Question: Refer to the statements for Google in

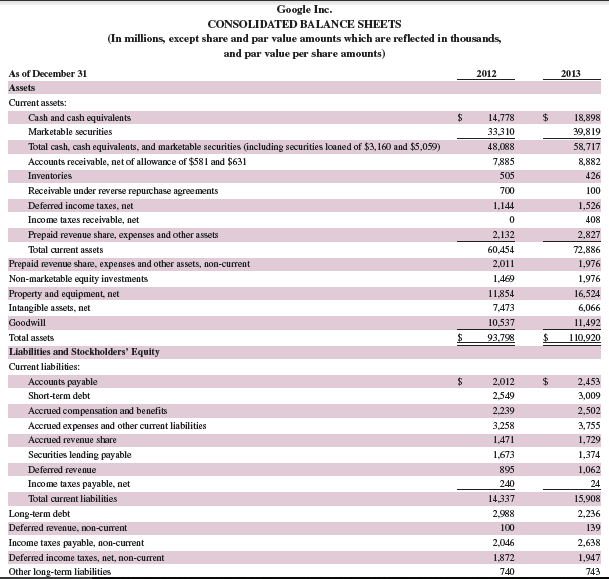

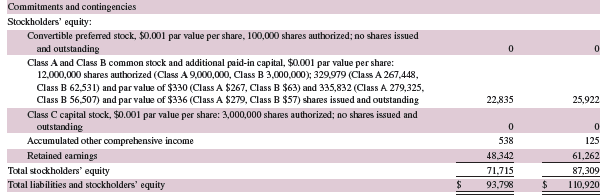

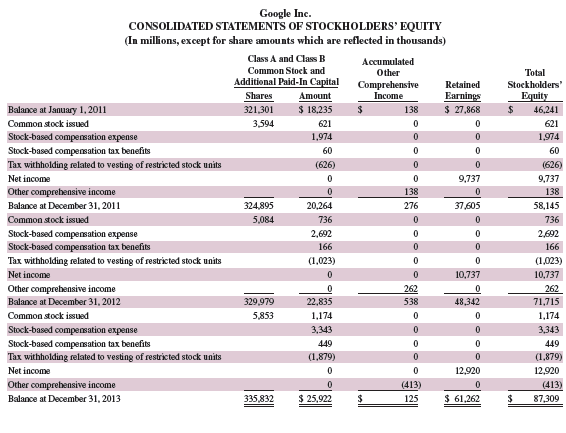

Refer to the statements for Google in Appendix A. For the year ended December 31, 2013, what is its debt-to-equity ratio? What does this ratio tell us?

Google’s Financial Statements from Appendix A:

Transcribed Image Text:

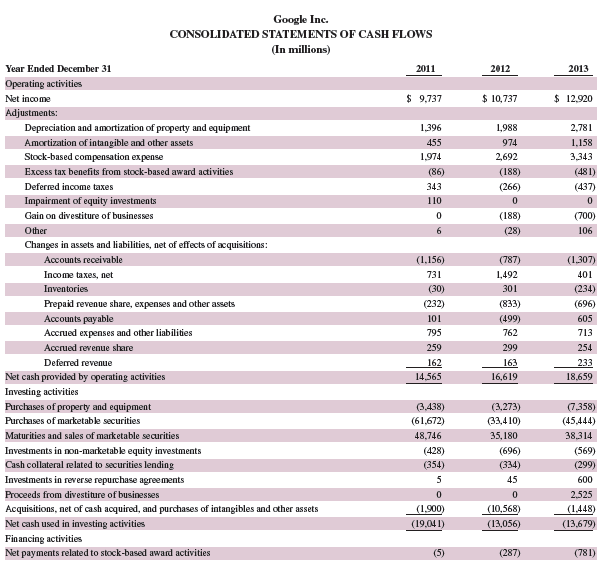

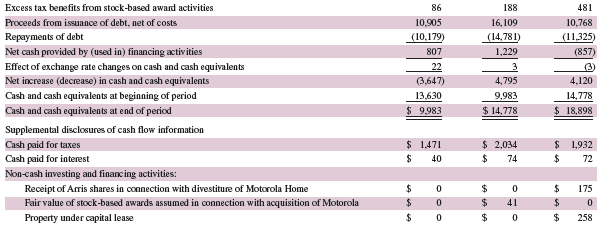

Google Inc. CONSOLIDATED BALANCE SHEETS (In millions, except share and par value amounts which are reflected in thousands, and par value per share amounts) As of December 31 2012 2013 Assets Current assets: Cash and cash equivalents 14,778 18,898 Marketable securities 33,310 39,819 Total cash, cash equivalents, and marketable securities (including securities loaned of $3,160 and $5,059) 48,088 58,717 Accounts receivable, net of allowance of $581 and $631 7,885 8,882 Inventories 505 426 Receivable under reverse repurchase agreements 700 100 Deferred income taxes, net 1,144 1,526 Income taxes receivable, net 408 Prepaid revenue share, expenses and other assets 2,132 2,827 Total current assets 60,454 72,886 Prepaid revenue share, expenses and other assets, non-current 2,011 1,976 Non-marketable equity investments 1,469 1,976 Property and equipment, net 11.854 16,524 Intangible assets, net 7,473 6,066 Goodwill 10,537 11,492 Total assets 93.798 110.920 Liabilities and Stockholders' equity Current liabilities: Accounts payable 2$ 2,012 24 2,453 Short-term debt 2,549 3,009 Accrued compensation and benefits 2.239 2,502 Accrued expenses and other current liabilities 3,258 3,755 Accrued revenue share 1,471 1,729 Securities lending payable 1,673 1,374 Deferred revenue 895 1,062 Income taxes payable, net 240 24 Total current liabilities 14,337 15,908 Long-term debt 2,988 2,236 Deferred revenue, non-current 100 139 Income taxes payable, non-current 2,046 2,638 Deferred income taxes, net, non-current 1,872 1,947 Other long-term liabilities 740 743 Commitments and contingencies Stockholders' equity: Convertible preferred stock, $0.001 par value per share, 100,000 shares authorized; no shares issued and outstanding Class A and Class B common stock and additional paid-in capital, $0.001 par value per share: 12,000,000 shares authorized (Class A 9,000,000, Class B 3,000,000); 329,979 (Class A 267,448, Class B 62,531) and par value of $330 (Class A $267, Class B $63) and 335,832 (Class A 279,325, Class B 56,507) and par value of $336 (Class A $279, Class B $57) shares issued and outstanding Class C capital stock, $0.001 par value per share: 3,000,000 shares authorized; no shares issued and outstanding 22,835 25,922 Accumulated other comprehensive income 538 125 Retained eamings 48,342 61,262 Total stockholders' equity 71,715 87,309 1 10,920 Total liabilities and stockholders' equity 93,798 Google Inc. CONSOLIDATED STATEMENTS OF INCOME (In millions, except per share amounts) Year Ended December 31 2011 2012 2013 Revenues: Google (advertising and other) $37,905 $46,039 $55,519 Motorola Mobile (hardware and other) 4,136 4,306 Total revenues $37,905 $50,175 $59,825 Costs and expenses: Cost of revenues-Google (advertising and other) ( 13,188 17,176 21,993 Cost of revenues–Motorola Mobile (hardware and othery) 3,458 3,865 Research and dewelopment) Sales and marketing General and administrative 5,162 6,793 7,952 4,589 6,143 7,253 2,724 3,845 4,796 Charge related to the resolution of Department of Justice imvestigation 500 37415 Total costs and expenses Income from operations 26,163 45,859 11,742 12,760 13,966 Interest and other income, net 584 626 530 14,496 2,282 Income from continuing operations before income taxes 12,326 13,386 Provision for income taxes 2,589 2,598 Net income from continuing operations $ 9,737 $10,788 $12,214 Net income (loss) from discontinuad operations (51) 706 Net income $ 9,737 $10,737 $12,920 Net income (loss) per share of Class A and Class B common stock-basic: Continuing operations $ 30.17 $ 36.70 $ 32.97 Discontinued operations 0.00 (0.16) 2.12 Net income (loss) per share of Class A and Class B common stock-basic $ 30.17 $ 32.81 $ 38.82 Net income (loss) per share of Class A and Class B common stock-diluted: Continuing operations $ 29.76 $ 32.46 $ 36.05 Discontinued operations 0.00 (0.15) 2.08 Net income (loss) per share of Clas A and Class B common stock-diluted $ 29.76 $ 32.31 $ 38.13 "Includes stock-based compensation expense as follows: Cost of revenues-Google (advertising and other) $ 249 $ 359 2$ 469 Cost of revenues-Motorola Mobile (hardware and other) 14 18 Research and development Sales and marketing 1,061 1,325 1,717 361 498 578 General and administrative 303 453 486 $ 1.974 $ 2,649 $ 3,268 Google Inc. CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (In millions, except for share amounts which are reflected in thousands) Class A and Class B Accumulated Other