Question: Airport Complex was founded in Northern Europe

Airport Complex was founded in Northern Europe in the early 1960s, and at the time it primarily served as a domestic airport. During the 1980s, flights to foreign destinations became an ever more vital activity for the airport. Today, the airport functions as a hub for a large portion of Nordic air traffic. The fact that the airport is a hub means that a great deal (approximately 35-40 per cent) of the airport’s passengers only touch down at the airport to catch another plane to a new destination. The airport remained state property until the late-2000s when the airport was transformed into a private company, though the state held on to a substantial ownership share.

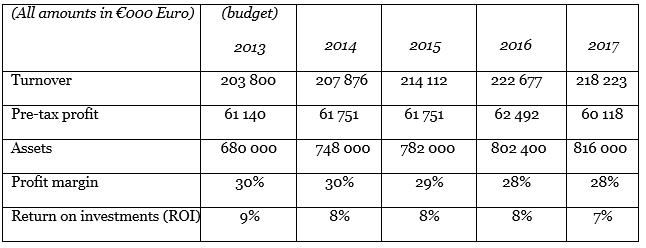

Naturally, this generated an increased focus on the airport’s financial performance, which, however, boosted healthy profit margins. This also constituted the background for the continued expansion of the airport, which today has placed itself as an airport entering the medium-size class of Nordic airports. The profit margins of the airport (see Exhibit 1) have suffered a decline over the past few years due to a combination of deteriorating income as a result of a fall in domestic traffic, costs that have not decreased correspondingly and the abolition of tax-free sales in 2012.

Investors have consequently requested that the airport commit itself more to a focus on the overall profitability measured against the invested capital. Accordingly, the management has now decided that the efficiency of the airport should be subject to assessment. An airport is characterized by the fact that almost all costs are capacity costs. This is partly due to significant investment in buildings, runways and technology, but also to the large staff which handles the administration, operation and maintenance of the airport. The management suspects that the costs are not sufficiently adjusted to the income. In particular, the management finds it difficult to get an overview of how the various business areas utilize the airport’s resources and services and thus contribute to the bottom line of the airport.

BUSINESS AREAS

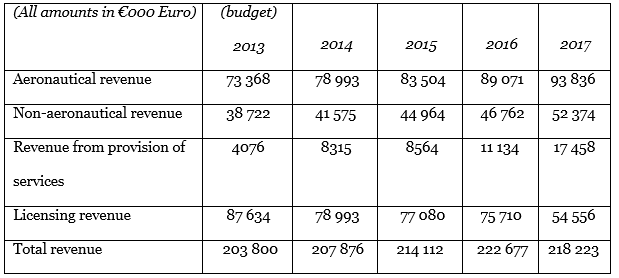

The revenue of Airport Complex derived from five different areas; take-off duties from air traffic, passenger fees, rental income from property, licensing income from the airport’s shopping centre and sundry income related to provision of services in the airport. Each of the five business areas is briefly outlined in the following discussion.

TAKE-OFF DUTIES

Every time an aircraft departs from the airport, the airline pays a take-off duty. The duty is calculated on the basis of the type and weight of the aircraft. The income is related to the airline’s use of the airport’s control of the air space, runways, technical equipment such as runway lights, meteorological equipment, facilities on the gate for cleaning the aircraft, changing the air in the aircraft, fuelling, de-icing, etc. After the aircraft has landed, it is guided to a gate. If the pilot does not know the airport, airport personnel will guide the aircraft to its gate. There are two types of gates: gates served by a building, i.e. the gate is connected to one of the airport’s terminals allowing passengers to leave the aircraft and enter the terminal directly, and remote gates where the aircraft is parked somewhere else in the airport area from where passengers are subsequently transported by buses to one of the airport terminals. Airlines are in broad consent that building-served gates service passengers far better than remote gates. Still, prices for building-served and remote gates are currently not differentiated, though the management has discussed this question. In addition to the take-off duties, a stopover duty is also payable depending on how long the aircraft stays in the gate. The first hour, however, is free.

PASSENGER FEES

Take-off and stopover duties are complemented by a passenger fee per passenger on the aircraft. These three sources of income are collectively referred to as traffic income. Passenger fees depend solely on the number of passengers. The passengers’ points of departure and final destination are thus not relevant to the calculation of the fee. In principle, passenger fees relate to the passengers’ use of the airport area and services. This covers for instance buildings, transport to the terminal, service information, luggage handling and passenger areas in the airport. A differentiation on the prices for domestic passengers and those travelling to destinations abroad was previously in force, but EU competition rules have now put an end to this differentiation. It has been discussed whether there should be different passenger fees for passengers who merely touch down at the airport, but never leave the aircraft (transit passengers) as opposed to passengers who only land at the airport in order to get on a new plane (transfer passengers), as these passengers do not use the airport’s landside areas. Every year, the relation between take-off duties and passenger duties is also discussed, as there are occasional imbalances in the case of small aircraft with many passengers and large aircraft with few passengers.

