Question: Refer to the financial statements and notes

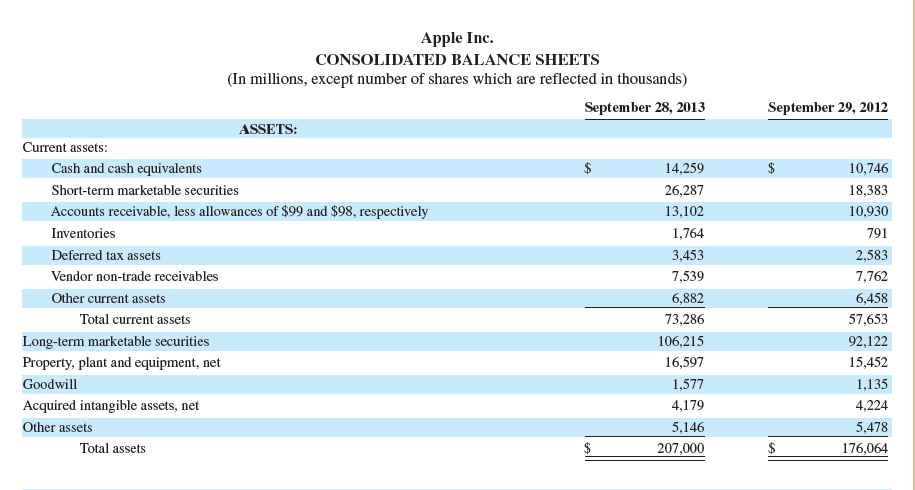

Refer to the financial statements and notes of Apple in Appendix A. In its presentation of accounts receivable on the balance sheet, how does it title accounts receivable? What does it report for its allowance as of September 28, 2013?

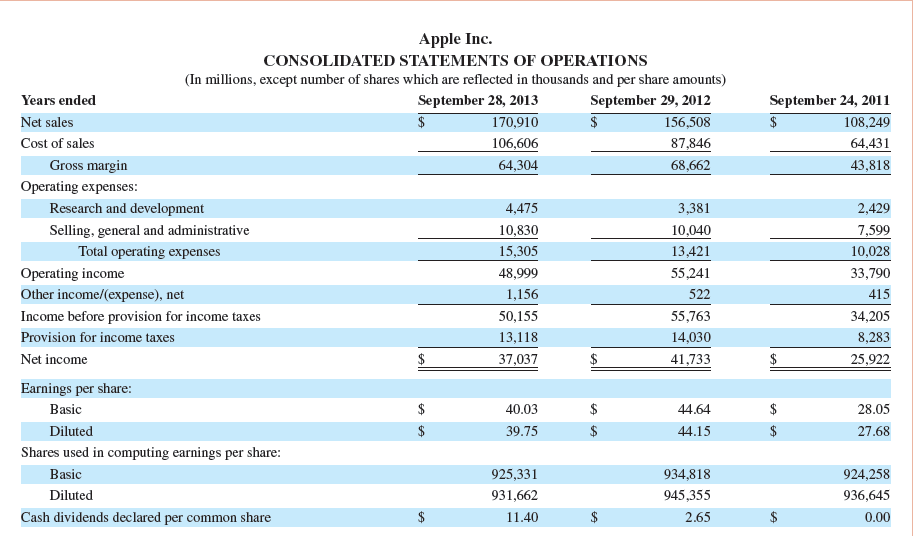

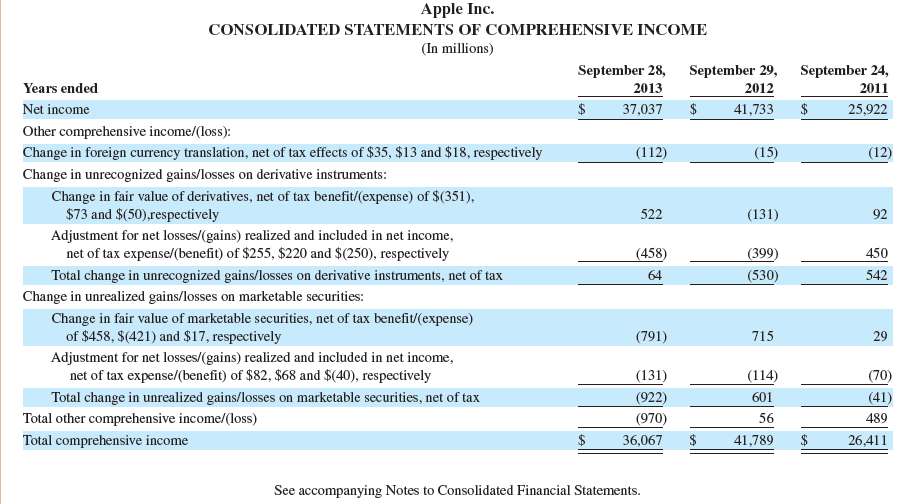

Apple’s financial statements from Appendix A:

Transcribed Image Text:

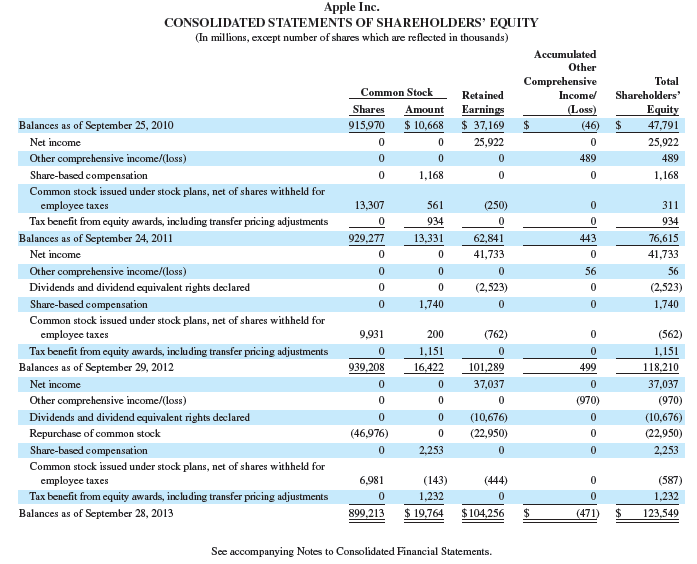

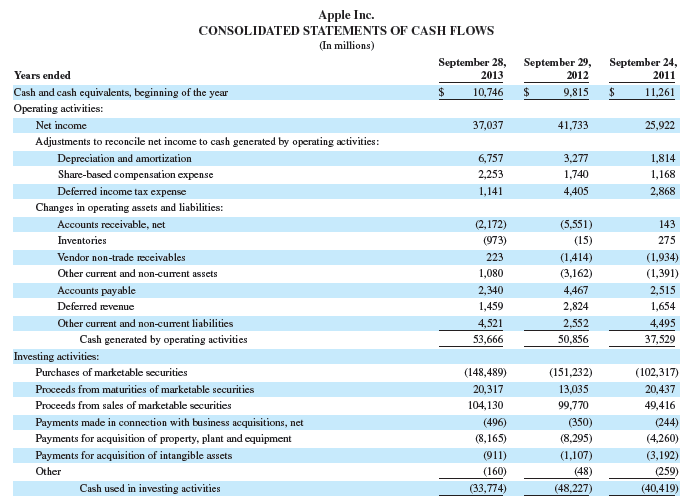

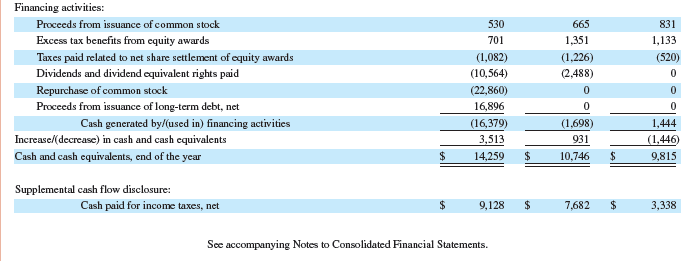

Apple Inc. CONSOLIDATED BALANCE SHEETS (In millions, except number of shares which are reflected in thousands) September 28, 2013 September 29, 2012 ASSETS: Current assets: Cash and cash equivalents 14,259 10,746 Short-term marketable securities 26,287 18,383 Accounts receivable, less allowances of $99 and $98, respectively 13,102 10,930 Inventories 1,764 791 Deferred tax assets 3,453 2,583 Vendor non-trade receivables 7,539 7,762 Other current assets 6,882 6,458 Total current assets 73,286 57,653 Long-term marketable securities 106,215 92,122 Property, plant and equipment, net 16,597 15,452 Goodwill 1,577 1,135 Acquired intangible assets, net 4,179 4,224 Other assets 5,146 5,478 Total assets 207,000 176,064 LIABILITIES AND SHAREHOLDERS’ EQUITY: Current liabilities: Accounts payable $ 22,367 $ 21,175 Accrued expenses 13,856 11,414 Deferred revenue 7,435 5,953 Total current liabilities 43,658 38,542 Deferred revenue – non-current 2,625 2,648 Long-term debt 16,960 Other non-current liabilities 20,208 16,664 Total liabilities 83,451 57,854 Commitments and contingencies Shareholders' equity: Common stock, no par value; 1,800,000 shares authorized; 899,213 and 939,208 shares issued and outstanding, respectively 19,764 16,422 Retained earnings 104,256 101,289 499 Accumulated other comprehensive income/(loss) Total shareholders' equity (471) 123,549 118,210 Total liabilities and shareholders' equity 207,000 176,064 See accompanying Notes to Consolidated Financial Statements. Apple Inc. CONSOLIDATED STATEMENTS OF OPERATIONS (In millions, except number of shares which are reflected in thousands and per share amounts) Years ended September 28, 2013 September 29, 2012 156,508 September 24, 2011 Net sales $ 170,910 108,249 24 Cost of sales 106,606 87,846 64,431 Gross margin Operating expenses: 64,304 68,662 43,818 Research and development 4,475 3,381 2,429 Selling, general and administrative 10,830 10,040 7,599 Total operating expenses 15,305 13,421 10,028 Operating income 48,999 55,241 33,790 Other income/(expense), net 1,156 522 415 Income before provision for income taxes 50,155 55,763 34,205 Provision for income taxes 13,118 14,030 8,283 Net income $ 37,037 41,733 25,922 Earnings per share: Basic 40.03 44.64 28.05 Diluted $ 39.75 44.15 27.68 Shares used in computing earnings per share: Basic 925,331 934,818 924,258 Diluted 931,662 945,355 936,645 Cash dividends declared per common share $ 11.40 2.65 0.00 Apple Inc. CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (In millions) September 29, 2012 September 24, September 28, 2013 Years ended 2011 Net income $ 37,037 $ 41,733 $ 25,922 Other comprehensive income/(loss): Change in foreign currency translation, net of tax effects of $35, $13 and $18, respectively (112) (15) (12) Change in unrecognized gains/losses on derivative instruments: Change in fair value of derivatives, net of tax benefit/(expense) of $(351), $73 and $(50),respectively Adjustment for net losses/(gains) realized and included in net income, net of tax expense/(benefit) of $255, $220 and $(250), respectively 522 (131) 92 (458) (399) 450 Total change in unrecognized gains/losses on derivative instruments, net of tax 64 (530) 542 Change in unrealized gains/losses on marketable securities: Change in fair value of marketable securities, net of tax benefit/(expense) of $458, $(421) and $17, respectively (791) 715 29 Adjustment for net losses/(gains) realized and included in net income, net of tax expense/(benefit) of $82, $68 and $(40), respectively (131) (114) (70) (922) (970) Total change in unrealized gains/losses on marketable securities, net of tax 601 (41) Total other comprehensive income/(loss) 56 489 Total comprehensive income $ 36,067 $ 41,789 $ 26,411 