Question: The Kraft Heinz Co. case was discussed

The Kraft Heinz Co. case was discussed in the chapter. To refresh your memory, on May 6, 2019, Kraft Heinz disclosed that it would restate its financial statements due to faulty procurement practices. The financial statements for 2016, 2017, and the first three quarters of 2018 were misstated because of inappropriate timing of the recognition of when certain cost and rebate elements associated with supplier contracts were initially recorded and then recognized through corresponding decreases to costs of products sold in future financial periods. The Form 8-K Report was filed with the SEC on May 2, 2019 pursuant to Items 2.02 and 4.02 of the Securities Exchange Act of 1934. The information in Exhibit 1 is taken from the Report.

Due to the findings above, the company said it would not be able to timely file its quarterly report for the period ended March 30, 2018.

Exhibit 1 Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or Completed Interim Review

On May 2, 2019, the Company, in consultation with the Audit Committee of its Board of Directors reached a determination that the Company’s consolidated financial statements and related disclosures for the years ended December 30, 2017, and December 31, 2016, included in its Annual Reports on Form 10-K, and for each of the quarterly and year-to-date periods in 2017 and the quarterly and year-to-date periods for the nine months ended September 29, 2018, should no longer be relied upon because of certain misstatements contained in those financial statements.

The Company does not believe that such misstatements constitute a quantitatively material misstatement to any individual period presented in the Company’s prior annual or interim financial statements, but due to the qualitative nature of the matters identified in the investigation, including the number of years over which the misconduct occurred and the number of transactions, suppliers, and procurement employees involved, the Company has determined that it is appropriate to correct the misstatements in the Company’s previously issued financial statements through restating such financial statements.

As previously disclosed in the Company’s press release as furnished with its Current Report on Form 8-K filed on February 21, 2019 (the "Earnings Release"), the Company received a subpoena in October 2018 from the SEC related to the Company’s procurement area, more specifically the Company’s accounting policies, procedures, and internal controls related to its procurement function, including, but not limited to, agreements, side agreements, and changes or modifications to its agreements with its suppliers. Following receipt of this subpoena, the Company, together with external counsel and forensic accountants, and under the oversight of the Audit Committee, initiated an investigation into the procurement area, which is now substantially complete.

As a result of the findings from the Company's investigation, which identified that several employees in the procurement area engaged in misconduct, the Company has recorded adjustments to correct prior period misstatements that increase the total cost of products sold in prior financial periods, which the Company does not believe constitute a quantitatively material misstatement to any individual period. These misstatements principally relate to the incorrect timing of when certain cost and rebate elements associated with complex supplier contracts and arrangements were initially recognized, and once corrected for, the Company expects to recognize corresponding decreases to costs of products sold in future financial periods.

The findings from the investigation did not identify any misconduct by any member of the senior management team. Additionally, the Company has implemented and continues to implement certain remedial actions, including employee personnel actions and certain improvements to its internal controls, to mitigate the likelihood of this occurring in the future. The Company also continues to cooperate fully with the SEC.

In connection with the internal investigation described above, the Company also conducted a comprehensive review of significant supplier contracts to identify other potential misstatements in the timing of the recognition of supplier rebates, incentive payments, and pricing arrangements. The review identified additional misstatements, which may or may not have resulted from the misconduct noted above, primarily related to certain supplier contracts and arrangements where the allocation of value of all or a portion of rebates and up-front payments to contractual elements in the current period should have been deferred and recognized over an applicable contractual period.

These misstatements will be corrected for in the same manner as those noted above. The Company corrected these misstatements to defer the up-front consideration from suppliers when the retention or receipt of that consideration was contingent upon future events and to correctly recognize the consideration as a reduction of cost of products sold over the terms of the arrangements with the suppliers. The misstatements arising from the contract review relate to the timing of recognizing certain cost and rebate elements, and the Company thus expects to recognize corresponding decreases to costs of products sold in future financial periods.

