Question: Johnson trades as a chandler at the

Johnson trades as a chandler at the Savoy Marina. His profit in this business during the year to 30 June was £12 000. Johnson also undertakes occasional contracts to build pleasure cruisers, and is considering the price at which to bid for the contract to build the Blue Blood for Mr B.W. Dunn, delivery to be in one year’s time. He has no other contract in hand, or under consideration, for at least the next few months.

Johnson expects that if he undertakes the contract, he would devote one-quarter of his time to it. To facilitate this, he would employ G. Harrison, an unqualified practitioner, to undertake his book-keeping and other paperwork, at a cost of £2000.

He would also have to employ on the contract one supervisor at a cost of £11 000 and two craftsmen at a cost of £8800 each; these costs include Johnson’s normal apportionment of the fixed overheads of his business at the rate of 10 per cent of labour cost.

During spells of bad weather one of the craftsmen could be employed for the equivalent of up to three months full time during the winter in maintenance and painting work in the chandler’s business. He would use materials costing £1000. Johnson already has two inclusive quotations from jobbing builders for this maintenance and painting work, one for £2500 and the other for £3500, the work to start immediately.

The equipment that would be used on the Blue Blood contract was bought nine years ago for £21 000. Depreciation has been written off on a straight-line basis, assuming a ten-year life and a scrap value of £1000. The current replacement cost of similar new equipment is £60 000, and is expected to be £66 000 in one year’s time. Johnson has recently been offered £6000 for the equipment, and considers that in a year’s time he would have little difficulty in obtaining £3000 for it. The plant is useful to Johnson only for contract work.

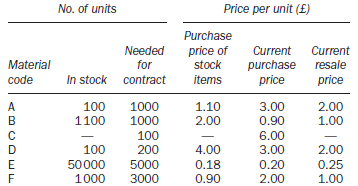

In order to build the Blue Blood Johnson will need six types of material, as follows:

Materials B and E are sold regularly in the chandler’s business. Material A could be sold to a local sculptor, if not used for the contract. Materials A and E can be used for other purposes, such as property maintenance. Johnson has no other use for materials D and F, the stocks of which are obsolete.

The Blue Blood would be built in a yard held on a lease with four years remaining at a fixed annual rental of £5000. It would occupy half of this yard, which is useful to Johnson only for contract work. Johnson anticipates that the direct expenses of the contract, other than those noted above, would be £6500.

Johnson has recently been offered a one-year appointment at a fee of £15 000 to manage a boat building firm on the Isle of Wight. If he accepted the offer he would be unable to take on the contract to build Blue Blood or any other contract. He would have to employ a manager to run the chandler’s business at an annual cost (including fidelity insurance) of £10 000, and would incur additional personal living costs of £2000.

You are required:

(a). to calculate the price at which Johnson should be willing to take on the contract in order to break even, based exclusively on the information given above;

(b). to set out any further considerations which you think that Johnson should take into account in setting the price at which he would tender for the contract.

Transcribed Image Text:

No. of units Price per unit (£) Purchase Needed price of stock Current Current Material for purchase price resale code In stock contract items price 100 1000 1.10 3.00 2.00 1100 1000 2.00 0.90 1.00 6.00 3.00 100 100 200 4.00 2.00 50000 0.20 2.00 5000 0.18 0.90 0.25 1000 3000 1.00 ABC EF

> According to Gillian Lees, a blogger on www.cimaglobal .com, the typical risk assessment model for a management accountant reads like this: identify risks, assess their impact and probability, and develop risk responses. This seems a reasonable approach,

> The CGMA website offers management accountants a collection of tools and resources which are useful to identify, assess and respond to (or manage) various types of risk faced by an organization. For example, it identifies risks in four categories – exten

> The remuneration system that is applied in healthcare organizations in several countries (e.g. Australia, the USA, Switzerland, Spain and Italy) enables ABC profitability analysis to be applied in hospitals. These countries apply the Diagnosis Related Gr

> Raab, Shoemaker and Mayer (2007) developed a workable ABC model for a restaurant operation in the USA that enabled previously undistributed indirect operating expenses to be traced to individual menu items. Menu prices were previously determined on a cos

> Until recently, Xu Ji Electric Co Ltd was a typical state-owned Chinese enterprise manufacturing electrical product such as relays. From an accounting point of view, this implied a manual book-keeping system which was primarily designed to meet external

> In recent years, two global companies have had to deal with some quite large costs as a result of quality control failures. First, take the example of Toyota cars in the USA. In late 2009 and early 2010, Toyota recalled several of its US models, the Camr

