000 FMV on the transfer date. Raj

> For the first five months of its existence (August through December 2017), the Estate of Amy Ennis had gross income (net of expenses) of $7,000 per month. For January through July 2018, the executor estimates that the estate will have gross income (net o

> Art Rutter sold an apartment building in May 2017 for a small amount of cash and a note payable with payments beginning in 2018. Principal and interest payments are due annually on the note in April of 2018 through 2022. Art died in August 2017. He wille

> a. When are fiduciary income tax returns due? b. Must estates and trusts pay estimated income taxes?

> What is the benefit of the 65-day rule?

> Amelia, a widow, is in the top marginal income tax bracket and has considerably more income than she can spend. She is considering creating a trust for the benefit of her adult son Jason but is reluctant to make it irrevocable, at least presently. If she

> Can a client escape the grantor trust rules by providing in a trust instrument that income is payable to a nephew for 20 years and that the trust assets pass at the end of 20 years to the client’s spouse?

> Describe three situations that cause trusts to be subject to the grantor trust rules.

> Given the tax rate schedule for trusts, what reasons (tax and/or nontax) exist today for creating a trust?

> a. Describe to a client what income in respect of a decedent (IRD) is. b. Describe to the client one tax disadvantage and one tax advantage that occur because of the classification of a receipt as IRD.

> Determine the accuracy of the following statement: Under the tier system, beneficiaries who receive mandatory distributions of income are more likely to be taxed on the entire distributions they receive than are beneficiaries who receive discretionary di

> Describe the tier system for taxing trust beneficiaries.

> The Mary Morgan Trust, a simple trust governed by the Uniform Act, sells one capital asset in the current year. The sale results in a loss. a. When will the capital loss produce a tax benefit for the trust or its beneficiary? Explain. b. Would the resu

> When does the NOL of a trust or estate produce tax deductions for the beneficiaries?

> a. Describe the shortcut approach for verifying that the amount calculated as a simple trust’s taxable income is correct. b. Can a shortcut verification process be applied for trusts and estates that accumulate some of their income? Explain.

> The IRS is disputing a deduction reported on your Year 1 tax return, which you filed on April 12 of Year 2. On April 4 of Year 5, the IRS audit agent asks you to waive the statute of limitations for the entire return so as to give her additional time to

> Harold and Betty, factory workers who until this year prepared their own individual tax returns, purchased an investment from a broker last year. Although they reviewed the prospectus for the investment, the broker explained the more complicated features

> Art is named executor of the Estate of Stu Stone, his father, who died on February 3 of the current year. Art hires Larry to be the estate’s attorney. Larry advises Art that the estate must file an estate tax return but does not mention the due date. Art

> Assume that a trust collects rental income and interest income on tax-exempt bonds. Will a portion of the rental expenses, such as repairs, have to be allocated to tax-exempt income and thereby become nondeductible? Explain.

> Five years ago, Spyros Dietrich wanted to sell IMPEXT, Inc., his wholly owned import export business. He also wanted to avoid recognizing the substantial gain that would result from his selling his IMPEXT shares on the open market. Spyros’ basis in the s

> A colleague comes to you with the following investment proposal that he would like to market for Client: • Client obtains cash of $60,000 from Bank. • Bank loan agreement specifies that $40,000 of this amount represents principal; the remaining $20,

> On April 15 of Year 2, Adam and Renee Tyler jointly filed a Year 1 return that reported AGI of $68,240 ($20,500 attributable to Renee) and a tax liability of $3,050. They paid this amount in a timely fashion. On their return, the Tylers claimed a $18,405

> Gene employed his attorney to draft identical trust instruments for each of his three minor children: Judy (age 5), Terry (age 7), and Grady (age 11). Each trust instrument names the Fourth City Bank as trustee and states that the trust is irrevocable. I

> The IRS audits Tan’s individual return for the current year and assesses a $9,000 deficiency, $2,800 of which results from Tan’s negligence. What is the amount of Tan’s negligence penalty? Does the penalty bear interest?

