Question: Fran Corporation acquired all outstanding $10 par

Fran Corporation acquired all outstanding $10 par value voting common stock of Brey Inc. on January 1, 20X9, in exchange for 25,000 shares of its $20 par value voting common stock. On December 31, 20X8, Fran’s common stock had a closing market price of $30 per share on a national stock exchange. The acquisition was appropriately accounted for under the acquisition method. Both companies continued to operate as separate business entities maintaining separate accounts for its investment in Brey stock using the fully adjusted equity method (i.e., adjusting for unrealized intercompany profits).

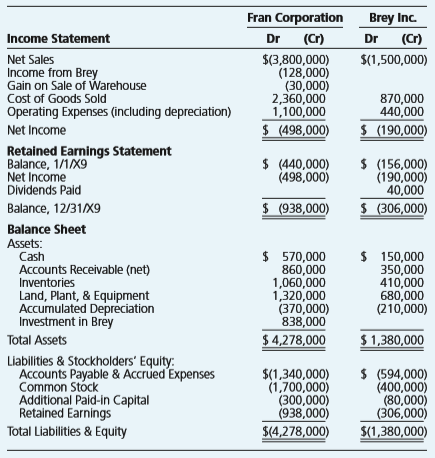

On December 31, 20X9, the companies had condensed financial statements as follows:

Additional Information:

No changes occurred in the Common Stock and Additional Paid-in Capital accounts during 20X9 except the one necessitated by Fran’s acquisition of Brey.

At the acquisition date, the fair value of Brey’s machinery exceeded its book value by $54,000. The excess cost will be amortized over the estimated average remaining life of six years. The fair values of all of Brey’s other assets and liabilities were equal to their book values. At December 31, 20X9, Fran’s management reviewed the amount attributed to goodwill as a result of its purchase of Brey’s common stock and concluded an impairment loss of $35,000 should be recognized in 20X9. During 20X9, Fran purchased merchandise from Brey at an aggregate invoice price of $180,000, which included a 100 percent markup on Brey’s cost. At December 31, 20X9, Fran owed Brey $86,000 on these purchases, and $36,000 of this merchandise remained in Fran’s inventory.

Required:

Develop and complete a consolidation worksheet that would be used to prepare a consolidated income statement and a consolidated retained earnings statement for the year ended December 31, 20X9, and a consolidated balance sheet as of December 31, 20X9. List the accounts in the w orksheet in the same order as they are listed in the financial statements provided. Formal consolidated statements are not required. Ignore income tax considerations. Supporting computations should be in good form.

Transcribed Image Text:

Fran Corporation Brey Inc. Income Statement Dr (Cr) Dr (Cr) $(3,800,000) (128,000) (30,000) 2,360,000 1,100,000 $ (498,000) $(1,500,000) Net Sales Income from Brey Gain on Sale of Warehouse Cost of Goods Sold Operating Expenses (including depreciation) Net Income 870,000 440,000 $ (190,000) Retained Earnings Statement Balance, 1/1/X9 Net Income Dividends Paid $ (440,000) (498,000) $ (156,000) (190,000) 40,000 Balance, 12/31/X9 $ (938,000) $ (306,000) Balance Sheet Assets: Cash $ 570,000 860,000 1,060,000 1,320,000 (370,000) 838,000 $ 150,000 350,000 410,000 680,000 (210,000) Accounts Receivable (net) Inventories Land, Plant, & Equipment Accumulated depreciation Investment in Brey Total Assets $ 4,278,000 $ 1,380,000 Liabilities & Stockholders' Equity: Accounts Payable & Accrued Expenses Common Stóck Additional Paid-in Capital Retained Earnings Total Liabilities & Equity $(1,340,000) (1,700,000) (300,000) (938,000) $ (594,000) (400,000) (80,000) (306,000) $(4,278,000) $(1,380,000)

> Frazer Corporation purchased 60 percent of Minnow Corporation’s voting common stock on January 1, 20X1. On December 31, 20X5, Frazer received $210,000 from Minnow for a truck Frazer had purchased on January 1, 20X2, for $300,000. The truck is expected to

