Question: Figure 27.3 includes a box for

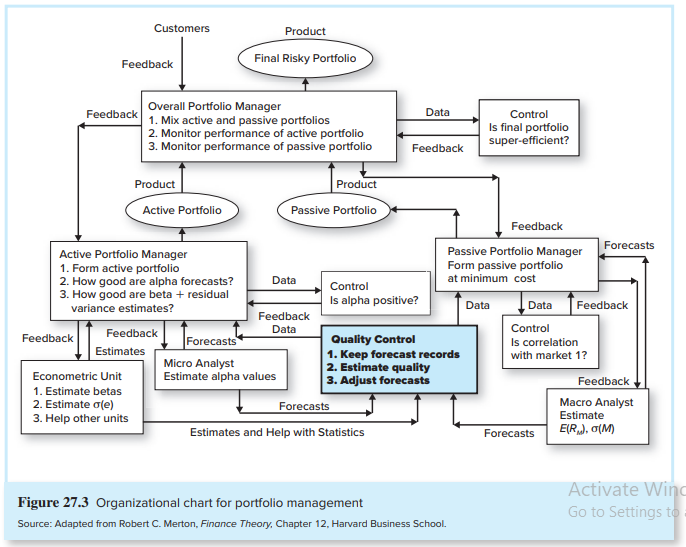

Figure 27.3 includes a box for the econometrics unit. Item (3) is to “help other units.†What sorts of specific tasks might this entail?

> Consider the following data for the firms Acme and Apex: a. Which firm has the higher economic value added? b. Which firm has the higher economic value added per dollar of invested capital?

> Use the financial statements of Heifer Sports Inc. in Table 19A to find the following information for Heifer’s: a. Inventory turnover ratio in 2020. b. Debt/equity ratio in 2020. c. Cash flow from operating activities in 2020. d. Avera

> Chiptech, Inc., is an established computer chip firm with several profitable existing products as well as some promising new products in development. The company earned $1 a share last year, and just paid out a dividend of $.50 per share. Investors belie

> The MoMi Corporation’s cash flow from operations before interest and taxes was $2 million in the year just ended, and it expects that this will grow by 5% per year forever. To make this happen, the firm will have to invest an amount equal to 20% of preta

> The Duo Growth Company just paid a dividend of $1 per share. The dividend is expected to grow at a rate of 25% per year for the next three years and then to level off to 5% per year forever. You think the appropriate market capitalization rate is 20% per

> a. MF Corp. has an ROE of 16% and a plowback ratio of 50%. If the coming year’s earnings are expected to be $2 per share, at what price will the stock sell? The market capitalization rate is 12%. b. What price do you expect MF shares to sell for in three

> In what circumstances is it most important to use multistage dividend discount models rather than constant-growth models?

> Recalculate the intrinsic value of Rio Tinto in each of the following scenarios by using the three-stage growth model of Spreadsheet 18.1 (available in Connect; link to Chapter 18 material). Treat each scenario independently. a. The terminal growth rate

> The Digital Electronic Quotation System (DEQS) Corporation pays no cash dividends currently and is not expected to for the next five years. Its latest EPS was $10, all of which was reinvested in the company. The firm’s expected ROE for the next five year

> The stock of Nogro Corporation is currently selling for $10 per share. Earnings per share in the coming year are expected to be $2. The company has a policy of paying out 50% of its earnings each year in dividends. The rest is retained and invested in pr

> The FI Corporation’s dividends per share are expected to grow indefinitely by 5% per year. a. If this year’s year-end dividend is $8 and the market capitalization rate is 10% per year, what must the current stock price be according to the DDM? b. If the

> The market consensus is that Analog Electronic Corporation has an ROE = 9%, a beta of 1.25, and plans to maintain indefinitely its traditional plowback ratio of 2/3. This year’s earnings were $3 per share. The annual dividend was just paid. The consensus

