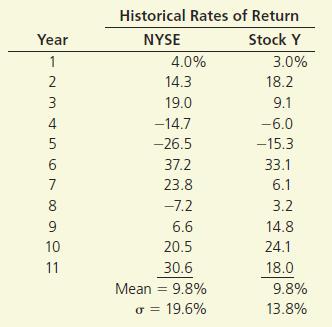

Question: You are given the following set of

You are given the following set of data:

a. Construct a scatter diagram showing the relationship between returns on Stock Y and the market. Use a spreadsheet or a calculator with a linear regression function to estimate beta.

b. Give a verbal interpretation of what the regression line and the beta coefficient show about Stock Y’s volatility and relative risk as compared with those of other stocks.

c. Suppose the regression line were exactly as shown by your graph from part b but the scatter plot of points was more spread out. How would this affect:

(1) the firm’s risk if the stock is held in a one-asset portfolio, and

(2) the actual risk premium on the stock if the CAPM holds exactly?

d. Suppose the regression line were downward sloping and the beta coefficient were negative. What would this imply about:

(1) Stock Y’s relative risk,

(2) its correlation with the market, and

(3) its probable risk premium?

Transcribed Image Text:

Historical Rates of Return Year NYSE Stock Y 1 4.0% 3.0% 2 14.3 18.2 3 19.0 9.1 4 -14.7 -6.0 -26.5 -15.3 37.2 33.1 7 23.8 6.1 8 -7.2 3.2 9 6.6 14.8 10 20.5 24.1 11 30.6 18.0 Mean = 9.8% 9.8% %3D o = 19.6% 13.8%

> How is the value of a financial option affected by: (a) the current price of the underlying asset, (b) the exercise (or strike) price, (c) the risk-free rate, (d) the time until expiration (or maturity), and (e) the variance of returns on the asset?

> Define each of the following terms: a. MM Proposition I without taxes and with corporate taxes b. MM Proposition II without taxes and with corporate taxes c. Miller model d. Adjusted present value (APV) model e. Value of debt tax shield f. Equity as an o

> Your firm’s CEO has just learned about options and how your firm’s equity can be viewed as an option. Why might he want to increase the riskiness of the firm, and why might the bondholders be unhappy about this?

> Modigliani and Miller assumed that firms do not grow. How does positive growth change their conclusions about the value of the levered firm and its cost of capital?

> A utility company is allowed to charge prices high enough to cover all costs, including its cost of capital. Public service commissions are supposed to take actions that stimulate companies to operate as efficiently as possible in order to keep costs, an

> Explain, in your own words, how MM uses the arbitrage process to prove the validity of Proposition I. Also, list the major MM assumptions and explain why each of these assumptions is necessary in the arbitrage proof.

> Greene Sisters has a DSO of 20 days. The company’s average daily sales are $20,000. What is the level of its accounts receivable? Assume there are 365 days in a year.

> The Jimenez Corporation’s forecasted 2016 financial statements follow, along with some industry average ratios. Calculate Jimenez’s 2016 forecasted ratios, compare them with the industry average data, and comment brief

> How can a company use a bankruptcy to abrogate labor contracts? Has this occurred in certain industries in recent years?

> Data for Lozano Chip Company and its industry averages follow. a. Calculate the indicated ratios for Lozano. b. Construct the extended DuPont equation for both Lozano and the industry. c. Outline Lozano’s strengths and weaknesses as

> The Kretovich Company had a quick ratio of 1.4, a current ratio of 3.0, a days sales outstanding of 36.5 days (based on a 365-day year), total current assets of $810,000, and cash and marketable securities of $120,000. What were Kretovich’s annual sales?

> Complete the balance sheet and sales information in the table that follows for J. White Industries using the following financial data: Total assets turnover: 1.5 Gross profit margin on sales: (Sales 2 Cost of goods sold)/Sales 5 25% Total liabilities-

> The Morris Corporation has $600,000 of debt outstanding, and it pays an interest rate of 8% annually. Morris’ annual sales are $3 million, its average tax rate is 40%, and its net profit margin on sales is 3%. If the company does not maintain a TIE ratio

> You are considering an investment in either individual stocks or a portfolio of stocks. The two stocks you are researching, Stock A and Stock B, have the following historical returns: a. Calculate the average rate of return for each stock during the 5-ye

> Stock R has a beta of 1.5, Stock S has a beta of 0.75, the expected rate of return on an average stock is 13%, and the risk-free rate is 7%. By how much does the required return on the riskier stock exceed that on the less risky stock?