See accompanying Notes to Consolidated Financial Statements. Apple Inc. CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY (In millions, except number of shares which are reflected in thousands) Accumulated Other Comprehensive Total Common Stock Retained Income/ Shareholders' Shares Amount Earnings (Loss) 915,970 $ 10,668 $ 37,169 $ EQUITY 2$ Balances as of September 25, 2010 (46) 47,791 Net income 25,922 25,922 Other comprehensive income/(loss) 489 489 Share-based compensation 1,168 1,168 Common stock issued under stock plans, net of shares withheld for employee taxes 13,307 561 (250) 311 Tax benefit from equity awards, including transfer pricing adjustments 934 934 Balances as of September 24, 2011 929,277 13,331 62,841 443 76,615 Net income 41,733 41,733 Other comprehensive income/(loss) 56 56 Dividends and dividend equivalent rights declared (2,523) (2,523) Share-based compensation 1,740 1,740 Common stock issucd under stock plans, net of shares withheld for employee taxes 9,931 200 (762) (562) Tax benefit from equity awards, including transfer pricing adjustments 1,151 1,151 Balances as of September 29, 2012 939,208 16,422 101,289 499 118,210 Net income 37,037 37,037 Other comprehensive income/(loss) (970) (970) Dividends and dividend equivalent rights declared (10,676) (10,676) Repurchase of common stock (46,976) (22,950) (22,950) Share-based compensation 2,253 2,253 Common stock issued under stock plans, net of shares withheld for employee taxes 6,981 (143) (444) (587) Tax benefit from equity awards, including transfer pricing adjustments 1,232 1,232 Balances as of September 28, 2013 899,213 $ 19,764 $104,256 (471) $ 123,549 Sec accompanying Notes to Consolidated Financial Statements. O ol Apple Inc. CONSOLIDATED STATEMENTS OF CASH FLOWS (In millions) September 28, 2013 September 29, 2012 September 24, 2011 Years ended Cash and cash equivalents, beginning of the ycar 10,746 9,815 %2$ 11,261 Operating activities: Net income 37,037 41,733 25,922 Adjustments to reconcile net income to cash generated by operating activities: Depreciation and amortization 6,757 3,277 1,814 Share-based compensation expense 2,253 1,740 1,168 Deferred income tax expense 1,141 4,405 2,868 Changes in operating assets and liabilities: Accounts receivable, net (2,172) (5,551) 143 Inventories (973) (15) 275 Vendor non-trade receivables 223 (1,414) (1,934) Other current and non-curent assets 1,080 (3,162) (1,391) Accounts payable 2,340 4,467 2,515 Deferred revenue 1,459 2,824 1,654 Other current and non-curent liabilities 4,521 2,552 4,495 Cash generated by operating activities 53,666 50,856 37,529 Investing activities: Purchases of marketable securities (148,489) (151,232) (102,317) Proceeds from maturities of marketable securities 20,317 13,035 20,437 Proceeds from sales of marketable securities 104,130 99,770 49,416 Payments made in connection with business acquisitions, net (496) (350) (244) Payments for acquisition of property, plant and equipment (8,165) (8,295) (4,260) Payments for acquisition of intangible assets (911) (1,107) (3,192) Other (160) (48) (259) Cash used in investing activities (33,774) (48,227) (40,419) Financing activities: Proceeds from issuance of common stock 530 665 831 Excess tax benefits from cquity awards 701 1,351 1,133 Taxes paid related to net share settlement of equity awards (1,082) (1,226) (520) Dividends and dividend equivalent rights paid (10,564) (2,488) Repurchase of common stock (22,860) Proceeds from issuance of long-term debt, net 16,896 Cash generated by/(used in) financing activities (16,379) (1,698) 1,444 Increase/(decrease) in cash and cash equivalents 3,513 931 (1,446) Cash and cash equivalents, end of the year 14,259 $ 10,746 2$ 9,815 Supplemental cash flow disclosure: Cash paid for income taxes, net 24 9,128 24 7,682 24 3,338 See accompanying Notes to Consolidated Financial Statements.

