Question: Refer to Google’s financial statements in

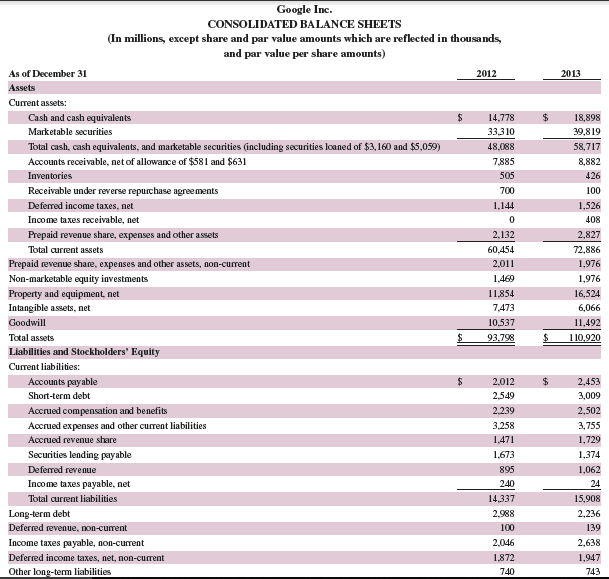

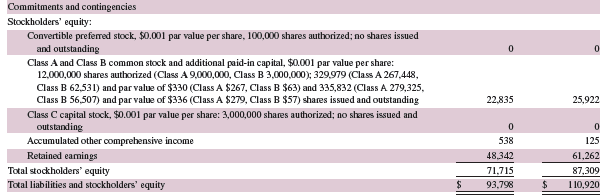

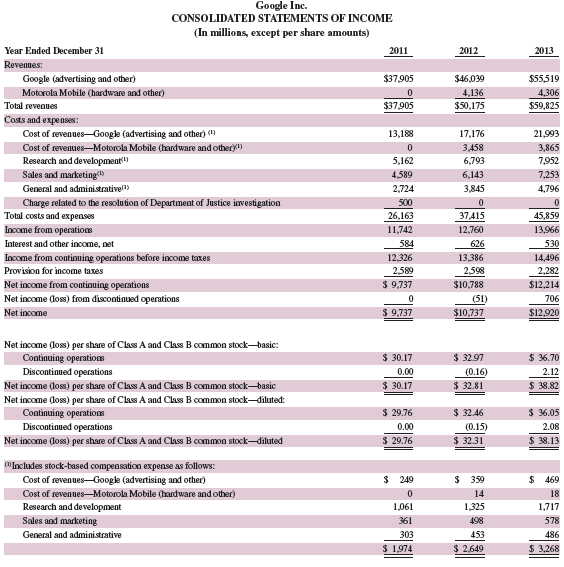

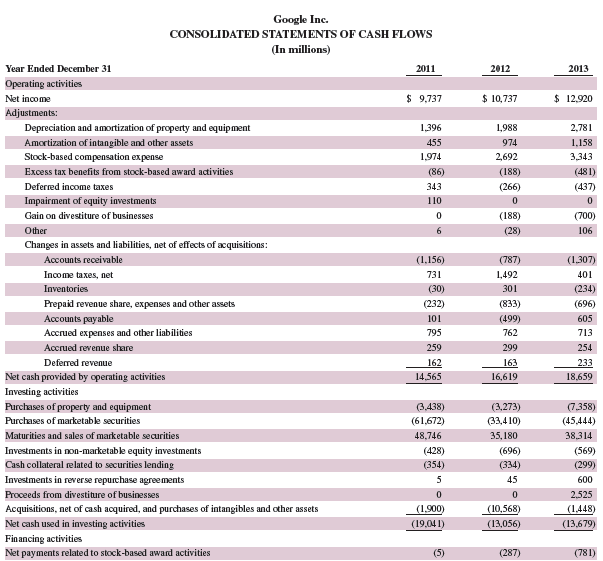

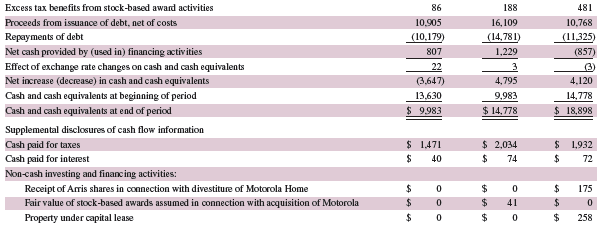

Refer to Google’s financial statements in Appendix A. Identify Google’s net earnings (income) for the year ended December 31, 2013. Is its net earnings equal to the increase in cash and cash equivalents for the year? Explain the difference between net earnings and the increase in cash and cash equivalents.

Google’s financial statements from Appendix A:

Transcribed Image Text:

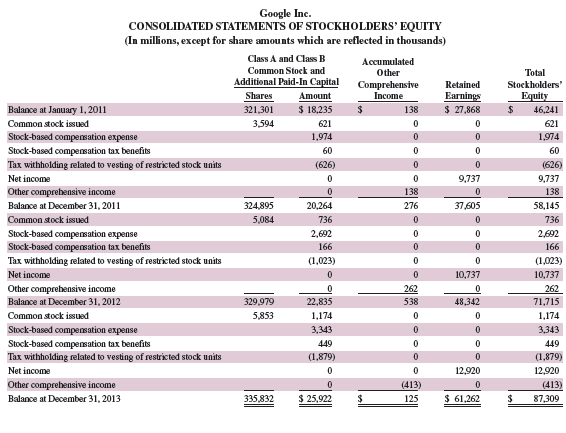

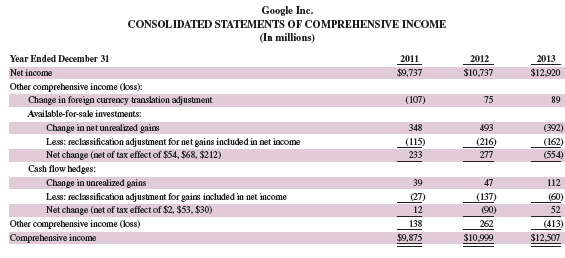

Google Inc. CONSOLIDATED BALANCE SHEETS (In millions, except share and par value amounts which are reflected in thousands, and par value per share amounts) As of December 31 2012 2013 Assets Current assets: Cash and cash equivalents 14,778 18,898 Marketable securities 33,310 39,819 Total cash, cash equivalents, and marketable securities (including securities loaned of $3,160 and $5,059) 48,088 58,717 Accounts receivable, net of allowance of $581 and $631 7,885 8,882 Inventories 505 426 Receivable under reverse repurchase agreements 700 100 Deferred income taxes, net 1,144 1,526 Income taxes receivable, net 408 Prepaid revenue share, expenses and other assets 2,132 2,827 Total current assets 60,454 72,886 Prepaid revenue share, expenses and other assets, non-current 2,011 1,976 Non-marketable equity investments 1,469 1,976 Property and equipment, net 11.854 16,524 Intangible assets, net 7,473 6,066 Goodwill 10,537 11,492 Total assets 93.798 110.920 Liabilities and Stockholders' equity Current liabilities: Accounts payable 2$ 2,012 24 2,453 Short-term debt 2,549 3,009 Accrued compensation and benefits 2.239 2,502 Accrued expenses and other current liabilities 3,258 3,755 Accrued revenue share 1,471 1,729 Securities lending payable 1,673 1,374 Deferred revenue 895 1,062 Income taxes payable, net 240 24 Total current liabilities 14,337 15,908 Long-term debt 2,988 2,236 Deferred revenue, non-current 100 139 Income taxes payable, non-current 2,046 2,638 Deferred income taxes, net, non-current 1,872 1,947 Other long-term liabilities 740 743 Commitments and contingencies Stockholders' equity: Convertible preferred stock, $0.001 par value per share, 100,000 shares authorized; no shares issued and outstanding Class A and Class B common stock and additional paid-in capital, $0.001 par value per share: 12,000,000 shares authorized (Class A 9,000,000, Class B 3,000,000); 329,979 (Class A 267,448, Class B 62,531) and par value of $330 (Class A $267, Class B $63) and 335,832 (Class A 279,325, Class B 56,507) and par value of $336 (Class A $279, Class B $57) shares issued and outstanding Class C capital stock, $0.001 par value per share: 3,000,000 shares authorized; no shares issued and outstanding 22,835 25,922 Accumulated other comprehensive income 538 125 Retained eamings 48,342 61,262 Total stockholders' equity 71,715 87,309 1 10,920 Total liabilities and stockholders' equity 93,798 Google Inc. CONSOLIDATED STATEMENTS OF INCOME (In millions, except per share amounts) Year Ended December 31 2011 2012 2013 Revenues: Google (advertising and other) $37,905 $46,039 $55,519 Motorola Mobile (hardware and other) 4,136 4,306 Total revenues $37,905 $50,175 $59,825 Costs and expenses: Cost of revenues-Google (advertising and other) ( 13,188 17,176 21,993 Cost of revenues–Motorola Mobile (hardware and othery) 3,458 3,865 Research and dewelopment) Sales and marketing General and administrative 5,162 6,793 7,952 4,589 