Question: Intel Corporation’s consolidated income statement

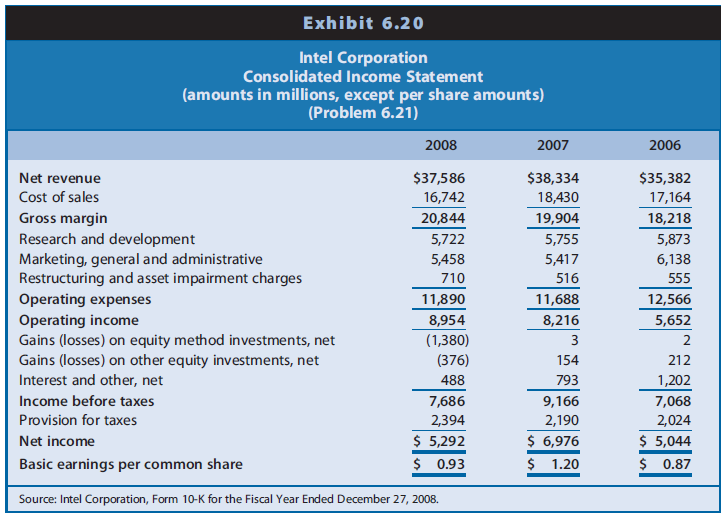

Intel Corporation’s consolidated income statement appears in Exhibit 6.20.

Note 15, which follows, explains the source of the restructuring charges, the breakdown of the charges into employee-related costs and asset impairments, and the balance of the accrued restructuring liability account.

Note 15: Restructuring and asset Impairment Charges

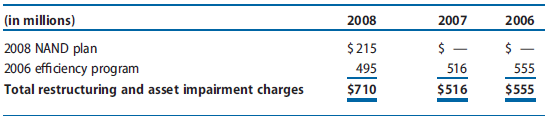

The following table summarizes restructuring and asset impairment charges by plan for the three years ended December 27, 2008:

We may incur additional restructuring charges in the future for employee severance and benefit arrangements, and facility-related or other exit activities. Subsequent to the end of 2008, management approved plans to restructure some of our manufacturing and assembly and test operations, and align our manufacturing and assembly and test capacity to current market conditions. These actions, which are expected to take place beginning in 2009, include closing two assembly and test facilities in Malaysia, one facility in the Philippines, and one facility in China; stopping production at a 200mm wafer fabrication facility in Oregon; and ending production at our 200mm wafer fabrication facility in California.

2008 NAND PLAN

In the fourth quarter of 2008, management approved a plan with Micron to discontinue the supply of NAND flash memory from the 200mm facility within the IMFT manufacturing network.

The agreement resulted in a $215 million restructuring charge, primarily related to the IMFT 200mm supply agreement. The restructuring charge resulted in a reduction of our investment in IMFT of $184 million, a cash payment to Micron of $24 million, and other cash payments of $7 million.

2006 EFFICIENCY PROGRAM

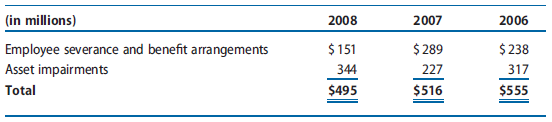

The following table summarizes charges for the 2006 efficiency program for the three years ended December 27, 2008:

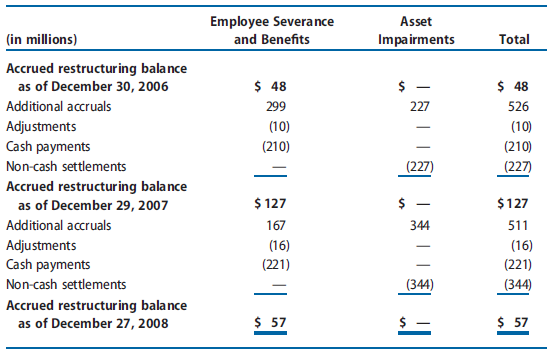

The following table summarizes the restructuring and asset impairment activity for the 2006 efficiency program during 2007 and 2008:

We recorded the additional accruals, net of adjustments, as restructuring and asset impairment charges. The remaining accrual as of December 27, 2008 was related to severance benefits that we recorded within accrued compensation and benefits.

From the third quarter of 2006 through the fourth quarter of 2008, we incurred a total of $1.6 billion in restructuring and asset impairment charges related to this program. These charges included a total of $678 million related to employee severance and benefit arrangements for approximately 11,900 employees, and $888 million in asset impairment charges.