> Bowen Corporation owns 70 percent of Roan Corporation’s voting common stock. On March 12, 20X2, Roan sold land it had purchased for $140,000 to Bowen for $185,000. Bowen plans to build a new warehouse on the property in 20X3. Required: Give th

> Pam Corporation holds 70 percent ownership of Northern Enterprises. On December 31, 20X6, Northern paid Pam $40,000 for a truck that Pam had purchased for $45,000 on January 1, 20X2. The truck was considered to have a 15-year life from January 1, 20X2, a

> Power Corporation owns 75 percent of Swift Company’s stock. Swift provides health care services to its employees and those of Power. During 20X2, Power recorded $45,000 as health care expense for medical care given to its employees by Swift. Swift’s cost

> Huckster Corporation purchased land on January 1, 20X1, for $20,000. On June 10, 20X4, it sold the land to its subsidiary, Lowly Corporation, for $30,000. Huckster owns 60 percent of Lowly’s voting shares. Required: Give the worksheet consolidation

> Select the correct answer for each of the following questions. Upper Company holds 60 percent of Lower Company’s voting shares. During the preparation of consolidated financial statements for 20X5, the following consolidation entry wa

> Parent Company holds 90 percent of Sunway Company’s voting common shares. On December 31, 20X8, Parent recorded a loss of $16,000 on the sale of equipment to Sunway. At the time of the sale, the equipment’s estimated remaining economic life was eight yea

> Turner Company purchased 70 percent of Split Company’s stock approximately 20 years ago. On December 31, 20X8, Turner purchased a building from Split for $300,000. Split had purchased the building on January 1, 20X1, at a cost of $400,000 and used straig

> Newtime Products purchased 65 percent of TV Sales Company’s stock at underlying book value on January 1, 20X3. At that date, the fair value of the noncontrolling interest was equal to 35 percent of the book value of TV Sales. TV Sales reported shares out

> Grand Delivery Service acquired at book value 80 percent of the voting shares of Acme Real Estate Company. On that date, the fair value of the noncontrolling interest was equal to 20 percent of Acme’s book value. Acme Real Estate reported common stock of

> Norgaard Corporation purchased management consulting services from its 75 percent-owned subsidiary, Bline Inc. During 20X3, Norgaard paid Bline $123,200 for its services. For the year 20X4, Bline billed Norgaard $138,700 for such services and collected a

> Verry Corporation owns 75 percent of Spawn Corporation’s voting common stock. Verry reported income from its separate operations of $90,000 and $110,000 in 20X4 and 20X5, respectively. Spawn reported net income of $60,000 and $40,000 in 20X4 and 20X5, re

> Pastel Corporation acquired a controlling interest in Somber Corporation in 20X5 for an amount equal to its underlying book value. At the date of acquisition, the fair value of the noncontrolling interest was equal to its proportionate share of the book

> Kline Corporation holds 90 percent ownership of Andrews Company. On July 1, 20X3, Kline sold equipment that it had purchased for $30,000 on January 1, 20X1, to Andrews for $28,000. The equipment’s original six-year estimated total economic life remains u

> Stern Manufacturing purchased an ultrasound drilling machine with a remaining 10-year economic life from a 70 percent-owned subsidiary for $360,000 on January 1, 20X6. Both companies use straightline depreciation. The subsidiary recorded the following en

> Baywatch Industries has owned 80 percent of Tubberware Corporation for many years. On January 1, 20X6, Baywatch paid Tubberware $270,000 to acquire equipment that Tubberware had purchased on January 1, 20X3, for $300,000. The equipment is expected to hav

> Blank Corporation owns 60 percent of Grand Corporation’s voting common stock. On December 31, 20X4, Blank paid Grand $276,000 for dump trucks Grand had purchased on January 1, 20X2. Both companies use straight-line depreciation. The con

> On January 1, 20X7, Wainwrite Corporation sold to Lance Corporation equipment it had purchased for $150,000 and used for eight years. Wainwrite recorded a gain of $14,000 on the sale. The equipment has a total useful life of 15 years and is depreciated o

> Swanson Corporation purchased land from Clayton Corporation for $240,000 on December 20, 20X3. This purchase followed a series of transactions between Swanson-controlled subsidiaries. On February 7, 20X3, Sullivan Corporation purchased the land from a no

> Brown Corporation holds 70 percent of Transom Company’s voting common stock. On January 1, 20X2, Transom paid $300,000 to acquire a building with a 15-year expected economic life. Transom uses straight-line depreciation for all depreciable assets. On Dec

> Home Products Corporation, which sells a broad line of home detergent products, owns 75 percent of the stock of Level Brothers Soap Company. During 20X8, Level Brothers sold soap products to Home Products for $180,000, which it had produced for $120,000.

