Question: On 30 October the following were among

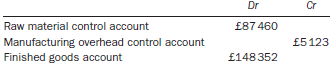

On 30 October the following were among the balances in the cost ledger of a company manufacturing a single product (Product X) in a single process operation:

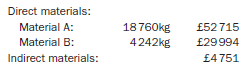

The raw material ledger comprised the following balances at 30 October:

12 160kg of Product X were in finished goods stock on 30 October. During November the following occurred:

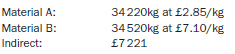

(i). Raw materials purchased on credit:

(ii). Raw materials issued from stock:

Direct materials are issued at weighted average prices (calculated at the end of each month to three decimal places of £).

(iii). Wages incurred:

Direct: ……………………………………………………… £186 743 (23 900 hours)

Indirect: ……………………………………………………………………………. £74 887

(iv). Other manufacturing overhead costs totalled £112 194. Manufacturing overheads are absorbed at a predetermined rate of £16.00 per direct labour hour. Any over-/under- absorbed overhead at the end of November should be left as a balance on the manufacturing overhead control account.

(v). 45 937kg of Product X were manufactured. There was no work in progress at the beginning or end of the period. A normal loss of 5 per cent of input is expected.

(vi). 43 210kg of Product X were sold. A monthly weighted average cost per kg (to three decimal places of £) is used to determine the production cost of sales.

Required:

(a). Prepare the following cost accounts for the month of November:

Raw material control account

Manufacturing overhead control account

Work in progress account

Finished goods account

All entries to the accounts should be rounded to the nearest whole £. Clearly show any workings supporting your answer.

(b). Explain the concept of equivalent units and its relevance in a process costing system.

Transcribed Image Text:

> Trimake Limited makes three main products, using broadly the same production methods and equipment for each. A conventional product costing system is used at present, although an activity-based costing (ABC) system is being considered. Details of the thr

> A product is manufactured by passing through three processes: A, B and C. In process C a by-product is also produced which is then transferred to process D where it is completed. For the first week in October, actual data included: Budgeted production

> It has been stated that companies do not have profitable products, only profitable customers. Many companies have placed emphasis on the concept of customer account profitability (CAP) analysis in order to increase their earnings and returns to sharehold

> Finnish paper company M-real produced paper and packaging products, the demand for which is highly influenced by the demand for end consumer products. Global demand decreased due to the global economic recession and during this same time energy and fuel

> The traditional methods of cost allocation, cost apportionment and absorption into products are being challenged by some writers who claim that much information given to management is misleading when these methods of dealing with fixed overheads are used

> Nuts plc produces alpha and beta in two stages. The separation process produces crude alpha and beta from a raw material costing £170 per tonne. The cost of the separation process is £100 per tonne of raw material. Each tonne of

> AB plc makes two products, Alpha and Beta. The company made a £500 000 profit last year and proposes an identical plan for the coming year. The relevant data for last year are summarized in Table 1. Table 1: Actuals for last year Fixed cos

> French Ltd is about to commence operations utilizing a simple production process to produce two products X and Y. It is the policy of French to operate the new factory at its maximum output in the first year of operations. Cost and production details est

> Sniwe plc intend to launch a commemorative product on 1 August 2017 for a sports event commencing in 2019. The product will have variable costs of £16 per unit. Production capacity available for the product is sufficient for 2000 units per annum. Sniwe p

> Josun plc manufactures cereal-based foods, including various breakfast cereals under private brand labels. In March the company had been approached by Cohin plc, a large national supermarket chain, to tender for the manufacture and supply of a crunchy-st

> A producer of high-quality executive motor cars has developed a new model that it knows to be very advanced both technically and in style by comparison with the competition in its market segment. The company’s reputation for high quality is well establi

> A company supplying capital equipment to the engineering industry is part of a large group of diverse companies. It determines its tender prices by adding a standard profit margin as a percentage of its prime cost. Although it is working at full capacity

> Johnson trades as a chandler at the Savoy Marina. His profit in this business during the year to 30 June was £12 000. Johnson also undertakes occasional contracts to build pleasure cruisers, and is considering the price at which to bid for t