REQUIRED

a. Based on your reading of the note, how would you treat Intel’s restructuring charges in the assessment of current profitability and the prediction of future earnings?

b. Why is the balance of the ‘‘accrued restructuring’’ limited to employee-related costs?

c. Describe the effect on net income of each entry in the ‘‘accrued restructuring balance’’ account reconciliation. (For example, what is the effect of ‘‘Additional accruals’’ on net income?)

d. How do U.S. GAAP and IFRS differ on the rules used to compute the restructuring charge?

Transcribed Image Text:

Exhibit 6.20 Intel Corporation Consolidated Income Statement (amounts in millions, except per share amounts) (Problem 6.21) 2008 2007 2006 Net revenue $37,586 $38,334 $35,382 Cost of sales 16,742 18,430 17,164 Gross margin Research and development Marketing, general and administrative Restructuring and asset impairment charges 20,844 19,904 18,218 5,722 5,755 5,873 5,458 5,417 6,138 555 710 516 Operating expenses 11,890 11,688 12,566 Operating income Gains (losses) on equity method investments, net Gains (losses) on other equity investments, net Interest and other, net 8,216 5,652 8,954 (1,380) 3 2 (376) 154 212 488 793 1,202 Income before taxes 7,686 9,166 7,068 Provision for taxes 2,394 2,190 2,024 Net income $ 5,292 $ 6,976 $ 5,044 Basic earnings per common share $ 0.93 $ 1.20 $ 0.87 Source: Intel Corporation, Form 10-K for the Fiscal Year Ended December 27, 2008. (in millions) 2008 2007 2006 2008 NAND plan $215 $ $ 2006 efficiency program 495 516 555 Total restructuring and asset impairment charges $710 $516 $555 (in millions) 2008 2007 2006 Employee severance and benefit arrangements $ 151 $ 289 $ 238 asset impairments 344 227 317 Total $495 $516 $555 Employee Severance asset (in millions) and Benefits Impairments Total Accrued restructuring balance as of December 30, 2006 $ 48 $ - $ 48 Additional accruals 299 227 526 Adjustments Cash payments (10) (10) (210) (210) Non-cash settlements (227) (227) Accrued restructuring balance as of December 29, 2007 $ 127 $ $127 - Additional accruals 167 344 511 (16) Adjustments Cash payments (16) (221) (221) Non-cash settlements (344) (344) Accrued restructuring balance as of December 27, 2008 $ 57 $ 57

> Vulcan Materials Company, a member of the S&P 500 Index, is the nation’s largest producer of construction aggregates, a major producer of asphalt mix and concrete, and a leading producer of cement in Florida. Exhibit 6.19 presents V

> The chapter describes free cash flows for common equity shareholders. Suppose a firm has no debt and uses marketable securities to manage operating liquidity. If the firm uses cash to purchase marketable securities, how does that transaction affect free

> Gap Inc. operates chains of retail clothing stores under the names of Gap, Banana Republic, and Old Navy. Exhibit 3.21 presents the statement of cash flows for Gap for Year 0 to Year 4. REQUIRED Discuss the relations between net income and cash flow fro

> Tesla Motors manufactures high performance electric vehicles that are extremely slick looking. Exhibit 3.20 presents the statement of cash flows for Tesla Motors for 2010–2012. REQUIRED Discuss the relations among net income, cash flow

> Texas Instruments primarily develops and manufactures semiconductors for use in technology-based products for various industries. The manufacturing process is capital-intensive and subject to cyclical swings in the economy. Because of overcapacity in the

> Refer to the websites and the Form 10-K reports of Home Depot (www.homedepot.com) and Lowe’s (www.lowes.com). Compare and contrast their business strategies.