> Herb Corporation holds 60 percent ownership of Spice Company. Each year, Spice purchases large quantities of a gnarl root used in producing health drinks. Spice purchased $150,000 of roots in 20X7 and sold $40,000 of these purchases to Herb for $60,000.

> Klon Corporation owns 70 percent of Brant Company’s stock and 60 percent of Torkel Company’s stock. During 20X8, Klon sold inventory purchased in 20X7 for $100,000 to Brant for $150,000. Brant then sold the inventory at its cost of $150,000 to Torkel. Pr

> The December 31, 20X8, balance sheets for Doorst Corporation and its 70 percent-owned subsidiary Hingle Company contained the following summarized amounts: Boorst acquired the shares of Hingle Company on January 1, 20X7. On December 31, 20X8, assume Do

> Hollow Corporation acquired 70 percent of Surg Corporation’s voting stock on May 18, 20X1. The companies reported the following data with respect to intercompany sales in 20X4 and 20X5: Hollow reported operating income (excluding inco

> Prem Company acquired 60 percent ownership of Cooper Company’s voting shares on January 1, 20X2. During 20X5, Prem purchased inventory for $20,000 and sold the full amount to Cooper Company for $30,000. On December 31, 20X5, Cooper&aci

> Holiday Bakery owns 60 percent of Farmco Products Company’s stock. On January 1, 20X9, inventory reported by Holiday included 20,000 bags of flour purchased from Farmco at $9 per bag. By December 31, 20X9, all the beginning inventory purchased from Farmc

> Holiday Bakery owns 60 percent of Farmco Products Company’s stock. During 20X8, Farmco produced 100,000 bags of flour, which it sold to Holiday Bakery for $900,000. On December 31, 20X8, Holiday had 20,000 bags of flour purchased from Farmco Products on

> Karlow Corporation owns 60 percent of Draw Company’s voting shares. During 20X3, Karlow produced 25,000 computer desks at a cost of $82 each and sold 10,000 of them to Draw for $94 each. Draw sold 7,000 of the desks to unaffiliated companies for $130 eac

> Nordway Corporation acquired 90 percent of Olman Company’s voting shares of stock in 20X1. During 20X4, Nordway purchased 40,000 Playday doghouses for $24 each and sold 25,000 of them to Olman for $30 each. Olman sold 18,000 of the doghouses to retail es

> Nordway Corporation acquired 90 percent of Olman Company’s voting shares of stock in 20X1. During 20X4, Nordway purchased 40,000 Playday doghouses for $24 each and sold 25,000 of them to Olman for $30 each. Olman sold all of the doghouses to retail estab

> For each question, select the single best answer. Water Company owns 80 percent of Fire Company’s outstanding common stock. On December 31, 20X9, Fire sold equipment to Water at a price in excess of Fire’s carryi

> Select the correct answer for each of the following questions. Lorn Corporation purchased inventory from Dresser Corporation for $120,000 on September 20, 20X1, and resold 80 percent of the inventory to unaffiliated companies prior to December 31, 20X1,

> Select the correct answer for each of the following questions. Blue Company purchased 60 percent ownership of Kelly Corporation in 20X1. On May 10, 20X2, Kelly purchased inventory from Blue for $60,000. Kelly sold all of the inventory to an unaffiliated

> Select the correct answer for each of the following questions. During 20X3, Park Corporation recorded sales of inventory for $500,000 to Small Company, its wholly owned subsidiary, on the same terms as sales made to third parties. At December 31, 20X3,

> Select the correct answer for each of the following questions: Perez Inc. owns 80 percent of Senior Inc. During 20X2, Perez sold goods with a 40 percent gross profit to Senior. Senior sold all of these goods in 20X2. For 20X2 consolidated financial st

