Question: On December 31, Year 7, Maple Company

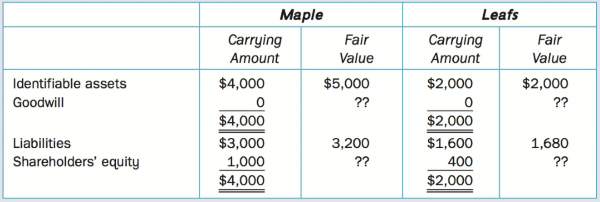

On December 31, Year 7, Maple Company issued preferred shares with a fair value of $1,200,000 to acquire 24,000 (60%) of the common shares of Leafs Limited. The Leafs shares were trading in the market at around $40 per share just days prior to and just after the purchase by Maple. Maple had to and was willing to pay a premium of $10 per share, or $240,000 in total, in order to gain control over Leafs. The balance sheets for the two companies just prior to acquisition were as follows (in OOOs):

Consolidated financial statements will be prepared to combine the financial statements for the two companies. The management of Maple is concerned about the valuation of goodwill on the consolidated financial statements. It was willing to pay a premium of $240,000 to gain control of Leafs. It maintains that it would have paid the same premium in total whether it acquired 60% or 100% of the shares of Leafs.

Given that the return on assets is a closely monitored ratio by the shareholders, the management of Maple would like to minimize the value assigned to goodwill on consolidation. Management wants to see how the consolidated balance sheet would differ under three different theories of reporting: proprietary, parent company extension, and entity. Management also has the following questions when reporting this business combination:

• How will we determine the value of the goodwill for the subsidiary?

• How will this affect the valuation of NCI?

• Will we have to revalue the subsidiary's assets and liabilities every year when we prepare the consolidated financial statements?

• Which consolidation theory best reflects the economic reality of the business combination?

Required:

Prepare a consolidated balance sheet at the date of acquisition under the three theories, and respond to the questions asked by management.

Transcribed Image Text:

Мaple Leafs Carrying Fair Carrying Fair Amount Value Aтount Value Identifiable assets $4,000 $5,000 $2,000 $2,000 Goodwill ?? ?? $4,000 $2,000 $3,000 $1,600 400 Liabilities 3,200 1,680 Shareholders' equity 1,000 $4,000 ?? ?? $2,000

> You, CPA, are employed at Beaulieu & Beauregard, Chartered Professional Accountants. On November 20, Year 3, Dominic Jones, a partner in your firm, sends you the following email: Our firm has been reappointed auditors of Floral Impressions Ltd. (FIL)

> Identify the financial statement ratios typically used to assess profitability, liquidity and solvency, respectively.

> Foreign Infants Adoption Inc. (FIA) is a consulting company wholly owned by Roger Tremblay, a wealthy, recently retired lawyer. FIA helps Canadian families adopt infants from other countries. Typically, these infants have been abandoned or have lost thei

> Mega Communications Inc. (MCI) is a Canadian-owned public company operating throughout North America. Its core business is communications media, including newspapers, radio, television, and cable. The company's year-end is December 31. You, a CPA, have r

> RAD Communications Ltd. (RAD), a Canadian public company, recently purchased the shares of TOP Systems Inc. (TOP), a Canadian-controlled private corporation. Both companies are in the communications industry and own television, radio, and magazine and ne

> Vulcan Manufacturing Limited (VML) is a Canadian-based multinational plastics firm, with subsidiaries in several foreign countries and worldwide consolidated total assets of $500 million. VML's shares are listed on a Canadian stock exchange. VML is attra

> Long Life Enterprises was a well-€stablished Toronto-based company engaged in the importation and wholesale marketing of specialty grocery items originating in various countries of the western Pacific Rim. They had recently also entered the high-risk bus

> The Rider Corporation operates throughout Canada buying and selling widgets. In hopes of expanding into more profitable markets, the company recently decided to open a small subsidiary in California. On October 1, Year 2, Rider invested CDN$1,000,000 in

> You, CPA, have been working for Plener and Partners, Chartered Professional Accountants (P&P), a mid-size CPA firm, for three years. You have been assigned a new project for a long-term client of your firm, Oxford Developments Inc. (ODI). Information

> ZIM Inc. (ZIM) is a high-technology company that develops, designs, and manufactures telecommunications equipment. ZIM was founded in Year 5 by Dr. Alex Zimmer, the former assistant head of research and development at a major telephone company. He and th

> The United Football League (UFL), a North American professional football league, has been in work stoppage since July 1, Year 9, immediately after the six-week training camp ended. Faced with stalled negotiations, the players' union representing the leag

> Canada Cola Inc. (CCI) is a public company engaged in the manufacture and distribution of soft drinks across Canada. Its primary product is Canada Cola ("Fresh as a Canadian stream"), which is a top seller in Canada and generates large export sales. You

> For the items listed in Exhibit 1.1, for which items would the debt-to-equity ratio not change when a company switched from ASPE to IFRS? Exhibit 1.1: Accounting Item IFRS ASPE Very extensive for many items, especially financial instruments, post-e

> Interfast Corporation, a fastener manufacturer, has recently been expanding its sales through exports to foreign markets. Earlier this year, the company negotiated the sale of several thousand cases of fasteners to a wholesaler in the country of Loznia.