> Explain the relationship between earnings per share, projected earnings, and the market price for a share of stock.

> 1. Corporations sell common stock to finance their business start-up costs and help pay for expansion and their ongoing business activities. 2. A corporation must pay dividends to stockholders. 3. The record date is the date when a stockholder must be r

> 1. You can’t predict exactly how much money you’ll need when you retire 2. Social Security is an important source of retirement income for most Americans. 3. A defined-contribution plan does not guarantee any particular benefit at retirement. 4 .An execu

> 1. The major reasons why investors purchase mutual funds are professional management and diversification. 2. Shares in a closed-end mutual fund are issued by the investment company only when the fund is organized. 3. Typically, the management fee for a m

> 1. Who elects a corporation’s board of directors? a. Preferred stockholders b. Common stockholders c. The corporation’s top executives d. The corporation’s employees 2. A stock split a. always guarantees that the investor will make money. b. enables man

> 1. The first step in retirement planning is to a. estimate your spending needs. b. estimate the inflation rate. c. evaluate your planned retirement income. d. analyze your current assets and liabilities. 2. Under what retirement plan does your employer

> 1. A mutual fund in which new shares are issued and redeemed by the investment company at the request of investors is called a (n) ____________ fund. a. closed end b. open-end c. load d. no-load 2. Some mutual funds charge 12b-1 fees to defray the cost

> What is the major difference between a regular IRA and a Roth IRA?

> What are the most popular personal retirement plans?

> What are the two basic types of employer pension plans?

> What are four major sources of retirement income?

> In your own words, describe how an investment in common stock could help you obtain your investment goals.

> 1. What is the benefit to Jamie Lee and Ross investing in a company’s IPO? Will they be guaranteed a large return from this investment? At this life stage, would you recommend that Jamie Lee and Ross invest in an IPO? Why? 2. Jamie Lee’s father suggest

> Entering an Industry: A firm (player 1) is considering entering an established industry with one incumbent firm (player 2). Player 1 must choose whether to enter or to not enter the industry. If player 1 enters the industry then player 2 can either accom

> Continuous all pay auction: Consider an all-pay auction for a good worth 1 to each of the two bidders. Each bidder can choose to offer a bid from the unit interval so that Si = [0, 1]. Players only care about the expected value they will e