> Topp Corporation acquired 70 percent of Morris Company’s voting common stock on January 1, 20X3, for $158,900. Morris reported common stock outstanding of $100,000 and retained earnings of $85,000. The fair value of the noncontrolling i

> On January 1, 20X5, Pond Corporation acquired 80 percent of Skate Company’s stock by issuing common stock with a fair value of $180,000. At that date, Skate reported net assets of $150,000. The fair value of the noncontrolling interest

> Prime Company holds 80 percent of Lane Company’s stock, acquired on January 1, 20X2, for $160,000. On the acquisition date, the fair value of the noncontrolling interest was $40,000. Lane reported retained earnings of $50,000 and had $1

> Lofton Company owns 60 percent of Temple Corporation’s voting shares, purchased on May 17, 20X1, at book value. At that date, the fair value of the noncontrolling interest was equal to 40 percent of the book value of Temple

> In its 20X7 consolidated income statement, Bower Development Company reported consolidated net income of $961,000 and $39,000 of income assigned to the 30 percent noncontrolling interest in its only subsidiary, Subsidence Mining Inc. During the year, Su

> Select the correct answer for each of the following questions. In the preparation of a consolidated income statement: Income assigned to noncontrolling shareholders always is computed as a pro rata portion of the reported net income of the cons

> In preparing its consolidated financial statements at December 31, 20X7, the following consolidation entries were included in the consolidation worksheet of Master Corporation: Master owns 60 percent of Rakel Corporation’s voting comm

> Pelts Company holds a total of 70 percent of Bugle Corporation and 80 percent of Cook Products Corporation stock. Bugle purchased a warehouse with an expected life of 20 years on January 1, 20X1, for $40,000. On January 1, 20X6, it sold the warehouse to

> Bold Corporation acquired 75 percent of Toll Corporation’s voting common stock on January 1, 20X4, for $348,000, when the fair value of its net identifiable assets was $464,000 and the fair value of the noncontrolling interest was $116,000. Toll reported

> Petime Corporation acquired 90 percent ownership of United Grain Company on January 1, 20X4, for $108,000 when the fair value of United’s net assets was $10,000 higher than its $110,000 book value. The increase in value was attributed to amortizable asse

> The trial balance data presented in Problem P6-34 can be converted to reflect use of the cost method by inserting the following amounts in place of those presented for Randall Corporation: Required: Prepare the journal entries that would have been rec

> On December 31, 20X7, Randall Corporation recorded the following entry on its books to adjust from the fully adjusted equity method to the modified equity method for its investment in Sharp Company stock: Required: Adjust the data reported by Randall

> Randall Corporation acquired 80 percent of Sharp Company’s voting shares on January 1, 20X4, for $280,000 in cash and marketable securities. At that date, the noncontrolling interest had a fair value of $70,000 and Sharp reported net as

> The December 31, 20X6, condensed balance sheets of Pine Corporation and its 90 percent–owned subsidiary, Slim Corporation, are presented in the accompanying worksheet. Additional Information: Pine’s investment in

> Block Corporation was created on January 1, 20X0, to develop computer software. On January 1, 20X5, Foster Company purchased 90 percent of Block’s common stock at underlying book value. At that date, the fair value of the noncontrolling

> ower Corporation acquired 60 percent of Concerto Company’s stock on January 1, 20X3, for $24,000 in excess of book value. On that date, the book values and fair values of Concerto’s assets and liabilities were equal an

> Pine Corporation acquired 70 percent of Bock Company’s voting common shares on January 1, 20X2, for $108,500. At that date, the noncontrolling interest had a fair value of $46,500 and Bock reported $70,000 of common stock outstanding an

> Bunker Corporation owns 80 percent of Harrison Company’s stock. At the end of 20X8, Bunker and Harrison reported the following partial operating results and inventory balances: Bunker regularly prices its products at cost plus a 40 p

> Crow Corporation purchased 70 percent of West Company’s voting common stock on January 1, 20X5, for $291,200. On that date, the noncontrolling interest had a fair value of $124,800 and the book value of West’s net asse

> Bell Company purchased 60 percent ownership of Troll Corporation on January 1, 20X1, for $82,800. On that date, the noncontrolling interest had a fair value of $55,200 and Troll reported common stock outstanding of $100,000 and retained earnings of $20,0

