Question: The Town of Bedford Falls approved a

The Town of Bedford Falls approved a General Fund operating budget for the fiscal year ending June 30, 2011. The budget provides for estimated revenues of $2,700,000 as follows: property taxes, $1,900,000; licenses and permits, $350,000; fines and forfeits, $250,000; and intergovernmental (state grants), $200,000. The budget approved appropriations of $2,650,000 as follows: General Government, $500,000; Public Safety, $1,600,000; Public Works, $350,000; Parks and Recreation, $150,000; and Miscellaneous, $50,000.

Required

a. Prepare the journal entry (or entries), including subsidiary ledger entries, to record the Town of Bedford Falls’s General Fund operating budget on July 1, 2010, the beginning of the Town’s 2011 fiscal year.

b. Prepare journal entries to record the following transactions that occurred during the month of July 2010.

1. Revenues were collected in cash amounting to $31,000 for licenses and permits and $12,000 for fines and forfeits.

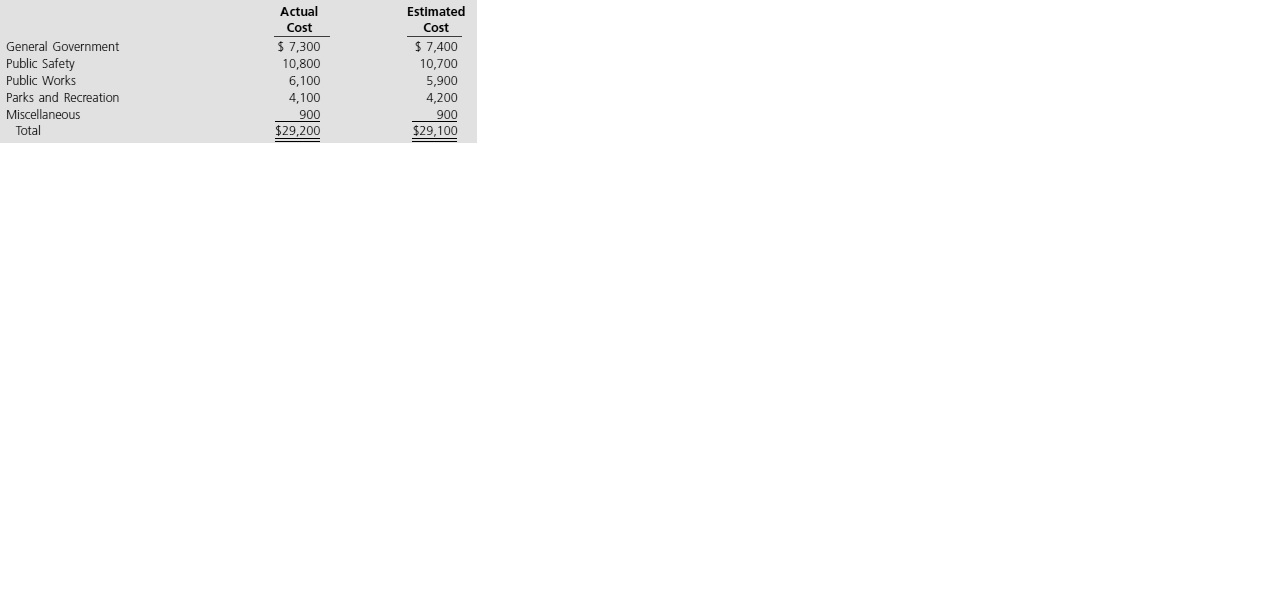

2. Supplies were ordered by the following functions in early July 2010 at the estimated costs shown:

3. During July 2010, supplies were received at the actual costs shown below and were paid in cash. General Government, Parks and Recreation, and Miscellaneous received all supplies ordered. Public Safety and Public Works received part of the supplies ordered earlier in the month at estimated costs of $10,700 and $5,900, respectively.

c. Calculate and show in good form the amount of budgeted but unrealized revenues in total and from each source as of July 31, 2010.

d. Calculate and show in good form the amount of available appropriation in total and for each function as of July 31, 2010.