> Mary Smith, a CFA candidate, was recently hired for an analyst position at a large bank in London. Her first assignment is to examine the competitive strategies employed by various French wineries. Smith’s report identifies four winerie

> Mary Smith, a CFA candidate, was recently hired for an analyst position at a large bank in London. Her first assignment is to examine the competitive strategies employed by various French wineries. Smith’s report identifies four winerie

> Institutional Advisors for All Inc., or IAAI, is a consulting firm that advises foundations, endowments, pension plans, and insurance companies. The members of the research department foresee an upward trend in job creation and consumer confidence and pr

> OceanGate sells external hard drives for $200 each. Its total fixed costs are $30 million, and its variable costs per unit are $140. The corporate tax rate is 21%. If the economy is strong, the firm will sell 2 million drives, but if there is a recession

> a. Computer stocks currently provide an expected rate of return of 16%. MBI, a large computer company, will pay a year-end dividend of $2 per share. If the stock is selling at $50 per share, what must be the market’s expectation of the dividend growth ra

> General Weedkillers dominates the chemical weed control market with its patented product Weed-ex. The patent is about to expire, however. What are your forecasts for changes in the industry? Specifically, what will happen to industry prices, sales, the p

> a. Use a spreadsheet to answer this question and assume the yield curve is flat at a level of 4%. Calculate the convexity of a “bullet” fixed-income portfolio, that is, a portfolio with a single cash flow. Suppose a single $1,000 cash flow is paid in yea

> A newly issued bond has a maturity of 10 years and pays a 7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. b. Fin

> A 12.75-year-maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 150.3 and modified duration of 11.81 years. A 30-year-maturity 6% coupon bond making annual coupon payments also selling at a yield to m

> Mary Smith, a CFA candidate, was recently hired for an analyst position at a large bank in London. Her first assignment is to examine the competitive strategies employed by various French wineries. Smith’s report identifies four winerie

> a.Use a spreadsheet to calculate the durations of the two bonds in Spreadsheet 16.1 if the market interest rate increases to 12%. Why does the duration of the coupon bond fall while that of the zero remains unchanged? (Hint: Examine what happens to th

> A 30-year maturity bond has a 7% coupon rate, paid annually. It sells today for $867.42. A 20-year maturity bond has a 6.5% coupon rate, also paid annually. It sells today for $879.50. A bond market analyst forecasts that in five years, 25-year maturity

> Institutional Advisors for All Inc., or IAAI, is a consulting firm that advises foundations, endowments, pension plans, and insurance companies. The members of the research department foresee an upward trend in job creation and consumer confidence and pr

> Why do you think the change in the index of labor cost per unit of output is a useful lagging indicator of the macroeconomy? (See Table 17.2.)

> Your business plan for your proposed start-up firm envisions first-year revenues of $120,000, fixed costs of $30,000, and variable costs equal to one-third of revenue. a. What are expected profits based on these expectations? b. What is the degree of ope

> Tri-coat Paints has a current market value of $41 per share with earnings of $3.64. What is the present value of its growth opportunities (PVGO) if the required return is 9%?

> A 30-year maturity bond making annual coupon payments with a coupon rate of 12% has duration of 11.54 years and convexity of 192.4. The bond currently sells at a yield to maturity of 8%. a. Use a financial calculator or spreadsheet to find the price of t

> My pension plan will pay me $10,000 once a year for a 10-year period. The first payment will come in exactly five years. The pension fund wants to immunize its position. a. What is the duration of its obligation to me? The current interest rate is 10% pe

> You are managing a portfolio of $1 million. Your target duration is 10 years, and you can invest in two bonds, a zero-coupon bond with maturity of five years and a perpetuity, each currently yielding 5%. a. How much of (i) the zero-coupon bond and (ii) t

> Pension funds pay lifetime annuities to recipients. If a firm will remain in business indefinitely, the pension obligation will resemble a perpetuity. Suppose, therefore, that you are managing a pension fund with obligations to make perpetual payments of

> You will be paying $10,000 a year in tuition expenses at the end of the next two years. Bonds currently yield 8%. a. What are the present value and duration of your obligation? b. What maturity zero-coupon bond would immunize your obligation? c. Suppose

> Consider two firms producing smartphones. One uses a highly automated robotics process, whereas the other uses workers on an assembly line and pays overtime when there is heavy production demand. a. Which firm will have higher profits in a recession? b.

