Question: Calculate breadth for NASDAQ using the data

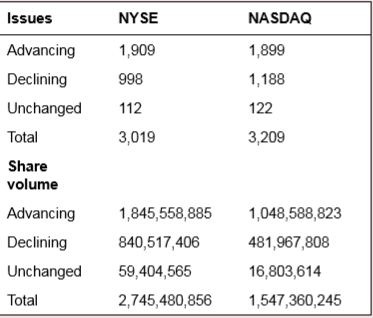

Calculate breadth for NASDAQ using the data in Figure 9.7. Is the signal bullish or bearish?

Figure 9.7:

> Consider a bond with a 10% coupon and with yield to maturity = 8%. If the bond’s yield to maturity remains constant, then in one year will the bond price be higher, lower, or unchanged? Why?

> Two bonds have identical times to maturity and coupon rates. One is callable at 105, the other at 110. Which should have the higher yield to maturity? Why?

> Why do bond prices go down when interest rates go up? Don’t bond investors like to receive high interest rates?

> A zero-coupon bond with face value $1,000 and maturity of five years sells for $746.22. a. What is its yield to maturity? b. What will happen to its yield to maturity if its price falls immediately to $730?

> A newly issued bond pays its coupons once a year. Its coupon rate is 5%, its maturity is 20 years, and its yield to maturity is 8%. a. Find the holding-period return for a one-year investment period if the bond is selling at a yield to maturity of 7% by

> A coupon bond paying semiannual interest is reported as having an ask price of 117% of its $1,000 par value. If the last interest payment was made one month ago and the coupon rate is 6%, what is the invoice price of the bond?

> What would be the likely effect on a bond’s yield to maturity of: a. An increase in the issuing firm’s times-interest earned ratio? b. An increase in the issuing firm’s debt-equity ratio? c. An increase in the issuing firm’s quick ratio?

> Consider a bond with a settlement date of February 22, 2022, and a maturity date of March 15, 2030. The coupon rate is 5.5%. a. If the yield to maturity of the bond is 5.34% (bond equivalent yield, semiannual compounding), what is the list price of the

> Is the coupon rate of the bond in the previous problem more or less than 9%?

> A bond has a current yield of 9% and a yield to maturity of 10%. Is the bond selling above or below par value? Explain.

> Joan McKay is a portfolio manager for a bank trust department. McKay meets with two clients, Kevin Murray and Lisa York, to review their investment objectives. Each client expresses an interest in changing his or her individual investment objectives. Bot

> A bond with a coupon rate of 7% makes semiannual coupon payments on January 15 and July 15 of each year. The Wall Street Journal reports the ask price for the bond on January 30 at 100.125. What is the invoice price of the bond? The coupon period has 182

> A bond has a par value of $1,000, a time to maturity of 10 years, and a coupon rate of 8% with interest paid annually. If the current market price is $800, what will be the percentage capital gain of this bond over the next year if its yield to maturity

> Fill in the table below for the following zero-coupon bonds, all of which have par values of $1,000.

> What is the option embedded in a callable bond? A puttable bond?

> Return to Table 10.1, showing the cash flows for TIPS bonds. a. What is the nominal rate of return on the bond in year 2? b. What is the real rate of return in year 2? c. What is the nominal rate of return on the bond in year 3? d. What is the real ra

> Redo the previous problem using the same data, but now assume that the bond makes its coupon payments annually. Why are the yields you compute lower in this case?

> A 20-year maturity bond with par value $1,000 makes semiannual coupon payments at a coupon rate of 8%. Find the bond equivalent and effective annual yield to maturity of the bond if the bond price is: a. $950 b. $1,000 c. $1,050

> Consider a bond paying a coupon rate of 10% per year semiannually when the market interest rate is only 4% per half-year. The bond has three years until maturity. a. Find the bond’s price today and six months from now after the next coupon is paid. b.

> Treasury bonds paying an 8% coupon rate with semiannual payments currently sell at par value. What coupon rate would they have to pay in order to sell at par if they paid their coupons annually?

> Which security has a higher effective annual interest rate? a. A three-month T-bill with face value of $100,000 currently selling at $97,645. b. A coupon bond selling at par and paying a 10% coupon semiannually.

> Here are some characteristics of two portfolios, the market index, and the risk-free asset. a. If you currently hold a market-index portfolio, would you choose to add either portfolio A or B to your holdings? Explain. b. If instead you could invest only

> The stated yield to maturity and realized compound yield to maturity of a (default-free) zero-coupon bond are always equal. Why?

