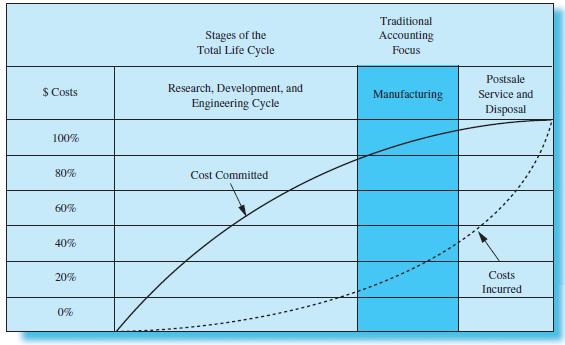

Question: Review Exhibit 8-2, showing the relationship

Review Exhibit 8-2, showing the relationship between committed costs and incurred costs over the total life cycle of a product. Explain what the diagram means and what the implications are for managing costs.

Exhibit 8-2

Transcribed Image Text:

Traditional Stages of the Total Life Cycle Accounting Focus Postsale Research, Development, and Engineering Cycle $ Costs Manufacturing Service and Disposal 100% 80% Cost Committed 60% 40% Costs Incurred 20%

> How would you reward a group of people that includes product designers, engineers, production personnel, purchasing agents, marketing staff, and accountants whose job is to identify and develop a new car? How would you reward a person whose job is to dis

> When should an organization use stock options?

> When should an organization use gain sharing?

> Why do a company’s operators/workers, managers, and executives have different informational needs than shareholders and external suppliers of capital?

> What does the controllability principle require?

> When should an organization use a cash bonus?

> You work for a consulting firm and have been given the assignment of deciding whether a particular company president is overpaid both in absolute terms and relative to presidents of comparable companies. How would you undertake this task?

> Explain when one would reward outcomes or outputs, reward inputs, or use knowledge-based pay.

> Do you believe that people value intrinsic rewards? Give an example of an intrinsic reward that you would value and explain why. Why are extrinsic rewards important to people? If you value only extrinsic rewards, explain why.

> What are budgeting games, and why do employees engage in them?

> What are the pros and cons of building slack into the budget from (1) The point of view of the employee building in slack and (2) From a senior manager’s point of view?

> How does participation in the budgeting process differ from consultation?

> What are the advantages for the individual in being able to participate in decision making in the organization, and what are the advantages for the organization in allowing the individual to participate in decision making?

> Can you think of instances when gaming behavior is appropriate in an organization?

> List some methods of gaming performance indicators.

> What is management accounting?

> In December 2002, Time magazine named Cynthia Cooper, Coleen Rowley, and Sherron Watkins as its Persons of the Year. Cynthia Cooper was vice president of internal audit for WorldCom and informed the firm’s audit committee that the firm had improperly tre

> Chow Company is an insurance company in Hong Kong. Chow hires 55 people to process insurance claims. The volume of claims is extremely high, and all claims examiners are kept extremely busy. The number of claims in which errors are made runs about 10%. I

> Frits Seegers, President of Citibank California, was meeting with his management team to review the performance evaluation and bonus decisions for the California branch managers. James McGaran’s performance evaluation was next. Frits felt uneasy about th

> What is a quality function deployment matrix, and how does it relate to value index computations for target costing?

> What is target costing?

> What three substages typically occur in the postsale service and disposal stage of total life- cycle costing?

> What are the three substages of the RD&E stage of total-life-cycle costing?

> What is the difference between committed costs and incurred costs?

> What are the three major stages of the total life- cycle costing approach in a manufacturing situation?

> What is the total-life-cycle costing approach? Why is it important?

> What activities are included in environmental costing?

> What are some examples of explicit and implicit environmental costs?

> What are some nonfinancial measures that a company might use in order to motivate achieving the objective of reducing product development cycle time across an array of products?

> What are some nonfinancial measures that a company might use in order to motivate achieving the objective of anticipating future customer needs?

> Explain why using percentage of revenues from new products as a performance metric may fail to stimulate the creation of highly innovative products.

> What desirable behavioral consequences are likely as people focus on improving the BET metric?

> What three critical elements does the BET metric bring together?

> What roles do cross-functional teams and supply chain management play in target costing?

> What is value engineering?

> Pierre LeBlanc, manager of Centaur Corporation, is thinking about implementing a target costing system in his organization. Several managers have taken him aside and have expressed concerns about implementing target costing in their organization. Requir

> Stacy Yoo, president of Caremore, Inc., an appliance manufacturer in Seattle, Washington, has been trying to decide whether one of her product-line managers, Bill Mann, has been achieving the companywide return-on-sales target of 45%. Stacy has just rece

> Briefly explain each of the four steps of the plan–do–check–act cycle.

> Calcutron Company is contemplating introducing a new type of calculator to complement its existing line of scientific calculators. The target price of the calculator is $75; annual sales volume of the new calculator is expected to be 500,000 units. Calcu

> Gregoire Grant is a traditional manufacturing manager who is concerned only with managing costs over the manufacturing cycle of the product. He argues that since traditional accounting methods are focused on this cycle, he should not bother with the RD&E

> Consider the following situation: Your manager comes to you and says, “I don’t understand why everyone is talking about the total-life-cycle costing approach to product costing. As far as I am concerned, this new approach is a waste of time and energy. I

> Amajor car manufacturer developed the following information as part of its target costing efforts: Required (a) Prepare an exhibit similar to Exhibit 8-9 showing percentage contributions of each function group to categories of customer requirements. (b

> Imagine that you are the manager of a large bank. Having heard about a management accounting method called target costing, you are wondering whether it can be applied to the banking industry. In particular, you are trying to determine how to benchmark ot

> According to this chapter, the target costing and traditional cost reduction methods approach the relationships among cost, selling price, and profit margin quite differently. Required Write an essay that illustrates how the target costing and tradition

> As a manager interested in implementing target costing, you are contemplating three approaches. The first is to bring in an outside consultant; the second is to develop your own system inside your organization with little to no outside assistance; and th

> Traditional cost reduction in the United States differs significantly from the Japanese method of target costing. Required Discuss the similarities and differences in the process by which cost reduction under both systems occurs. Be specific in your ans

> What is the profitability measure most widely used to develop the target profit margin under target costing?