The Company's investigation and review described above identified required adjustments of approximately $208 million, of which approximately $27 million was recorded in the previously furnished fourth quarter 2018 cost of products sold. As a result, the cumulative net misstatements to the previously furnished or reported annual and interim financial statements were approximately $181 million, which, when reflected over the relevant periods, resulted in misstatements that are not quantitatively material to any prior year or quarter, but would have been significant to the fourth quarter of 2018 if corrected in that period. The impact of these corrections to previously reported financial statements is an increase to cost of products sold of approximately $25 million in 2015, $26 million in 2016 and $100 million in 2017. The impact to the previously furnished financial statements in 2018 is an increase in cost of products sold of approximately $30 million. These misstatements were also not quantitatively material to any quarter, with the largest correction being a $38 million increase to cost of products sold in the third quarter of 2017.

In addition, the Company evaluated other elements of these complex supplier contracts and arrangements, including the classification of leases embedded in supplier arrangements as capital or operating. As a result of the review, the Company identified certain arrangements that were improperly classified as embedded capital leases. The correction of this error did not impact previously reported 2017 net income and resulted in a decrease to previously furnished 2018 net loss of approximately $2 million. The correction reduced previously reported 2017 Adjusted EBITDA by approximately $2 million and previously furnished 2018 Adjusted EBITDA by approximately $33 million. The Company will also correct for these misstatements in connection with the restatement.

The effect of the restatements in prior periods on both Adjusted EBITDA and Adjusted EPS is expected to be less than two percent in each year and less than four percent in each quarter. The misstatements also had less than one percent impact on total assets or total liabilities at December 30, 2017.

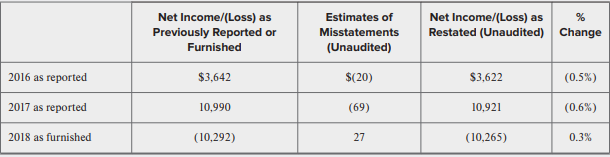

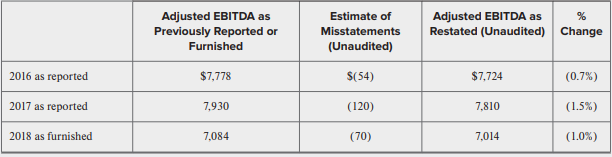

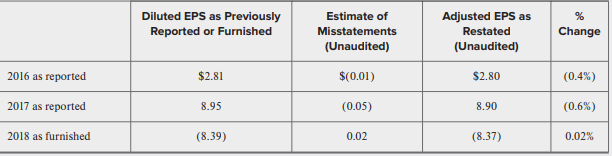

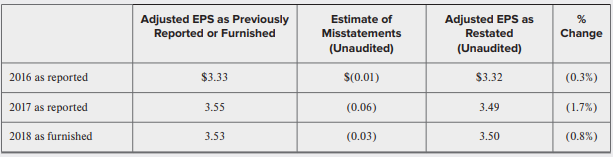

Exhibit 2 shows the preliminary estimated impact of misstatements for supplier rebates, capital leases, impairments and other misstatements described in Exhibit 1. The tables illustrate the impact to net income/(loss), Adjusted EBITDA, diluted earnings per share ("diluted EPS") and Adjusted EPS for 2016 and 2017 as compared to the previously reported financial statements as well as the impact of these metrics for 2018 as compared to the previously furnished financial statements in the Earnings Release issued on February 21, 2019. These misstatements and illustrated restated numbers are preliminary, unaudited, and subject to further change in connection with the completion of the Company's Annual Report on Form 10-K for the fiscal year ended December 29, 2018.

SEC Issues Two Subpoenas

In February 2019, buried in a press release announcing its 2018 Quarter 4 results, the company stated that it had received a subpoena from the SEC associated with an investigation into the company’s procurement area. It said the SEC was investigating its “accounting policies, procedures, and internal controls related to its procurement function, including, but not limited to, agreements, side agreements, and changes or modifications to its agreements with its vendors.†At that time Kraft Heinz said it was recording a $25 million increase to costs of products sold as an out of period correction as the Company determined the amounts were immaterial to the fourth quarter of 2018.