> You buy an eight-year maturity bond that has a 6% current yield and a 6% coupon (paid annually). In one year, promised yields to maturity have risen to 7%. What is your holdingperiod return?

> Which of the following most accurately describes the behavior of credit default swaps? a. When credit risk increases, swap premiums increase. b. When credit and interest rate risks increase, swap premiums increase. c. When credit risk increases, swap

> An investor believes that a bond may temporarily increase in credit risk. Which of the following would be the most liquid method of exploiting this? a. The purchase of a credit default swap. b. The sale of a credit default swap. c. The short sale of t

> Define the following types of bonds: a. Catastrophe bond. b. Eurobond. c. Zero-coupon bond. d. Samurai bond. e. Junk bond. f. Convertible bond. g. Serial bond. h. Equipment obligation bond. i. Original-issue-discount bond. j. Indexed bond.

> Which one of the following would be a bullish signal to a technical analyst using moving average rules? a. A stock price crosses above its 52-week moving average. b. A stock price crosses below its 52-week moving average. c. The stock’s moving average

> All of the following actions are consistent with feelings of regret except: a. Selling losers quickly. b. Hiring a full-service broker. c. Holding on to losers too long.

> After Polly Shrum sells a stock, she avoids following it in the media. She is afraid that it may subsequently increase in price. What behavioral characteristic does Shrum have as the basis for her decision making? a. Fear of regret b. Representativenes

> Jill Davis tells her broker that she does not want to sell her stocks that are below the price she paid for them. She believes that if she just holds on to them a little longer, they will recover, at which time she will sell them. What behavioral charact

> What are some possible investment implications of the behavioral critique?

> You are considering an investment in a mutual fund with a 4% load and an expense ratio of 0.5%. You can invest instead in a bank CD paying 6% interest a. If you plan to invest for two years, what annual rate of return must the fund portfolio earn for yo

> What are the strong points of the behavioral critique of the efficient market hypothesis? What are some problems with the critique?

> What do we mean by fundamental risk, and why may such risk allow behavioral biases to persist for long periods of time?

> One apparent violation of the Law of One Price is the pervasive discrepancy between the prices and net asset values of closed-end mutual funds. Would you expect to observe greater discrepancies on diversified or less diversified funds? Why?

> Log in to Connect and link to the material for Chapter 9, where you will find five years of weekly returns for the S&P 500 and Fidelity’s Select Banking Fund (ticker FSRBX). Templates and spreadsheets are available in Connect a. Set up a spreadsheet to

> Log in to Connect and link to the material for Chapter 9, where you will find five years of weekly returns for the S&P 500. a. Set up a spreadsheet to calculate the 26-week moving average of the index. Set the value of the index at the beginning of the

> Using the following data on bond yields, calculate the change in the confidence index from last year to this year. What besides a change in confidence might explain the pattern of yield changes?

> If the trading volume in advancing shares on day 1 in the previous problem was 1.1 billion shares, while the volume in declining issues was 0.9 billion shares, what was the trin statistic for that day? Was trin bullish or bearish?

> Table 9.4 contains data on market advances and declines. Calculate cumulative breadth and decide whether this technical signal is bullish or bearish

> Yesterday, the Dow Jones industrials gained 54 points. However, 1,704 issues declined in price while 1,367 advanced. Why might a technical analyst be concerned even though the market index rose on this day?

> a. Construct a point and figure chart for Computers, Inc., using the data in Table 9.3. Use $2 increments for your chart. b. Do the buy or sell signals derived from your chart correspond to those derived from the moving average rule (see the previous pr

> Karen Kay, a portfolio manager at Collins Asset Management, is using the capital asset pricing model for making recommendations to her clients. Her research department has developed the information shown in the following exhibit. a. Calculate the equilib

> After reading about three successful investors in The Wall Street Journal you decide that active investing will also provide you with superior trading results. What sort of behavioral tendency are you exhibiting?

> Use the data in Table 9.3 to compute a five-day moving average for Computers, Inc. Can you identify any buy or sell signals? Tale 9.3:

> Table 9.3 presents price data for Computers, Inc., and a computer industry index. Does Computers, Inc., show relative strength over this period?