RENTAL INCOME

Parts of the airport buildings are let out to airlines, travel agencies and shops. This revenue is collectively referred to as rental income. Prices are fixed as per square metre and vary with the use of the rented premises and its location within the airport area. Besides yielding a reasonable profit margin, rental income must in principle cover wear and tear, maintenance, use of common facilities such as toilets, lifts, etc.

SERVICES

In connection with renting of buildings, supplementary services such as cleaning, security guard surveillance of rooms and shops, access to canteens and to the airport’s computer network are also offered. This income is collectively referred to as income from provision of services and is of course related to the airport’s costs in connection with these services. In recent years, this income has seen a rapid increase as a result of the airport seizing ever more opportunities for expanding the range of its services offered to the airport’s customers.

LICENSING INCOME

Finally, the airport generates income from licensing agreements entered into with shops and agencies that rent premises in the airport. In addition to rent for the premises, a duty is payable for running a shop within the airport’s area. The licensing agreements are based on the payment of a certain share of the turnover of shops and agencies to the airport. This income is collectively referred to as licensing income. In return, the airport takes on costs for decoration and marketing of the shopping centre such as signs, brochures, campaigns and information staff. Campaigns are budgeted separately, though there is no connection between the budgeting of campaigns and that of licensing agreements. The revenue of Airport Complex is shown in Exhibit 2.

ORGANIZATION

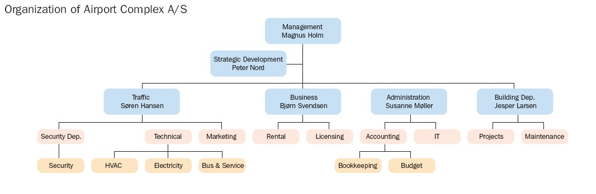

The organization of Airport Complex is a result of a continuous development of the company. Originally, everything was collected under the traffic department, as there were no other business activities. As other commercial activities and letting out of premises were developed, the business area was isolated. Immediately after this separation, the need for a distinct building department was recognized, and the new department was established. In connection with the transfer from a state enterprise to a private undertaking, the administrative activities were collected under their own organizational area. Figure 1 shows the organization plan of Airport Complex.

FINANCIAL MANAGEMENT

The accounting department handles the company’s financial control. The bookkeeping department takes care of the day-to-day invoicing and bookkeeping of the company’s transactions and of the company’s financial accounting and tax accounting. The budget department is in charge of the coordination of budgets, whereas part budgets are prepared in the individual departments, which subsequently report their budget to the budget department. The budgets are entered into the airport’s financial control system, which at the same time ensures that the individual department is only able to view its own budgets. Subsequently, the total budget is subject to approval first by the management and then by the board. The exact budgeting is of course very different from one

department to the other, depending on the functions of each department and the people responsible for the budget of the department. Nevertheless, some general comments can be made on the airport’s budget procedure. Staff budgets are normally prepared on the basis of a combination of price and amount per staff category. The remaining costs are predominantly provided for in the budget as a fixed amount. Depreciation is not allocated to the individual departments, but is estimated as a total amount by the budget department. The budget for traffic income is based on a forecast of the number of different types of aircraft. For each type of plane, the average weight and the average number of passengers are calculated and subsequently multiplied by the current take-off and passenger fees and the number of planes of that type. Rental income is estimated on the basis of the number of square metres relative to the average rent per square metre. Different prices per square metre are used depending on the type of building, use and location. The buildings may typically be divided into terminal buildings, office buildings, workshops, hangars, and warehouses. The income from provision of services is estimated on the basis of expected sales measured as an amount, and finally, the licensing income is estimated as expected turnover per shop type multiplied by the licence percentage.

OUTLINE OF DEPARTMENTS

Strategic development

The department is situated in the administrative office building. It was established three years ago with the task of supporting the management and the board in their work with strategic development of the airport. The department employs 4-5 people who make analyses of the operation of the airport and perform benchmarking analysis of the company compared to other airports. The department typically works on 3-4 projects at a time. Examples of projects are:

• the profitability of future extension projects;

• analyses of traffic statistics and forecasts of future traffic development;

• strategies for the information structure in the airport, including the future extension of the network and the number of services implemented in the network.