> You have a $2 million portfolio consisting of a $100,000 investment in each of 20 different stocks. The portfolio has a beta of 1.1. You are considering selling $100,000 worth of one stock with a beta of 0.9 and using the proceeds to purchase another sto

> Suppose you manage a $4 million fund that consists of four stocks with the following investments: If the market’s required rate of return is 14% and the risk-free rate is 6%, what is the fund’s required rate of return?

> Your retirement fund consists of a $5,000 investment in each of 15 different common stocks. The portfolio’s beta is 1.20. Suppose you sell one of the stocks with a beta of 0.8 for $5,000 and use the proceeds to buy another stock whose beta is 1.6. Calcul

> As an equity analyst you are concerned with what will happen to the required return to Universal Toddler Industries’ stock as market conditions change. Suppose rRF 5 5%, rM 5 12%, and bUTI 5 1.4. a. Under current conditions, what is rUTI, the required r

> Carter Enterprises can issue floating-rate debt at LIBOR + 2% or fixed-rate debt at 10%. Brence Manufacturing can issue floating-rate debt at LIBOR + 3.1% or fixed-rate debt at 11%. Suppose Carter issues floating-rate debt and Brence issues fixed-rate de

> Suppose rRF 5 5%, rM 5 10%, and rA 5 12%. a. Calculate Stock A’s beta. b. If Stock A’s beta were 2.0, then what would be A’s new required rate of return?

> The market and Stock J have the following probability distributions: a. Calculate the expected rates of return for the market and Stock J. b. Calculate the standard deviations for the market and Stock J Probability IM r, 0.3 15% 20% 0.4 9 5 0.3 18 1

> A stock’s return has the following distribution: Calculate the stock’s expected return and standard deviation. Rate of Return if Probability of This Demand Occurring Demand for the This Demand Company's Products

> An analyst has modeled the stock of a company using the Fama-French threefactor model. The risk-free rate is 5%, the market return is 10%, the return on the SMB portfolio (rSMB) is 3.2%, and the return on the HML portfolio (rHML) is 4.8%. If ai 5 0, bi 5

> Suppose that the risk-free rate is 5% and that the market risk premium is 7%. What is the required return on (1) the market, (2) a stock with a beta of 1.0, and (3) a stock with a beta of 1.7?

> AA Industries’ stock has a beta of 0.8. The risk-free rate is 4% and the expected return on the market is 12%. What is the required rate of return on AA’s stock?

> Your investment club has only two stocks in its portfolio. $20,000 is invested in a stock with a beta of 0.7, and $35,000 is invested in a stock with a beta of 1.3. What is the portfolio’s beta?

> You have observed the following returns over time: Copyright Assume that the risk-free rate is 6% and the market risk premium is 5%. a. What are the betas of Stocks X and Y? b. What are the required rates of return on Stocks X and Y? c. What is the re

> Assume that you recently graduated and landed a job as a financial planner with Cicero Services, an investment advisory company. Your first client recently inherited some assets and has asked you to evaluate them. The client owns a bond portfolio with $1

> Define and discuss how to calculate a bond’s coupon rate, current yield, expected capital gains yield for the current year, yield to maturity (YTM), and yield to call (YTC). What might be some representative numbers for a strong company like GE today? Ar

> What is the implied interest rate on a Treasury bond ($100,000) futures contract that settled at 100’16? If interest rates increased by 1%, what would be the contract’s new value?

> Financial assets such as mortgages, credit card receivables, and auto loan receivables are often bundled up, placed in a bank trust department, and then used as collateral for publicly traded bonds. Bond prices typically rise when interest rates decline,

> What is a bond rating, and how do ratings affect bonds’ prices and yields? Who rates bonds, and what are some of the factors the rating agencies consider? Is it possible for a given company to have several different bonds outstanding that have different

> Would a bond be more or less desirable if you learned that it has a sinking fund that requires the company to redeem, say, 10% of the original issue each year beginning in 2019, either through open market purchases or by calling the redeemed bonds at par

> Define the terms interest rate risk and reinvestment rate risk. How are these risks affected by maturities, call provisions, and coupon rates? Why might different types of investors view these risks differently? How would they affect the yield curve? Ill

> What is the difference between a diversifiable risk and a nondiversifiable risk? Should stock portfolio managers try to eliminate both types of risk?