Transcribed Image Text:

$ 7,400 11,300 6,100 General Government Public Safety Public Works Parks and Recreation 4,200 Miscellaneous 900 Total $29 900 Actual Estimated Cost Cost General Government $ 7,300 $ 7,400 Public Safety Public Works 10,800 6,100 4,100 900 $29,200 10,700 5,900 Parks and Recreation 4,200 Miscellaneous 900 Total $29,100

> In the current fiscal year, St. George County issued $3,000,000 in general obligation term bonds for 102. The county is required to use any accrued interest or premiums for servicing the debt issue. a. How would the bond issue be recorded at the fund and

> On July 20, 2011, the building occupied by Sunshine City’s Parks and Recreation Department suffered severe structural damage as a result of a hurricane. It had been 48 years since a hurricane had hit the Sunshine City area, although hurricanes in Sunshin

> Crystal City signed a lease agreement with East Coast Builders, Inc., under which East Coast will construct a new office building for the city at a cost of $12 million and lease it to the city for 30 years. The city agrees to make an initial payment of $

> Lynn County has prepared the following schedule related to its capital asset activity for the fiscal year 2011. Lynn County has governmental activities only, with no business-type activities. Required a. Does the above capital asset footnote disclosure

> Make all necessary entries in the appropriate governmental fund general journal and the government-wide governmental activities general journal for each of the following transactions entered into by the City of Fordache. 1. The city received a donation o

> Recent river flooding damaged a part of the Town of Brownville Library. The library building is over 70 years old and is located in a part of the town that is on the national historic preservation register. Some of the costs related to the damage include

> How does the modified accrual basis of accounting differ from the accrual basis?

> Desert City is a rapidly growing city in the Southwest, with a current population of 200,000. To cope with the growing vehicular traffic and the need for infrastructure expansion (e.g., streets, sidewalks, lighting, storm water drains, and sewage systems

> Compare the accounting for capital projects financed by special assessment bonds when (a) a government assumes responsibility for debt service should special assessment collections be insufficient, as opposed to (b) the government assumes no responsibi

> The county replaced its old office building with a new structure. Rather than destroy the old office building, the county decided to convert the old building and use it as a storage facility. Why would the old office building need to be evaluated for imp

> Which expenditures of a capital projects fund should be capitalized to Construction Work in Progress? Is Construction Work in Progress included in the chart of accounts of a capital projects fund? If not, where would it be found?

> What disclosures about long-term liabilities are required in the notes to the financial statements?

> If a capital project is incomplete at the end of a fiscal year, why is it considered desirable to close Encumbrances and all operating statement accounts at year-end? Why is it desirable to reestablish the Encumbrances account as of the first day of the

> What is the purpose of a capital projects fund? Give some examples of projects that might be considered capital projects.

> Compare the reporting of intangible assets under GASB and FASB standards.

> How does one determine whether a particular lease is a capital lease or an operating lease? What entries are required in the general journals of a governmental fund and governmental activities at the government-wide level to record a capital lease at its

> What is the difference between using the modified approach to accounting for infrastructure assets and depreciating infrastructure assets? Under the modified approach, what happens if infrastructure assets are not maintained at or above the established c

> Explain what disclosures the GASB requires for capital assets in the notes to the financial statements.

> Why do governmental fund financial statements use a different basis of accounting and measurement focus than the Governmental Activities column of the government-wide financial statements? Also, which basis of accounting and which measurement focus appli

> What are general capital assets? How are they reported?

> Annabelle Benton, great-granddaughter of the founder of the Town of Benton, made a cash contribution in the amount of $500,000 to be held as an endowment. To account for this endowment, the town has created the Alex Benton Park Endowment Fund. Under term

> The City of Ashland’s General Fund had the following post-closing trial balance at April 30, 2010, the end of its fiscal year: During the year ended April 30, 2011, the following transactions, in summary form, with subsidiary ledger d

> What are the three sections of a comprehensive annual financial report (CAFR)? What information is contained in each section? How do the minimum requirements for general purpose external financial reporting relate in scope to the CAFR?