> In an article in Strategic Finance, Garry Cokins states that many companies’ managerial accounting systems are not able to report customer profitability information to support analysis for how to rationalize which types of customers to retain, grow or wi

> In the first quarter of the year 2015/2016, City Steel’s total revenues (THB 135.44 million) decreased by 35 per cent compared with the previous year. Adverse economic conditions caused the Group’s products to decrease substantially and made price compet

> Apple Inc. is well known for developing innovative products like the iPhone, iPad and iPod. Such devices are manufactured with complex electronic components and incur substantial design and development costs. The actual cost of manufacture of these produ

> Cloud computing is a term used to describe the delivery of information systems without, for example, the purchase of physical hardware or even software in some instances. What this means for an average business is that they can purchase processing capabi

> Asda is staging a major push south opening 11 new stores in the greater London region over the next few months with plans for a further 150 by 2018. Two of the new stores will be a trial of a new smaller format. These will be Asda’s first ‘High Street’ s

> The economic recession has resulted in original equipment manufacturers (OEMs) seeking to drive down costs by re-examining their manufacturing strategy, with many companies increasing their level of outsourcing, writes Ronnie Darroch, Plexus regional pre

> According to an article authored by Yayla-Küllü et al., multi-product firms account for 91 per cent of the output in US manufacturing and they often make short- to medium-term adjustments in their product-lines. For many of these product-line decisions,

> Most developed economies have well-developed road and highway networks. From time to time new highways are built to relieve congested cities, but by and large most developed countries are not embarking on major road-building projects. Reducing government

> Operating leverage can tell investors a lot about a company’s risk profile, and although high operating leverage can often benefit companies, firms with high operating leverage are also vulnerable to sharp economic and business cycle swings. In good time

> According to the International Air and Transport Association (IATA) conference airlines were expected to make around £3.18 profit from each passenger in 2014. Although carriers were expecting net profits of £11 billion, margins were so thin the air indus

> Every time Apple releases a new device it cannot satisfy immediate demand. This is a result of Apple’s precise JIT manufacturing system. Apple does not wish to take the risk of producing more devices than it will sell, so it adjusts manufacturing to matc

> The break-even price of crude oil includes production costs, exploring or finding costs, oil well development costs, transportation costs, and selling and general administration expenses. A survey published in 2015 showed some interesting insights into t

> The Airbus A380 was the world’s first double decker aircraft. It can accommodate from 555 to 853 passengers depending on the class configuration. Long haul airlines such as Singapore Airlines were early adopters of the aircraft back in 2007. The 2016 lis

> Bubble tea cafés are becoming increasingly popular across Malaysia and in recent years, many new chains have been formed, opening cafés in mainly urban locations. Leading bubble tea firms provide some interesting information on the rapid growth of the p

> SAP, the global leader in enterprise resource planning (ERP) systems, offers several tools to help a business find an optimal solution to scheduling and planning problems. The advanced planner and optimizer (APO) offer solutions to help firms find the be

> In the March 2016 edition of CIMA’s Financial Management journal, Lawrie Homes interviewed Noel Togoe, CIMA’S director of Education. Togoe stated that value measurement has been an area of dramatic change affecting the financial management landscape. The

> Goode, Billings and Prosper plc manufactures two products, Razzle and Dazzle. Unit selling prices and variable costs, and daily fixed costs are: Production of the two products is restricted by limited supplies of three essential inputs: Raz, Ma and Taz

> A company makes two products, X and Y. Product X has a contribution of £124 per unit and product Y £80 per unit. Both products pass through two departments for processing and the times in minutes per unit are: Currently there

> G Limited, manufacturers of superior garden ornaments, is preparing its production budget for the coming period. The company makes four types of ornament, the data for which are as follows: Fixed overhead amounts to £15 000 per period. Ea

> The Ruddle Co. Ltd had planned to install and, with effect from next April, commence operating sophisticated machinery for the production of a new product – product Zed. However, the supplier of the machinery has just announced that del

> Warren Ltd is to produce a new product in a short-term venture which will utilize some obsolete materials and expected spare capacity. The new product will be advertised in quarter I with production and sales taking place in quarter II. No further produc

> Z Ltd is considering various product pricing and material purchasing options with regard to a new product it has in development. Estimates of demand and costs are as follows: Each unit requires 3kg of material and because of storage problems any unused

> Crabbe, the owner of the Ocean Hotel, is concerned about the hotel’s finances and has asked your advice. Crabbe gives you the following information: ‘We have rooms for 80 guests. When the hotel is open, whatever the le