Traffic department

The traffic department has the overall responsibility for the development of the airport’s traffic activities. The department handles traffic-related security and co-ordination with the aviation authorities, which are in charge of the actual control of the airspace, i.e. permission to take off and land. The traffic department is also the most wage consuming department since a major part of the airport staff is employed here.

Technical departments

The complicated technical structure of the airport such as traffic and passenger co-ordination systems, bridges from airport buildings to the aircraft, runway lights, etc. is handled by the technical department. The department has three sub-departments: electricity, HVAC, and buses and service. The department takes care of these same functions for the rest of the airport.

Electricity department

The electricity department employs 125 employees on an annual basis. The department is divided between five area managers, each responsible for specific parts of the airport. However, the department seeks to maintain a certain degree of job rotation to ensure that the employees acquire a high level of knowledge within all job functions in the department. Apart from vehicles, the department is responsible for a great deal of technical equipment, cranes, lifts, etc. The tasks in the department vary from mounting and repairing of control and marking equipment in connection with the runways, to maintenance of the airport’s technical equipment and more ordinary electricity work in connection with the airport buildings. Work in connection with the airport buildings is co-ordinated by the building department, apart from work in connection with the airport’s rented property, which is coordinated by the rental department. The electricity department is naturally also involved in the implementation of the airport’s network, which is performed on the basis of requirements from the IT department.

HVAC department

The HVAC department employs approximately 150 people annually, and the department is divided on the basis of geographical areas in the airport. The division is as follows: airside undeveloped areas, airside developed areas, terminals, and finally, other landside buildings. Each area has its own head of department. Like the electricity department, the HVAC department has at its disposal a large amount of technical equipment used in its daily work. The major part of the tasks of the department is coordinated with the building department.

Bus and service department

The bus and service department are responsible for transporting the passengers to the terminals and for servicing the runways and other outdoor areas. The service primarily consists of maintenance of the green areas of the airport and of snow removal, and the service department employs 25 people. The bus department employs approximately 50 chauffeurs who are responsible mainly for transporting the passengers to and from the aircraft, but who sometimes also function as guides for aircraft whose pilots do not know the airport.

Marketing department

The marketing department is in charge of conducting negotiations with both airlines that already use the airport and airlines that wish to use the airport in the future. This applies to passenger traffic as well as freight traffic. The department employs six people on average.

Security department

Traditionally, airports are always associated with large security risks. Therefore, security is an important work area. The security department is thus responsible for monitoring the security in the airport. The main tasks of the security department are outdoor area surveillance, indoor security

check of passengers and screening of luggage, and security service in connection with the airport’s own premises and rented premises. This includes security checking of all passengers and screening of luggage. If the airport uses external artisans in connection with the activities of the building department or the technical department, these will be constantly monitored by a security guard. Furthermore, the security personnel are responsible for security surveillance of rented premises. On an annual basis, the area surveillance function employs 30 people who always work together in teams of two. Each team has at its disposal a cross-country vehicle, which enables them to turn out quickly to any place in the airport. They communicate with the central security function on a current basis via the internal communication system, which also includes GPS surveillance of all vehicles. The system has just recently been fully implemented and is controlled by the IT department. Apart from a meeting room in the terminal building, the department has at its disposal three smaller buildings located in opposite parts of the airport. There are always three teams working at the same time and their activities are coordinated by the central security service, which is manned by the security manager in charge and an assistant. The indoor security check function is manned in relation to the expected number of passengers during the day and employs approximately 70 people on an annual basis. The airport is divided into a landside and an airside area. The airside area can only be accessed through the security lock with a valid ticket and after screening of hand luggage and scanning of the passenger. The landside area, on the other hand, is accessible to everybody. There are three security locks in the airport that are manned according to the expected passenger flow during the day. Each lock is manned by three security employees who are in constant radio contact with the security manager in charge. Apart from this, two to three security employees are constantly patrolling the airside of the airport as well as the landside terminal areas. Moreover, both the indoor and the outdoor security personnel also function as security service in connection with the rented premises in the airport. The most cost intensive item in the security department is therefore staff costs and staff related costs such as uniforms and security courses. Furthermore, the department has at its disposal considerable assets such as cars, and security equipment such as scanners, X-ray equipment, etc.

Business department

The main activities in the business department are renting of areas as well as buildings and licensing agreements with retailers, restaurants, car hire firms, etc. The eight employees in the rental department administer the rental agreements and are responsible for finding suitable premises for this purpose. Extensions, renovation and maintenance of the rented premises are coordinated with the technical department and the building department. The 12 employees in the licensing department draw up agreements on how-to carry-on business in the airport areas, including agreements on the turnover-related fees to be paid for this. The promotion of the shopping centre is planned and carried out by the business department. The extension of the shopping centre is co- ordinated with the project department.