6,143 7,253 2,724 3,845 4,796 Charge related to the resolution of Department of Justice imvestigation 500 37415 Total costs and expenses Income from operations 26,163 45,859 11,742 12,760 13,966 Interest and other income, net 584 626 530 14,496 2,282 Income from continuing operations before income taxes 12,326 13,386 Provision for income taxes 2,589 2,598 Net income from continuing operations $ 9,737 $10,788 $12,214 Net income (loss) from discontinuad operations (51) 706 Net income $ 9,737 $10,737 $12,920 Net income (loss) per share of Class A and Class B common stock-basic: Continuing operations $ 30.17 $ 36.70 $ 32.97 Discontinued operations 0.00 (0.16) 2.12 Net income (loss) per share of Class A and Class B common stock-basic $ 30.17 $ 32.81 $ 38.82 Net income (loss) per share of Class A and Class B common stock-diluted: Continuing operations $ 29.76 $ 32.46 $ 36.05 Discontinued operations 0.00 (0.15) 2.08 Net income (loss) per share of Clas A and Class B common stock-diluted $ 29.76 $ 32.31 $ 38.13 "Includes stock-based compensation expense as follows: Cost of revenues-Google (advertising and other) $ 249 $ 359 2$ 469 Cost of revenues-Motorola Mobile (hardware and other) 14 18 Research and development Sales and marketing 1,061 1,325 1,717 361 498 578 General and administrative 303 453 486 $ 1.974 $ 2,649 $ 3,268 Google Inc. CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (In millions, except for share amounts which are reflected in thousands) Class A and Class B Accumulated Other Comprehensive Income Common Stock and Total Additional Paid-In Capital Retained Stockholders' Earnings $ 27,868 Shares Amount equity Balance at January 1, 2011 321,301 $ 18,235 138 2$ 46,241 Common stock issued 3,594 621 621 Stock-based compensation expense 1,974 1,974 Stock-based compensation tax benefits 60 60 Tax withholding related to vesting of restricted stock units (626) (626) Net income 9,737 9,737 Other comprehensive income 138 138 Balance at December 31, 2011 324,895 20,264 276 37,605 58,145 Common stock issued 5,084 736 736 Stock-based compemation expense Stock-based compensation tax benefits 2,692 2,692 166 166 Tax withholding related to vesting of restricted stock units (1,023) (1,023) Net income 10,737 10,737 Other comprebensive income 262 262 Balance at December 31, 2012 329,979 22,835 538 48,342 71,715 Common stock issued 5,853 1,174 1,174 Stock-based compesation expense 3,343 3,343 Stock-based compensation tax benefits Tax withholding related to vesting of restricted stock units 449 449 (1,879) (1,879) Net income 12,920 12,920 Other comprehensive income Balance at December 31, 2013 (413) 125 (413) 335,832 $ 25,922 $ 61,262 87,309 Google Inc. CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (In millions) Year Ended December 31 2011 2012 2013 Net income $9,737 $10,737 $12,920 Other comprehensive income (loss): Change in foreign currency translation adjustment (107) 75 89 Available-for-sale investments: Change in net unrealized gains 348 493 (392) Less: reclassification