Comprehensive Income Common Stock and Total Additional Paid-In Capital Retained Stockholders' Earnings $ 27,868 Shares Amount equity Balance at January 1, 2011 321,301 $ 18,235 138 2$ 46,241 Common stock issued 3,594 621 621 Stock-based compensation expense 1,974 1,974 Stock-based compensation tax benefits 60 60 Tax withholding related to vesting of restricted stock units (626) (626) Net income 9,737 9,737 Other comprehensive income 138 138 Balance at December 31, 2011 324,895 20,264 276 37,605 58,145 Common stock issued 5,084 736 736 Stock-based compemation expense Stock-based compensation tax benefits 2,692 2,692 166 166 Tax withholding related to vesting of restricted stock units (1,023) (1,023) Net income 10,737 10,737 Other comprebensive income 262 262 Balance at December 31, 2012 329,979 22,835 538 48,342 71,715 Common stock issued 5,853 1,174 1,174 Stock-based compesation expense 3,343 3,343 Stock-based compensation tax benefits Tax withholding related to vesting of restricted stock units 449 449 (1,879) (1,879) Net income 12,920 12,920 Other comprehensive income Balance at December 31, 2013 (413) 125 (413) 335,832 $ 25,922 $ 61,262 87,309 Google Inc. CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (In millions) Year Ended December 31 2011 2012 2013 Net income $9,737 $10,737 $12,920 Other comprehensive income (loss): Change in foreign currency translation adjustment (107) 75 89 Available-for-sale investments: Change in net unrealized gains 348 493 (392) Less: reclassification adjustment for net gains included in net income Net change (net of tax effect of $54, $68, $212) Cash flow hedges: (115) (216) (162) 233 277 (554) Change in unrealized gains 39 47 112 (60) Less: reclassification adjustment for gains included in net income Net change (net of tax effect of $2, $53, $30) (27) (137) 12 (90) 52 Other comprehensive income (loss) 138 262 (413) Comprebensive income $9,875 $10,999 $12,507 Google Inc. CONSOLIDATED STATEMENTS OF CASH FLOWS (In millions) Year Ended December 31 2011 2012 2013 Operating activities Net income $ 9,737 $ 10,737 $ 12,920 Adjustments: Depreciation and amortization of property and equipment 1,396 1,988 2,781 amortization of intangible and other assets 455 974 1,158 Stock-based compensation expense 1,974 2,692 3343 Excess tax benefits from stock-based award activities (86) (188) (481) Deferred income taxes 343 (266) (437) Impairment of equity investments 110 Gain on divestiture of businesses (188) (700) Other 6 (28) 106 Changes in assets and liabilities, net of effects of acquisitions: Accounts receivable (1,156) (787) (1,307) Income taxes, net 731 1,492 401 Inventories (30) 301 (234) Prepaid revenue share, expenses and other assets (232) (833) (696) Accounts payable 101 (499) 605 Accrued expenses and other liabilities 795 762 713 Accrued revenue share 259 299 254 Deferred revenue 162 163 233 18,659 Net cash provided by operating activities 14,565 16,619 Investing activities Purchases of property and equipment (3,438) (3,273) (7,358) Purchases of marketable securities (61,672) (33,4 10) (45,444) Maturities and sales of marketable securities 48,746 35,180 38,314 (428) Investments in non-marketable equity investments Cash collateral related to securities lending (696) (569) (354) (334) (299) Investments in reerse repurchase agreements 45 600 Proceeds from divestiture of businesses 2,525 Acquisitions, net of cash acquired, and purchases of intangibles and other assets (1,900) (10,568) (1,448) Net cash used in investing activities (19,04 1) (13,056) (13,679) Financing activities Net payments related to stock-based award activities (5) (287) (781) Excess tax benefits from stock-based award activities 86 188 481 Proceeds from issuance of debt, net of costs 10.905 16,109 10,768 Repayments of debt (10,179) (14,781) (11,325) Net cash provided by (used in) financing activities 807 1,229 (857) Effect of exchange rate changes on cash and cash equivalents 22 (3) Net increase (decrease) in cash and cash equivalents (3,647) 4,795 4,120 Cash and cash equivalents at beginning of period 13,630 9,983 14,778 Cash and cash equivalents at end of period $ 9,983 $ 14,778 $ 18,898 Supplemental disclosures of cash flow information Cash paid for taxes $ 1,471 $ 2,034 1,932 Cash paid for interest 40 24 74 %24 72 Non-cash investing and financing activities: Receipt of Arris shares in connection with divestiture of Motorola Home 175 Fair value of stock-based awards assumed in connection with acquisition of Motorola $ 24 41 Property under capital lease 258