> Suppose Baa-rated bonds currently yield 6%, while Aa-rated bonds yield 4%. Now suppose that due to an increase in the expected inflation rate, the yields on both bonds increase by 1%. a. What would happen to the confidence index? b. Would this be inter

> Collect data on the S&P 500 for a period covering a few months. (You can download a historical sample from finance.yahoo.com.) Try to identify primary trends. Can you tell whether the market currently is in an upward or downward trend?

> Use the data from The Wall Street Journal in Figure 9.7 to calculate the trin ratio for NASDAQ. Is the trin ratio bullish or bearish? Figure 9.7:

> Following a shock to a firm’s intrinsic value, the share price will slowly but surely approach that new intrinsic value. Is this view characteristic of a technical analyst or a believer in efficient markets? Explain.

> What is meant by “limits to arbitrage”? Give some examples of such limits.

> Even if prices follow a random walk, they still may not be information ally efficient. Explain why this may be true, and why it matters for the efficient allocation of capital.

> In contrast to the capital asset pricing model, arbitrage pricing theory: a. Requires that markets be in equilibrium. b. Uses risk premiums based on micro variables. c. Specifies the number and identifies specific factors that determine expected retur

> What is meant by data mining, and why must technical analysts be careful not to engage in it?

> a. Investors are slow to update their beliefs when given new evidence. i. Disposition effect b. Investors are reluctant to bear losses due to their unconventional decisions. ii. Representativeness bias c. Investors exhibit less risk tolerance in their re

> “Constantly fluctuating stock prices suggest that the market does not know how to price stocks.” Respond.

> Which version of the efficient market hypothesis (weak, semistrong, or strong-form) focuses on the most inclusive set of information?

> In an efficient market, professional portfolio management can offer all of the following benefits except which of the following? a. Low-cost diversification. b. A targeted risk level. c. Low-cost record keeping. d. A superior risk-return trade-off.

> Which of the following statements are true if the efficient market hypothesis holds? a. It implies that future events can be forecast with perfect accuracy. b. It implies that prices reflect all available information. c. It implies that security price

> At a cocktail party, your co-worker tells you that he has beaten the market for each of the last three years. Suppose you believe him. Does this shake your belief in efficient markets?

> A successful firm like Microsoft has consistently generated large profits for years. Is this a violation of the EMH?

> If prices are as likely to increase as decrease, why do investors earn positive returns from the market on average?

> Suppose that as the economy moves through a business cycle, risk premiums also change. For example, in a recession when people are concerned about their jobs, risk aversion and therefore risk premiums might be higher. In a booming economy, tolerance for

> An investor takes as large a position as possible when an equilibrium price relationship is violated. This is an example of: a. A dominance argument. b. The mean-variance efficient frontier. c. Arbitrage activity. d. The capital asset pricing model.

> Examine the accompanying figure, which presents cumulative abnormal returns (CARs) both before and after dates on which insiders buy or sell shares in their firms. How do you interpret this figure? What are we to make of the pattern of CARs before and af

> Shares of small firms with thinly traded stocks tend to show positive CAPM alphas. Is this a violation of the efficient market hypothesis?

> Good News, Inc., just announced an increase in its annual earnings, yet its stock price fell. Is there a rational explanation for this phenomenon?

> You know that firm XYZ is very poorly run. On a scale of 1 (worst) to 10 (best), you would give it a score of 3. The market consensus evaluation is that the management score is only 2. Should you buy or sell the stock?

> We know that the market should respond positively to good news and that good-news events such as the coming end of a recession can be predicted with at least some accuracy. Why, then, can we not predict that the market will go up as the economy recovers?

> “If all securities are fairly priced, all must offer equal expected rates of return.” Comment.

> Dollar-cost averaging means that you buy equal dollar amounts of a stock every period, for example, $500 per month. The strategy is based on the idea that when the stock price is low, your fixed monthly purchase will buy more shares, and when the price i

> Why are the following effects” considered efficient market anomalies? Are there rational explanations for these effects? a. P/E effect. b. Book-to-market effect. c. Momentum effect. d. Small-firm effect.

> Which of the following phenomena would be either consistent with or a violation of the efficient market hypothesis? Explain briefly. a. Nearly half of all professionally managed mutual funds are able to outperform the S&P 500 in a typical year. b. Mone

> “If the business cycle is predictable, and a stock has a positive beta, the stock’s returns also must be predictable.” Respond.