> Has the validity of the CAPM been confirmed through empirical tests?

> What is the difference between a historical beta, an adjusted beta, and a fundamental beta? Does it matter which beta is used, and if so, which is best?

> What is the Security Market Line (SML)? What information is developed in the Capital Market Line analysis and then carried over and used to help specify the SML? For practical applications as opposed to theoretical considerations, which is more relevant,

> What is an efficient portfolio? What is the Capital Market Line (CML), how is it related to efficient portfolios, and how does it interface with an investor’s indifference curve to determine the investor’s optimal portfolio? Is it possible that two ratio

> Define the terms covariance and correlation coefficient. How are they related to one another, and how do they affect the required rate of return on a stock? Would correlation affect its required rate of return if a stock were held (say, by the company’s

> A Treasury bond futures contract has a settlement price of 89’08. What is the implied annual yield?

> What is the difference between a spot rate and a forward rate? How can forward rates be used for hedging purposes? Why would hedging occur?

> If a publicly traded company has a large number of undiversified investors, along with some who are well diversified, can the undiversified investors earn a rate of return high enough to compensate them for the risk they bear? Does this affect the compan

> You are given the following set of data: a. Use a spreadsheet (or a calculator with a linear regression function) to determine Stock X’s beta coefficient. b. Determine the arithmetic average rates of return for Stock X and the NYSE over

> The beta coefficient of an asset can be expressed as a function of the asset’s correlation with the market as follows: a. Substitute this expression for beta into the Security Market Line (SML), Equation 3-9. This results in an alterna

> Stock A has an expected return of 12% and a standard deviation of 40%. Stock B has an expected return of 18% and a standard deviation of 60%. The correlation coefficient between Stocks A and B is 0.2. What are the expected return and standard deviation o

> An analyst has modeled the stock of Crisp Trucking using a two-factor APT model. The risk-free rate is 6%, the expected return on the first factor (r1) is 12%, and the expected return on the second factor (r2) is 8%. If bi15 0.7 and bi2 5 0.9, what is Cr

> The standard deviation of stock returns for Stock A is 40%. The standard deviation of the market return is 20%. If the correlation between Stock A and the market is 0.70, then what is Stock A’s beta?

> Define the following terms, using graphs or equations to illustrate your answers wherever feasible: a. Portfolio; feasible set; efficient portfolio; efficient frontier b. Indifference curve; optimal portfolio c. Capital Asset Pricing Model (CAPM); Capita

> a. Suppose Asset A has an expected return of 10% and a standard deviation of 20%. Asset B has an expected return of 16% and a standard deviation of 40%. If the correlation between A and B is 0.35, what are the expected return and standard deviation for a

> Differentiate between (a) stand-alone risk and (b) risk in a portfolio context. How are they measured and are both concepts relevant for investors? What is securitization? How is securitization supposed to help banks and S&Ls manage risks and increas

> The Zinn Company plans to issue $10,000,000 of 20-year bonds in June to help finance a new research and development laboratory. The bonds will pay interest semiannually. It is now November, and the current cost of debt to the high-risk biotech company is

> What are the advantages of the corporate for mover a sole proprietorship or a partnership? What are the disadvantages of this form?

> What is presumed to be the primary goal of financial management? How is this goal related to other societal goals and considerations? Is this goal consistent with the basic assumptions of microeconomics? Are managers’ actions always consistent with this

> What was the global economic crisis? This is a really big question, so specifically, explain how in our interconnected global economy a decrease in housing prices in large U.S. cities ended up bankrupting Norwegian retirees.