Administrative department

This department handles the overall day-to-day administration in connection with invoicing, bookkeeping and cash. Furthermore, the IT department, which is part of the administrative department, is responsible for the airport’s network which is used by the airport’s own departments as well as other uses of the airport. This applies to both networks for administrative use, for traffic monitoring and for signboards in the airport. Moreover, access to the airport’s network and support in this connection are let out. The administrative department employs 120 people on an annual basis of which approximately half are employed in the IT department.

Building department

The project department is responsible for the continuous extension of the airport, i.e. the strategic planning in collaboration with the management as well as the actual project management.

Approximately 20 people are employed on an annual basis to perform these tasks. The operative part is placed with the maintenance department, which is responsible for the continuous maintenance of both the airport area and the buildings, and which employs approximately 80 people. Exemptions are HVAC and technical appliances, which are the responsibility of the technical department under the traffic unit.

REQUIREMENTS:

1. Comment on the financial management of Airport Complex.

2. Discuss the problems and opportunities connected with assessing the profitability of the different services offered by the airport to the airlines and their customers. You are, among other things, asked to consider whether you would recommend the use of Full Cost, Activity Based Costing or Contribution Margin Concept to the company and state the reasons for your recommendation.

3. Draw up a reasoned suggestion for how an assessment of the productivity of selected departments can be organized, including an indication of the financial and non-financial measures that can be used.

4. Discuss the methods used by Airport Complex for budgeting revenue and costs and give reasoned suggestions for improvements.

Transcribed Image Text:

(All amounts in €o0o Euro) (budget) 2013 2014 2015 2016 2017 Turnover 203 800 207 876 214 112 222 677 218 223 Pre-tax profit 61 140 61 751 61 751 62 492 бо 118 Assets 680 000 748 o00 782 000 802 400 816 000 Profit margin 30% 30% 29% 28% 28% Return on investments (ROI) 9% 8% 8% 8% 7% (All amounts in €o00 Euro) (budget) 2013 2014 2015 2016 2017 Aeronautical revenue 73 368 78 993 83 504 89 071 93 836 Non-aeronautical revenue 38 722 41 575 44 964 46 762 52 374 Revenue from provision of 4076 8315 8564 11 134 17 458 services Licensing revenue 87 634 78 993 77 080 75 710 54 556 Total revenue 203 800 207 876 214 112 222 677 218 223 Organization of Airport Complex A/S Management Magnus Holm Strategie Development Peter Nord raffie Soren Hansen Business Bjøm Svendsen Building Dep. Jesper Larsen Administration Susanne Moller Security Dep. Technical Marketing Rental Licensing Accounting IT Projects Maintenance Security HVAC Electricity Bus & Service Bookkeeping Budget

> Use Bartlett’s test at the 0.05 level of significance to test for homogeneity of variances in Exercise 13.6 on page 519. Exercise 13.6: A study measured the sorption (either absorption or adsorption) rates of three different types of o

> A random variable X follows a negative binomial distribution with parameters k = 5 and p [i.e.,b ∗ (x; 5, p)]. Furthermore, we know that p follows a uniform distribution on the interval (0, 1). Find the Bayes estimate of p under the squared-error loss fu

> Use Cochran’s test at the 0.01 level of significance to test for homogeneity of variances in Exercise 13.4 on page 519. Exercise 13.4: Immobilization of free-ranging white-tailed deer by drugs allows researchers the opportunity to clos

> Six different machines are being considered for use in manufacturing rubber seals. The machines are being compared with respect to tensile strength of the product. A random sample of four seals from each machine is used to determine whether the mean tens

> (a) Fit a multiple regression equation of the form μY |x = β0 + β1x + β2x2 to the data of Example 11.8 on page 420. (b) Estimate the yield of the chemical reaction for a temperature of 225 ◦ C.

> The following is a set of coded experimental data on the compressive strength of a particular alloy at various values of the concentration of some additive: (a) Estimate the quadratic regression equation μY |x = β0 + Î&s

> An experiment was conducted in order to determine if cerebral blood flow in human beings can be predicted from arterial oxygen tension (millimeters of mercury). Fifteen patients participated in the study, and the following data were collected: Estimat

> An experiment was conducted on a new model of a particular make of automobile to determine the stopping distance at various speeds. The following data were recorded. (a) Fit a multiple regression curve of the form μD|v = β0 +

> Rayon whiteness is an important factor for scientists dealing in fabric quality. Whiteness is affected by pulp quality and other processing variables. Some of the variables include acid bath temperature, â—¦ C (x1); cascade acid concent