adjustment for net gains included in net income Net change (net of tax effect of $54, $68, $212) Cash flow hedges: (115) (216) (162) 233 277 (554) Change in unrealized gains 39 47 112 (60) Less: reclassification adjustment for gains included in net income Net change (net of tax effect of $2, $53, $30) (27) (137) 12 (90) 52 Other comprehensive income (loss) 138 262 (413) Comprebensive income $9,875 $10,999 $12,507 Google Inc. CONSOLIDATED STATEMENTS OF CASH FLOWS (In millions) Year Ended December 31 2011 2012 2013 Operating activities Net income $ 9,737 $ 10,737 $ 12,920 Adjustments: Depreciation and amortization of property and equipment 1,396 1,988 2,781 amortization of intangible and other assets 455 974 1,158 Stock-based compensation expense 1,974 2,692 3343 Excess tax benefits from stock-based award activities (86) (188) (481) Deferred income taxes 343 (266) (437) Impairment of equity investments 110 Gain on divestiture of businesses (188) (700) Other 6 (28) 106 Changes in assets and liabilities, net of effects of acquisitions: Accounts receivable (1,156) (787) (1,307) Income taxes, net 731 1,492 401 Inventories (30) 301 (234) Prepaid revenue share, expenses and other assets (232) (833) (696) Accounts payable 101 (499) 605 Accrued expenses and other liabilities 795 762 713 Accrued revenue share 259 299 254 Deferred revenue 162 163 233 18,659 Net cash provided by operating activities 14,565 16,619 Investing activities Purchases of property and equipment (3,438) (3,273) (7,358) Purchases of marketable securities (61,672) (33,4 10) (45,444) Maturities and sales of marketable securities 48,746 35,180 38,314 (428) Investments in non-marketable equity investments Cash collateral related to securities lending (696) (569) (354) (334) (299) Investments in reerse repurchase agreements 45 600 Proceeds from divestiture of businesses 2,525 Acquisitions, net of cash acquired, and purchases of intangibles and other assets (1,900) (10,568) (1,448) Net cash used in investing activities (19,04 1) (13,056) (13,679) Financing activities Net payments related to stock-based award activities (5) (287) (781) Excess tax benefits from stock-based award activities 86 188 481 Proceeds from issuance of debt, net of costs 10.905 16,109 10,768 Repayments of debt (10,179) (14,781) (11,325) Net cash provided by (used in) financing activities 807 1,229 (857) Effect of exchange rate changes on cash and cash equivalents 22 (3) Net increase (decrease) in cash and cash equivalents (3,647) 4,795 4,120 Cash and cash equivalents at beginning of period 13,630 9,983 14,778 Cash and cash equivalents at end of period $ 9,983 $ 14,778 $ 18,898 Supplemental disclosures of cash flow information Cash paid for taxes $ 1,471 $ 2,034 1,932 Cash paid for interest 40 24 74 %24 72 Non-cash investing and financing activities: Receipt of Arris shares in connection with divestiture of Motorola Home 175 Fair value of stock-based awards assumed in connection with acquisition of Motorola $ 24 41 Property under capital lease 258