> Long-term Treasury bonds currently are selling at yields to maturity of nearly 6%. You expect interest rates to fall. The rest of the market thinks that they will remain unchanged over the coming year. In each question, choose the bond that will provide

> Unlike other investors, you believe the Fed is going to loosen monetary policy. What would be your recommendations about investments in the following industries? a. Gold mining b. Construction

> Rank the durations or effective durations of the following pairs of bonds: a. Bond A is a 6% coupon bond, with a 20-year time to maturity selling at par value. Bond B is a 6% coupon bond, with a 20-year time to maturity selling below par value. b. Bond A

> What characteristics will give firms greater sensitivity to business cycles?

> A firm pays a current dividend of $1.00, which is expected to grow at a rate of 5% indefinitely. If current value of the firm’s shares is $35.00, what is the required return based on the constant growth dividend discount model (DDM)?

> The administrator of a large pension fund wants to evaluate the performance of four portfolio managers. Each portfolio manager invests only in U.S. common stocks. Assume that during the most recent 5-year period, the average annual total rate of return i

> a. The historical yield spread between AAA bonds and Treasury bonds widened dramatically during the financial crisis in 2008. If you believed that the spread would soon return to more typical historical levels, what should you have done? b. This would be

> Repeat Problem 4, but now assume the coupons are paid semiannually. Problem 4: a. Find the duration of a 6% coupon bond making annual coupon payments if it has three years until maturity and has a yield to maturity of 6%. b. What is the duration if the

> What are the differences between bottom-up and top-down approaches to security valuation? What are the advantages of a top-down approach?

> If a security is underpriced (i.e., intrinsic value > price), then what is the relationship between its market capitalization rate and its expected rate of return?

> The difference between a Roth IRA and a traditional IRA is that in a Roth IRA taxes are paid on the income that is contributed, but the withdrawals at retirement are tax-free. In a traditional IRA, however, the contributions reduce your taxable income, b

> George More is a participant in a defined contribution pension plan that offers a fixed-income fund and a common stock fund as investment choices. He is 40 years old and has an accumulation of $100,000 in each of the funds. He currently contributes $1,50

> What is the least-risky asset for each of the following investors? a. A person investing for her 3-year-old child’s college tuition. b. A defined benefit pension fund with benefit obligations that have an average duration of 10 years. The benefits are no

> Your neighbor has heard that you successfully completed a course in investments and has come to seek your advice. She and her husband are both 50 years old. They just finished making their last payments for their condominium and their children’s college

> Suppose that sending an analyst to an executive education program will raise the precision of the analyst’s forecasts as measured by R-square by .01. How might you put a dollar value on this improvement? Provide a numerical example.

> Jand, Inc., currently pays a dividend of $1.22, which is expected to grow indefinitely at 5%. If the current value of Jand’s shares based on the constant-growth dividend discount model is $32.03, what is the required rate of return?

> How would the application of the BL model to a stock and bond portfolio (per the example in the text) affect security analysis? What does this suggest about the hierarchy of use of the BL and TB models?

> Is statistical arbitrage true arbitrage? Explain.

> With respect to hedge fund investing, the net return to an investor in a fund of funds would be lower than that earned from an individual hedge fund because of: a. Both the extra layer of fees and the higher liquidity offered. b. No reason; funds of fund

> Which of the following would be the most appropriate benchmark to use for hedge fund evaluation? a. A multifactor model. b. The S&P 500. c. The risk-free rate.