> A client from the Department of Mechanical Engineering approached the Consulting Center at Virginia Tech for help in analyzing an experiment dealing with gas turbine engines. The voltage output of engines was measured at various combinations of blade spe

> For the quadratic model of Exercise 12.51(b), give estimates of the variances and covariances of the estimates of β1 and β11. Exercise 12.51(b): The following is a set of data for y, the amount of money (in thousands of dollars)

> For the model of Exercise 12.50(a), test the hypothesis H0: β4 = 0, H1: β4 ≠0. Use a P-value in your conclusion. Exercise 12.50(a): For the punter data in Case Study 12.2, an additional response, â€

> Suppose that a sample consisting of 5, 6, 6, 7, 5, 6, 4, 9, 3, and 6 comes from a Poisson population with mean λ. Assume that the parameter λ follows a gamma distribution with parameters (3, 2). Under the squared-error loss function, find the Bayes estim

> The following is a set of data for y, the amount of money (in thousands of dollars) contributed to the alumni association at Virginia Tech by the Class of 1960, and x, the number of years following graduation: (a) Fit a regression model of the type &Ici

> For the punter data in Case Study 12.2, an additional response, “punting distance,” was also recorded. The average distance values for each of the 13 punters are given. (a) Using the distance data rather than the hang

> The electric power consumed each month by a chemical plant is thought to be related to the average ambient temperature x1, the number of days in the month x2, the average product purity x3, and the tons of product produced x4. The past yearâ€&

> Use the techniques of backward elimination with α = 0.05 to choose a prediction equation for the data of Table 12.8.

> For the data of Exercise 12.15 on page 452, use the techniques of (a) forward selection with a 0.05 level of significance to choose a linear regression model; (b) backward elimination with a 0.05 level of significance to choose a linear regression mode

> Consider the “hang time” punting data given in Case Study 12.2, using only the variables x2 and x3. (a) Verify the regression equation shown on page 489. (b) Predict punter hang time for a punter with LLS = 180 pounds and Power = 260 foot-pounds. (c) C

> A study was done to determine whether the gender of the credit card holder was an important factor in generating profit for a certain credit card company. The variables considered were income, the number of family members, and the gender of the card hold

> A study was done to assess the cost effectiveness of driving a four-door sedan instead of a van or an SUV (sports utility vehicle). The continuous variables are odometer reading and octane of the gasoline used. The response variable is miles per gallon.

> For the data set given in Exericise 12.16 on page 453, can the response be explained adequately by any two regressor variables? Discuss. Exericise 12.16: An engineer at a semiconductor company wants to model the relationship between the gain or hFE of a

> Consider the data of Exercise 12.13 on page 452. Can the response, wear, be explained adequately by a single variable (either viscosity or load) in an SLR rather than with the full two-variable regression? Justify your answer thoroughly through tests of

> Suppose that the time to failure T of a certain hinge is an exponential random variable with probability density f(t) = θe−θt, t>0. From prior experience we are led to believe that θ is a value

> In Example 12.8, a case is made for eliminating x1, powder temperature, from the model since the P-value based on the F-test is 0.2156 while P-values for x2 and x3 are near zero. (a) Reduce the model by eliminating x1, thereby producing a full and a rest

> Consider Example 12.3 on page 447. Compare the two competing models. First order: yi = β0 + β1x1i + β2x2i + €i, Second order: yi = β0 + β1x1i + β2x2i+ β11x21i + β22x22i + β12x1ix2i + i. Use R2adj in your comparison. Test H0 : β11 = β22 =β12 = 0. In addit

> Consider Example 12.4. Figure 12.1 on page 459 displays a SAS printout of an analysis of the model containing variables x1, x2, and x3. Focus on the confidence interval of the mean response μY at the (x1, x2, x3) locations representing the 13 data points

> An experiment was conducted to determine if the weight of an animal can be predicted after a given period of time on the basis of the initial weight of the animal and the amount of feed that was eaten. The following data, measured in kilograms, were reco

> Consider the data of Exercise 11.55 on page 437. Fit a regression model using weight and drive ratio as explanatory variables. Compare this model with the SLR (simple linear regression) model using weight alone. Use R2, R2adj, and any t-statistics (or F-

> Consider the data for Exercise 12.36. Compute the following: R(β1 | β0), R(β1 | β0, β2, β3), R(β2 | β0, β1), R(β2 | β0, &I

> Consider the electric power data of Exercise 12.5 on page 450. Test H0: β1 = β2 = 0, making use of R(β1, β2 | β3, β4). Give a P-value, and draw conclusions. Exercise 12.5: The elec