> Assume that the firm’s cost of equity capital is 10% and that the firm’s existing assets and operations generate a 10% return on common equity. If the firm raises additional equity capital and invests in assets that will generate a return less than 10%,

> Microsoft Corporation (Microsoft) and Oracle Corporation (Oracle) engage in the design, manufacture, and sale of computer software. Microsoft sells and licenses a wide range of systems and application software to businesses, computer hardware manufacture

> The Coca-Cola Company (Coca-Cola), like PepsiCo, manufactures and markets a variety of beverages. Exhibit 3.18 presents a statement of cash flows for Coca-Cola for three years. REQUIRED Discuss the relations between net income and cash flow from operat

> BTB Electronics Inc. manufactures parts, components, and processing equipment for electronics and semiconductor applications in the communications, computer, automotive, and appliance industries. Its sales tend to vary with changes in the business cycle

> United Van Lines purchased a truck with a list price of $250,000 subject to a 6% discount if paid within 30 days. United Van Lines paid within the discount period. It paid $4,000 to obtain title to the truck with the state and an $800 license fee for the

> Flight Training Corporation is a privately held firm that provides fighter pilot training under contracts with the U.S. Air Force and the U.S. Navy. The firm owns approximately 100 Lear jets that it equips with radar jammers and other sophisticated elect

> Nojiri Pharmaceutical Industries develops, manufactures, and markets pharmaceutical products in Japan. The Japanese economy experienced recessionary conditions in recent years. In response to these conditions, the Japanese government increased the propor

> Eli Lilly and Company produces pharmaceutical products for humans and animals. Exhibit 7.18 includes a footnote excerpt from the annual report of Lilly for the period ending December 31, 2004. REQUIRED Review Exhibit 7.18 and answer the following questi

> Exhibit 3.27 presents common-size statements of cash flows for eight firms in various industries. All amounts in the common-size statements of cash flows are expressed as a percentage of cash flow from operations. In constructing the common-size percenta

> Aer Lingus is an international airline based in Ireland. Exhibit 3.26 provides the statement of cash flows for Year 1 and Year 2, which includes a footnote from the financial statements. Year 2 was characterized by weakening consumer demand for air trave

> Exhibit 6.22 presents selected financial statement data for Enron Corporation as originally reported for 1997, 1998, 1999, and 2000. In 2001, Enron restated its financial statements for earlier years because it reported several items beyond the limits of

> If a firm’s residual income for a particular year is positive, does that mean the firm was profitable? Explain. If a firm’s residual income for a particular year is negative, does that mean the firm necessarily reported a loss on the income statement? Ex

> The text states, ‘‘Over sufficiently long time periods, net income equals cash inflows minus cash outflows, other than cash flows with owners.’’ Demonstrate the accuracy of this statement in the following scenario: Two friends contributed $50,000 each to

> Firms value inventory under a variety of assumptions, including two common methods: last-in first out (LIFO) and first-in first-out (FIFO). Ignore taxes, assume that prices increase over time, and assume that a firm’s inventory balance is stable or grows

> ‘‘Asset valuation and recognition of net income closely relate.’’ Explain, including conditions when they do not.

> Exhibit 4.22 presents selected operating data for three retailers for a recent year. Macy’s operates several department store chains selling consumer products such as brand-name clothing, china, cosmetics, and bedding and has a large pr

> The chapter describes free cash flows for common equity shareholders. If the firm borrows cash by issuing debt, how does that transaction affect free cash flows for common equity shareholders in that period? If the firm uses cash to repay debt, how does

> ‘‘Some asset valuations using historical costs are highly relevant and very representationally faithful, whereas others may be representationally faithful but lack relevance. Some asset valuations based on fair values are highly relevant and very represe

> A recent article in Fortune magazine listed the following firms among the top ten most admired companies in the United States: Dell, Southwest Airlines, Microsoft, and Johnson & Johnson. Access the websites of these four companies or read the Business se

> A firm’s income tax return shows income taxes for 2009 of $35,000. The firm reports deferred tax assets before any valuation allowance of $24,600 at the beginning of 2009 and $27,200 at the end of 2009. It reports deferred tax liabilities of $18,900 at t

> Describe how the statement of cash flows is linked to each of the other financial statements (income statement and balance sheet). Also review how the other financial statements are linked with each other.

> Explain residual ROCE (return on common shareholders’ equity). What does residual ROCE represent? What does residual ROCE measure?

> Suppose the following hypothetical data represent total assets, book value, and market value of common shareholders’ equity (dollar amounts in millions) for Microsoft, Intel, and Dell, three firms involved in different aspects of the co

> What are the fundamental determinants of share value, and how do they affect market-based valuation multiples, such as market-to-book and price earnings ratios?

> A firm’s income tax return shows $50,000 of income taxes owed for 2009. For financial reporting, the firm reports deferred tax assets of $42,900 at the beginning of 2009 and $38,700 at the end of 2009. It reports deferred tax liabilities of $28,600 at th

> Explain the implications of a value to- book ratio that is exactly equal to 1. Compare the implications of a value-to-book ratio that is greater than 1 to those of a value-to-book ratio that is less than 1.