> A South American farmer has 960 hectares of land on which he grows squash, kale, lettuce and beans. Of the total, 680 hectares are suitable for all four vegetables, but the remaining 280 hectares are suitable only for kale and lettuce. Labour for all kin

> According to a recent survey undertaken by CIMA, variable (or marginal) costing is used by almost 40 per cent of firms. Management accountants from a wide range of sectors, including manufacturing and service firms, were queried on how they use tradition

> B Ltd manufactures a range of products which are sold to a limited number of wholesale outlets. Four of these products are manufactured in a particular department on common equipment. No other facilities are available for the manufacture of these product

> PQR Limited is an engineering company engaged in the manufacture of components and finished products. The company is highly mechanized and each of the components and finished products requires the use of one or more types of machine in its machining depa

> PDR plc manufactures four products using the same machinery. The following details relate to its products: There is a maximum of 2000 machine hours available per week. Requirement: (a). Determine the production plan which will maximize the weekly pr

> A company is currently manufacturing at only 60 per cent of full practical capacity, in each of its two production departments, due to a reduction in market share. The company is seeking to launch a new product which, it is hoped, will recover some lost

> (a). ‘While the ascertainment of product costs could be said to be one of the objectives of cost accounting, where joint products are produced and joint costs incurred, the total cost computed for the product may depend on the method se

> JB Limited is a small specialist manufacturer of electronic components and much of its output is used by the makers of aircraft for both civil and military purposes. One of the few aircraft manufacturers has offered a contract to JB Limited for the suppl

> Shown below is a typical cost–volume– profit chart: Required: (a). Explain to a colleague who is not an accountant the reasons for the change in result on this cost–volume–profit

> York plc was formed three years ago by a group of research scientists to market a new medicine that they had developed. The technology involved in the medicine’s manufacture is both complex and expensive. Because of this, the company is

> Video Technology Plc was established in 1987 to assemble video cassette recorders (VCRs). There is now increased competition in its markets and the company expects to find it difficult to make an acceptable profit next year. You have been appointed as an

> (a). ‘The analysis of total cost into its behavioural elements is essential for effective cost and management accounting.’ Required: Comment on the statement above, illustrating your answer with examples of cost behaviour patterns. (b). The total costs i

> Each year, the paper and pulp industry produce millions of tonnes of sludge in the production of paper. This sludge is typically disposed of in landfill sites or incinerated. Both disposal methods are costly and environmentally undesirable. However, some

> (a). Identify and discuss briefly five assumptions underlying cost–volume–profit analysis. (b). A local authority, whose area includes a holiday resort situated on the east coast, operates, for 30 weeks each year, a holiday home which is let to visiting

> JK Limited has prepared a budget for the next 12 months when it intends to make and sell four products, details of which are shown below: Budgeted fixed costs are £240 000 per annum and total assets employed are £570 000. You

> A manufacturer of glass bottles has been affected by competition from plastic bottles and is currently operating at between 65 and 70 per cent of maximum capacity. The company at present reports profits on an absorption costing basis but with the high f

> ‘A break-even chart must be interpreted in the light of the limitations of its underlying assumptions …’ (From Cost Accounting: A Managerial Emphasis, by C.T. Horngren.) Required: (a). Discuss the extent to which the above statement is valid and both d

> The graphs shown below show cost– volume–profit relationships as they are typically represented in (i) management accounting and (ii) economic theory. In each graph, T = total revenue, TC = total cost, and P = profit.

> A local government authority owns and operates a leisure centre with numerous sporting facilities, residential accommodation, a cafeteria and a sports shop. The summer season lasts for 20 weeks including a peak period of six weeks corresponding to the sc

> A company has two products with the following unit costs for a period: Production and sales of the two products for the period were: Production was at normal levels. Unit costs in opening stock were the same as those for the period listed above. Req

> A chemical company produces among its product range two industrial cleaning fluids, A and B. These products are manufactured jointly. Total sales are expected to be restricted because home trade outlets for fluid B are limited to 54 000 gallons for the y

> A chemical company has a contract to supply annually 3600 tonnes of product A at £24 a tonne and 4000 tonnes of product B at £14.50 a tonne. The basic components for these products are obtained from a joint initial distillation

