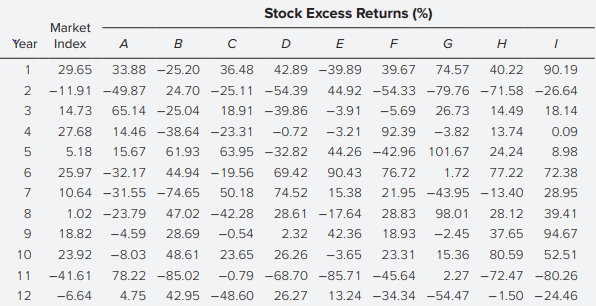

Question: Group the nine stocks into three portfolios,

Group the nine stocks into three portfolios, maximizing the dispersion of the betas of the three resultant portfolios. Repeat the test and explain any changes in the results.

> Consider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two for one in the last period. a. Calculate the rate of return on a price-weighted index of the three stocks

> Wall Street firms have traditionally compensated their traders with a share of the trading profits that they generated. How might this practice have affected traders’ willingness to assume risk? What agency problem can this practice engender?

> Turn to Figure 2.8 and look at the listing for Herbalife. a. How many shares could you buy for $5,000? b. What would be your annual dividend income from those shares? c. What must be Herbalife’s earnings per share? d. What was the firm&

> You see an advertisement for a book that claims to show how you can make $1 million with no risk and with no money down. Will you buy the book?

> Growth and value can be defined in several ways. “Growth” usually conveys the idea of a portfolio emphasizing or including only issues believed to possess above-average future rates of pershare earnings growth. Low current yield, high price-to-book ratio

> What are some advantages and disadvantages of top-down versus bottom-up investing styles?

> In what ways is preferred stock like long-term debt? In what ways is it like equity?

> Give an example of three financial intermediaries and explain how they act as a bridge between small investors and large capital markets or corporations.

> Oversight by large institutional investors or creditors is one mechanism to reduce agency problems. Why don’t individual investors in the firm have the same incentive to keep an eye on management?

> Discuss the advantages and disadvantages of the following forms of managerial compensation in terms of mitigating agency problems, that is, potential conflicts of interest between managers and shareholders. a. A fixed salary. b. Stock in the firm that mu

> Consider Figure 1A, which describes an issue of American gold certificates. a. Is this issue a primary or secondary market transaction? b. Are the certificates primitive or derivative assets?

> Examine the balance sheet of commercial banks in Table 1.3. a. What is the ratio of real assets to total assets? b. What is the ratio of real assets to total assets for nonfinancial firms (Table 1.4)? c. Why should this difference be expected?

> Reconsider Lanni Products from the previous problem. a. Prepare its balance sheet just after it gets the bank loan. What is the ratio of real assets to total assets? b. Prepare the balance sheet after Lanni spends the $70,000 to develop its software prod

> Lanni Products is a start-up computer software development firm. It currently owns computer equipment worth $30,000 and has cash on hand of $20,000 contributed by Lanni’s owners. For each of the following transactions, identify the real and/or financial

> Suppose housing prices across the world double. a. Is society any richer for the change? b. Are homeowners wealthier? c. Can you reconcile your answers to (a) and (b)? Is anyone worse off as a result of the change?

> a. Briefly explain the concept of the efficient market hypothesis (EMH) and each of its three forms—weak, semistrong, and strong—and briefly discuss the degree to which existing empirical evidence supports each of the three forms of the EMH. b. Briefly d

> Firms raise capital from investors by issuing shares in the primary markets. Does this imply that corporate financial managers can ignore trading of previously issued shares in the secondary market?

> Which of the following is true according to the pure expectations theory? Forward rates: a. Exclusively represent expected future short rates. b. Are biased estimates of market expectations. c. Always overestimate future short rates.

> Use the data from Problem 18. Suppose that you want to construct a 2-year maturity forward loan commencing in 3 years. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you hav

> Suppose that the prices of zero-coupon bonds with various maturities are given in the following table. The face value of each bond is $1,000. Maturity (years)…………..Price 1………………………$925.93 2………………………..853.39 3………………………..782.92 4………………………..715.00 5……………………

> The current yield curve for default-free zero-coupon bonds is as follows: Maturity (years) YTM (%) 1…………………..10% 2…………………..11 3…………………..12 a. What are the implied 1-year forward rates? b. Assume that the pure expectations hypothesis of the term structur

> Suppose that a 1-year zero-coupon bond with face value $100 currently sells at $94.34, while a 2-year zero sells at $84.99. You are considering the purchase of a 2-year-maturity bond making annual coupon payments. The face value of the bond is $100, and