> Which of the following is most accurate in describing the problems of survivorship bias and backfill bias in the performance evaluation of hedge funds? a. Survivorship bias and backfill bias both result in upwardly biased hedge fund index returns. b. Sur

> Why is it harder to assess the performance of a hedge fund portfolio manager than that of a typical mutual fund manager?

> How might the incentive fee of a hedge fund affect the manager’s proclivity to take on high-risk assets in the portfolio?

> Here are data on three hedge funds. Each fund charges its investors an incentive fee of 20% of total returns. Suppose initially that a fund of funds (FF) manager buys equal amounts of each of these funds, and also charges its investors a 20% incentive fe

> Return again to Problem 14. Now suppose that the manager misestimates the beta of Waterworks stock, believing it to be .50 instead of .75. The standard deviation of the monthly market rate of return is 5%. a. What is the standard deviation of the (now im

> Return to Problem 14. a. Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta, and residual standard deviation as Waterworks. Assume the residual returns (the e terms in Equations 26.1 and 26.2) on each of these stocks a

> Deployment Specialists pays a current (annual) dividend of $1.00 and is expected to grow at 20% for 2 years and then at 4% thereafter. If the required return for Deployment Specialists is 8.5%, what is the intrinsic value of its stock?

> The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2% over the coming month. a. If he holds a

> Suppose a hedge fund follows the following strategy. Each month it holds $100 million of an S&P 500 index fund and writes out-of-the-money put options on $100 million of the index with exercise price 5% lower than the current value of the index. Suppose

> Log in to Connect and link to Chapter 26 to find a spreadsheet containing monthly values of the S&P 500 index. Suppose that in each month you had written an out-of-the-money put option on one unit of the index with an exercise price 5% lower than the cur

> Reconsider the hedge fund in Problem 10. Suppose it is January 1, the standard deviation of the fund’s annual returns is 50%, and the risk-free rate is 4%. The fund has an incentive fee of 20%, but its current high water mark is $66, and net asset value

> A hedge fund with net asset value of $62 per share currently has a high water mark of $66. Is the value of its incentive fee more or less than it would be if the high water mark were $67?

> Would a market-neutral hedge fund be a good candidate for an investor’s entire retirement portfolio? If not, would there be a role for the hedge fund in the overall portfolio of such an investor?

> Much of this chapter was written from the perspective of a U.S. investor. But suppose you are advising an investor living in a small country (choose one to be concrete). How might the lessons of this chapter need to be modified for such an investor?

> Calculate the contribution to total performance from currency, country, and stock selection for the manager in the example below. All exchange rates are expressed as units of foreign currency that can be purchased with 1 U.S. dollar.

> Now suppose the investor in Problem 3 also sells forward £5,000 at a forward exchange rate of $2.10/£. a. Recalculate the dollar-denominated returns for each scenario. b. What happens to the standard deviation of the dollar-denominated return? Compare it

> In Figure 25.2, we provide stock market returns in both local and dollar-denominated terms. Which of these is more relevant? What does this have to do with whether the foreign exchange risk of an investment has been hedged?

> The Generic Genetic (GG) Corporation pays no cash dividends currently and is not expected to for the next four years. Its latest EPS was $5, all of which was reinvested in the company. The firm’s expected ROE for the next four years is 20% per year, duri

> Do you agree with the following claim? “U.S. companies with global operations can give you international diversification.” Think about both business risk and foreign exchange risk.

> Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 6%, and the market’s average return was 14%. Performance is measured using an index model regression on excess re

> Based on current dividend yields and expected capital gains, the expected rates of return on portfolios A and B are 12% and 16%, respectively. The beta of A is .7, while that of B is 1.4. The T-bill rate is currently 5%, whereas the expected rate of retu

> A manager buys three shares of stock today and then sells one of those shares each year for the next three years. His actions and the price history of the stock are summarized below. The stock pays no dividends. a. Calculate the time-weighted geometric a

> XYZ’s stock price and dividend history are as follows: An investor buys three shares of XYZ at the beginning of 2018, buys another two shares at the beginning of 2019, sells one share at the beginning of 2020, and sells all four remaini

> Consider the rate of return of stocks ABC and XYZ. a. Calculate the arithmetic average return on these stocks over the sample period. b. Which stock has greater dispersion around the mean return? c. Calculate the geometric average returns of each stock.