> The term TetraPak® is one which is familiar to most consumers – it is the name you will see on the card cartons in which milk, juice and other liquid products are frequently packaged. The Tetra group offers a broader range of food processing solutions be

> A ticket agent has an arrangement with a concert hall that holds pop concerts on 60 nights a year whereby he receives discounts as follows per concert: For purchase of: ……………………………………………. He receives a discount of: 200 tickets ………………………………………………………………………

> The accountant of Laburnum Ltd is preparing documents for a forthcoming meeting of the budget committee. Currently, variable cost is 40 per cent of selling price and total fixed costs are £40 000 per year. The company uses an historical cost

> Seeprint Limited is negotiating an initial one-year contract with an important customer for the supply of a specialized printed colour catalogue at a fixed contract price of £16 per catalogue. Seeprint’s normal capacity for

> A company sells and services photocopying machines. Its sales department sells the machines and consumables, including ink and paper, and its service department provides an after-sales service to its customers. The after-sales service includes planned ma

> Excel Ltd make and sell two products, VG4U and VG2. Both products are manufactured through two consecutive processes – making and packing. Raw material is input at the commencement of the making process. The following estimated informat

> ABC plc, a group operating retail stores, is compiling its budget statements for the next year. In this exercise, revenues and costs at each store A, B and C are predicted. Additionally, all central costs of warehousing and a head office are allocated ac

> Duo plc produces two products, A and B. Each has two components specified as sequentially numbered parts, i.e. product A (parts 1 and 2) and product B (parts 3 and 4). Two production departments (machinery and fitting) are supported by five service activ

> Trimake Limited makes three main products, using broadly the same production methods and equipment for each. A conventional product costing system is used at present, although an activity-based costing (ABC) system is being considered. Details of the thr

> A product is manufactured by passing through three processes: A, B and C. In process C a by-product is also produced which is then transferred to process D where it is completed. For the first week in October, actual data included: Budgeted production

> It has been stated that companies do not have profitable products, only profitable customers. Many companies have placed emphasis on the concept of customer account profitability (CAP) analysis in order to increase their earnings and returns to sharehold

> Finnish paper company M-real produced paper and packaging products, the demand for which is highly influenced by the demand for end consumer products. Global demand decreased due to the global economic recession and during this same time energy and fuel

> The traditional methods of cost allocation, cost apportionment and absorption into products are being challenged by some writers who claim that much information given to management is misleading when these methods of dealing with fixed overheads are used

> Nuts plc produces alpha and beta in two stages. The separation process produces crude alpha and beta from a raw material costing £170 per tonne. The cost of the separation process is £100 per tonne of raw material. Each tonne of

> AB plc makes two products, Alpha and Beta. The company made a £500 000 profit last year and proposes an identical plan for the coming year. The relevant data for last year are summarized in Table 1. Table 1: Actuals for last year Fixed cos

> French Ltd is about to commence operations utilizing a simple production process to produce two products X and Y. It is the policy of French to operate the new factory at its maximum output in the first year of operations. Cost and production details est

> Sniwe plc intend to launch a commemorative product on 1 August 2017 for a sports event commencing in 2019. The product will have variable costs of £16 per unit. Production capacity available for the product is sufficient for 2000 units per annum. Sniwe p

> Josun plc manufactures cereal-based foods, including various breakfast cereals under private brand labels. In March the company had been approached by Cohin plc, a large national supermarket chain, to tender for the manufacture and supply of a crunchy-st

> A producer of high-quality executive motor cars has developed a new model that it knows to be very advanced both technically and in style by comparison with the competition in its market segment. The company’s reputation for high quality is well establi

> A company supplying capital equipment to the engineering industry is part of a large group of diverse companies. It determines its tender prices by adding a standard profit margin as a percentage of its prime cost. Although it is working at full capacity

> A South American farmer has 960 hectares of land on which he grows squash, kale, lettuce and beans. Of the total, 680 hectares are suitable for all four vegetables, but the remaining 280 hectares are suitable only for kale and lettuce. Labour for all kin

> According to a recent survey undertaken by CIMA, variable (or marginal) costing is used by almost 40 per cent of firms. Management accountants from a wide range of sectors, including manufacturing and service firms, were queried on how they use tradition

> B Ltd manufactures a range of products which are sold to a limited number of wholesale outlets. Four of these products are manufactured in a particular department on common equipment. No other facilities are available for the manufacture of these product