In the most recent SEC filing, the company also said it has received a second subpoena associated with its assessment of goodwill and intangible asset impairments, and that this subpoena also included document requests related to the procurement area.

“The Company is taking action to improve our policies and procedures and will continue to strengthen our internal financial controls,†said Michael Mullen senior vice president of corporate affairs at Kraft Heinz. “The findings from the investigation did not identify any misconduct by any member of the senior management team. We are pleased to report that the investigation is now substantially complete.â€

Questions.

1. Given the discussion in the chapter about reporting restatements of the financial statements to the SEC, explain why Kraft did not follow all the rules in reporting the numbers in Exhibit 2.

2. Comment on how the company addressed operational issues in its Form 8-K. What role did they play in deciding to restate the financial statements?

3. Are there any conclusions you can draw about the cause of misstatements at Kraft Heinz during the affected periods with respect to ethical leadership? Explain.

> Do you think the "Resolution of Ethical Issues" section in The IMA Statement of Ethical Professional Practice is a helpful part of its ethical standards?

> Why do you think good people sometimes do bad things? Explain.

> MacIntyre, in his account of Aristotelian virtue, states that integrity is the one trait of character that encompasses all the others. How does this relate to the Principles in the AICPA Code of Professional Conduct?

> Explain the components of Burchard’s Ethical Dissonance Model and how it describes the ethical person-organization fit at various stages of the contractual relationship in each potential fit scenario. Assume a Low Organizational Ethics, High Individual E

> What does the term "civility" mean to you? Do you think it is civil behavior to shout down a speaker with whom you do not agree? What about cancelling someone because you don't agree with their message?

> Answer the following with regard to egoism. (a) Do you think it is the same to act in your own self-interest as it is to act in a selfish way? (b) Do you think “enlightened self-interest” is a contradiction in terms, or is it a valid basis for all action

> David Starr Jordan (1851–1931), an educator and writer, said, “Wisdom is knowing what to do next; virtue is doing it.” Explain the meaning of this phrase as you see it.

> What is the comparative negligence defense? When can it shield auditors from legal liability for their actions?

> Tinseltown Construction just received a $2.6 billion contract to construct a modern football stadiumfor the L.A. Rams and San Diego Chargers at the L.A. Sports and Entertainment District. The company estimates that it will cost $1.8 billion to construct

> Describe the possible entities that may sue an auditor and the possible reasons for a lawsuit.

> Is there a difference between an error in financial statements, fraud, and negligence from a reasonable care perspective? Give examples of each of your response. How would these events affect accountants’ legal liability?

> During a particularly stimulating lecture by your accounting ethics professor on accountants’ legal liabilities, the following question was posed: Assume you are a CPA and have just been sued by a third-party for your failure to conduct a proper audit. W

> Under what circumstances might an auditor be held legally liable for negligent representation versus a fraudulent misrepresentation based on court rulings discussed in the chapter? Include in your discussion the tests for reliance on misrepresentations.

> Explain how the intent requirement of the legal principle of scienter relates to ethical standards of behavior discussed in previous chapters.

> Distinguish between the legal standards of gross negligence and fraud.

> How does auditors’ meeting public interest obligations relate to avoiding legal liability?

> How has the Sarbanes-Oxley Act affected the legal liability of accountants and auditors?

> Do you believe the standard for liability under the PSLRA better protects auditors from legal liability than the standards which existed before the Act was adopted by Congress? Explain.

> Danny Boy, a local CPA who owns a tax practice, is being investigated by the IRS for the preparation of false income tax returns for a client. The IRS alleges that the individual taxpayer/client used a substantial amount of his company’s funds for person

> Revenue recognition in the Xerox case called for determining the stand-alone selling price for each of the deliverables and using it to separate out the revenue amounts. Why do you think it is important to separate out the selling prices of each element

> What must a plaintiff assert in a Section 11 claim under the Securities Act of 1933 to properly allege an “opinion” statement is materially misleading? When might certain financial statement items constitute “opinions”?