> Is the declining-balance method an acceptable way to compute depletion of natural resources? Explain.

> What is the process of allocating the cost of natural resources to expense as they are used?

> What characteristics of a plant asset make it different from other assets?

> Explain the accounting constraint of materiality.

> Why should cash receipts be deposited on the day of receipt?

> When do we know that a company has goodwill? When can goodwill appear in a company’s balance sheet?

> What is a petty cash receipt? Who should sign it?

> Which of the following assets—inventory, building, accounts receivable, or cash—is most liquid? Which is least liquid?

> What are the limitations of internal controls?

> When a store purchases merchandise, why are individual departments not allowed to directly deal with suppliers?

> Why should the person who keeps the records of an asset not be the person responsible for its custody?

> Why should responsibility for related transactions be divided among different departments or individuals?

> Internal control procedures are important in every business, but at what stage in the development of a business do they become especially critical?

> Apple’s statement of cash flows in Appendix A describes changes in cash and cash equivalents for the year ended September 28, 2013. What total amount is provided (used) by investing activities? What amount is provided (used) by financin

> List the seven broad principles of internal control.

> When a general journal entry is used to record sales returns, the credit of the entry must be posted twice. Does this cause the trial balance to be out of balance? Explain.

> What general procedures are applied in accounting for the acquisition and potential cost allocation of intangible assets?

> When special journals are used, they are usually used to record each of four different types of transactions. What are these four types of transactions?

> What purpose is served by the output devices of an accounting system?

> What is the difference between data that are stored off-line and data that are stored online?

> What is the purpose of an input device? Give examples of input devices for computer systems.

> What are source documents? Give two examples.

> Locate “Note 15” that reports Google’s geographical segments from its 2013 annual report on its website (Google.com). Identify its geographical segments and list the revenues for each.

> Why should sales to and receipts of cash from credit customers be recorded and posted immediately?

> Describe the procedures involving the use of copies of a company’s sales invoices as a sales journal.

> What are five basic components of an accounting system?

> When preparing interim financial statements, what two methods can companies utilize to estimate cost of goods sold and ending inventory?

> Samsung’s balance sheet in Appendix A reports the change in cash and equivalents for the year ended December 31, 2013. Identify the cash generated (or used) by operating activities, by investing activities, and by financing (funding) ac

> What factors contribute to (or cause) inventory shrinkage?

> Buyers negotiate purchase contracts with suppliers. What type of shipping terms should a buyer attempt to negotiate to minimize freight-in costs?

> Refer to the income statement of Samsung in Appendix A. Does its income statement report a gross profit figure? If yes, what is the amount? Income Statement of Samsung from Appendix A: Samsung Electronics Co, Ltd. and its subsidiaries CONSOLIDATED

> Refer to the income statement for Samsung in Appendix A. What does Samsung title its cost of goods sold account? Income Statement of Samsung from Appendix A: Samsung Electronics Co, Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF INCOME (In mi

> Refer to Google’s income statement in Appendix A. What title does it use for cost of goods sold? Google’s Income Statement from Appendix A: CONSOLIDATED STATEMENTS OF INCOME (In millions, except per share amounts

> What guidance does the accounting constraint of conservatism offer?

> What is the meaning of market as it is used in determining the lower of cost or market for inventory?

> Explain the following statement: “Inventory errors correct themselves.”

> What notations are entered into the Posting Reference column of a ledger account?

> Does the accounting concept of consistency preclude any changes from one accounting method to another?

> Locate “Note 11” that reports Apple’s segments from its September 28, 2013, annual report on its website (Apple.com). Compute the ratio “Operating income/Net sales” for each segment. Comment on the results.

> Can a company change its inventory method each accounting period? Explain.

> What does the full-disclosure principle prescribe if a company changes from one acceptable accounting method to another?

> If costs are declining, will the LIFO or FIFO method of inventory valuation yield the lower cost of goods sold? Why?