> Assume that you recently graduated and have just reported to work as an investment advisor at the brokerage firm of Balik and Kiefer Inc. One of the firm’s clients is Michelle Della Torre, a professional tennis player who has just come to the Unite

> Differentiate between (a) stand-alone risk and (b) risk in a portfolio context. How are they measured, and are both concepts relevant for investors? What is presumed to be the primary goal of financial management? How is this goal related to other societ

> What is the Capital Asset Pricing Model (CAPM)? What are some of its key assumptions? Has it been empirically verified? What is the role of the Security Market Line in the CAPM? Suppose you had to estimate the required rate of return on a stock using the

> Assume you have just been hired as a financial analyst by Tennessee Sunshine Inc., a mid-sized Tennessee company that specializes in creating exotic sauces from imported fruits and vegetables. The firm’s CEO, Bill Stooksbury, recently returned from an in

> a. Differentiate between the terms expected rate of return, required rate of return, and historical rate of return as they are applied to common stocks. b. If you found values for each of these returns for several different stocks, would the values for

> If investors’ aversion to risk increased, would the risk premium on a high beta stock increase by more or less than that on a low-beta stock? Explain.

> Define the following terms, using graphs or equations to illustrate your answers where feasible. a. Risk in general; stand-alone risk; probability distribution and its relation to risk b. Expected rate of return, r⁄ c. Continuous probability d

> If a company’s beta were to double, would its expected return double?

> Edmund Enterprises recently made a large investment to upgrade its technology. Although these improvements won’t have much of an impact on performance in the short run, they are expected to reduce future costs significantly. What impact will this investm

> What is a firm’s fundamental, or intrinsic, value? What might cause a firm’s intrinsic value to be different from its actual market value?

> What are the three principal forms of business organization? What are the advantages and disadvantages of each?

> Security A has an expected return of 7%, a standard deviation of returns of 35%, a correlation coefficient with the market of 20.3, and a beta coefficient of 21.5. Security B has an expected return of 12%, a standard deviation of returns of 10%, a corre

> The probability distribution of a less risky return is more peaked than that of a riskier return. What shape would the probability distribution have for (a) completely certain returns and (b) completely uncertain returns?

> Hager’s Home Repair Company, a regional hardware chain that specializes in “do it yourself” materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternat

> Sam Strother and Shawna Tibbs are vice presidents of Mutual of Seattle Insurance Company and co_directors of the company’s pension fund management division. An important new client, the North-Western Municipal Alliance, has requested that Mutual of Seat

> Assume that you have just been hired as a financial analyst by Triple Play Inc., a mid-sized California company that specializes in creating high-fashion clothing. Because no one at Triple Play is familiar with the basics of financial options, you have b

> The current price of a stock is $20. In 1 year, the price will be either $26 or $16. The annual risk-free rate is 5%. Find the price of a call option on the stock that has a strike price of $21 and that expires in 1 year. (Hint: Use daily compounding.)

> Use the Black-Scholes Model to find the price for a call option with the following inputs: (1) current stock price is $30, (2) strike price is $35, (3) time to expiration is 4 months, (4) annualized risk-free rate is 5%, and (5) variance of stock ret

> Assume that you have been given the following information on Purcell Industries: According to the Black-Scholes option pricing model, what is the option’s value? Current stock price = $15 Time to maturity of option = 6 months Varian

> The exercise price on one of Flanagan Company’s options is $15, its exercise value is $22, and its time value is $5. What are the option’s market value and the price of the stock?

> The current price of a stock is $15. In 6 months, the price will be either $18 or $13. The annual risk-free rate is 6%. Find the price of a call option on the stock that has a strike price of $14 and that expires in 6 months. (Hint: Use daily compounding

> Arnot International’s bonds have a current market price of $1,200. The bonds have an 11% annual coupon payment, a $1,000 face value, and 10 years left until maturity. The bonds may be called in 5 years at 109% of face value (call price 5 $1,090). a. What

> Suppose Hillard Manufacturing sold an issue of bonds with a 10-year maturity, a $1,000 par value, a 10% coupon rate, and semiannual interest payments. a. Two years after the bonds were issued, the going rate of interest on bonds such as these fell to 6%.

> Because of a recession, the inflation rate expected for the coming year is only 3%. However, the inflation rate in Year 2 and thereafter is expected to be constant at some level above 3%. Assume that the real risk-free rate is r*= 2% for all maturities a

> Does interest rate parity imply that interest rates are the same in all countries?