> Sunbeam Corporation manufactures and sells a variety of small household appliances, including toasters, food processors, and waffle grills. Exhibit 6.21 presents a statement of cash flows for Sunbeam for Year 5, Year 6, and Year 7. After experiencing dec

> Effective financial statement analysis requires an understanding of a firm’s economic characteristics. The relations between various financial statement items provide evidence of many of these economic characteristics. Exhibit 1.22 pres

> Dick’s Sporting Goods is a chain of full-line sporting goods retail stores offering a broad assortment of brand name sporting goods equipment, apparel, and footwear. Dick’s Sporting Goods had its initial public offerin

> In conceptual terms, explain the value-to-book valuation approach. Explain how the value-to-book approach described and demonstrated in this chapter relates to the residual income valuation approach described and demonstrated in Chapter 13.

> Analyzing the profitability of restaurants requires consideration of their strategies with respect to ownership of restaurants versus franchising. Firms that own and operate their restaurants report the assets and financing of those restaurants on their

> If the firm borrows capital from a bank and invests it in assets that earn a return greater than the interest rate charged by the bank, what effect will that have on residual income for the firm? How does that effect compare with the effects of capital s

> Why is it appropriate to use the required rate of return on equity capital (rather than the weighted-average cost of capital) as the discount rate when using the residual income valuation approach?

> The Coca-Cola Company is a global soft drink beverage company (ticker symbol ¼ KO) that is a primary and direct competitor with PepsiCo. The data in Exhibits 12.14–12.16 include the actual amounts for 2010, 2011, and 2012

> Identify conditions that would lead an analyst to expect that management might attempt to manage earnings downward.

> Explain the two roles of book value of common shareholders’ equity in the residual income valuation approach.

> Explain the theory behind the residual income valuation approach. Why is residual income value-relevant to common equity shareholders?

> Explain residual income. What does residual income represent? What does residual income measure?

> Explain required income. What does required income represent? How is required income conceptually analogous to interest expense?

> Conceptually, why should an analyst expect a valuation based on dividends, a valuation based on the free cash flows for common equity shareholders, and a valuation based on residual income to yield equivalent value estimates for a given firm?

> The 3M Company is a global diversified technology company active in the following product markets: consumer and office; display and graphics; electronics and communications; health care; industrial; safety, security, and protection services; and transpor

> Suppose you are applying the residual income valuation model to value a firm with extremely aggressive accounting. Suppose, for example, the firm has a substantially overvalued asset on the balance sheet. (Perhaps the firm has a large amount of goodwill

> The text discusses inputs managers might use to determine fair values of assets and liabilities and identifies different classifications of assets identified in SFAS No. 157. Suppose a major university endowment has investments in a wide array of assets,

> Suppose the following hypothetical data represent total assets, book value, and market value of common shareholders’ equity (dollar amounts in millions) for Abbott Labs, IBM, and Target Stores. Abbott Labs manufactures and sells health

> Suppose the following hypothetical data represent total assets, book value, and market value of common shareholders’ equity (dollar amounts in millions) for three firms. Each of these firms, Southwest Airlines, Kroger, and Yum! Brands,

> Conceptually, why should you expect valuation based on dividends and valuation based on the free cash flows for common equity shareholders to yield identical value estimates?

> Explain the theory behind the free cash flows valuation approaches. Why are free cash flows value-relevant to common equity shareholders when they are not cash flows to those shareholders but rather are cash flows into the firm?

> Explain ‘‘free’’ cash flows. Describe which types of cash flows are free and which are not. How do free cash flows available for debt and equity stakeholders differ from free cash flows available for common equity shareholders?

> Describe circumstances and give an example of when free cash flows to equity shareholders and free cash flows to all debt and equity stakeholders will be identical. Under those circumstances, will the required rate of return on equity and the weighted-av

> Describe valuation settings in which the appropriate discount rate to use is the required rate of return on equity capital versus settings in which it is appropriate to use a weighted-average cost of capital.

> The chapter describes valuation using free cash flows for all debt and equity stakeholders as well as free cash flows for equity shareholders. For each approach, give one example of valuation settings in which that approach is appropriate.