> The accountant of Minerva Ltd, a small company manufacturing only one product, wishes to decide how to present the company’s monthly management accounts. To date, only actual information has been presented on an historic cost basis, wit

> South Africa is one of the top gold producers in the world, holding about 6000 metric tons of reserves in mines as of 2015. Most mining operations have waste and by-products, some of which are disposable, reusable or even saleable, others are not. A by-p

> Synchro dot Ltd manufactures two standard products, product 1 selling at £15 and product 2 selling at £18. A standard absorption costing system is in operation and summarized details of the unit cost standards are as follows:

> A company manufactures a single product with the following variable costs per unit: Direct materials …………………&acir

> Solo Limited makes and sells a single product. The following data relate to periods 1 to 4: (£) Variable cost per unit ……………â€&br

> (a). Describe briefly three major differences between: (i). financial accounting, and (ii). cost and management accounting. (b). Below are incomplete cost accounts for a period: Stores ledger control account (£000) Opening balance …………………………………………………………

> The Isis Engineering Company operates a job order costing system which includes the use of predetermined overhead absorption rates. The company has two service cost centres and two production cost centres. The production cost centre overheads are charged

> On 1 October Bland Ltd opened a plant for making verniers. Data for the first two months’ operations are shown below: At 31 October the units in closing work in progress were 100 per cent complete for materials and 80 per cent complet

> (a). Describe the distinguishing characteristics of production systems where: (i). job costing techniques would be used, and (ii). process costing techniques would be used. (b). Job costing produces more accurate product costs than process costing. Crit

> Milo plc has a number of chemical processing plants in the UK. At one of these plants, it takes an annual input of 400 000 gallons of raw material A and converts it into two liquid products, B and C. The standard yield from one gallon of material A is 0

> A company manufactures four products from an input of a raw material to process 1. Following this process, product A is processed in process 2, product B in process 3, product C in process 4 and product D in process 5. The normal loss in process 1 is 10

> (a). A company uses a process costing system in which the following terms arise: conversion costs work in progress equivalent unit’s normal loss abnormal loss. Required: Provide a definition of each of these terms. (b). Explain how you would treat normal

> Bushmills Irish Whiskey, a world-renowned brand of Diageo plc, is distilled in County Antrim in Northern Ireland. The Old Bushmills distillery has been in operation since 1608 and currently markets five distinct whiskeys under the Bushmills brand. Whiske

> XYZ plc, a paint manufacturer, operates a process costing system. The following details related to process 2 for the month of October: Opening work in progress 5000 litres fully complete as to transfers from process 1 and 40% complete as to labour and ov

> (a). You are required to explain and discuss the alternative methods of accounting for normal and abnormal spoilage. (b). Weston Harvey Ltd assembles and finishes trapfoils from bought-in components which are utilized at the beginning of the assembly pr

> A company produces a single product from one of its manufacturing processes. The following information of process inputs, outputs and work in progress relates to the most recently completed period: kg Opening work in progress …………………………………………………………… 21

> BEC Limited operates an absorption costing system. Its budget for the year ended 31 December shows that it expects its production overhead expenditure to be as follows: During the year it expects to make 200 000 units of its product. This is expected t

> ABC plc operates an integrated cost accounting system and has a financial year which ends on 30 September. It operates in a processing industry in which a single product is produced by passing inputs through two sequential processes. A normal loss of 10

> Industrial Solvents Limited mixes together three chemicals – A, B and C – in the ratio 3:2:1 to produce Allklean, a specialized anti-static fluid. The chemicals cost £8, £6 and £3.90 per litre respectively. In a period, 12 000 litres in total were input

> A large firm of solicitors uses a job costing system to identify costs with individual clients. Hours worked by professional staff are used as the basis for charging overhead costs to client services. A predetermined rate is used, derived from budgets dr

> A company produces several products which pass through the two production departments in its factory. These two departments are concerned with filling and sealing operations. There are two service departments, maintenance and canteen, in the factory. Pr

> A manufacturing company has prepared the following budgeted information for the forthcoming year: £ Direct material ………………………………………………………………………… 800 000 Direct labour …………………………………………………………………………… 200 000 Direct expenses ………………………………………………………………………… 40