> The following transactions occurred during the 2011 fiscal year for the City of Fayette. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures

> The following transactions affected various funds and activities of the City of Atwater. 1. The Fire Department, a governmental activity, purchased $100,000 of water from the Water Utility Fund, a business-type activity. 2. The Municipal Golf Course, an

> At the end of a fiscal year, budgetary and operating statement control accounts in the general ledger of the General Fund of Dade City had the following balances: Appropriations, $6,224,000; Estimated Other Financing Uses, $2,776,000; Estimated Revenues,

> The City of Eldon applied for a competitive grant from the state government for park improvements such as upgrading hiking trails and bike paths. On May 1, 2011, the City was notified that it had been awarded a grant of $200,000 for the program, to be re

> The Village of Baxter uses the purchases method of accounting for its inventories of supplies in the General Fund. GASB standards, however, require that the consumption method be used for the government-wide financial statements. Because its computer sys

> The Village of Darby’s budget calls for property tax revenues for the fiscal year ending December 31, 2011, of $2,660,000. Village records indicate that, on average, 2 percent of taxes levied are not collected. The county tax assessor has assessed the va

> The City of Perrin collects its annual property taxes late in its fiscal year. Consequently, each year it must finance part of its operating budget using tax anticipation notes. The notes are repaid upon collection of property taxes. On April 1, 2011, th

> GASB financial reporting standards assist users in assessing the operational accountability of a government’s business-type activities and the fiscal accountability of its governmental activities.” Do you agree or disagree with this statement? Why or why

> Choose the best answer. 1. When equipment was purchased with General Fund resources, which of the following accounts would have been debited in the General Fund? a. Expenditures. b. Equipment. c. Encumbrances. d. No entry should be made in the General Fu

> In this case, local governments receive reimbursements from the state government’s Department of Social Services Teen Assistance Program for expenditures incurred in conducting an array of locally administered programs that benefit troubled teens. The st

> How are general long-term liabilities distinguished from other long-term liabilities of the government? How does the financial reporting of general long-term liabilities differ from the financial reporting of other long-term liabilities?

> During the current fiscal year, the City of Manchester created a Printing and Sign Fund (an internal service fund) to provide custom printing and signage for city departments, predominantly those financed by the General Fund. As this is the city’s first

> Property owners in Trevor City were shocked when they recently received notice that assessed valuations on their homes had increased by an average 35 percent, based on a triennial reassessment by the County Board of Equalization. Like many homeowners in

> Using either a city’s own Web site or the GASBS 34 link of the GASB’s Web site, download either the city’s entire comprehensive annual financial report (CAFR) or, if possible, just the portion of the CAFR that contains the basic financial statements. Pri

> Name the four classes of nonexchange transactions defined by GASB standards and explain the revenue and expenditure/expense recognition rules applicable to each class.

> How does a permanent fund differ from public-purpose trusts that are reported in special revenue funds? How does it differ from private-purpose trust funds?

> If interim financial reporting to external parties is not required, why should a government bother to prepare interim financial statements and schedules? Give some examples of interim financial statements or schedules that a government should consider fo

> Explain the primary differences between ad valorem taxes, such as property taxes, and other taxes that generate derived tax revenues, such as sales and income taxes. How does accounting differ between these classes of taxes?

> Explain why expenses reported on the government-wide statement of activities for supplies used in conducting governmental activities may differ in amounts from expenditures for the same supplies reported on the statement of revenues, expenditures, and ch

> Explain the essential differences between extraordinary items and special items and how each of these items should be reported on the government-wide statement of activities.

> “Actual revenues and expenditures reported on a budget and actual comparison schedule should be prepared on the same basis as budgeted revenues and expenditures, even if a cash basis is used.” Do you agree with this statement? Why or why not?

> In 2011, Falts City began work to improve certain streets to be financed by a bond issue and supplemented by a federal grant. Estimated total cost of the project was $4,000,000; $2,500,000 was to come from the bond issue, and the balance from the federal

> If the General Fund of a certain city needs $6,720,000 of revenue from property taxes to finance estimated expenditures of the next fiscal year and historical experience indicates that 4 percent of the gross levy will not be collected, what should be the

> How does the use of encumbrance procedures improve budgetary control over expenditures?

> In what ways does the government-wide statement of net assets differ from the balance sheet for governmental funds?