> Distinguish between the legal standards of negligence and recklessness.

> Rule 10b-5 is a regulation created under the Securities and Exchange Act of 1934 that targets securities fraud. Explain how the provision is applied in determining whether fraud has occurred including when earnings management is the underlying motivation

> Explain how the quality of corporate governance, risk management, and compliance systems are critical in controlling financial restatement risk within organizations.

> Explain how restatements due to operational issues can trigger restatements.

> Explain how errors in accounting and reporting can trigger restatements.

> Distinguish between big R and little r restatements. What is required of management and the external auditors when such events occur?

> Assume the auditor has determined that prior financial statements need to be restated. What disclosures and other information should be communicated to shareholders, investors, and creditors about this matter?

> It has been said that “Businesses don’t fail – Leaders do.” Explain what this means.

> When should financial statements be restated?

> What is the purpose of using financial analysis to spot earnings management?

> Assume you are asked in an interview: Give me one word that describes you best? Then, explain why it is important in effective leadership. What would you say?

> Describe the role of professional judgment in ethical leadership as it pertains to accountants and auditors and the link to their moral role in society.

> On August 15, 2017, the SEC completed an Administrative Hearing process initiated by a PCAOB investigation of KPMG, LLP and one of their audit partners John Riordan, CPA1 for conducting a materially deficient audit of Miller Energy Resources Inc. KPMG be

> Billy Muldoon, CPA and CFO, just finished reading a preliminary draft of his company’s annual audit report from Local CPAs, LLC. He was concerned that the CPA firm plans to issue a qualified audit report because it had concluded that the company had a ma

> Alexion is a global biopharmaceutical company whose shares are traded on the Nasdaq Stock Market in the U.S. The company develops and sells drugs for patients with life-threatening rare and ultra-rare diseases. Alexion began commercial sales of its first

> When financial results aren’t what they seemed to be – and a company is forced to issue material financial restatements –should it be required to develop policies to claw back incentive pay and bonuses that were awarded to senior managers on the basis of

> Kay & Lee LLP was retained as the auditor for Holligan Industries to audit the financial statements required by prospective banks as a prerequisite to extending a loan to the client. The auditor knows whichever bank lends money to the client is likely to

> On December 13, 2012, Vertical Pharmaceuticals Inc. and an affiliated company sued Deloitte & Touche LLP in New Jersey state court for alleged accountant malpractice, claiming the firm’s false accusations of fraudulent conduct scrapped Trigen Laboratorie

> In the 2007 case of Paul V. Anjoorian v. Arnold Kilberg & Co., Arnold Kilberg, and Pascarella & Trench, the Rhode Island Superior Court ruled that a shareholder can sue a company’s outside accounting firm for alleged negligence in the preparation of the

> QSGI, Inc., is in the business of purchasing, refurbishing, selling, and servicing used computer equipment, parts, and mainframes. During its 2008 fiscal year (FY) and continuing up to its filing for Chapter 11 bankruptcy on July 2, 2009 (the “relevant p

> Joker & Wild LLC has just been sued by its audit client, Canasta, Inc., claiming the audit failed to be conducted in accordance with generally accepted auditing standards, lacked the requisite care expected in an audit, and failed to point out that inter

> Helen Roberts is reviewing two transactions recorded by her client, Biotechnologies (Biotech), as part of her accounting firm’s annual audit of the client for the December 31, 2021, financial statements. She knows Biotech is under pressure to maximize re

> Your tax client, Steve Michaels, told you that his former accountant who prepared his annual tax returns made errors that resulted in him suffering more than $100,000 in losses. Apparently, the errors involved adjustments to his income for a loss resulti