> Describe the two basic types of pension plans.

> Compare and contrast an operating lease with a capital lease.

> What obligation does an entrepreneur (owner) have to investors that purchase bonds to finance the business?

> Describe the debt-to-equity ratio and explain how creditors and owners would use this ratio to evaluate a company’s risk.

> What is the difference between the market value per share and the par value per share?

> List the general rights of common stockholders.

> How is book value per share computed for a corporation with no preferred stock? What is the main limitation of using book value per share to value a corporation?

> What is the difference between a stock dividend and a stock split?

> Why are incidental costs sometimes ignored in inventory costing? Under what accounting constraint is this permitted?

> How does declaring a stock dividend affect the corporation’s assets, liabilities, and total equity? What are the effects of the eventual distribution of that stock?

> Identify and explain the importance of the three dates relevant to corporate dividends.

> Enter the letter of the description A through H that best fits each term or phrase 1 through 8. A. Records and tracks the bondholders’ names. B. Is unsecured; backed only by the issuer’s credit standing. C. Has varying maturity dates for amounts owed. D.

> On January 1, 2015, the $2,000,000 par value bonds of Spitz Company with a carrying value of $2,000,000 are converted to 1,000,000 shares of $1.00 par value common stock. Record the entry for the conversion of the bonds.

> Identify the following as either an advantage (A) or a disadvantage (D) of bond financing. ______ a. Bonds do not affect owner control. ______ b. A company earns a lower return with borrowed funds than it pays in interest. ______ c. A company earns a hig

> Which of the following statements are true regarding dividends? ______ 1. Cash and stock dividends reduce retained earnings. ______ 2. Dividends payable is recorded at the time a cash dividend is declared. ______ 3. The date of record refers to the date

> Costs of $5,000 were incurred to acquire goods and make them ready for sale. The goods were shipped to the buyer (FOB shipping point) for a cost of $200. Additional necessary costs of $400 were incurred to acquire the goods. What is the buyer’s total cos

> Identify the inventory costing method best described by each of the following separate statements. Assume a period of increasing costs. ______ 1. Yields a balance sheet inventory amount often markedly less than its replacement cost. ______ 2. Results in

> Answer each of the following questions related to international accounting standards. a. Explain how the accounting for merchandise purchases and sales is different between accounting under IFRS versus U.S. GAAP. b. Income statements prepared under IFRS

> After all partnership assets have been converted to cash and all liabilities paid, the remaining cash should equal the sum of the balances of the partners’ capital accounts. Why?