> Brothers: Consider the following game that proceeds in two steps: In the first stage one brother (player 2) has two $10 bills and can choose one of two options: he can give his younger brother (player 1) $20, or give him one of the $10 bills (giving noth

> Market entry: There are 3 firms that are considering entering a new market. The payoff for each firm that enters is 150 / n where n is the number of firms that enter. The cost of entering is 62. (a) Find all the pure strategy Nash equilibria. (b) Find the

> Mutually Assured Destruction (revisited): Consider the game in section 8.3.3. (a) Find the mixed strategy equilibrium of the war stage game and argue that it is unique. (b) What is the unique sub-game perfect equilibrium that includes the mixed strategy

> Declining Industry: Consider two competing firms in a declining indus- try that cannot support both firms profitably. Each firm has three possible choices as it must decide whether or not to exit the industry immediately, at the end of this quarter, or a

> Centipedes: Imagine a two player game that proceeds as follows. A pot of money is created with $6 in it initially. Player 1 moves first, then player 2, then player 1 again and finally player 2 again. At each player’s turn to move, he has two possible act

> Monitoring: An employee (player 1) who works for a boss (player 2) can either work (W) or shirk (S), while his boss can either monitor the employee (M) or ignore him (I). Like most employee-boss relationships, if the employee is working then the boss pre

> Strategies and equilibrium: Consider a two player game in which player 1 can choose A or B. The game ends if he chooses A while it continues to player 2 if he chooses B. Player 2 can then choose C or D, with the game ending after C and continuing again w

> Entry Deterrence 1: NSG is considering entry into the local phone market in the Bay Area. The incumbent S&P, predicts that a price war will result if NSG enters. If NSG stays out, S&P earns monopoly profits valued at $10 million (net present value, or NP

> Investment in the Future: Consider two firms that play a Cournot competition game with demand p = 100 − q, and costs for each firm given by ci (qi) = 10qi. Imagine that before the two firms play the Cournot game, firm 1 can invest in cost reduction. If i

> The Value of Commitment: Consider the three period example of a player with hyperbolic discounting described in section 8.3.4 with ln(x) utility in each of the three periods and with discount factors = 1 and = 1/2. We solved the optimal consumption p

> The Industry Leader: Three oligopolists operate in a market with inverse demand given by P (Q) = a−Q, where Q = q1+q2+q3, and qi is the quantity produced by firm i. Each firm has a constant marginal cost of production, c and no fixed cost. The firms choo

> Hyperbolic Discounting: Consider the three period example of a player with hyperbolic discounting described in section 8.3.4 with ln(x) utility in each of the three periods and with discount factors 0 < < 1 and 0 < < 1 (a) Solve the optimal choice o

> Agenda Setting: An agenda-setting game is described as follows. The “issue space” (set of possible policies) is an interval X = [0, 5]. An Agenda Setter (player 1) proposes an alternative x ∈ X against the status quo q = 4 After player 1 proposes x, the

> The Tax Man: A citizen (player 1) must choose whether or not to file taxes honestly or whether to cheat. The tax man (player 2) decides how much effort to invest in auditing and can choose ∈ [0, 1], and the cost to the tax man of investing at level

> Playing it safe: Consider the following dynamic game: Player 1 can choose to play it safe (denote this choice by S), in which case both he and player 2 get a payoff of 3 each, or he can risk playing a game with player 2 (denote this choice

> Let i be a mixed strategy of player i that puts positive weight on one strictly dominated pure strategy. Show that there exists a mixed strategy ’i that puts no weight on any dominated pure strategy and that dominates i.

> Refer to the financial statements of Samsung in Appendix A. What does Samsung title its accounts receivable on its consolidated balance sheet? What are Samsung’s accounts receivable at December 31, 2013? Samsung’s Fin

> Compute Topp Company’s price-earnings ratio if its common stock has a market value of $20.54 per share and its EPS is $3.95. Would an analyst likely consider this stock potentially overpriced, underpriced, or neither? Explain.

> Refer to the information in QS 6-4 and assume the periodic inventory system is used. Determine the costs assigned to ending inventory when costs are assigned based on the weighted average method. (Round per unit costs and inventory amounts to cents.)