> In Chapter 4 we discussed the artificial tax shelter arrangements developed by KPMG LLP for wealthy clients that led to the settlement of a legal action with the Department of Treasury and the Internal Revenue Service. On August 29, 2005, KPMG admitted t

> One of the earliest frauds during the late 1990s and early 2000s was at Sunbeam. The SEC alleged in its charges against Sunbeam that top management engaged in a scheme to fraudulently misrepresent Sunbeam’s operating results in connecti

> On March 4, 2009, the SEC reached an agreement with Krispy Kreme Doughnuts, Inc., and issued a cease-and-desist order to settle charges that the company fraudulently inflated or otherwise misrepresented its earnings for the fourth quarter of its FY2003 a

> What are financial statement restatements?

> On June 12, 2017, GE announced that 30-year GE veteran and current President and CEO of GE Healthcare John Flannery would be replacing Jeff Immelt as CEO of the company as of August 1, 2017. Immelt had been the CEO for 16 years, taking over that role fro

> Monsanto is an agricultural seed and chemical company that manufactures and sells glyphosate, an herbicide, under the trade name “Roundup.” Roundup historically was one of Monsanto’s most profitable products, and the company sells it to both retailers an

> Jeremy Strong, CPA was recently hired as the new CFO of Imageware Consolidated (IC) a small publicly owned company. This is Jeremy’s first job outside of public accounting, leaving Deloitte after ten years, where he rose in the ranks to senior audit and

> Meredith Merriweather, CPA is the CFO of Trego Bikes and Trikes (TBT), a manufacturer of Bicycles ranging from tricycles to high end racing bikes. The company has good market penetration and has seen a very stable demand for its bikes over the last few y

> The story of Theranos, a company that sought to make blood tests cheaper, is a cautionary tale for Silicon Valley about what can happen when a company fails to develop internal control systems or overrides them, and when the CEO creates a psychological c

> You just became the new external auditor of a large public company that carries freight throughout the world. You just began to audit the 2021 financial statements and have come across a transaction that occurred in 2020 that would materially change the

> The North Face, Inc. (North Face) is an American outdoor product company specializing in outerwear, fleece, coats, shirts, footwear, and equipment such as backpacks, tents, and sleeping bags. North Face sells clothing and equipment lines catered toward w

> The SEC bought an action against BMW NA for inaccurate disclosures of its retail vehicle sales volume in the United States. In order to close the gap between actual retail sales volume and internal retail sales targets, and in an effort to publicly maint

> According to an October 16, 2017, article by Richard Clough of Bloomberg News,1 General Electric reported earnings per share of $.28, $.13, $.19 and $.15 for the quarter ending September 30, 2017, on an earnings call. Yes, you read that correctly, GE rep

> What is the risk of management bias for each earnings judgment and estimate? What safeguards should be in place to mitigate the risk of management bias, if any? What is the external auditor’s role in this process?

> It took a long time but the Securities and Exchange Commission finally acted and held auditors responsible for the fraud that occurred in banks during the financial recession in 2014. Surprisingly to some, the TierOne bank case explained below was the na

> It’s no fun accepting a position for your dream job and then red flags are raised that make you wonder about the culture of the company. Those are the thoughts of Donna Mason on January 18, 2022, as she prepares for a meeting with her a

> The CFO, King Bernard, of Blackswan Petfood, a large publicly traded manufacturer of organic gourmet dog and cat food, is getting ready for the quarterly conference call with major investors and financial analysts in two days. The King has been reviewing

> Exhibit 1 presents the fourth quarter press release of Allergan. Allergan is a global pharmaceutical company and a leader in a new industry model – Growth Pharma. Allergan’s product lines include Botox, Juvederm, Latis

> We can’t recognize revenue immediately, Paul, since we agreed to buy similar software from DSS,” Sarah Young stated. “That’s ridiculous,” Paul Henley replied. &acir

> Winners & Losers, Inc. (WLI) is a Nevada corporation with its principal place of business in Las Vegas. Its business model is to provide electronic sports betting in conjunction with a new law that legalized it in Nevada. The companyâ€