> A zero-investment, well-diversified portfolio with a positive alpha could arise if: a. The expected return of the portfolio equals zero. b. The capital market line is tangent to the opportunity set. c. The law of one price remains inviolate. d. A risk

> Suppose you find that before large dividend increases, stocks show on average consistently positive abnormal returns. Is this a violation of the EMH?

> Steady Growth Industries has never missed a dividend payment in its 94-year history. Does this make it more attractive to you as a possible purchase for your stock portfolio?

> Which of the following observations would provide evidence against the semistrong form of the efficient market theory? Explain. a. Mutual fund managers do not on average make superior returns. b. You cannot make superior profits by buying (or selling)

> Suppose that, after conducting an analysis of past stock prices, you come up with the following observations. Which would appear to contradict the weak form of the efficient market hypothesis? Explain. a. The average rate of return is significantly gre

> Which of the following would most appear to contradict the proposition that the stock market is weakly efficient? Explain. a. Over 25% of mutual funds outperform the market on average. b. Insiders earn abnormal trading profits. c. Every January, the s

> Which of the following sources of market inefficiency would be most easily exploited? a. A stock price drops suddenly due to a large block sale by an institution. b. A stock is overpriced because traders are restricted from short sales. c. Stocks are

> If markets are efficient, what should be the correlation coefficient between stock returns for two no overlapping time periods?

> What must be the beta of a portfolio with E(rP) = 20%, if rf = 5% and E(rM) = 15%?

> In a single-factor market, the SML relationship of both the CAPM and the APT states that the risk premium on any security is proportional to beta, or, equivalently, that the security’s expected return must be a linear function of beta.

> Kidskin, Inc., stock has a beta of 1.2 and Quinn, Inc., stock has a beta of 0.6. Which of the following statements is most accurate? a. The equilibrium expected rate of return is higher for Kaskin than for Quinn. b. The stock of Kaskin has higher volati

> According to the theory of arbitrage: a. High-beta stocks are consistently overpriced. b. Low-beta stocks are consistently overpriced. c. Positive-alpha investment opportunities will quickly disappear. d. Rational investors will pursue arbitrage cons

> What is the expected rate of return for a stock that has a beta of 1 if the expected return on the market is 15%? a. 15%. b. More than 15%. c. Cannot be determined without the risk-free rate.

> Characterize each company in the previous problem as underpriced, overpriced, or properly priced.

> Here are data on two companies. The T-bill rate is 4% and the market risk premium is 6% What should be the expected rate of return for each company, according to the capital asset pricing model (CAPM)?

> Suppose the market can be described by the following three sources of systematic risk. Each factor in the following table has a mean value of zero (so factor values represent surprises relative to prior expectations), and the risk premiums associated wit

> As a finance intern at Pork Products, Jennifer Wainwright’s assignment is to come up with fresh insights concerning the firm’s cost of capital. She decides that this would be a good opportunity to try out the new material on the APT that she learned last

> The APT itself does not provide information on the factors that one might expect to determine risk premiums. How should researchers decide which factors to investigate? Is industrial production a reasonable factor to test for a risk premium? Why or why n

> Are the following true or false? Explain. a. Stocks with a beta of zero offer an expected rate of return of zero. b. The CAPM implies that investors require a higher return to hold highly volatile securities c. You can construct a portfolio with a bet

> Suppose the yield on short-term government securities (perceived to be risk-free) is about 4%. Suppose also that the expected return required by the market for a portfolio with a beta of 1 is 12%. According to the capital asset pricing model: a. What is

> Two investment advisers are comparing performance. One averaged a 19% return and the other a 16% return. However, the beta of the first adviser was 1.5, while that of the second was 1. a. Can you tell which adviser was a better selector of individual st

> In Problem below, assume the risk-free rate is 8% and the expected rate of return on the market is 18%. Use the SML of the simple (one-factor) CAPM to answer this question. A stock has an expected return of 6%. What is its beta?

> Assume that both X and Y are well-diversified portfolios and the risk-free rate is 8%. In this situation you could conclude that portfolios X and Y: a. Are in equilibrium. b. Offer an arbitrage opportunity. c. Are both underpriced. d. Are both fairly

> Which of the following statements about the standard deviation is/are true? A standard deviation: a. Is the square root of the variance. b. Is denominated in the same units as the original data. c. Can be a positive or a negative number.

> In Problem below, assume the risk-free rate is 8% and the expected rate of return on the market is 18%. Use the SML of the simple (one-factor) CAPM to answer this question. I am buying a firm with an expected perpetual cash flow of $1,000 but am unsure o