> A small experiment was conducted to fit a multiple regression equation relating the yield y to temperature x1, reaction time x2, and concentration of one of the reactants x3. Two levels of each variable were chosen, and measurements corresponding to the

> Repeat Exercise 12.17 on page 461 using an F-statistic. Exercise 12.17: For the data of Exercise 12.2 on page 450, estimate σ2. Exercise 12.2: In Applied Spectroscopy, the infrared reflectance spectra properties of a viscous liquid used in

> For the model of Exercise 12.5 on page 450, test the hypothesis H0: β1 = β2 = 0, H1: β1 and β2 are not both zero. Exercise 12.5: The electric power consumed each month by a chemical plant is thought to be

> Suppose that in Example 18.7 the electrical firm does not have enough prior information regarding the population mean length of life to be able to assume a normal distribution for μ. The firm believes, however, that μ is surel

> Estimate the proportion of defectives being produced by the machine in Example 18.1 if the random sample of size 2 yields 2 defectives.

> This is an extract from Ducker, H., Head, A., McDonnell, B., O’Brien, R. and Richardson, S. (1998), A Creative Approach to Management Accounting: Case Studies in Management Accounting and Control, Sheffield Hallam University Press, ISBN

> This case study is taken from Ducker, J., Head, A., McDonnell, B., O'Brien, R. and Richardson, S. (1998), A Creative Approach to Management Accounting: Case Studies in Management Accounting and Control, Sheffield Hallam University Press, ISBN 086339 791

> Southern Paper Inc. is a global packaging company headquartered in the United States. The company was founded in the 1880s and has three principal business sectors – forest products, packaging and papers. The forest products division supplies lumber to t

> This case study is taken from Ducker, J., Head, A., McDonnell, B., O'Brien, R. and Richardson, S. (1998), A Creative Approach to Management Accounting: Case Studies in Management Accounting and Control, Sheffield Hallam University Press, ISBN 086339 791

> This case was originally set in the 1960s in rural Vermont. The Majestic Lodge is an old but well-maintained property that has changed ownership several times over the years. It has no restaurant or bar. It is positioned as a mid-price, good quality "des

> The Managing Director of the Kiddy Toy Company (KTC) needs to decide whether a special export order should be accepted or rejected, with reasons provided, for the manufacture of Panda bears. The background Official statistics indicate that China manufact

> Professor Anthony Atkinson, (University of Waterloo) and adapted by Professor John Shank (The Amos Tuck School of Business Administration Dartmouth College) This case is reprinted from Cases in Cost Management, Shank, J. K., 1996, South Western Publishin

> Anjo Ltd was established in 1986 by two brothers, Andrew and Jonathan Bright. They saw a market for providing accessories in the home to accommodate the new era of home entertainment, such as television cabinets, record stands, hi-fi cabinets, tape casse

> Permission to reprint this case has been granted by Captus Press Inc. and the Accounting Education Resource Centre of the University of Lethbridge. Foster’s Construction Ltd: Organizational Background Fosters Construction Ltd (FCL) is a privately owned c

> Hardhat Ltd’s Budget Committee, which has members drawn from all the major functions in the business, is meeting to consider the projected income statement for 2018/2019, which is composed of the ten months’ actuals to

> The Application of Linear Programming to Management Accounting Midland Airport Ltd LEARNING OBJECTIVES: After reading this case study and completing the questions you will be able to: • Formulate the initial linear programming model (ob

> Fleet operates a chain of high street retail outlets selling clothing and household items. In 1995 this company was heading for a financial loss and was deemed to have lost strategic direction. The business formula that had proved successful in the 1980s

> This case study is taken from Ducker, J., Head, A., McDonnell, B., O'Brien, R. and Richardson, S. (1998), A Creative Approach to Management Accounting: Case Studies in Management Accounting and Control, Sheffield Hallam University Press, ISBN 086339 791

> In November 2012, a consultant was employed to review and document the planning and control systems of Integrated Technology Services (UK) Ltd (ITS-UK), to ensure that these were effectively meeting the needs of the business and to provide a basis for st

> This case was originally set in a specialty manufacturer of industrial measuring instruments in Scotland in 1979. The topic is profit variance analysis. THE FIRM Kinkead has been a leading UK firm since World War II in specialty instruments for measuring

> Company A is in the chemical industry and a manufacturer of industrial paints. At one of its manufacturing sites (site 1) a new system of costing and management information is being considered to replace a traditional system, which was not meeting fully

> The Board of Dumbellow Ltd are meeting on the 23rd January to discuss the draft budget for 2018/19, some two months before the start of that year. The company produces three industrial valves which are incorporated into equipment used in the Oil and Gas