> Explain why some transactions for governmental activities at the government wide level are reported differently than transactions for the General Fund. Give some examples of transactions that would be recorded in the general journals of (a) only the Gen

> Review the computer generated budgetary comparison report presented below for the Lincoln City Parks and Recreation Department as of July 1 of its fiscal year ending December 31, 2010, and respond to the questions that follow. Required a. Explain the a

> The finance director of the Town of Liberty has asked you to determine whether the appropriations, expenditures, and encumbrances comparison for Office Supplies for a certain year (reproduced as follows) presents the information correctly. You determine

> The printout of the Estimated Revenues and Revenues subsidiary ledger accounts for the General Fund of the City of Salem as of February 28, 2011, appeared as follows: Required Assuming that this printout is correct in all details and that there are no

> During July 2010, the first month of the 2011 fiscal year, the City of Marion issued the following purchase orders and contracts, Required a. Show the general journal entry to record the issuance of the purchase orders and contracts. Show entries in su

> How should one determine whether FASB or GASB standards should be followed by any particular not-for-profit organization?

> During FY 2011, the voters of the Town of Dex approved constructing and equipping a recreation center to be financed by tax-supported bonds in the amount of $3,000,000. During 2011, the following events and transactions occurred. 1. Preliminary planning

> The City of Marion adopted the following General Fund budget for fiscal year 2011: Required a. Assuming that a city ordinance mandates a balanced budget, what must be the minimum amount in the Fund Balance account of the General Fund at the beginning o

> The following information is provided about the Village of Wymette’s General Fund operating statement and budgetary accounts for the fiscal year ended June 30, 2010. Required a. Did the Village of Wymette engage in imprudent budgeting

> The following alphabetic listing displays selected balances in the governmental activities accounts of the City of Kokomo as of June 30, 2011. Prepare a (partial) statement of activities in good form. For simplicity, assume that the city does not have bu

> Refer to Case 3–1 for instructions about how to obtain the CAFR for a city of your choice. Using that CAFR, go to the required supplementary information (RSI) section, immediately following the notes to the financial statements, and locate the budgetary

> Locate a comprehensive annual financial report (CAFR) using a city’s Web site, or one from the link of the GASB’s Web site, www.gasb.org. Examine the city’s government-wide statement of activities and statement of revenues, expenditures, and changes in f

> Explain how expenditure and revenue classifications for public school systems differ from those for state and local governments.

> For which funds are budgetary comparison schedules or statements required? Should the actual revenues and expenditures on the budgetary comparison schedules be reported on the GAAP basis? Why or why not?

> Distinguish between: a. Expenditures and Encumbrances. b. Revenues and Estimated Revenues. c. Reserve for Encumbrances and Encumbrances. d. Reserve for Encumbrances and Fund Balance. e. Appropriations and Expenditures. f. Expenditures and Expenses.

> Explain the essential differences between extraordinary items and special items and how each of these items should be reported on the government-wide statement of activities.

> Why depreciation expense is typically reported as a direct expense in the government-wide statement of activities?

> The pre-closing trial balance for the Annette County Public Works Capital Project Fund is provided below. Required a. Prepare the June 30, 2011, statement of revenues, expenditures, and changes in fund balance for the capital projects fund. b. Has the

> Which standard-setting bodies have responsibility for establishing accounting and reporting standards for (1) State and local governments, (2) Business organizations, (3) Not-for-profit organizations, and (4) The federal government and its agencies an

> Explain why governmental fund financial statements are insufficient for users seeking information about operational accountability.

> The Town of Trenton has recently implemented GAAP reporting and is attempting to determine which of the following special revenue funds should be classified as “major funds” and therefore be reported in separate column

> The Case of the Vanishing Debt. Facts: A county government and a legally separate organization—the Sports Stadium Authority—entered into an agreement under which the authority issued revenue bonds to construct a new stadium. Although the intent is to mak

> Financial Statement Impact of Incurring General Long-term Debt on Behalf of Other Governments. Facts: The Bates County government issued $2.5 million of tax-supported bonds to finance a major addition to the Bates County Hospital, a legally separate orga

> Facts: Pursuant to its capital improvement plan, the City of Kirkland decided to make certain improvements to Oak Ridge Street, a residential thoroughfare located in the northern part of the city. Specifically, the project entailed purchasing 20 feet at

> Under what circumstances might a government consider an advance refunding of general obligation bonds outstanding?

> What are the GASB requirements for reporting investments held for the purpose of servicing government debt?

> Explain the essential differences between regular serial bonds and term bonds and how debt service fund accounting differs for the two types of bonds.

> What is overlapping debt? Why would a citizen care about the amount of overlapping debt reported? Why would a government care about the amount of overlapping debt reported?