> Assume that a corporation needs to enter the private debt market to raise funds for plant expansion. The corporation expects debt covenants to place restrictions on the levels of its current ratio and total-liabilities to assets ratio. Considering the ac

> Kelly Services (Kelly) places employees at clients’ businesses on a temporary basis. It segments its services into (1) Commercial, (2) Professional and technical, and (3) International. Kelly recognizes revenues for the amount bille

> Suppose you are valuing a healthy, growing, profitable firm and you project that the firm will generate negative free cash flows for equity shareholders in each of the next five years. Can you use a free-cash-flows-based valuation approach when cash flow

> Prior to Year 8, Cooper Corporation engaged in a wide variety of industries, including weapons manufacturing under government contracts, information technologies, commercial aircraft manufacturing, missile systems, coal mining, material service, ship man

> Most economists describe three determinants of the interest rates on a borrower’s debt: a real interest rate, which is a charge for using capital; an adjustment for expected inflation to insure that debt is repaid in dollars having the same purchasing po

> A firm had the following values for the four debt ratios discussed in the chapter: Liabilities to Assets Ratio: less than 1.0 Liabilities to Shareholders’ Equity Ratio: equal to 1.0 Long-Term Debt to Long-Term Capital Ratio: less than 1.0 Long-Term Debt

> The use of the term reserve in the title of a financial statement account is not acceptable in the United States, primarily because its purpose is often too vague. However, informal use of the term by chief financial officers, analysts, and the media is

> All leases for financial reporting purposes are treated as either capital (finance) leases or operating leases. The effects of the two reporting techniques on the financial statements differ substantially. From the perspective of the lessee, prepare a ch

> Alfa Romeo incurs direct cash costs of $30,000 in manufacturing a red convertible automobile during 2009. Assume that it incurs all of these costs in cash. Alfa Romeo sells this automobile to you on January 1, 2010, for $45,000. You pay $5,000 immediatel

> Assume that Motorola, Inc., issues bonds with a face value of $10,000,000 for $9,200,000. The bonds have detachable warrants that may be traded in for shares of common stock. Assume that immediately after issue, bonds with warrants detached trade for $9,

> ARTL Company issued 3%, 10-year convertible bonds on January 1, 2013, at their par value of $500 million. Each $1,000 bond is convertible into 40 shares of ARTL’s $1 par value common stock. Use the template below to show the financial s

> Assume that John Deere Co. issues 2,000 shares of $100 par, 6% convertible preferred stock for $105 per share. Shareholders have the right to exchange each share of convertible preferred stock for five shares of $10 par common stock. Use the template bel

> Determine and compare the financial reporting (debt versus equity classification) of redeemable preferred stock with the following characteristics under U.S. GAAP and IFRS. a. Redemption will occur at a specific time or upon a specific event (for example

> Assume that Great Beef Co. owes Bank of America $5,000, 000 on a 3-year, 9% note originally issued at par. After one year of making scheduled payments, the firm faces financial difficulty. At the end of the second year, Great Beef owes Bank of America $5

> Assume that Circuit City owes Synovus Bank $1,000, 000 on a 4-year, 7% note originally issued at par. After one year of making scheduled payments, Circuit City faces financial difficulty. At the end of the second year, Circuit City owes Synovus $1,000,00

> Define earnings management. Discuss why it is difficult to discern whether a firm does in fact practice earnings management.

> Under U.S. GAAP, the statement of cash flows classifies cash expenditures for interest expense as an operating activity but classifies cash expenditures to redeem debt as a financing activity. Explain this apparent paradox.

> Exhibit 7.17 includes a footnote excerpt from the annual report of The Coca-Cola Company for 2004. The beverage company offers stock options to key employees under plans approved by stockholders. REQUIRED Review Exhibit 7.17 and answer the following que

> While a firm’s sales and net income have been steady during the last three years, the firm has experienced a decrease in its accounts receivable and inventory turnovers and an increase in its accounts payable turnover. What is the likely direction of cha

> Some retailing companies own their own stores or acquire their premises under capital leases. Other retailing companies acquire the use of store facilities under operating leases, contracting to make future payments. An analyst comparing the capital stru

> Exhibit 1.25 presents common-size income statements and balance sheets for seven firms that operate at various stages in the value chain for the pharmaceutical industry. These common- size statements express all amounts as a percentage of sales revenue.