> Learning objectives: After reading this case study and completing the questions you will be able to: • Demonstrate familiarity with two methods of process costing: weighted average and FIFO. • Discuss the treatment of normal loss, abnormal loss and abnor

> The case was prepared as the basis for discussion rather than to illustrate either effective or ineffective handling of an administrative situation. Danfoss Drives A/S is a Danish producer of frequency converters located in Graasten in the southern part

> Company B is a manufacturer of large, complex electrical motors. It has been making them 'to order', in order quantities of, typically, one-four in a jobbing/batch production system for many years. A typical selling price may range from £3000-£20 000 per

> Learning objectives: After reading this case study and completing the questions you will be able to: • Explain the alternative methods of allocating joint costs to products. • Discuss the arguments for and against each

> Mestral is a highly successful company manufacturing a range of quality bathroom fittings. For the past 15 years production has been carried out at three locations: Northern town in the North East of England; at Western town on the Severn estuary; and at

> Kaminsky Ltd manufactures belts and braces. The firm is organized into five departments. These are belt-making, braces-making and three service departments (maintenance, warehousing and administration). Direct costs are accumulated for each department. F

> (a). Flopro plc makes and sells two products A and B, each of which passes through the same automated production operations. The following estimated information is available for period 1: (ii). Production/sales of products A and B are 120 000 units and

> Galuppi plc is considering whether to scrap some highly specialized old plant or to refurbish it for the production of drive mechanisms, sales of which will last for only three years. Scrapping the plant will yield £25 000 immediately, where

> Franzl is a contract engineer working for a division of a large construction company. He is responsible for the negotiation of contract prices and the subsequent collection of instalment monies from customers. It is company policy to achieve a mark-up of

> Paragon Products plc has a factory that manufactures a wide range of plastic household utensils. One of these is a plastic brush that is made from a special raw material used only for this purpose. The brush is moulded on a purpose-built machine that was

> Losrock Housing Association is considering the implementation of a refurbishment programme on one of its housing estates which would reduce maintenance and heating costs and enable a rent increase to be made. Relevant data are as follows: (i). Number of

> Using the discounted cash flow yield (internal rate of return) for evaluating investment opportunities has the basic weakness that it does not give attention to the amount of the capital investment, in that a return of 20 per cent on an investment of &Ac

> The Portsmere Hospital operates its own laundry. Last year the laundry processed 120 000 kilograms of washing and this year the total is forecast to grow to 132 000 kilograms. This growth in laundry processed is forecast to continue at the same percentag

> You are employed as the assistant accountant in your company and you are currently working on an appraisal of a project to purchase a new machine. The machine will cost £55 000 and will have a useful life of three years. You have already est

> Your company is considering investing in its own transport fleet. The present position is that carriage is contracted to an outside organization. The life of the transport fleet would be five years, after which time the vehicles would have to be disposed

> Garrett Automative Ltd (GAL) is a UK subsidiary of a American parent company that manufactures turbochargers for the automative industry. GAL decided to begin its profit improvement programme by examining its factory throughput. Throughput was defined as

> The following information relates to three possible capital expenditure projects. Because of capital rationing only one project can be accepted: The company estimates its cost of capital is 18 per cent. Calculate: (a). The payback period for each proje

> Short flower Ltd currently publish, print and distribute a range of catalogues and instruction manuals. The management has now decided to discontinue printing and distribution and concentrate solely on publishing. Long plant Ltd will print and distribute

> Cassidy Computers plc sells one of its products, a plug-in card for personal computer systems, in both the UK and Ruritania. The relationship between price and demand is different in the two markets, and can be represented as follows: Home market: Price

> Butterfield Ltd manufactures a single brand of dog food called ‘Lots O Grissle’ (LOG). Sales have stabilized for several years at a level of £20 million per annum at current prices. This level is not expected to change in the foreseeable future (except a

> Safety or buffer stocks are held for many reasons. For example, road authorities might want to hold sufficient stock of grit salt in case of bad weather, or firms might build stock of key materials if a price rise is impending. In recent times climate c

> The Boeing 737 jet is the world’s most popular and reliable commercial airliner. The company has manufactured over 8000 jets in the 737 family. In 2005, the 737-900ER was launched, which can carry more passengers over a further range than any previous mo

> Modern day aircraft are complex pieces of engineering, increasingly using more technology, composite materials and more efficient engines. Aircraft engines are in particular improving not only in fuel efficiency, but also in range, thus contributing to l

> South African energy and chemicals company Sasol, like many companies dealing with large-scale projects, needs to prepare cost estimates. Sasol specialize in high value liquid fuels, chemicals and low-carbon electricity. In 2014, the company decided to i