> We have seen that market timing has tremendous potential value. Would it therefore be wise to shift resources to timing at the expense of security selection?

> We know that the geometric average (time-weighted return) on a risky investment is always lower than the corresponding arithmetic average. Can the IRR (the dollar-weighted return) similarly be ranked relative to these other two averages?

> Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector w

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Recalculate the intrinsic value of Rio Tinto shares using the free cash flow model of Spreadsheet 18.2 (available in Connect; link to Chapter 18 material) under each of the following assumptions. Treat each scenario independently. a. Rio Tinto’s P/E rati

> Is it possible for a positive alpha to be associated with inferior performance? Explain.

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Bill Smith is evaluating the performance of four large-cap equity portfolios: Funds A, B, C, and D. As part of his analysis, Smith computed the Sharpe ratio and the Treynor measure for all four funds. Based on his finding, the ranks assigned to the four

> During a particular year, the T-bill rate was 6%, the market return was 14%, and a portfolio manager with beta of .5 realized a return of 10%. a. Evaluate the manager based on the portfolio alpha. b. Reconsider your answer to part (a) in view of the empi

> Conventional wisdom says that one should measure a manager’s investment performance over an entire market cycle. What arguments support this convention? What arguments contradict it?

> A global equity manager is assigned to select stocks from a universe of large stocks throughout the world. The manager will be evaluated by comparing her returns to the return on the MSCI World Market Portfolio, but she is free to hold stocks from variou

> Evaluate the market timing and security selection abilities of four managers whose performances are plotted in the accompanying diagrams.

> A household savings-account spreadsheet shows the following entries: Use the Excel function XIRR to calculate the dollar-weighted average return between the first and final dates.

> You manage a $23 million portfolio, currently all invested in equities, and believe that the market is on the verge of a big but short-lived downturn. You would move your portfolio temporarily into T-bills, but you do not want to incur the transaction co

> Suppose that the value of the S&P 500 stock index is 2,000. a. If each E-mini futures contract (with a contract multiplier of $50) costs $25 to trade with a discount broker, how much is the transaction cost per dollar of stock controlled by the futures c

> The risk-free rate of return is 8%, the expected rate of return on the market portfolio is 15%, and the stock of Xyrong Corporation has a beta coefficient of 1.2. Xyrong pays out 40% of its earnings in dividends, and the latest earnings announced were $1

> Consider the futures contract written on the S&P 500 index and maturing in one year. The interest rate is 3%, and the future value of dividends expected to be paid over the next year is $35. The current index level is 2,000. Assume that you can short sel

> You believe that the spread between municipal bond yields and U.S. Treasury bond yields is going to narrow in the coming month. How can you profit from such a change using the municipal bond and T-bond futures contracts?

> Both gold-mining firms and oil-producing firms might choose to use futures to hedge uncertainty in future revenues due to price fluctuations. But trading activity sharply tails off for maturities beyond one year. Suppose a firm wishes to use available (s

> Consider these futures market data for the June delivery S&P 500 contract, exactly one year from today. The S&P 500 index is at 2,145, and the June maturity contract is at F0 = 2,146. a. If the current interest rate is 2.5%, and the average dividend rate

> Suppose the 1-year futures price on a stock-index portfolio is 1,914, the stock index currently is 1,900, the 1-year risk-free interest rate is 3%, and the year-end dividend that will be paid on a $1,900 investment in the market index portfolio is $40. a

> Suppose that at the present time, one can enter 5-year swaps that exchange LIBOR for 5%. An off-market swap would then be defined as a swap of LIBOR for a fixed rate other than 5%. For example, a firm with 7% coupon debt outstanding might like to convert