> The yield to maturity (YTM) on 1-year zero-coupon bonds is 5%, and the YTM on 2-year zeros is 6%. The YTM on 2-year-maturity coupon bonds with coupon rates of 12% (paid annually) is 5.8%. a. What arbitrage opportunity is available for an investment banki

> You observe the following term structure: Effective Annual YTM 1-year zero-coupon bond…………6.1% 2-year zero-coupon bond…………6.2 3-year zero-coupon bond…………6.3 4-year zero-coupon bond…………6.4 a. If you believe that the term structure next year will be

> Prices of zero-coupon bonds reveal the following pattern of forward rates: Year Forward Rate 1……………………..5% 2……………………..7 3……………………..8 In addition to the zero-coupon bond, investors also may purchase a 3-year bond making annual payments of $6

> Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Bond Maturity (years) (zero-coupon) 1……………………………….$943.40 2………………………………….873.52 3………………………………….816.37 a. An 8.5% coupon $1,000 par bond pays an annual co

> Your investment client asks for information concerning the benefits of active portfolio management. She is particularly interested in the question of whether active managers can be expected to consistently exploit inefficiencies in the capital markets to

> The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9%. The face value of the bond is $100. a. At

> The term structure for zero-coupon bonds is currently: Maturity (years) YTM (%) 1………………………4% 2………………………5 3………………………6 Next year at this time, you expect it to be: Maturity (years) YTM (%) 1……………………5% 2……………………6 3……………………7 a. What do you expect the rate

> What is the relationship between forward rates and the market’s expectation of future short rates? Explain in the context of both the expectations hypothesis and the liquidity preference theory of the term structure of interest rates.

> Consider an 8% coupon bond selling for $953.10 with three years until maturity making annual coupon payments. The interest rates in the next three years will be, with certainty, r1 = 8%, r2 = 10%, and r3 = 12%. Calculate the bond’s (a) yield to maturity

> Why do bond prices go down when interest rates go up? Don’t bond lenders like to receive high interest rates?

> A newly issued bond pays its coupons once annually. Its coupon rate is 5%, its maturity is 20 years, and its yield to maturity is 8%. a. Find the holding-period return for a 1-year investment period if the bond is selling at a yield to maturity of 7% by

> FinCorp issued two bonds with 20-year maturities. Both bonds are callable at $1,050. The first bond was issued at a deep discount with a coupon rate of 4% and a price of $580 to yield 8.4%. The second bond was issued at par value with a coupon rate of 8.

> These two bonds were issued five years ago, with terms given in the following table: a. Why is the price range greater for the 6% coupon bond than the floating-rate bond? b. What factors could explain why the floating-rate bond is not always sold at par

> An investor believes that a bond may temporarily increase in credit risk. Which of the following would be the most liquid method of exploiting this? a. The purchase of a credit default swap. b. The sale of a credit default swap. c. The short sale of the

> Assume that two firms issue bonds with the following characteristics. Both bonds are issued at par. Ignoring credit quality, identify four features of these issues that might account for the lower coupon on the ABC debt. Explain.

> Karen Kay, a portfolio manager at Collins Asset Management, is using the capital asset pricing model for making recommendations to her clients. Her research department has developed the information shown in the following exhibit. a. Calculate expected re

> A 2-year bond with par value $1,000 making annual coupon payments of $100 is priced at $1,000. What is the yield to maturity of the bond? What will be the realized compound yield to maturity if the 1-year interest rate next year turns out to be (a) 8%, (

> A 30-year maturity, 7% coupon bond paying coupons semiannually is callable in five years at a call price of $1,100. The bond currently sells at a yield to maturity of 6% (3% per half-year). a. What is the yield to call? b. What is the yield to call if th

> A newly issued 10-year maturity, 4% coupon bond making annual coupon payments is sold to the public at a price of $800. What will be an investor’s taxable income from the bond over the coming year? The bond will not be sold at the end of the year. The bo

> Consider a bond paying a coupon rate of 10% per year semiannually when the market interest rate is only 4% per half-year. The bond has three years until maturity. a. Find the bond’s price today and six months from now after the next coupon is paid. b. Wh

> Repeat Problem 11 using the same data, but now assume that the bond makes its coupon payments annually. Why are the yields you compute lower in this case? Problem 11: A 20-year maturity bond with par value of $1,000 makes semiannual coupon payments at

> A 20-year maturity bond with par value of $1,000 makes semiannual coupon payments at a coupon rate of 8%. Find the bond equivalent and effective annual yield to maturity of the bond if the bond price is: a. $950 b. $1,000 c. $1,050

> Assume you have a 1-year investment horizon and are trying to choose among three bonds. All have the same degree of default risk and mature in 10 years. The first is a zero-coupon bond that pays $1,000 at maturity. The second has an 8% coupon rate and pa

> Define the following types of bonds: a. Catastrophe bond b. Eurobond c. Zero-coupon bond d. Samurai bond e. Junk bond f. Convertible bond g. Serial bond h. Equipment obligation bond i. Original-issue discount bond j. Indexed bond k. Callable bond l. Putt

> Specify the hypothesis for a test of a second-pass regression for the two-factor SML.