> Listed below are various transactions that a company incurred during the current year. Indicate the impact on total stockholders’ equity for each scenario. Specifically state whether stockholders’ equity would “Increase,” “Decrease,” or have “No Effect”

> Of the following statements, which are true for the corporate form of organization? ______ 1. Ownership rights cannot be easily transferred. ______ 2. Owners have unlimited liability for corporate debts. ______ 3. Capital is more easily accumulated than

> Identify whether each description best applies to a periodic or a perpetual inventory system. ______ a. Updates the inventory account only at period-end. ______ b. Requires an adjusting entry to record inventory shrinkage. ______ c. Markedly increased in

> Answer each of the following related to international accounting standards. a. In general, how similar or different are the definitions and characteristics of current liabilities between IFRS and U.S. GAAP? b. Companies reporting under IFRS often referen

> Fancher organized a limited partnership and is the only general partner. Carley invested $20,000 in the partnership and was admitted as a limited partner with the understanding that she would receive 10% of the profits. After two unprofitable years, the

> The following legal claims exist for Huprey Co. Identify the accounting treatment for each claim as either (a) a liability that is recorded or (b) an item described in notes to its financial statements. 1. Huprey (defendant) estimates that a pending law

> Which of the following items are normally classified as current liabilities for a company that has a 15-month operating cycle? ______ 1. Portion of long-term note due in 15 months. ______ 2. Note payable maturing in 2 years. ______ 3. Note payable due

> For each item below indicate whether the statement describes a multiple-step income statement or a single-step income statement. a. Multiple-step income statement b. Single-step income statement 1. Shows detailed computations of net sales and other cost

> Enter the letter for each term in the blank space beside the definition that it most closely matches. A. Sales discount B. Credit period C. Discount period D. FOB destination E. FOB shipping point F. Gross profit I. Cash discount G. Merchandise inven

> On June 3, a company borrows $200,000 cash by giving its bank a 90-day, interest-bearing note. On the statement of cash flows, where should this be reported?

> If a partnership contract does not state the period of time the partnership is to exist, when does the partnership end?

> Refer to Samsung’s 2013 statement of cash flows in Appendix A. List its cash flows from operating activities, investing activities, and financing activities. Samsung’s Statement of Cash Flow from Appendix A: Sams

> Under what circumstances are long-term investments in debt securities reported at cost and adjusted for amortization of any difference between cost and maturity value?

> On a balance sheet, what valuation must be reported for debt securities classified as available-for-sale?

> If a company purchases its only long-term investments in available-for-sale debt securities this period and their fair value is below cost at the balance sheet date, what entry is required to recognize this unrealized loss?

> If a short-term investment in available-for-sale securities costs $10,000 and is sold for $12,000, how should the difference between these two amounts be recorded?

> On a balance sheet, what valuation must be reported for short-term investments in trading securities?

> Refer to the income statement of Samsung in Appendix A. How can you tell that it uses the consolidated method of accounting? Income Statement of Samsung from Appendix A: Samsung Electronics Co, Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF

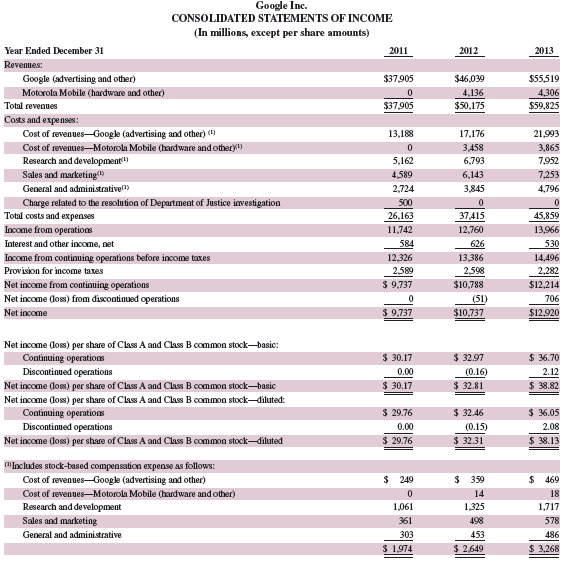

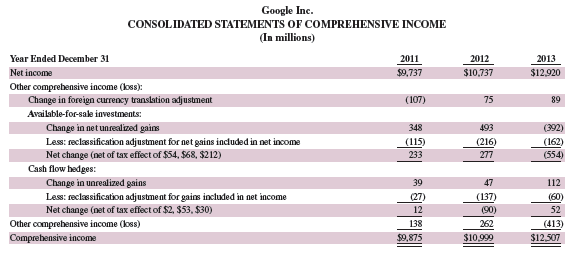

> Refer to Google’s statement of comprehensive income. What was the amount of its 2013 change in net unrealized gains for its AFS investments? Google’s Statement of Comprehensive Income: Google Inc. CONSOLIDATED ST

> Refer to Apple’s statement of comprehensive income in Appendix A. What is the amount of foreign currency translation adjustment for the year ended September 28, 2013? Is this adjustment an unrealized gain or an unrealized loss? Apple&a

> If a U.S. company makes a credit sale to a foreign customer required to make payment in U.S. dollars, can the U.S. company have an exchange gain or loss on this sale?

> What is an employer’s unemployment merit rating? How are these ratings assigned to employers?

> What are two major challenges in accounting for international operations?

> Under what circumstances does a company prepare consolidated financial statements?

> In accounting for investments in equity securities, when should the equity method be used?

> Under what two conditions should investments be classified as current assets?

> What factors affect the market rates for bonds?

> What are the duties of a trustee for bondholders?

> What is the main difference between a bond and a share of stock?

> When can a lease create both an asset and a liability for the lessee?

> Refer to the statement of cash flows for Samsung in Appendix A. For the year ended December 31, 2013, what was the amount for repayment of long-term borrowings and debentures? Samsung’s Statement of Cash Flow from Appendix A: Sams

> Refer to Samsung’s recent balance sheet in Appendix A. What current liabilities related to income taxes are on its balance sheet? Explain the meaning of each income tax account identified. Samsung’s Balance Sheet from Appendix A: / /

> By what amount did Samsung’s long-term borrowings increase or decrease in 2013? Samsung’s Financial Statements from Appendix A: Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF FI

> Refer to Apple’s annual report in Appendix A. Is there any indication that Apple has issued long-term debt? Apple’s Balance Sheet from Appendix A: Apple Inc. CONSOLIDATED BALANCE SHEETS (In millions, except numbe

> What is the issue price of a $2,000 bond sold at 98 1⁄4? What is the issue price of a $6,000 bond sold at 101 1⁄2?

> If you know the par value of bonds, the contract rate, and the market rate, how do you compute the bonds’ price?

> What is the main difference between notes payable and bonds payable?

> Why would an investor find convertible preferred stock attractive?

> What is the difference between the par value and the call price of a share of preferred stock?

> What is the preemptive right of common stockholders?

> What is the difference between authorized shares and outstanding shares?

> Who is responsible for directing a corporation’s affairs?

> Suppose that a company has a facility located where disastrous weather conditions often occur. Should it report a probable loss from a future disaster as a liability on its balance sheet? Explain.

> Refer to the financial statements for Samsung in Appendix A. How much were its cash payments for treasury stock purchases for the year ended December 31, 2013? Samsung’s Financial Statements from Appendix A: Samsung Electronic

> Refer to the 2013 balance sheet for Google in Appendix A. What is the par value per share of its preferred stock? Suggest a rationale for the amount of par value it assigned. Google’s Balance Sheet from Appendix A: Google Inc. CON

> Refer to Apple’s fiscal 2013 balance sheet in Appendix A. How many shares of common stock are authorized? How many shares of voting common stock are issued? Apple’s Balance Sheet from Appendix A:

> How are organization expenses reported?