> Nix’It Company’s ledger on July 31, its fiscal year-end, includes the following selected accounts that have normal balances (Nix’It uses the perpetual inventory system). A physical count of its July

> Refer to the information in QS 6-4 and assume the periodic inventory system is used. Determine the costs assigned to ending inventory when costs are assigned based on the FIFO method. (Round per unit costs and inventory amounts to cents.) Information fr

> Refer to QS 5-7 and prepare journal entries to record each of the merchandising transactions assuming that the periodic inventory system is used. Data from QS 5-7: Apr. 1 Sold merchandise for $3,000, granting the customer terms of 2y10, EOM; invoice dat

> Refer to QS 5-4 and prepare journal entries to record each of the merchandising transactions assuming that the periodic inventory system is used. Data from QS 5-4: Nov. 5 Purchased 600 units of product at a cost of $10 per unit. Terms of the sale are 2/

> Refer to the balance sheet of Google in Appendix A. Does it use the direct write-off method or allowance method in accounting for its accounts receivable? What is the realizable value of its receivables balance as of December 31, 2013? Googleâ

> Refer to the information in QS 6-10 and assume the periodic inventory system is used. Determine the costs assigned to ending inventory when costs are assigned based on the LIFO method. (Round per unit costs and inventory amounts to cents.) Data from QS

> Refer to the information in QS 6-10 and assume the periodic inventory system is used. Determine the costs assigned to ending inventory when costs are assigned based on the FIFO method. (Round per unit costs and inventory amounts to cents.) Data from QS

> Label the following headings, line items, and notes with the numbers 1 through 13 according to their sequential order (from top to bottom) for presentation of the statement of cash flows. a. “Cash flows from investing activities” title b. “For period End

> Refer to the data in QS 16-11. 1. How much cash is received from sales to customers for year 2015? 2. What is the net increase or decrease in cash for year 2015? Data from QS 16-11: CRUZ, INC. Comparative Balance Sheets December 31, 2015 2015 2014

> Classify the following cash flows as either operating, investing, or financing activities. ______ 1. Sold long-term investments for cash. ______ 2. Received cash payments from customers. ______ 3. Paid cash for wages and salaries. ______ 4. Purchased

> On February 1, 2015, Garzon purchased 6% bonds issued by PBS Utilities at a cost of $40,000, which is their par value. The bonds pay interest semiannually on July 31 and January 31. For 2015, prepare entries to record Garzon’s July 31 receipt of interest

> Prepare Hertog Company’s journal entries to reflect the following transactions for the current year. May 7 Purchases 200 shares of Kraft stock as a short-term investment in trading securities at a cost of $50 per share plus $300 in broker fees. June 6

> On April 18, Riley Co. made a short-term investment in 300 common shares of XLT Co. The purchase price is $42 per share and the broker’s fee is $250. The intent is to actively manage these shares for profit. On May 30, Riley Co. receives $1 per share fro

> On March 1, 2015, a U.S. company made a credit sale requiring payment in 30 days from a Malaysian company, Hamac Sdn. Bhd., in 20,000 Malaysian ringgits. Assuming the exchange rate between Malaysian ringgits and U.S. dollars is $0.4538 on March 1 and $0.

> A U.S. company sells a product to a British company with the transaction listed in British pounds. On the date of the sale, the transaction total of $14,500 is billed as £10,000, reflecting an exchange rate of 1.45 (that is, $1.45 per pound). Prepare the

> The return on total assets is the focus of analysts, creditors, and other users of financial statements. 1. How is the return on total assets computed? 2. What does this important ratio reflect?

> On July 1, 2015, Advocate Company exercises an $8,000 call option (plus par value) on its outstanding bonds that have a carrying value of $416,000 and par value of $400,000. The company exercises the call option after the semiannual interest is paid on J

> Garcia Company issues 10%, 15-year bonds with a par value of $240,000 and semiannual interest payments. On the issue date, the annual market rate for these bonds is 8%, which implies a selling price of 117 1⁄4. Prepare the journal entry for the issuance

> Enviro Company issues 8%, 10-year bonds with a par value of $250,000 and semiannual interest payments. On the issue date, the annual market rate for these bonds is 10%, which implies a selling price of 87 1⁄2. Prepare the journal entries for the issuance

> Algoma, Inc., signs a five-year lease for office equipment with Office Solutions. The present value of the lease payments is $15,499. Prepare the journal entry that Algoma records at the inception of this capital lease.

> Jin Li, an employee of ETrain.com, leases a car at O’Hare airport for a three-day business trip. The rental cost is $250. Prepare the entry by ETrain.com to record Jin Li’s short-term car lease cost.