> In Erikus County, the Parks and Recreation Department constructed a library in one of the county’s high growth areas. The construction was funded by a number of sources. Below is selected information related to the funding and closing of the Library Capi

> Write T if the corresponding statement is true. If the statement is false, write F and state what changes should be made to make it a true statement. 1. Activities of a general purpose government that provide the basis for GASB’s financial accounting and

> Locate a comprehensive annual financial report (CAFR) for a local government from some source on the Internet, perhaps the Web site of the governmental entity or the Governmental Accounting Standards Board’s Web site. Print a copy of the balance sheet an

> For more than 100 years, the financial statements of the Town of Brookfield have consisted of a statement of cash receipts and a statement of cash disbursements prepared by the town treasurer for each of its three funds: the General Fund, the Road Tax Fu

> Explain the criteria for determining if a governmental or enterprise fund must be reported as a major fund. What other funds should or may be reported as major funds?

> Amber City borrowed $1,000,000 secured by a 5-year mortgage note. The cash from the note was used to purchase a building for vehicle and equipment maintenance. Show how these two transactions should be recorded in the General Fund and governmental activi

> Which fund category uses the modified accrual basis of accounting? What are the recognition rules for revenues and expenditures under the modified accrual basis of accounting?

> What are the three categories of funds prescribed by GASB standards and which fund types are included in each? Do the three fund categories correspond precisely with the three activity categories described in Chapter 2? If not, how do they differ?

> “Governmental and not-for-profit organizations do not differ significantly from for-profit organizations and therefore should follow for-profit accounting and reporting standards.” Do you agree or disagree with this statement? Why or why not?

> The government-wide financial statements for the City of Arborland for a three-year period are presented on the following pages. Additional information follows: Population: Year 2011: 30,420, Year 2010: 28,291, Year 2009: 26,374. Debt limit remained

> “If a discrete presentation is used for the financial data of a component unit in the statement of net assets of a governmental financial reporting entity, there is no need for the component unit to issue a separate financial report.” Is this statement t

> Condensed government-wide financial information from the comprehensive annual financial report for the Commonwealth of Pennsylvania for the fiscal year ended June 30, 2007, is provided below. Required a. Identify significant trends that appear in the co

> The transmittal letter from the chief financial officer to the mayor and city council of Detroit that accompanies the City of Detroit’s Comprehensive Annual Financial Report for the Year Ended June 30, 2004, includes the following: Econ

> The City of Scottsdale, Arizona, provides the following report on the following page about its reserve policies on page 12 of its October 2007 financial trends booklet. Required a. Refer to Illustration 10–1. To which categories of fac

> Examine the following tables from the 2009 Financial Trend Monitoring Report for the Town of Oakdale that reports on fiscal year 2008. The performance indicators selected are total revenue and revenue per capita. The town provides three reference groups

> Write the letters a through o on a sheet of paper. Beside each letter, put a plus (+) if a high or increasing value of the item is generally associated with stronger financial condition, a minus (─) if a high or increasing value of the item is generally

> Choose the best answer. 1. Which of the following groups or parties generally has taken the most initiative to evaluate the financial condition of a city? a. Citizens. b. Managers. c. Credit market analysts. d. Legislative and oversight bodies. 2. Which

> The City of Edmond, Oklahoma, uses the Crawford Performeter® as a financial analysis tool and presents the results of this analysis in its Managements’s Discussion and Analysis in the annual audited financial statements. For

> You are a new city council person for the City of Scottsdale, Arizona. You are aware that several cities have been in the news recently for financial crises for which the council or board is being held accountable. The governing bodies have been criticiz

> For the fiscal year 2007, the City and County of Denver, Colorado, had approximately $4.9 billion in bonded debt. You are a senior accountant in the controller’s office of the City and County of Denver and have been asked to make a presentation at the ne

> You are an accountant with the national office of the National Association of State Retirement Administrators (NASRA) and have just been appointed by the membership as its representative to the Governmental Accounting Standards Advisory Council (GASAC) f

> What organizations does the governmental reporting entity include? Define primary government. How does a component unit differ from the primary government?

> “Credit or bond analysts are interested only in the financial condition of the government when determining bond ratings.” Do you agree or disagree with this statement? Explain.

> Identify some financial indicators or ratios that are designed to measure the short-term financial position of a governmental entity. Why are these measures not as useful in assessing long-term financial or economic condition?