> PQR Limited is an engineering company engaged in the manufacture of components and finished products. The company is highly mechanized and each of the components and finished products requires the use of one or more types of machine in its machining depa

> PDR plc manufactures four products using the same machinery. The following details relate to its products: There is a maximum of 2000 machine hours available per week. Requirement: (a). Determine the production plan which will maximize the weekly pr

> A company is currently manufacturing at only 60 per cent of full practical capacity, in each of its two production departments, due to a reduction in market share. The company is seeking to launch a new product which, it is hoped, will recover some lost

> (a). ‘While the ascertainment of product costs could be said to be one of the objectives of cost accounting, where joint products are produced and joint costs incurred, the total cost computed for the product may depend on the method se

> JB Limited is a small specialist manufacturer of electronic components and much of its output is used by the makers of aircraft for both civil and military purposes. One of the few aircraft manufacturers has offered a contract to JB Limited for the suppl

> Shown below is a typical cost–volume– profit chart: Required: (a). Explain to a colleague who is not an accountant the reasons for the change in result on this cost–volume–profit

> York plc was formed three years ago by a group of research scientists to market a new medicine that they had developed. The technology involved in the medicine’s manufacture is both complex and expensive. Because of this, the company is

> Video Technology Plc was established in 1987 to assemble video cassette recorders (VCRs). There is now increased competition in its markets and the company expects to find it difficult to make an acceptable profit next year. You have been appointed as an

> (a). ‘The analysis of total cost into its behavioural elements is essential for effective cost and management accounting.’ Required: Comment on the statement above, illustrating your answer with examples of cost behaviour patterns. (b). The total costs i

> Each year, the paper and pulp industry produce millions of tonnes of sludge in the production of paper. This sludge is typically disposed of in landfill sites or incinerated. Both disposal methods are costly and environmentally undesirable. However, some

> (a). Identify and discuss briefly five assumptions underlying cost–volume–profit analysis. (b). A local authority, whose area includes a holiday resort situated on the east coast, operates, for 30 weeks each year, a holiday home which is let to visiting

> JK Limited has prepared a budget for the next 12 months when it intends to make and sell four products, details of which are shown below: Budgeted fixed costs are £240 000 per annum and total assets employed are £570 000. You

> A manufacturer of glass bottles has been affected by competition from plastic bottles and is currently operating at between 65 and 70 per cent of maximum capacity. The company at present reports profits on an absorption costing basis but with the high f

> ‘A break-even chart must be interpreted in the light of the limitations of its underlying assumptions …’ (From Cost Accounting: A Managerial Emphasis, by C.T. Horngren.) Required: (a). Discuss the extent to which the above statement is valid and both d

> The graphs shown below show cost– volume–profit relationships as they are typically represented in (i) management accounting and (ii) economic theory. In each graph, T = total revenue, TC = total cost, and P = profit.

> A local government authority owns and operates a leisure centre with numerous sporting facilities, residential accommodation, a cafeteria and a sports shop. The summer season lasts for 20 weeks including a peak period of six weeks corresponding to the sc

> A company has two products with the following unit costs for a period: Production and sales of the two products for the period were: Production was at normal levels. Unit costs in opening stock were the same as those for the period listed above. Req

> A chemical company produces among its product range two industrial cleaning fluids, A and B. These products are manufactured jointly. Total sales are expected to be restricted because home trade outlets for fluid B are limited to 54 000 gallons for the y

> A chemical company has a contract to supply annually 3600 tonnes of product A at £24 a tonne and 4000 tonnes of product B at £14.50 a tonne. The basic components for these products are obtained from a joint initial distillation

> The accountant of Minerva Ltd, a small company manufacturing only one product, wishes to decide how to present the company’s monthly management accounts. To date, only actual information has been presented on an historic cost basis, wit

> South Africa is one of the top gold producers in the world, holding about 6000 metric tons of reserves in mines as of 2015. Most mining operations have waste and by-products, some of which are disposable, reusable or even saleable, others are not. A by-p

> Synchro dot Ltd manufactures two standard products, product 1 selling at £15 and product 2 selling at £18. A standard absorption costing system is in operation and summarized details of the unit cost standards are as follows:

> A company manufactures a single product with the following variable costs per unit: Direct materials …………………&acir

> Solo Limited makes and sells a single product. The following data relate to periods 1 to 4: (£) Variable cost per unit ……………â€&br

> (a). Describe briefly three major differences between: (i). financial accounting, and (ii). cost and management accounting. (b). Below are incomplete cost accounts for a period: Stores ledger control account (£000) Opening balance …………………………………………………………