> Madrid Company plans to issue 8% bonds on January 1, 2015, with a par value of $4,000,000. The company sells $3,600,000 of the bonds on January 1, 2015. The remaining $400,000 sells at par on March 1, 2015. The bonds pay interest semiannually as of June

> Garcia Company issues 10%, 15-year bonds with a par value of $240,000 and semiannual interest payments. On the issue date, the annual market rate for these bonds is 8%, which implies a selling price of 117 1⁄4. The effective interest method is used to al

> Garcia Company issues 10%, 15-year bonds with a par value of $240,000 and semiannual interest payments. On the issue date, the annual market rate for these bonds is 14%, which implies a selling price of 75 1⁄4. The effective interest method is used to al

> Compute the debt-to-equity ratio for each of the following companies. Which company appears to have a riskier financing structure? Explain.

> On September 15, Krug Company purchased merchandise inventory from Makarov with an invoice price of $35,000 and credit terms of 2/10, n/30. Krug Company paid Makarov on September 28. Prepare any required journal entry (ies) for Krug Company (the purcha

> Murray Company borrows $340,000 cash from a bank and in return signs an installment note for five annual payments of equal amount, with the first payment due one year after the note is signed. Use Table B.3 in Appendix B to compute the amount of the an

> Prepare journal entries to record the following transactions for Emerson Corporation. July 15 Declared a cash dividend payable to common stockholders of $165,000. Aug. 15 Date of record is August 15 for the cash dividend declared on July 15. Aug. 31

> Prepare the journal entry to record Autumn Company’s issuance of 63,000 shares of no-par value common stock assuming the shares: a. Sell for $29 cash per share. b. Are exchanged for land valued at $1,827,000.

> Prepare the journal entry to record Zende Company’s issuance of 75,000 shares of $5 par value common stock assuming the shares sell for: a. $5 cash per share. b. $6 cash per share.

> Air France-KLM reports the following equity information for its fiscal year ended March 31, 2014 (euros in millions). Prepare its journal entry, using its account titles, to record the issuance of capital stock assuming that its entire par value stock wa

> The stockholders’ equity section of Montel Company’s balance sheet follows. The preferred stock’s call price is $40. Determine the book value per share of the common stock. Preferred stock-5% cum

> Epic Company earned net income of $900,000 this year. The number of common shares outstanding during the entire year was 400,000, and preferred shareholders received a $20,000 cash dividend. Compute Epic Company’s basic earnings per share.

> Murray Company reports net income of $770,000 for the year. It has no preferred stock, and its weighted average common shares outstanding is 280,000 shares. Compute its basic earnings per share.

> Stockholders’ equity of Ernst Company consists of 80,000 shares of $5 par value, 8% cumulative preferred stock and 250,000 shares of $1 par value common stock. Both classes of stock have been outstanding since the company’s inception. Ernst did not decla

> Stein agrees to pay Choi and Amal $10,000 each for a one-third (331⁄3%) interest in the Choi and Amal partnership. Immediately prior to Stein’s admission, each partner had a $30,000 capital balance. Make the journal entry to record Stein’s purchase of th

> On August 1, Gilmore Company purchased merchandise from Hendren with an invoice price of $60,000 and credit terms of 2/10, n/30. Gilmore Company paid Hendren on August 11. Prepare any required journal entry(ies) for Gilmore Company (the purchaser) on: (

> Jules and Johnson are partners, each with $40,000 in their partnership capital accounts. Kwon is admitted to the partnership by investing $40,000 cash. Make the entry to show Kwon’s admission to the partnership.

> Blake and Matthew are partners who agree that Blake will receive a $100,000 salary allowance and that any remaining income or loss will be shared equally. If Matthew’s capital account is credited for $2,000 as his share of the net income in a given perio

> Ann Stolton and Susie Bright are partners in a business they started two years ago. The partnership agreement states that Stolton should receive a salary allowance of $15,000 and that Bright should receive a $20,000 salary allowance. Any remaining income

> On September 11, 2014, Home Store sells a mower for $500 with a one-year warranty that covers parts. Warranty expense is estimated at 8% of sales. On July 24, 2015, the mower is brought in for repairs covered under the warranty requiring $35 in materials

> Chavez Co.’s salaried employees earn four weeks’ vacation per year. It pays $312,000.00 in total employee salaries for 52 weeks, but its employees work only 48 weeks. This means Chavez’s total weekly expense is $6,500 ($312,000/48 weeks) instead of the $

> Noura Company offers an annual bonus to employees if the company meets certain net income goals. Prepare the journal entry to record a $15,000 bonus owed to its workers (to be shared equally) at calendar year-end.