> Almost all beer contains four basic ingredients – a grain (typically barley), water, hops and yeast. While the process of brewing can be complex and some ingredients varied, the basic process is quite consistent. First the barley (or other grain) is soak

> Just-in-Time (JIT) manufacturing and inventory systems have been operated by many companies to reduce manufacturing time, reduce waste and ultimately increase profitability. The JIT concept is based on close relationships with key suppliers, which means

> One of the production departments in A Ltd’s factory employs 52 direct operatives and nine indirect operatives. Basic hourly rates of pay are £14.40 and £11.70, respectively. Overtime, which is worked regularly

> (a). Identify the costs to a business arising from labour turnover. (5 marks) (b). A company operates a factory which employed 40 direct workers throughout the four-week period just ended. Direct employees were paid at a basic rate f £10.00 per hour for

> JR Co. Ltd’s budgeted overheads for the forthcoming period applicable to its production departments, are as follows: (£000) 1 …………â€

> (a). Explain why predetermined overhead absorption rates are preferred to overhead absorption rates calculated from factual information after the end of a financial period. (b). The production overhead absorption rates of factories X and Y are calculated

> Dunstan Ltd manufactures tents and sleeping bags in three separate production departments. The principal manufacturing processes consist of cutting material in the pattern cutting room and sewing the material in either the tent or the sleeping bag depart

> A company makes a range of products with total budgeted manufacturing overheads of £973 560 incurred in three production departments (A, B and C) and one service department. Department A has ten direct employees, who each work 37 hours per week. Departme

> Incorporated Finance plc is a finance company that has 100 branch offices in major towns and cities throughout the UK. These offer a variety of hire purchase and loan facilities to personal customers both directly and through schemes operated on behalf o

> A new private hospital of 100 beds was opened to receive patients on 2 January although many senior staff members including the supervisor of the laundry department had been in situ for some time previously. The first months were expected to be a settlin

> 1. You are the group management accountant of a large divisionalized group. There has been extensive board discussion of the existing system of rewarding divisional general managers with substantial bonuses based on the comparison of the divisional prof

> Jim Smith has recently been appointed as the headteacher of Mayfield School in Midshire. The age of the pupils ranges from 11 years to 18 years. For many years, Midshire County Council was responsible for preparing and reporting on the school budget. Fro

> According to the Plex website, in their Enterprise Resource Planning Systems cost accounting software modules you can: ● Set up a flexible, detailed cost structure for each operation and for each product, including purchased materials, ingredients and co

> You have been provided with the following operating statement, which represents an attempt to compare the actual performance for the quarter which has just ended with the budget: Required: (a). Using a flexible budgeting approach, re-draft the operati

> Rainbow Ltd is a manufacturer that uses alkahest in many of its products. At present the company has an alkahest plant on a site close to the company’s main factory. A summary of the alkahest plants budget for the next year is shown below: Production ……

> The financial controller of Mexet plc is reviewing the company’s stock management procedures. Stock has gradually increased to 25 per cent of the company’s total assets and, with finance costs at 14 per cent per annum,

> A company needs to hold a stock of item X for sale to customers. Although the item is of relatively small value per unit, the customers’ quality control requirements and the need to obtain competitive supply tenders at frequent intervals result in high p

> Hint: Reverse the signs and ignore entries of 0 and 1. The Kaolene Co. Ltd has six different products all made from fabricated steel. Each product passes through a combination of five production operations: cutting, forming, drilling, welding and coating

> (a). The Argonaut Company makes three products, Xylos, Yo-yos and Zicons. These are assembled from two components, Agrons and Bovons, which can be produced internally at a variable cost of £5 and £8 each respectively. A limited

> ‘Attributing direct costs and absorbing overhead costs to the product/service through an activity-based costing approach will result in a better understanding of the true cost of the final output.’ (Source: a recent CIMA publication on costing in a servi

> Usine Ltd is a company whose objective is to maximize profits. It manufactures two speciality chemical powders, gamma and delta, using three processes: heating, refining and blending. The powders can be produced and sold in infinitely divisible quantitie

> For the relevant cost data in items (1) – (7), indicate which of the following is the best classification. (a). sunk cost; (b). incremental cost; (c). variable cost; (d). fixed cost; (e). semi-variable cost; (f). semi-fixed cost; (g). controllable cost;

> XY Limited commenced trading on 1 February with fully paid issued share capital of £500 000, Fixed Assets of £275 000 and Cash at Bank of £225 000. By the end of April, the following transactions had taken place: 1.