> Proud Company and Slinky Company both produce and purchase equipment for resale each period and frequently sell to each other. Since Proud Company holds 60 percent ownership of Slinky Company, Proud’s controller compiled the following i

> On January 1, 20X1, Priority Corporation purchased 90 percent of Tall Corporation’s common stock at underlying book value. At that date, the fair value of the noncontrolling interest was equal to 10 percent of Tall Corporationâ

> Ajax Corporation purchased at book value 70 percent of Beta Corporation’s ownership and 90 percent of Cole Corporation’s ownership in 20X5. At the dates the ownership was acquired, the fair value of the noncontrolling

> Clean Air Products owns 80 percent of the stock of Superior Filter Company, which it acquired at underlying book value on August 30, 20X6. At that date, the fair value of the noncontrolling interest was equal to 20 percent of the book value of Superior

> Lever Corporation acquired 75 percent of the ownership of Tropic Company on January 1, 20X1. The fair value of the noncontrolling interest at acquisition was equal to its proportionate share of the fair value of the net assets of Tropic. The full amount

> Master Corporation acquired 80 percent ownership of Stanley Wood Products Company on January 1, 20X1, for $160,000. On that date, the fair value of the noncontrolling interest was $40,000, and Stanley reported retained earnings of $50,000 and had $100,00

> Amber Corporation acquired 60 percent ownership of Sparta Company on January 1, 20X8, at underlying book value. At that date, the fair value of the noncontrolling interest was equal to 40 percent of the book value of Sparta Company. Accumulated depreciat

> Amber Corporation acquired 60 percent ownership of Sparta Company on January 1, 20X8, at underlying book value. At that date, the fair value of the noncontrolling interest was equal to 40 percent of the book value of Sparta Company. Accumulated depreciat

> This problem is a continuation of P5-35. Mortar Corporation acquired 80 percent ownership of Granite Company on January 1, 20X7, for $173,000. At that date, the fair value of the noncontrolling interest was $43,250. The trial balances for the two compani

> Mortar Corporation acquired 80 percent ownership of Granite Company on January 1, 20X7, for $173,000. At that date, the fair value of the noncontrolling interest was $43,250. The trial balances for the two companies on December 31, 20X7, included the fol

> This problem is a continuation of P5-33. Power Corporation acquired 75 percent of Best Company’s ownership on January 1, 20X8, for $96,000. At that date, the fair value of the noncontrolling interest was $32,000. The book value of Best&

> Power Corporation acquired 75 percent of Best Company’s ownership on January 1, 20X8, for $96,000. At that date, the fair value of the noncontrolling interest was $32,000. The book value of Best’s net assets at acquisi

> Quill Corporation acquired 70 percent of North Company’s stock on January 1, 20X9, for $105,000. At that date, the fair value of the noncontrolling interest was equal to 30 percent of the book value of North Company. The companies repor

> Blue Corporation acquired controlling ownership of Skyler Corporation on December 31, 20X3, and a consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at that date follow: Du

> On January 2, 20X8, Total Corporation acquired 75 percent of Ticken Tie Company’s outstanding common stock. In exchange for Ticken Tie’s stock, Total issued bonds payable with a par value of $500,000 and fair value of

> Porter Corporation acquired 70 percent of Darla Corporation’s common stock on December 31, 20X4, for $102,200. At that date, the fair value of the noncontrolling interest was $43,800. Data from the balance sheets of the two companies in

> Hill Company paid $164,000 to acquire 40 percent ownership of Dale Company on January 1, 20X2. Net book value of Dale’s assets on that date was $300,000. Book values and fair values of net assets held by Dale were the same except for eq

> Balance sheet, income, and dividend data for Amber Corporation, Blair Corporation, and Carmen Corporation at January 1, 20X3, were as follows: On January 1, 20X3, Amber Corporation purchased 40 percent of the voting common stock of Blair Corporation by

> Ennis Corporation acquired 35 percent of Jackson Corporation’s stock on January 1, 20X8, by issuing 25,000 shares of its $2 par value common stock. Jackson Corporation’s balance sheet immediately before the acquisition