> Assume that the real risk-free rate, r*, is 3% and that inflation is expected to be 8% in Year 1, 5% in Year 2, and 4% thereafter. Assume also that all Treasury securities are highly liquid and free of default risk. If 2-year and 5-year Treasury notes bo

> The real risk-free rate is 2%. Inflation is expected to be 3% this year, 4% next year, and then 3.5% thereafter. The maturity risk premium is estimated to be 0.0005 × (t-1), where t = number of years to maturity. What is the nominal interest rate on a 7-

> An investor has two bonds in his portfolio. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity equal to 9.6%. One bond, Bond C, pays an annual coupon of 10%; the other bond, Bond Z, is a zero coupon bond. Assuming that

> A bond trader purchased each of the following bonds at a yield to maturity of 8%. Immediately after she purchased the bonds, interest rates fell to 7%. What is the percentage change in the price of each bond after the decline in interest rates? Fill in t

> Absalom Motors’ 14% coupon rate, semiannual payment, $1,000 par value bonds that mature in 30 years are callable 5 years from now at a price of $1,050. The bonds sell at a price of $1,353.54, and the yield curve is flat. Assuming that interest rates in t

> A bond that matures in 7 years sells for $1,020. The bond has a face value of $1,000 and a yield to maturity of 10.5883%. The bond pays coupons semiannually. What is the bond’s current yield?

> You just purchased a bond that matures in 5 years. The bond has a face value of $1,000 and has an 8% annual coupon. The bond has a current yield of 8.21%. What is the bond’s yield to maturity?

> A 10-year, 12% semiannual coupon bond with a par value of $1,000 may be called in 4 years at a call price of $1,060. The bond sells for $1,100. (Assume that the bond has just been issued.) a. What is the bond’s yield to maturity? b. What is the bond’s cu

> The Brownstone Corporation’s bonds have 5 years remaining to maturity. Interest is paid annually, the bonds have a $1,000 par value, and the coupon interest rate is 9%. a. What is the yield to maturity at a current market price of: (1) $829 or (2) $1,

> The Garraty Company has two bond issues outstanding. Both bonds pay $100 annual interest plus $1,000 at maturity. Bond L has a maturity of 15 years, and Bond S has a maturity of 1 year. a. What will be the value of each of these bonds when the going rate

> What is a Eurodollar? If a French citizen deposits $10,000 in Chase Bank in New York, have Eurodollars been created? What if the deposit is made in Barclays Bank in London? Chase’s Paris branch? Does the existence of the Eurodollar market make the Federa

> Thatcher Corporation’s bonds will mature in 10 years. The bonds have a face value of $1,000 and an 8% coupon rate, paid semiannually. The price of the bonds is $1,100. The bonds are callable in 5 years at a call price of $1,050. What is their yield to ma

> Renfro Rentals has issued bonds that have a 10% coupon rate, payable semiannually. The bonds mature in 8 years, have a face value of $1,000, and a yield to maturity of 8.5%. What is the price of the bonds?

> The real risk-free rate is 3%, and inflation is expected to be 3% for the next 2 years. A 2-year Treasury security yields 6.3%. What is the maturity risk premium for the 2-year security?

> A Treasury bond that matures in 10 years has a yield of 6%. A 10-year corporate bond has a yield of 9%. Assume that the liquidity premium on the corporate bond is 0.5%. What is the default risk premium on the corporate bond?

> The real risk-free rate of interest is 4%. Inflation is expected to be 2% this year and 4% during the next 2 years. Assume that the maturity risk premium is zero. What is the yield on 2-year Treasury securities? What is the yield on 3-year Treasury secur

> Heath Foods’ bonds have 7 years remaining to maturity. The bonds have a face value of $1,000 and a yield to maturity of 8%. They pay interest annually and have a 9% coupon rate. What is their current yield?

> Jackson Corporation’s bonds have 12 years remaining to maturity. Interest is paid annually, the bonds have a $1,000 par value, and the coupon interest rate is 8%. The bonds have a yield to maturity of 9%. What is the current market price of these bonds?

> Suppose you and most other investors expect the inflation rate to be 7% next year, to fall to 5% during the following year, and then to remain at a rate of 3% thereafter. Assume that the real risk-free rate, r*, will remain at 2% and that maturity risk p