> What is a stock option?

> How are EPS results computed for a corporation with a simple capital structure?

> Why do laws place limits on treasury stock purchases?

> How does the purchase of treasury stock affect the purchaser’s assets and total equity?

> Courts have ruled that a stock dividend is not taxable income to stockholders. What justifies this decision?

> Why is the term liquidating dividend used to describe cash dividends debited against paid-in capital accounts?

> Why are warranty liabilities usually recognized on the balance sheet as liabilities even when they are uncertain?

> What are organization expenses? Provide examples.

> George, Burton, and Dillman have been partners for three years. The partnership is being dissolved. George is leaving the firm, but Burton and Dillman plan to carry on the business. In the final settlement, George places a $75,000 salary claim against th

> What does the term unlimited liability mean when it is applied to partnership members?

> Allocation of partnership income among the partners appears on what financial statement?

> Assume that the Barnes and Ardmore partnership agreement provides for a two-third/one-third sharing of income but says nothing about losses. The first year of partnership operation resulted in a loss, and Barnes argues that the loss should be shared equa

> Assume that Amey and Lacey are partners. Lacey dies, and her son claims the right to take his mother’s place in the partnership. Does he have this right? Why or why not?

> Can partners limit the right of a partner to commit their partnership to contracts? Would such an agreement be binding (a) on the partners and (b) on outsiders?

> How does a general partnership differ from a limited partnership?

> Apple began as a partnership. What does the term mutual agency mean when applied to a partnership?

> Assume a partner withdraws from a partnership and receives assets of greater value than the book value of his equity. Should the remaining partners share the resulting reduction in their equities in the ratio of their relative capital balances or accordi

> Identify the main difference between (a) plant assets and current assets, (b) plant assets and inventory, and (c) plant assets and long-term investments.

> Kay, Kat, and Kim are partners. In a liquidation, Kay’s share of partnership losses exceeds her capital account balance. Moreover, she is unable to meet the deficit from her personal assets, and her partners shared the excess losses. Does this relieve Ka

> What determines the amount deducted from an employee’s wages for federal income taxes?

> Which payroll taxes are the employee’s responsibility and which are the employer’s responsibility?

> What is the current Medicare tax rate? This rate is applied to what maximum level of salary and wages?

> What is the combined amount (in percent) of the employee and employer Social Security tax rate? (Assume wages do not exceed $200,000 per year.)

> If $988 is the total of a sale that includes its sales tax of 4%, what is the selling price of the item only?

> What are the three important questions concerning the uncertainty of liabilities?

> What is an estimated liability?

> Refer to Samsung’s balance sheet in Appendix A. List Samsung’s current liabilities as of December 31, 2013. Samsung’s Balance Sheet from Appendix A: / /

> Refer to Google’s balance sheet in Appendix A. What accrued expenses (liabilities) does Google report at December 31, 2013? Google’s Balance Sheet from Appendix A: Google Inc. CONSOLIDATED BALANCE SHEETS (In mill

> What is the difference between ordinary repairs and extraordinary repairs? How should each be recorded?

> Why does the direct write-off method of accounting for bad debts usually fail to match revenues and expenses?

> Refer to Apple’s balance sheet in Appendix A. What is the amount of Apple’s accounts payable as of September 28, 2013? Apple’s Balance Sheet from Appendix A: Apple Inc. CONSOLIDATED BALANCE SHEE

> What amount of income tax is withheld from the salary of an employee who is single with two withholding allowances and earning $725 per week? What if the employee earned $625 and has no withholding allowances? (Use Exhibit 11A.6.) Exhibit 11A.6: SI

> What is a wage bracket withholding table?

> What is the difference between a current and a long-term liability?