> Explain Roll’s critique as it applies to the tests performed in Problems 1–5.

> Joan McKay is a portfolio manager for a bank trust department. McKay meets with two clients, Kevin Murray and Lisa York, to review their investment objectives. Each client expresses an interest in changing his or her individual investment objectives. Bot

> Summarize your test results and compare them to the results reported in the text.

> Suppose you own your own business, which now makes up about half your net worth. On the basis of what you have learned in this chapter, how would you structure your portfolio of financial assets?

> Can you identify a factor portfolio for the second factor?

> Do the data suggest a two-factor economy?

> All of the following actions are consistent with feelings of regret except: a. Selling losers quickly. b. Hiring a full-service broker. c. Holding on to losers too long.

> Some advocates of behavioral finance agree with efficient market advocates that indexing is the optimal investment strategy for most investors. But their reasons for this conclusion differ greatly. Compare and contrast the rationale for indexing accordin

> Even if behavioral biases do not affect equilibrium asset prices, why might it still be important for investors to be aware of them?

> What sorts of factors might limit the ability of rational investors to take advantage of any “pricing errors” that result from the actions of “behavioral investors”?

> Log in to Connect and link to the material for Chapter 12, where you will find five years of weekly returns for the S&P 500 and Fidelity’s Select Banking Fund (ticker FSRBX). a. Set up a spreadsheet to calculate the relative strength of the banking secto

> Briefly explain whether investors should expect a higher return on portfolio A than on portfolio B according to the capital asset pricing model.

> Log in to Connect and link to the material for Chapter 12, where you will find five years of weekly returns for the S&P 500. a. Set up a spreadsheet to calculate the 26-week moving average of the index. Set the value of the index at the beginning of the

> Why would an advocate of the efficient market hypothesis believe that even if many investors exhibit the behavioral biases discussed in the chapter, security prices might still be set efficiently?

> Using the data in Table 12A, compute a five-day moving average for Computers, Inc. Can you identify any buy or sell signals?

> Table 12A presents price data for Computers, Inc., and a computer industry index. Does Computers, Inc., show relative strength over this period?

> What is meant by data mining, and why must technical analysts be careful not to engage in it?

> Explain how some of the behavioral biases discussed in the chapter might contribute to the success of technical trading rules.

> If prices are as likely to increase as decrease, why do investors earn positive returns from the market on average?

> Why are the following “effects” considered efficient market anomalies? Are there rational explanations for any of these effects? a. P/E effect. b. Book-to-market effect. c. Momentum effect. d. Small-firm effect.

> “Constantly fluctuating stock prices suggest that the market does not know how to price stocks.” Comment.

> At a cocktail party, your co-worker tells you that he has beaten the market for each of the last three years. Suppose you believe him. Does this shake your belief in efficient markets?

> Dudley Trudy, CFA, recently met with one of his clients. Trudy typically invests in a master list of 30 equities drawn from several industries. As the meeting concluded, the client made the following statement: “I trust your stock-picking ability and bel

> Suppose that as the economy moves through a business cycle, risk premiums also change. For example, in a recession, when people are concerned about their jobs, risk tolerance might be lower and risk premiums might be higher. In a booming economy, toleran

> Examine the accompanying figure, which presents cumulative abnormal returns both before and after dates on which insiders buy or sell shares in their firms. How do you interpret this figure? What are we to make of the pattern of CARs before and after the

> Shares of small firms with thinly traded stocks tend to show positive CAPM alphas. Is this a violation of the efficient market hypothesis?

> Suppose that during a certain week the Fed announces a new monetary growth policy, Congress surprisingly passes legislation restricting imports of foreign automobiles, and Ford comes out with a new car model that it believes will increase profits substan

> Dollar-cost averaging means that you buy equal dollar amounts of a stock every period, for example, $500 per month. The strategy is based on the idea that when the stock price is low, your fixed monthly purchase will buy more shares, and when the price i

> Investors expect the market rate of return in the coming year to be 12%. The T-bill rate is 4%. Changing Fortunes Industries’ stock has a beta of .5. The market value of its outstanding equity is $100 million. a. Using the CAPM, what is your best guess c

> A successful firm like Microsoft has consistently generated large profits for years. Is this a violation of the EMH?