> Ed’s tax liability for last year was $24,000. Ed projects that his tax for this year will be $34,000. Ed is self-employed and, thus, will have no withholding. His AGI for last year did not exceed $150,000. How much estimated tax should Ed pay for this ye

> Ted’s current year return reported a tax liability of $1,800. Ted’s wage withholding for the current year was $2,200. Because of his poor memory, Ted did not file his current year return until May 28 of the following year. What penalties (if any) does Te

> Amy files her current year tax return on August 13 of the following year. She pays the amount due without requesting an extension. The tax shown on her return is $24,000. Her current year wage withholding amounts to $15,000. Amy pays no estimated taxes a

> Which of the following communications between an accountant and client are privileged? a. For tax preparation purposes only, client informs the accountant that she contributed $10,000 to a homeless shelter. b. Client informs the accountant that he forg

> Your client, Envirocosmetics, recently has filed for bankruptcy. In the course of bankruptcy proceedings, you (a) prepare a plan of reorganization that alters the rights of preferred stockholders, (b) notify the Envirocosmetics’ creditors of an impending

> a. Are net accounting income and DNI always the same amount? b. If not, explain a common reason for a difference. c. Are capital gains usually included in DNI?

> Your client, Meade Technical Solutions, proposes to merge with Dealy Cyberlabs. In advance of the merger, you (a) issue an opinion concerning the FMV of Dealy, (b) prepare pro forma financials for the merged entity to be, (c) draft Meade shareholder reso

> Maria, a calendar year taxpayer, files her Year 1 individual return on March 12 of Year 2 and pays the amount of tax due. She later discovers that she overlooked some deductions that she should have reported on the return. By what date must she file a cl

> Frank, a calendar year taxpayer, reports $100,000 of gross income and $60,000 of taxable income on his Year 1 return, which he files on March 12 of Year 2. He fails to report on the return a $52,000 long-term capital gain and a $10,000 short term capital

> Luis, a bachelor, owes $56,000 of additional taxes, all due to fraud. a. What is the amount of Luis’ civil fraud penalty? b. What criminal fraud penalty might the government impose on Luis under Sec. 7201?

> Refer to Part c of the previous problem. Assume that Carmen discloses her position, which is not frivolous. How would your original answer change assuming the item does not involve a tax shelter? From problem 50 Part C: c. How would your answer to Parts

> The IRS audits Pearl’s current year individual return and determines that, among other errors, she negligently failed to report dividend income of $8,000. The deficiency relating to the dividends is $2,240. The IRS proposes an additional $12,000 deficien

> Amir’s projected tax liability for the current year is $23,000. Although Amir has substantial dividend and interest income, he does not pay any estimated taxes. Amir’s withholding for January through November of the current year is $1,300 per month. He w

> Pam’s prior year (Year 1) income tax liability was $23,000. Her current year (Year 2) AGI did not exceed $150,000. On April 2 of next year (Year 3), Pam, a calendar year taxpayer, timely files her current year individual return, which indicates a $30,000

> Refer to the preceding problem. Assume that Ed expects his income for this year to decline and his tax liability for this year to be only $15,000. What minimum amount of estimated taxes should Ed pay this year? What problem will Ed encounter if he pays t

> Refer to the preceding problem. a. Will Carl owe interest? If so, on what amount and for how many days? Assume that any interest period begins on April 16 of a non–leap year. b. Assume the applicable interest rate is 6%. Compute Carl’s interest payable

> A client inquires about the significance of distributable net income (DNI). Explain.

> Carl’s tax liability for last year was $19,000, and his AGI did not exceed $150,000. Carl requests an automatic extension for filing his current year individual return but does not pay any additional tax with his extension request. By April 15 of the fol

> Bob, a calendar year taxpayer, files his current year individual return on July 17 of the following year without having requested an extension. His return indicates an amount due of $5,100. Bob pays this amount on November 3 of the following year. What a

> The taxes shown on Hu’s tax returns for Year 1 and Year 2 are $5,000 and $8,000, respectively. Hu’s wage withholding for Year 2 was $5,200, and she paid no estimated taxes. Hu filed her Year 2 return on March 18 of Year 3, but she did not have sufficient

> In the preceding problem, how would your answers change if Amy instead files her return on June 18 and, on September 8 pays the amount due? Assume her wage withholding tax amounts to a. $19,000 b. $24,500 c. How would your answer to Part a change if A

> Which of the following communications between an accountant and client are not privileged? a. In a closed-door meeting, the accountant orally advises the client to set up a foreign subsidiary to shift taxable income to a low-tax jurisdiction. b. In a c