> When does the disposal phase of the postsale service and disposal stage of a product begin and end?

> Given a selected strategy, how do organizations use management accounting information to implement the strategy?

> What is the traditional accounting focus in managing costs over the total life cycle of a product? What is the problem with this focus?

> Explain the benefits of using a total-lifecycle costing approach to product costing.

> Explain how the total-life-cycle costing approach differs from traditional product costing.

> How can a firm use activity-based costing to help control and reduce environmental costs?

> Refer to Exhibit 8-14 regarding Greyson Technology’s launch of a new digital communications device. Suppose that Greyson reduced the quarterly spending on product development in panel A, which delayed launching the new product for two q

> Refer to Exhibit 8-14 regarding Greyson Technology’s launch of a new digital communications device. Suppose that Greyson reduced the quarterly spending on product development in panel A, which delayed launching the new product for two q

> Refer to the Kitchenhelp Coffeemaker example in the chapter. Suppose that Exhibits 8-6 and 8-7 remain the same but that engineers developed different numerical correlations, shown below, for the QFD matrix in Exhibit 8-8. Required (a) Prepare an exhibit

> Express the target costing relationship in equation form. How does this equation differ from the two other types of traditional equations relating to cost reduction? Why is this significant?

> As a manager asked to benchmark another organization’s target costing system, on what factors would you gather information? Why?

> Provide examples of how management accounting systems have changed in response to information needs as companies have become more complex, technologies have changed, or new competitors have appeared.

> From a behavioral point of view, what potential problems can occur when implementing a target costing system?

> What is the relationship between value engineering and target costing?

> Explain how target costing differs from traditional cost reduction methods.

> Refer to Case 7-57, which describes Kwik Clean’s environmental costs. Required (a) Of the costs listed by Pat Polley, identify which are explicit and which are implicit environmental costs. (b) Should Polley identify any other environmental costs? (c) P

> Bevans Co. makes two products, Product X and Product Y. Bevans has produced Product X for many years without generating any hazardous wastes. Recently, Bevans developed Product Y, which is superior to Product X in many respects. However, production of Pr

> During the recession beginning in the early 1990s, Mercedes-Benz (MB) struggled with product development, cost efficiency, material purchasing, and problems in adapting to changing markets. In 1993, these problems caused the worst sales slump in decades,

> List two types of costs incurred when implementing a group technology layout.

> Why are production cycle time and the level of work-in-process inventory positively related?

> Waste, rework, and net cost of scrap are examples of what kinds of quality costs?

> What is meant by the phrase cost of nonconformance in relation to quality?

> Why might senior executives need measures besides financial ones to assess how well their business performed in the most recent period?

> What is the additional cost if a unit rejected at inspection can be reworked to meet quality standards by performing some additional operations?

> What is a benchmarking (performance) gap?

> What are the three types of information gathering and sharing used under the cooperative form of benchmarking?

> What stage of the benchmarking process is the most important for benchmarking management accounting methods? Why?

> What are the five stages of the benchmarking process?

> Why is it said that a kaizen costing system operates “outside the standard costing system”?

> When is a cost variance investigation undertaken under kaizen costing?

> What is kaizen costing?

> What is benchmarking, and why is it used?

> What are two types of financial benefits resulting from a shift to group technology, just-in-time production, or continuous quality improvements?

> Why may financial information alone be insufficient for the ongoing informational needs of operators/workers, managers, and executives?

> What creates the need to maintain work-in process inventory? Why is work-in-process inventory likely to decrease on the implementation of group technology, just-in-time production, and quality improvement programs?

> How is a just-in-time manufacturing system different from a conventional manufacturing system?

> List three examples for each of the following quality costing categories: a. Prevention costs b. Appraisal costs c. Internal failure costs d. External failure costs.

> Quality engineering, quality training, statistical process control, and supplier certification are what kinds of quality costs?

> Describe the lean manufacturing approach.

> What is group technology?

> What is the difference between process and product layout systems?

> The theory of constraints relies on three measures: throughput contribution, investments, and operating costs. Define these three measures in the context of the theory of constraints.

> What costs and revenues are relevant in evaluating the profit impact of an increase in sales?

> What is the additional cost of replacing one unit of a product rejected at inspection and scrapped?

> What does the breakeven time (BET) metric for the product development process measure?

> What are the two general methods of information gathering and sharing when undertaking a benchmarking exercise?

> What are the three broad classes of information on which firms interested in benchmarking can focus? Describe each.

> According to the kaizen costing approach, who has the best knowledge to reduce costs? Why is this so?

> Under what condition will the cost savings due to kaizen costing not be applied to production?

> What do the terms kaizen and kaizen costing mean?

> One aspect of facilities layout for McDonald’s is that when customers come into the building, they can line up in one of several lines and wait to be served. In contrast, customers at Wendy’s are asked to stand in one line that snakes around the front of

> Ray Brown’s company, Whisper Voice Systems, is trying to increase its processing cycle efficiency (PCE). Because Ray has a very limited budget, he has been searching for a way to increase his PCE by using group technology. One of Ray&ac

> Gurland Valves Company manufactures brass valves that meet precise specification standards. All finished valves are inspected before being packaged and shipped to customers. Rejected valves are returned to the initial production stage to be melted and re