> Weatherford International PLC is a multinational Irish public limited company based in Switzerland, with U.S. offices in Houston, Texas. Weatherford’s shares are registered with the SEC and are listed on the NYSE. Weatherford files peri

> Ronnie Maloney, an audit partner for Forrester and Loomis, a registered public accounting firm in Boston, just received a meeting request from Jack McDuff, the chairman of the audit committee of Digital Solutions, one of his clients. The audit committee

> Diamond Foods, based in Stockton, California, is a premium snack food and culinary nut company with diversified operations. The company had a reputation of making bold and expensive acquisitions. Due to competition within the snack food industry, Diamond

> Maines and Wahlen state in their research paper on the reliability of accounting information: “Accrual estimates require judgment and discretion, which some firms under certain incentive conditions will exploit to report non-neutral accruals estimates wi

> In what some are suggesting is the worst financial reporting fraud since Enron, Wirecard filed for bankruptcy in June of 2020 after admitting that €1.9 billion Euros ($2.1bn U.S.) on its balance sheet (representing roughly 25% of its total assets) probab

> Travis McGee, a Senior Audit Manager for a Big Four Audit, Consulting, Tax and Data Analytics organization, has just spent the last year helping the firm rollout its new Artificial Intelligence (AI) based audit infrastructure. Travis is considered one of

> On January 30, 2018, General Electric (GE) announced that it was taking an after-tax charge of $6.2 billion in the December 31, 2017 financial statements and additional cash funding of $15 billion in statutory capital contributions to its insurance subsi

> Margaret Dairy is a CPA and the managing partner of Dairy and Cheese, a regional CPA firm located in northwest Wisconsin. She just left a meeting with a well-respected regional credit union headquartered in her hometown. Margaret was asked whether her fi

> Richard Lange, CPA, is a sole practitioner. The largest audit client in his office is Echo Park Sportswear (EP Sports). EP Sports is a privately owned company in South Bend, Indiana with a 12-person board of directors. Richard was hired by the audit comm

> Assume Ethan Lester and Vick Jensen are CPAs. Ethan was seen as a “model employee” who deserved a promotion to director of accounting, according to Kelly Fostermann, the CEO of Fostermann Corporation, a Maryland-based, largely privately held company that

> PwC violated SEC rule 2-02(b) of Regulation S-X and PCAOB Rule 3525 by engaging in improper professional conduct in violation of the independence rules on audit clients. This case is unique because the firm had mischaracterized certain nonaudit services

> On September 10, 2019, the Public Company Accounting Oversight Board (PCAOB) censured Marcum LLP and Alfonse Gregory on the basis of its findings that Marcum repeatedly violated PCAOB rules and standards over the course of four years by failing to satisf

> When Karen Ward started at Ernst & Young in 2013, only four senior managers in her division were women. All the partners were men. This was a red flag, but she didn’t see it then but soon realized that EY’s lack of female leaders was no accident but the

> Joe Kang is an owner and audit partner of Han, Kang & Lee, LLC. As the audit of Frost Systems was reaching its concluding stages on January 15, 2022, Kang met with Kate Boller, the CFO, who is also a CPA, to discuss the inventory valuation of one its hig

> Do you agree with Thomas McKee's conception of earnings management as applied to (a) operational earnings management and (b) accounting earnings management?