> In the March 2012 edition of CIMA’s Financial Management journal, Christian Doherty asks what will management accountants ten years on be grappling with? This question has been posed before (see, for example, Scapings et al., 2003) and technology is a fa

> According to a US Congressional enquiry, this accident apparently partly resulted from local decisions within the oil multinational BP and its contractors to save relatively immaterial costs by cutting corners in oil exploration safety measures (National

> As one of the pioneers in the low-cost airline market, easyJet’s business model includes some core values: ● Safety – Our number one value, sitting at the core of everything we do. ● Pioneering – We challenge to find new ways to make travel easy and affo

> Insteel Industries decided to implement ABM at the Andrews, South Carolina, plant. The ABM team analysed operations and identified 12 business processes involving a total of 146 activities. The ABM study revealed that the 20 most expensive activities acc

> Taylor, Woods and Cheng Ge Fang (2014) reported on how one UK company moved its target costing system away from profit targets and focused it on product-level economic value added (EVA(TM)) targets. The company, which used the pseudonym Electronics for c

> Management accounting combines accounting, finance and management with the leading-edge techniques needed to drive successful businesses. Chartered management accountants: ● Advise managers about the financial implications of projects. ● Explain the fina

> Following events of September 2001, airport security screening in the US and globally increased dramatically. As we all know, this led to increasing queues at airports which while inconvenient, are paramount to the safety and security of passengers. Sin

> As a result of the recent financial troubles at Tesco its shares declined to an 11-year low in 2014. Terry Smith, chief executive of investment house Fundsmith, stated in an article published in The Financial Times that investors had long ignored warning

> An article by Chen et al. (2015) published in Strategic Finance described how Zhongyuan Special Steel Co. (ZYSCO), a typical Chinese state-owned company, introduced a new strategic management system that would integrate its value creation strategy into e

> Southwest Airlines set ‘operating efficiency’ as its strategic theme. The four perspectives embodied in the balanced scorecard were linked together by a series of relatively simple questions and answers: Financial: Wha

> The Globe and Mail (Canada) quotes an article written by Professor Pietro Micheli in Industry Week in which he listed seven myths about performance management that promote the wrong behaviours. The following is a summary of these myths: Myth 1: Numbers

> Across Europe, just how much – or little – US multinational firms are paying in taxes is coming under intense scrutiny according to an article published in the Washington Post. Most of the investigations revolve around the issue of ‘transfer pricing’, wh

> According to an article in the Financial Times the UK tax authority (HMRC – HM Revenue & Customs) raised £1.1bn from challenging the pricing of multinational companies’ internal deals in 2013–14 – more than twice as much as in the previous year. The incr

> Medical devices are normally associated with use by hospitals and medical practices. Some devices are used by normal consumers and, according to an article on the Medical Device and Diagnostic Industry website (www.mddionline.com), are proliferating. The

> Teva Pharmaceutical Industries Ltd reorganized its pharmaceutical operations into decentralized cost and profit centres. Teva proposed a transfer pricing system based on marginal costs. But the proposed transfer pricing system generated a storm of contro

> The financial mission of a company should be to invest and create cash flows in excess of the cost of capital. If an investment is announced that is expected to earn in excess of the cost of capital, then the value of the firm will immediately rise by th

> From Real World View 19.1, you know that Siemens operates in many countries and has quite a diverse product offering. With such complex and broad operations, there are many factors that can affect the performance of a business sector or division. In its

> German global company Siemens AG had a turnover of almost €76 billion in 2015, recording a profit after taxes of €7.4 billion, according to its annual report. The company operates globally, with 351 000 employees globally. Siemens is a diverse organizati

> A distinguishing feature of today’s digital technology is that it is characterized by zero (or near-zero) marginal costs. Once you’ve made the investment needed to create a digital good, it costs next to nothing to roll out and distribute millions of cop

> In a BBC documentary called Power to the People, Michael Portillo visited a ‘You Decide’ session organized by the local council in Tower Hamlets, London. At this session, local people decide what is to be done with £250 000 of council money. They are giv

> Meditech South Africa (Pty) Ltd provides software solutions to meet the information needs of healthcare organizations in Africa and the Middle East. According to their website, the software can encompass all areas of healthcare from doctor’s offices to h

> Setting standards in an organization may be primarily to assist in the calculation of a standard cost for the product or service for management accounting purposes. Standards are also relevant for operational and customer service managers as they may aff

> Recipes are used in the manufacturing processes of many sectors. In the paper industry, a starch recipe consisting of borax, caustic soda, starch (from maize or potatoes) and hot water is used to glue corrugated board (cardboard) together. This process i