> What are the five fundamental principles of accounting information systems?

> Where is the amount of merchandise inventory disclosed in the financial statements?

> Describe how costs flow from inventory to cost of goods sold for the following methods: (a) FIFO and (b) LIFO.

> Management uses a voucher system to help control and monitor cash disbursements. Which of the four documents listed below are prepared as part of a voucher system of control? ______ a. Purchase order ______ b. Outstanding check ______ c. Invoice _____

> A good system of internal control for cash provides adequate procedures for protecting both cash receipts and cash disbursements. Identify each of the following statements as either true or false regarding this protection. ______ a. A basic guideline for

> Choose from the following list of terms/phrases to best complete the following statements. a. Cash b. Cash equivalents c. Outstanding check d. Liquidity e. Bank reconciliation f. Current assets 1. The ______ category includes currency and coins along

> An internal control system consists of all policies and procedures used to protect assets, ensure reliable accounting, promote efficient operations, and urge adherence to company policies. Evaluate each of the following statements and indicate which are

> Enter the letter of each system principle in the blank next to its best description. A. Control principle B. Relevance principle C. Compatibility principle D. Flexibility principle E. Cost-benefit principle ______ 1. The principle prescribes the accoun

> Identify the most likely role in an accounting system played by each of the numbered items 1 through 12 by assigning a letter from the list A through E on the left. A. Source documents B. Input devices C. Information processors D. Information storage E.

> Wilcox Electronics uses a sales journal, a purchases journal, a cash receipts journal, a cash disbursements journal, and a general journal as illustrated in this chapter. Wilcox recently completed the following transactions a through h. Identify the jour

> A solar company invests in the following securities. Identify those investments as either an investment in debt (D) securities or equity (E) securities. ______ a. U.S. treasury bonds ______ b. Google stock ______ c. Certificate of deposit ______ d. Ap

> Complete the following descriptions by filling in the blanks. 1. The controlling investor is called the ______, and the investee is called the ______. 2. A long-term investment classified as equity securities with controlling influence implies that the i

> Which of the following statements a through g are true of long-term investments? ______ a. They are held as an investment of cash available for current operations. ______ b. They can include funds earmarked for a special purpose, such as bond sinking fun

> 1. Prepare the journal entry to record Tamasine Company’s issuance of 5,000 shares of $100 par value, 7% cumulative preferred stock for $102 cash per share. 2. Assuming the facts in part 1, if Tamasine declares a year-end cash dividend, what is the amoun

> The stockholders’ equity section of Jun Company’s balance sheet as of April 1 follows. On April 2, Jun declares and distributes a 10% stock dividend. The stock’s per share market value on April 2 is $

> Prepare the issuer’s journal entry for each of the following separate transactions. a. On March 1, Atlantic Co. issues 42,500 shares of $4 par value common stock for $297,500 cash. b. On April 1, OP Co. issues no-par value common stock for $70,000 cash.

> Prepare the journal entry to record Jevonte Company’s issuance of 36,000 shares of its common stock assuming the shares have a: a. $2 par value and sell for $18 cash per share. b. $2 stated value and sell for $18 cash per share.

> Locate “Note 11” that reports Apple’s segments from its September 28, 2013, annual report on its website (Apple.com). Identify its segments and list the net sales for each.

> Foxburo Company expects to pay a $2.34 per share cash dividend this year on its common stock. The current market value of Foxburo stock is $32.50 per share. Compute the expected dividend yield on the Foxburo stock. Would you classify the Foxburo stock as

> Answer the following questions related to a company’s activities for the current year: 1. A review of the notes payable files discovers that three years ago the company reported the entire amount of a payment (principal and interest) on an installment no

> On May 3, Zirbal Corporation purchased 4,000 shares of its own stock for $36,000 cash. On November 4, Zirbal reissued 850 shares of this treasury stock for $8,500. Prepare the May 3 and November 4 journal entries to record Zirbal’s purchase and reissuanc