> On January 15, the end of the first biweekly pay period of the year, North Company’s payroll register showed that its employees earned $35,000 of sales salaries. Withholdings from the employees’ salaries include FICA Social Security taxes at the rate of

> Ticketsales, Inc., receives $5,000,000 cash in advance ticket sales for a four-date tour of Bon Jovi. Record the advance ticket sales on October 31. Record the revenue earned for the first concert date of November 5, assuming it represents one-fourth of

> Sera Corporation has made and recorded its quarterly income tax payments. After a final review of taxes for the year, the company identifies an additional $40,000 of income tax expense that should be recorded. A portion of this additional expense, $6,000

> The payroll records of Speedy Software show the following information about Marsha Gottschalk, an employee, for the weekly pay period ending September 30, 2015. Gottschalk is single and claims one allowance. Compute her Social Security tax (6.2%), Medica

> Biloxi Gifts uses a sales journal, a purchases journal, a cash receipts journal, a cash disbursements journal, and a general journal as illustrated in this chapter. Journalize its November transactions that should be recorded in the general journal. For

> Compute the times interest earned for Park Company, which reports income before interest expense and income taxes of $1,885,000 and interest expense of $145,000. Interpret its times interest earned (assume that its competitors average a times interest ea

> Assume a company’s equipment carries a book value of $16,000 ($16,500 cost less $500 accumulated depreciation) and a fair value of $14,750, and that the $1,250 decline in fair value in comparison to the book value meets the two-step impairment test. Prep

> On January 2, 2015, the Matthews Band acquires sound equipment for concert performances at a cost of $65,800. The band estimates it will use this equipment for four years. It estimates that after four years it can sell the equipment for $2,000. Matthews

> On January 2, 2015, the Matthews Band acquires sound equipment for concert performances at a cost of $65,800. The band estimates it will use this equipment for four years, during which time it anticipates performing about 200 concerts. It estimates that

> On January 2, 2015, the Matthews Band acquires sound equipment for concert performances at a cost of $65,800. The band estimates it will use this equipment for four years, during which time it anticipates performing about 200 concerts. It estimates that

> Listed below are certain costs (or discounts) incurred in the purchase or construction of new plant assets. (1) Indicate whether the costs should be expensed or capitalized (meaning they are included in the cost of the plant assets on the balance sheet).

> Aneko Company reports the following ($000s): net sales of $14,800 for 2015 and $13,990 for 2014; end-of-year total assets of $19,100 for 2015 and $17,900 for 2014. Compute its total asset turnover for 2015, and assess its level if competitors average a t

> On January 4 of this year, Diaz Boutique incurs a $105,000 cost to modernize its store. Improvements include new floors, ceilings, wiring, and wall coverings. These improvements are estimated to yield benefits for 10 years. Diaz leases its store and has

> Identify the following assets a through h as reported on the balance sheet as intangible assets (IA), natural resources (NR), or other (O). ______ a. Oil well ______ b. Trademark ______ c. Leasehold ______ d. Gold mine ______ e. Building ______ f. Copyri

> Perez Company acquires an ore mine at a cost of $1,400,000. It incurs additional costs of $400,000 to access the mine, which is estimated to hold 1,000,000 tons of ore. The estimated value of the land after the ore is removed is $200,000. 1. Prepare the

> Solstice Company determines on October 1 that it cannot collect $50,000 of its accounts receivable from its customer P. Moore. It uses the direct write-off method to record this loss as of October 1. On October 30, P. Moore unexpectedly paid his account

> Kegler Bowling installs automatic scorekeeping equipment with an invoice cost of $190,000. The electrical work required for the installation costs $20,000. Additional costs are $4,000 for delivery and $13,700 for sales tax. During the installation, a com

> On August 2, 2015, Jun Co. receives a $6,000, 90-day, 12% note from customer Ryan Albany as payment on his $6,000 account. Prepare Jun’s journal entry assuming the note is honored by the customer on October 31, 2015.

> Warner Company’s year-end unadjusted trial balance shows accounts receivable of $99,000, allowance for doubtful accounts of $600 (credit), and sales of $280,000. Uncollectibles are estimated to be 0.5% of sales. Prepare the December 31 year-end adjusting

> The following list describes aspects of either the allowance method or the direct write-off method to account for bad debts. For each item listed, indicate if the statement best describes either the allowance method or the direct write-off method. ______

> Record the sale by Balus Company of $125,000 in accounts receivable on May 1. Balus is charged a 2.5% factoring fee.

> Daw Company’s December 31 year-end unadjusted trial balance shows a $10,000 balance in Notes Receivable. This balance is from one 6% note dated December 1, with a period of 45 days. Prepare any necessary journal entries for December 31 and for the note’s

> Nolan Company deposits all cash receipts on the day when they are received and it makes all cash payments by check. At the close of business on June 30, 2015, its Cash account shows a $22,352 debit balance. Nolan’s June 30 bank statement shows $21,332 on