> Capturing labour costs accurately includes capturing time worked on customer orders, jobs or projects. In some cases, this is a reasonably easy task – such as in a supervised factory setting. In some cases, capturing hours worked accurately can be more d

> A company is planning to purchase 90 800 units of a particular item in the year ahead. The item is purchased in boxes, each containing ten units of the item, at a price of £200 per box. A safety stock of 250 boxes is kept. The cost of holding an item in

> Present a table of production times showing the following columns for E. Condon Ltd, which produces up to 16 units while experiencing a 90 per cent learning curve, the first unit requiring 1000 hours of production time: 1. units produced; 2. total produc

> The following information relates to a manufacturing process for a period: Materials costs ……………………………………………………………………… £16 445 Labour and overhead costs ……………………………………………………… £28 596 10 000 units of output were produced by the process in the period, of

> Mr Evans is a wholesaler who buys and sells a wide range of products, one of which is the Laker. Mr Evans sells 24 000 units of the Laker each year at a unit price of £20. Sales of the Laker normally follow an even pattern throughout the year but to prot

> Wagtail Ltd uses the ‘optimal batch size’ model (see below) to determine optimal levels of raw materials. Material B is consumed at a steady, known rate over the company’s planning horizon of one year; the current usage is 4000 units per annum. The costs

> Whirlygig plc manufactures and markets automatic dishwashing machines. Among the components that it purchases each year from external suppliers for assembly into the finished article are window units, of which it uses 20 000 units per annum. It is consid

> A company is reviewing the purchasing policy for one of its raw materials as a result of a reduction in production requirement. The material, which is used evenly throughout the year, is used in only one of the company’s products, the production of which

> A company is considering the possibility of purchasing from a supplier a component it now makes. The supplier will provide the components in the necessary quantities at a unit price of £9. Transportation and storage costs would be negligible. The company

> Sandy Lands Ltd carries an item of inventory in respect of which the following data apply: fixed cost of ordering per batch ……………………………………………………. £10 expected steady quarterly volume of sales …………………………… 3125 units cost of holding one unit in stock for

> Exel Division is part of the Supeer Group. It produces a basic fabric that is then converted in other divisions within the group. The fabric is also produced in other divisions within the Supeer Group and a limited quantity can be purchased from outside

> It was decided in the first quarter of fiscal 2016 that Commercial Metals Company Ltd would change the accounting method it used to value its inventories. This change would be for its Americas Mills, Americas Recycling and Americas Fabrication segments.

> Leano plc is investigating the financial viability of a new product X. Product X is a short life product for which a market has been identified at an agreed design specification. It is not yet clear whether the market life of the product will be six mont

> Engcorp and Flotilla are UK divisions of Griffin plc, a multinational company. Both divisions have a wide range of activities. You are an accountant employed by Griffin plc and the finance director has asked you to investigate a transfer pricing problem.

> The Crispy Biscuit Company (CBC) has developed a new variety of biscuit that it has successfully test marketed in different parts of the country. It has, therefore, decided to go ahead with full-scale production and is in the process of commissioning a p

> A management accountant is analyzing data relating to retail sales on behalf of marketing colleagues. The marketing staff believes that the most important influence on sales is local advertising undertaken by the retail store. The company also advertises

> Abourne Ltd manufactures a microcomputer for the home use market. The management accountant is considering using regression analysis in the annual estimate of total costs. The following information has been produced for the 12 months ended 31 December:

> (a). Comment on factors likely to affect the accuracy of the analysis of costs into fixed and variable components. (b). Explain how the analysis of costs into fixed and variable components is of use in planning, control and decision-making techniques use

> Explain the ‘learning curve’ and discuss its relevance to setting standards.

> Fabri Division is part of the Multo Group. Fabri Division produces a single product for which it has an external market that utilizes 70 per cent of its production capacity. Gini Division, which is also part of the Multo Group requires units of the produ