> On January 1, 20X0, Hunter Corporation issued 6,000 of its $10 par value shares to acquire 45 percent of the shares of Arrow Manufacturing. Arrow Manufacturing’s balance sheet immediately before the acquisition contained the following i

> Essex Company issued common shares with a par value of $50,000 and a market value of $165,000 in exchange for 30 percent ownership of Tolliver Corporation on January 1, 20X2. Tolliver reported the following balances on that date: The estimated economic

> Easy Chair Company purchased 40 percent ownership of Stuffy Sofa Corporation on January 1, 20X1, for $150,000. Stuffy Sofa’s balance sheet at the time of acquisition was as follows: During 20X1 Stuffy Sofa Corporation reported net inc

> Ball Corporation purchased 30 percent of Krown Company’s common stock on January 1, 20X5, by issuing preferred stock with a par value of $50,000 and a market price of $120,000. The following amounts relate to Krown’s b

> Select the correct answer for each of the following questions. 1. On July 1, 20X3, Barker Company purchased 20 percent of Acme Company’s outstanding common stock for $400,000 when the fair value of Acme’s net assets wa

> In preparing the consolidation worksheet for Bolger Corporation and its 60 percent–owned subsidiary, Feldman Company, the following consolidation entries were proposed by Bolger’s bookkeeper: Bolger’

> Master Corporation acquired 70 percent of Crown Corporation’s voting stock on January 1, 20X2, for $416,500. The fair value of the noncontrolling interest was $178,500 at the date of acquisition. Crown reported common stock outstanding of $200,000 and re

> Carroll Company sells all its output at 25 percent above cost. Pacific Corporation purchases all its inventory from Carroll. Selected information on the operations of the companies over the past three years is as follows: Pacific acquired 60 percent of

> Sweeny Corporation owns 60 percent of Bitner Company’s shares. Partial 20X2 financial data for the companies and consolidated entity were as follows: On January 1, 20X2, Sweeny’s inventory contained items purchased f

> How is the effect of unrealized intercompany profits on consolidated net income different between an upstream and a downstream sale?

> How are unrealized profits treated in the consolidated income statement if the intercompany sale occurred in a prior period and the transferred item is sold to a nonaffiliate in the current period?

> What dollar amounts in the consolidated financial statements will be incorrect if intercompany services are not eliminated?

> A parent company may use on its books one of several different methods of accounting for its ownership of a subsidiary: (a) cost method, (b) modified equity method, or (c) fully adjusted equity method. How will the choice of method affect the reported

> When is unrealized profit on an intercompany sale of land considered realized? When is profit on an intercompany sale of equipment considered realized? Why do the treatments differ?

> In the period in which an intercompany sale occurs, how do the consolidation entries differ when unrealized profits pertain to an intangible asset rather than a tangible asset?

> If the sale in the preceding question occurs on January 1, 20X3, what additional account will require adjustment in preparing the consolidated income statement?

> If a company sells a depreciable asset to its subsidiary at a profit on December 31, 20X3, what account balances must be eliminated or adjusted in preparing the consolidated income statement for 20X3?

> A subsidiary sold a depreciable asset to the parent company at a profit of $1,000 in the current period. Will the income assigned to the noncontrolling interest in the consolidated income statement for the current period be more if the intercompany sale

> A subsidiary sold a depreciable asset to the parent company at a gain in the current period. Will the income assigned to the noncontrolling interest in the consolidated income statement for the current period be more than, less than, or equal to a propor

> What consolidation entry is needed when inventory is sold to an affiliate at a profit and is resold to an unaffiliated party before the end of the reporting period? (Assume both affiliates use perpetual inventory systems.)

> Is an inventory sale from one subsidiary to another treated in the same manner as an upstream sale or a downstream sale? Why?

> What type of adjustment must be made in the consolidation worksheet if a differential is assigned to land and the subsidiary disposes of the land in the current period?

> How will the elimination of unrealized intercompany inventory profits recorded on the subsidiary’s books affect consolidated retained earnings?

> How will the elimination of unrealized intercompany inventory profits recorded on the parent’s books affect consolidated retained earnings?

> How do unrealized intercompany inventory profits from a prior period affect the computation of consolidated net income when the inventory is resold in the current period? Is it important to know whether the sale was upstream or downstream? Why, or why no