> Howe and Duley’s company is organized as a partnership. At the prior year-end, partnership equity totaled $150,000 ($100,000 from Howe and $50,000 from Duley). For the current year, partnership net income is $24,990 ($20,040 allocated to Howe and $4,950

> The Field, Brown & Snow partnership was begun with investments by the partners as follows: Field, $131,250; Brown, $165,000; and Snow, $153,750. The operations did not go well, and the partners eventually decided to liquidate the partnership, sharing all

> Amy and Lester are partners in operating a store. Without consulting Amy, Lester enters into a contract to purchase merchandise for the store. Amy contends that she did not authorize the order and refuses to pay for it. The vendor sues the partners for t

> Merger Co. has 10 employees, each of whom earns $2,000 per month and has been employed since January 1. FICA Social Security taxes are 6.2% of the first $117,000 paid to each employee, and FICA Medicare taxes are 1.45% of gross pay. FUTA taxes are 0.6% a

> On November 7, 2015, Mura Company borrows $160,000 cash by signing a 90-day, 8% note payable with a face value of $160,000. (1) Compute the accrued interest payable on December 31, 2015, (2) prepare the journal entry to record the accrued interest expe

> Dextra Computing sells merchandise for $6,000 cash on September 30 (cost of merchandise is $3,900). The sales tax law requires Dextra to collect 5% sales tax on every dollar of merchandise sold. Record the entry for the $6,000 sale and its applicable sal

> Garcia Co. owns equipment that cost $76,800, with accumulated depreciation of $40,800. Garcia sells the equipment for cash. Record the sale of the equipment assuming Garcia sells the equipment for (1) $47,000 cash, (2) $36,000 cash, and (3) $31,000 ca

> Refer to Samsung’s balance sheet in Appendix A. How does its cash (titled “Cash and cash equivalents”) compare with its other current assets (both in amount and percent) as of December 31, 2013? Compare and assess its cash at December 31, 2013, with its

> 1. Classify the following as either a revenue expenditure or a capital expenditure. ______ a. Paid $40,000 cash to replace a compressor on a refrigeration system that extends its useful life by four years. ______ b. Paid $200 cash per truck for the cost

> A fleet of refrigerated delivery trucks is acquired on January 5, 2015, at a cost of $830,000 with an estimated useful life of eight years and an estimated salvage value of $75,000. Compute the depreciation expense for the first three years using the dou

> Answer each of the following related to international accounting standards. a. Accounting for plant assets involves cost determination, depreciation, additional expenditures, and disposals. Is plant asset accounting broadly similar or dissimilar between

> Caleb Co. owns a machine that costs $42,400 with accumulated depreciation of $18,400. Caleb exchanges the machine for a newer model that has a market value of $52,000. (1) Record the exchange assuming Caleb paid $30,000 cash and the exchange has commerc

> On August 2, 2015, Jun Co. receives a $6,000, 90-day, 12% note from customer Ryan Albany as payment on his $6,000 account. (1) Compute the maturity date for this note. (2) Prepare Jun’s journal entry for August 2.

> Warner Company’s year-end unadjusted trial balance shows accounts receivable of $99,000, allowance for doubtful accounts of $600 (credit), and sales of $280,000. Uncollectibles are estimated to be 1.5% of accounts receivable. 1. Prepare the December 31 y

> Gomez Corp. uses the allowance method to account for uncollectibles. On January 31, it wrote off an $800 account of a customer, C. Green. On March 9, it receives a $300 payment from Green. 1. Prepare the journal entry or entries for January 31. 2. Prepar

> Answer each of the following related to international accounting standards. a. Explain (in general terms) how the accounting for recognition of receivables is different between IFRS and U.S. GAAP. b. Explain (in general terms) how the accounting for valu