> The concept of accounting quality has several dimensions, but two characteristics often dominate: the accounting information should be a fair representation of performance for the reporting period, and it should provide relevant information to forecast e

> Firms such as Deere & Company and Macy’s, Inc., often sell their receivables as a means of obtaining financing. Should firms selling receivables remove the receivables from the balance sheet, or should the receivables remain on the balance sheet? Should

> Diviney Company wants to raise $50 million cash but for various reasons does not want to do so in a way that results in a newly recorded liability. The firm is sufficiently solvent and profitable, so its bank is willing to lend up to $50 million at the p

> On June 24, Year 4, a major airline entered into a revolving accounts receivable facility (Facility) providing for the sale of $489 million of a defined pool of accounts receivable (Receivables) through a wholly owned subsidiary to a trust in exchange fo

> Loss contingencies may or may not give rise to accounting liabilities. Financial reporting requires firms to recognize a loss contingency when two criteria are met. Describe the two criteria and provide an example in which applying the criteria would tri

> Nestle´ Group, a multinational food products firm based in Switzerland, recently issued its financial statements. The auditor’s opinion attached to the financial statements stated the following: ‘‘In our opinion, the financial statements for the year end

> Financial accounting rules require firms to assess whether they will recover carrying amounts of long-lived assets and, if not, to write down the assets to their fair value and recognize an impairment loss in income from continuing operations. Impairment

> A firm has experienced an increasing current ratio but a decreasing operating cash flow to current liabilities ratio during the last three years. What is the likely explanation for these results?

> Firms often enter into transactions that are peripheral to their core operations but generate gains and losses that must be reported on the income statement. Provide an example in which a gain generated from the sale of an equity security may be labeled

> Delta Air Lines, Inc., is one of the largest airlines in the United States. It has operated on the verge of bankruptcy for several years. Exhibit 5.18 presents selected financial data for Delta Air Lines for each of the five years ending December 31, 200

> Refer to the profitability ratios of Coca-Cola in Problem 4.26. Exhibit 5.17 presents risk ratios for Coca-Cola for 2006–2008. As we did within the chapter for PepsiCo, we utilize Coca-Cola’s footnote disclosures to ex

> Checkpoint Systems is a leading provider of source tagging, handheld labeling systems, retail merchandising systems, and bar-code labeling systems. In a press release, Checkpoint stated the following: GAAP reported net loss for the fourth quarter of 2004

> Refer to the financial statement data for Abercrombie & Fitch in Problem 4.25. Exhibit 5.16 presents risk ratios for Abercrombie & Fitch for fiscal Year 3 and Year 4. Financial statement data for Abercrombie & Fitch from Problem 4.25 REQUIR

> Refer to the financial statement data for Hasbro in Problem 4.24 in Chapter 4. Exhibit 5.15 presents risk ratios for Hasbro for Year 2 and Year 3. Financial statement data for Hasbro from Problem 4.24 REQUIRED a. Calculate the amounts of these ratios f

> Ford Motor Credit Company discloses the following information with respect to finance receivables (amounts in millions). Notes to Financial Statements The Company periodically sells finance receivables in securitization transactions to fund operations a

> ‘‘The accrual basis of accounting creates the need for a statement of cash flows.’’ Explain.

> Exhibit 5.25 presents balance sheets for 2007 and 2008 for Whole Foods Market, Inc.; Exhibit 5.26 presents income statements for 2006–2008. REQUIRED a. Prepare the standard decomposition of ROCE into margin, turnover, and leverage. Us

> Exhibit 5.24 presents selected financial data for The Tribune Company and The Washington Post Company for fiscal 2006 and 2007. The Washington Post Company is an education and media company. It owns, among others, Kaplan, Inc.; Cable ONE Inc.; Newsweek m

> Exhibit 5.23 presents selected financial data for ABC Auto, and XYZ Comics, for fiscal Year 5 and Year 6. ABC Auto manufactures automobile components that it sells to automobile manufacturers. Competitive conditions in the automobile industry in recent y

> Exhibit 5.22 presents selected financial data for Best Buy Co., Inc., and Circuit City Stores, Inc., for fiscal 2008 and 2007. Best Buy and Circuit City operate as specialty retailers offering a wide range of consumer electronics, service contracts, prod

> Sun Microsystems, Inc., develops, manufactures, and sells computers for network systems. Exhibit 5.21 presents selected financial data for Sun Microsystems for each of the five years ending June 30, 2005, to June 30, 2009. The company did not go bankrupt

> VF Corporation is an apparel company that owns recognizable brands like Timberland, Vans, Reef, and 7 For All Mankind. Exhibit 5.19 and 5.20 present balance sheets and income statements, respectively, for 2011– 2012. (VF Corporation pre