> The monthly rate of return on T-bills is 1%. The market went up this month by 1.5%. In addition, AmbChaser, Inc., which has an equity beta of 2, surprisingly just won a lawsuit that awards it $1 million immediately. a. If the original value of AmbChaser

> Which of the following hypothetical phenomena would be either consistent with or a violation of the efficient market hypothesis? Explain briefly. a. Nearly half of all professionally managed mutual funds are able to outperform the S&P 500 in a typical ye

> “If the business cycle is predictable, and a stock has a positive beta, the stock’s returns also must be predictable.” Respond.

> Abigail Grace has a $900,000 fully diversified portfolio. She subsequently inherits ABC Company common stock worth $100,000. Her financial adviser provided her with the following estimates: / The correlation coefficient of ABC stock returns with the or

> Which of the following would be a viable way to earn abnormally high trading profits if markets are semistrong-form efficient? a. Buy shares in companies with low P/E ratios. b. Buy shares in companies with recent above-average price changes. c. Buy shar

> Respond to each of the following comments. a. If stock prices follow a random walk, then capital markets are little different from a casino. b. A good part of a company’s future prospects are predictable. Given this fact, stock prices can’t possibly foll

> The SML relationship states that the expected risk premium on a security in a one-factor model must be directly proportional to the security’s beta. Suppose that this were not the case. For example, suppose that expected return rises mo

> Assume that security returns are generated by the single-index model, where Ri is the excess return for security i and RM is the market’s excess return. The risk-free rate is 2%. Suppose also that there are three securities, A, B, and C

> Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1 on the market index. Firm-specific returns all have a standard deviation of 30%. Suppose that an analyst studies 20 stocks and

> Assume that both portfolios A and B are well diversified, that E(rA) = 12%, and E(rB) = 9%. If the economy has only one factor, and βA = 1.2, whereas βB = .8, what must be the risk-free rate?

> Consider the following data for a one-factor economy. Both portfolios are well diversified. Suppose that another portfolio, portfolio E, is well diversified with a beta of .6 and expected return of 8%. Would an arbitrage opportunity exist? If so, what wo

> Suppose that there are two independent economic factors, F1 and F2. The risk-free rate is 6%, and all stocks have independent firm-specific components with a standard deviation of 45%. Portfolios A and B are both well-diversified with the following prope

> If the APT is to be a useful theory, the number of systematic factors in the economy must be small. Why?

> The APT itself does not provide guidance concerning the factors that one might expect to determine risk premiums. How should researchers decide which factors to investigate? Why, for example, is industrial production a reasonable factor to test for a ris

> George Stephenson’s current portfolio of $2 million is invested as follows: Stephenson soon expects to receive an additional $2 million and plans to invest the entire amount in an index fund that best complements the current portfolio.

> Small firms generally have relatively high loadings (high betas) on the SMB (small minus big) factor. a. Explain why this is not surprising. b. Now suppose two unrelated small firms merge. Each will be operated as an independent unit of the merged compan

> Assume a universe of n (large) securities for which the largest residual variance is not larger than n σM2. Construct as many different weighting schemes as you can that generate well diversified portfolios.

> Orb Trust (Orb) has historically leaned toward a passive management style of its portfolios. The only model that Orb’s senior management has promoted in the past is the capital asset pricing model (CAPM). Now Orb’s management has asked one of its analyst

> Orb Trust (Orb) has historically leaned toward a passive management style of its portfolios. The only model that Orb’s senior management has promoted in the past is the capital asset pricing model (CAPM). Now Orb’s management has asked one of its analyst

> Orb Trust (Orb) has historically leaned toward a passive management style of its portfolios. The only model that Orb’s senior management has promoted in the past is the capital asset pricing model (CAPM). Now Orb’s management has asked one of its analyst

> As a finance intern at Pork Products, Jennifer Wainwright’s assignment is to come up with fresh insights concerning the firm’s cost of capital. She decides that this would be a good opportunity to try out the new material on the APT that she learned last

> Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Risk Premium Industrial production (I ) ………………………………6% Interest rates(R)

> Consider the following multifactor (APT) model of security returns for a particular stock. / a. If T-bills currently offer a 6% yield, find the expected rate of return on this stock if the market views the stock as fairly priced. b. Suppose that the mar