> The Isis Engineering Company operates a job order costing system which includes the use of predetermined overhead absorption rates. The company has two service cost centres and two production cost centres. The production cost centre overheads are charged

> On 1 October Bland Ltd opened a plant for making verniers. Data for the first two months’ operations are shown below: At 31 October the units in closing work in progress were 100 per cent complete for materials and 80 per cent complet

> (a). Describe the distinguishing characteristics of production systems where: (i). job costing techniques would be used, and (ii). process costing techniques would be used. (b). Job costing produces more accurate product costs than process costing. Crit

> Milo plc has a number of chemical processing plants in the UK. At one of these plants, it takes an annual input of 400 000 gallons of raw material A and converts it into two liquid products, B and C. The standard yield from one gallon of material A is 0

> A company manufactures four products from an input of a raw material to process 1. Following this process, product A is processed in process 2, product B in process 3, product C in process 4 and product D in process 5. The normal loss in process 1 is 10

> (a). A company uses a process costing system in which the following terms arise: conversion costs work in progress equivalent unit’s normal loss abnormal loss. Required: Provide a definition of each of these terms. (b). Explain how you would treat normal

> Bushmills Irish Whiskey, a world-renowned brand of Diageo plc, is distilled in County Antrim in Northern Ireland. The Old Bushmills distillery has been in operation since 1608 and currently markets five distinct whiskeys under the Bushmills brand. Whiske

> XYZ plc, a paint manufacturer, operates a process costing system. The following details related to process 2 for the month of October: Opening work in progress 5000 litres fully complete as to transfers from process 1 and 40% complete as to labour and ov

> On 30 October the following were among the balances in the cost ledger of a company manufacturing a single product (Product X) in a single process operation: The raw material ledger comprised the following balances at 30 October: 12 160kg of Product

> (a). You are required to explain and discuss the alternative methods of accounting for normal and abnormal spoilage. (b). Weston Harvey Ltd assembles and finishes trapfoils from bought-in components which are utilized at the beginning of the assembly pr

> A company produces a single product from one of its manufacturing processes. The following information of process inputs, outputs and work in progress relates to the most recently completed period: kg Opening work in progress …………………………………………………………… 21

> BEC Limited operates an absorption costing system. Its budget for the year ended 31 December shows that it expects its production overhead expenditure to be as follows: During the year it expects to make 200 000 units of its product. This is expected t

> ABC plc operates an integrated cost accounting system and has a financial year which ends on 30 September. It operates in a processing industry in which a single product is produced by passing inputs through two sequential processes. A normal loss of 10

> Industrial Solvents Limited mixes together three chemicals – A, B and C – in the ratio 3:2:1 to produce Allklean, a specialized anti-static fluid. The chemicals cost £8, £6 and £3.90 per litre respectively. In a period, 12 000 litres in total were input

> A large firm of solicitors uses a job costing system to identify costs with individual clients. Hours worked by professional staff are used as the basis for charging overhead costs to client services. A predetermined rate is used, derived from budgets dr

> A company produces several products which pass through the two production departments in its factory. These two departments are concerned with filling and sealing operations. There are two service departments, maintenance and canteen, in the factory. Pr

> A manufacturing company has prepared the following budgeted information for the forthcoming year: £ Direct material ………………………………………………………………………… 800 000 Direct labour …………………………………………………………………………… 200 000 Direct expenses ………………………………………………………………………… 40

> Almost all beer contains four basic ingredients – a grain (typically barley), water, hops and yeast. While the process of brewing can be complex and some ingredients varied, the basic process is quite consistent. First the barley (or other grain) is soak

> Just-in-Time (JIT) manufacturing and inventory systems have been operated by many companies to reduce manufacturing time, reduce waste and ultimately increase profitability. The JIT concept is based on close relationships with key suppliers, which means

> One of the production departments in A Ltd’s factory employs 52 direct operatives and nine indirect operatives. Basic hourly rates of pay are £14.40 and £11.70, respectively. Overtime, which is worked regularly

> (a). Identify the costs to a business arising from labour turnover. (5 marks) (b). A company operates a factory which employed 40 direct workers throughout the four-week period just ended. Direct employees were paid at a basic rate f £10.00 per hour for

> JR Co. Ltd’s budgeted overheads for the forthcoming period applicable to its production departments, are as follows: (£000) 1 …………â€

> (a). Explain why predetermined overhead absorption rates are preferred to overhead absorption rates calculated from factual information after the end of a financial period. (b). The production overhead absorption rates of factories X and Y are calculated