> Katy Carmichael, CPA, was just promoted to audit manager in the technology sector at a large public accounting firm. She started at the firm six years ago and has worked on a number of the same client audits for multiple years. She prefers being placed o

> Family Games, Inc., is a privately owned company with annual sales from a variety of wholesome electronic games that are designed for use by the entire family. The company sees itself as family-oriented and with a mission to serve the public. However, du

> Lance Popperson woke up in a sweat, with an anxiety attack coming on. Popperson popped two anti-anxiety pills, laid down to try and sleep for the third time that night, and thought once again about his dilemma. Popperson is an associate with the accounti

> In the first three months of 2021, Johnson Pharmaceutical’s sales and earnings were declining, placing the company in financial distress. As a result, Johnson had begun the process of borrowing $1 million to stay afloat. Around the same time, Paul Leona

> Jerry Maloney, CPA has been working at Mason Pharmaceuticals for fifteen years. Mason is a Fortune 1000 company whose stock trades on the New York Stock Exchange. He came to Mason after starting his career in the audit practice of PwC working on clients

> In 2005, Tony Menendez, a former Ernst & Young LLP auditor and Director of Technical Accounting and Research Training for Halliburton, blew the whistle on Halliburton’s accounting practices. The fight cost him nine years of his life. Just a few months la

> On September 8, 2016, Wells Fargo announced it was paying $185 million in fines to Los Angeles city and federal regulators to settle allegations that its employees created millions of fake bank accounts for customers. It also agreed to pay $142 million i

> John Stanton, CPA, is a seasoned accountant who left his Big-4 CPA firm Senior Manager position to become the CFO of a highly successful hundred million-dollar publicly-held manufacturer of solar panels. The company wanted John’s expertise in the renewab

> What possessed a CEO to hype a product that didn’t work and lie to financial institutions, pharmacies, the government, and the public about it? Is it hubris; plain and simple? Or was there something nefarious going on? The case of Theranos, an once high-

> What prompted partners at KPMG to facilitate cheating on internal training exams? In 2018, Timothy Daly, a former lead engagement partner, solicited and received questions and answers to the examination from a colleague, who was a second audit partner on

> Needles talks about the use of a continuum ranging from questionable or highly conservative to fraud to assess the amount to be recorded from for an estimated expense. Do you believe that the choice of an overly conservative or overly aggressive amount w

> Leaving home for the first time and going off to college is an exciting and stressful time for tens of thousands of students across the U.S. each year. Leaving the familiarity of family, friends and community behind and entering an often much more divers

> “I’m sorry, Jen. That’s the client's position,” Travis said. “I just don’t know if I can go along with it, Travis,” Jen replied. “I know. I agree with you. But, Chefs Delight is our biggest client, Jen. They’ve warned us that they will put the engagemen

> You are the Controller for Mountain Manufacturing which produces specialized components used in the manufacturing of cell phones sold by Apple, Motorola, and Samsung. The company is located in Southglenn Colorado, a suburb of Denver. Demand for your prod

> Jenna was irritated after class today. A classmate, Ben, had argued about the need for social justice reform that included defunding the police. Jenna was offended by the comments in part because her father was a policeman. She spoke to others in her cir

> Cleveland Custom Cabinets is a specialty cabinet manufacturer for high-end homes in the Cleveland Heights and Shaker Heights areas. The company manufactures cabinets built to the specifications of homeowners and employs 125 custom cabinetmakers and insta

> Section 179 of the IRS tax code allows qualifying businesses to deduct the full cost of “eligible property” on their income taxes as an expense, rather than requiring the cost of the property to be capitalized and depreciated over its useful life. The pr

> Milton Manufacturing Company produces a variety of textiles for distribution to wholesale manufacturers of clothing products. The company’s primary operations are located in Long Island City, New York, with branch factories and warehous

> On October 5, 2017, New York Times Investigative reporters Jodi Kantor and Megan Twohey broke the story ‘Harvey Weinstein Paid Off Sexual Harassment Accusers for Decades.’ Harvey Weinstein is one of the most powerful and influential movie executives in

> Sam and John have been friends for 20 years. They met in college and worked together for 10 of the 20 years. During that time, each made a promise that if they won a lottery they would share the winnings 50:50. Even though they drifted apart over the yea

> Hailey Declaire, a CPA, just sent the tax return that she prepared for a client in the marijuana growing and distribution business, Weeds ‘R’ Us, to Harry Smokes the manager of the tax department. Harry had just fielded a phone call from the president of