> The following data are taken from the comparative balance sheets of Ruggers Company. Compute and interpret its accounts receivable turnover for year 2015 (competitors average a turnover of 7.5). 2015 2014 Accounts receivable, net. $153,400 $138,500

> The following annual account balances are taken from Armour Sports at December 31. What is the change in the number of days’ sales uncollected between years 2014 and 2015? (Round the number of days to one decimal.) According to this a

> Credits to customer accounts and credits to Other Accounts are individually posted from a cash receipts journal such as the one in Exhibit 7.7. Why not put both types of credits in the same column and save journal space? Exhibit 7.7: Tasks Reports

> An entrepreneur commented that a bank reconciliation may not be necessary as she regularly reviews her online bank statement for any unusual items and errors. a. Describe how a bank reconciliation and an online review (or reading) of the bank statement a

> For each of the following items a through g, indicate whether its amount (1) affects the bank or book side of a bank reconciliation, (2) represents an addition or a subtraction in a bank reconciliation, and (3) requires an adjusting journal entry.

> 1. The petty cash fund of the Brooks Agency is established at $150. At the end of the current period, the fund contained $28 and had the following receipts: film rentals, $24; refreshments for meetings, $46 (both expenditures to be classified as Entertai

> Answer each of the following related to international accounting standards. a. Explain how the purposes and principles of internal controls are different between accounting systems reporting under IFRS versus U.S. GAAP. b. Cash presents special internal

> An important part of cash management is knowing when, and if, to take purchase discounts. a. Which accounting method uses a Discounts Lost account? b. What is the advantage of this method for management?

> Answer each of the following questions related to international accounting standards. a. Explain how the accounting for items and costs making up merchandise inventory is different between IFRS and U.S. GAAP. b. Can companies reporting under IFRS apply a

> Apple reports the following net sales by product segments. Compute the percentage of total sales for each of its six product segments. Comment on the relative contributions of each product segment. $ millions iPhone iPad Mac iPod iTunes Accessories

> Warton Company posts its sales invoices directly and then binds them into a sales journal. The company had the following credit sales to these customers during July. Required 1. Open an accounts receivable subsidiary ledger having a T-account for each

> In taking a physical inventory at the end of year 2015, Grant Company forgot to count certain units. Explain how this error affects the following: (a) 2015 cost of goods sold, (b) 2015 gross profit, (c) 2015 net income, (d) 2016 net income, (e) the c

> Following is information from Fredrickson Company for its initial month of business. (1) Identify the balances listed in the accounts receivable subsidiary ledger. (2) Identify the accounts receivable balance listed in the general ledger at monthâ

> Refer to the December 31, 2013, financial statements of Samsung in Appendix A. Does Samsung report its accounts receivable as a current or noncurrent asset? Does Samsung report its GOOGLE accounts receivable net of an allowance? Samsungâ€

> How do sellers benefit from allowing their customers to use credit cards?

> Suppose the price of an MP3 player decreases from $60 to $40. Using the midpoint approach, the percentage change in price is _________. Using the initial-value approach, the percentage change in price is _________.

> Compute the new values for the following changes: Initial Value Percentage Change New Value 100 12% 50 8 20 15

> Compute the percentage changes for the following: Initial Value New Value Percentage Change 10 12 100 92 40 45

> Suppose you have $120 to spend on CDs and movies. The price of a CD is $12, and the price of a movie is $6. a. Using Figure 1A.6 on page 51 as a model, prepare a table and draw a curve to show the relationship between the number of CDs (on the horizontal

> The following graph shows the relationship between the number of Frisbees produced and the cost of production. The vertical intercept is $_________, and the slope of the curve is $_________ per Frisbee. Point b shows that the cost of producing _________

> Suppose you belong to a tennis club that has a monthly fee of $100 and a charge of $5 per hour to play tennis. a. Using Figure 1A.4 as a model, prepare a table and draw a curve to show the relationship between the hours of tennis (on the horizontal axis)