> Segment reporting can provide useful information for investors and competitors. Segment disclosures can result in competitive harm for the company making the disclosures. By analyzing segment information, potential competitors can identify and concentrat

> P Co. is looking for some additional financing in order to renovate one of the company's manufacturing plants. It is having difficulty getting new debt financing because its debt-to-equity ratio is higher than the 3:1limit stated in its bank covenant. It

> Mr. Landman has spent the last 10 years developing small commercial strip malls and has been very successful. He buys a residential property in a high-traffic area, rezones the property, and then sells it to a contractor who builds the plaza and sells it

> Enviro Facilities Inc. (EFl) is a large, diversified Canadian-controlled private company with several Canadian and U.S. subsidiaries, operating mainly in the waste management and disposal industry. EFl was incorporated more than 50 years ago, and has gro

> You, a CPA, have recently accepted a job at the accounting firm of Cat, Scan & Partners, as a manager, and have been assigned the audit of Vision Clothing Inc. (VCI). The partner in charge had been at VCI the previous week and had met with the contro

> Dry Quick (DQ) is a medium-sized, private manufacturing company located near Timmins, Ontario. DQ has a June 30 year-end. Your firm, Poivre & Sel (P&S), has recently been appointed as auditors for DQ. It is now August 2, Year 10. You, CPA, have b

> Traveller Bus Lines Inc. (TBL) is a wholly owned subsidiary of Canada Transport Enterprises Inc. (CTE), a publicly traded transportation and communications conglomerate. TBL is primarily in the business of operating buses over short- and long distance ro

> Identify some of the financial statement items for which ASPE is different from IFRS.

> For the past 10 years, Prince Company (Prince) has owned 75,000 or 75% of the common shares of Stiff Inc. (Stiff). Elizabeth Winer owns another 20% and the other 5% are widely held. Although Prince has the controlling interest, you would never know it du

> On December 31, Year 7, Pepper Company, a public company, agreed to a business combination with Salt Limited, an unrelated private company. Pepper issued 72 of its common shares for all (50) of the outstanding common shares of Salt 'This transaction incr

> It is Monday, September 13, Year 10. You, CPA, work at Fife & Richardson LLP, a CPA firm. Ken Simpson, one of the partners, approaches you mid-morning regarding Brennan & Sons Limited (BSL), a private company client for which you performed the Au

> Stephanie Baker is an audit senior with the public accounting firm of Wilson & Lang. It is February Year 9, and the audit of Canadian Development Limited (CDL) for the year ended December 31, Year 8, is proceeding. Stephanie has identified several transa

> On January 1, Year 4, Plum purchased 100% of the common shares of Slum. On December 31, Year 5, Slum purchased a machine for $168,000 from an external supplier. The machine had an estimated useful life of six years with no residual value. On December 31,

> In early September Year 1, your firm's audit client, D Ltd. (D) acquired in separate transactions an 80% interest in N Ltd. (N) and a 40% interest in K Ltd. (K). All three companies are federally incorporated Canadian companies and have August 31 year-en

> Enron Corporation's 2000 financial statements disclosed the following transaction with LIM2, a nonconsolidated special purpose entity (SPE) that was formed by Enron: In June 2000, LIM2 purchased dark fibre optic cable from Enron for a purchase price of

> Digital Future Technologies (DFT) is a public technology company. It has a September 30 year-end, and last year it adopted IFRS. Kin Lo is a partner with Hi & Lo, the accounting firm that was newly appointed as DFT's auditor in July for the year endi

> Wedding Planners Limited (WP), owned by Anne and Francois Tremblay, provides wedding planning and related services. WP owns a building (the Pavilion) that has been custom-made for hosting weddings. Usually, WP plans a wedding from start to finish and hos

> You, the CPA, an audit senior at Grey & Co., Chartered Professional Accountants, are in charge of this year's audit of Plex-Fame Corporation (PFC). PFC is a rapidly expanding, diversified, and publicly owned entertainment company with operations througho

> Briefly explain why a Canadian private company may decide to follow IFRS even though it could follow ASPE.

> Distinguish between unrestricted and restricted contributions of a charitable organization.

> Good Quality Auto Parts Limited (GQ) is a medium-sized, privately owned producer of auto parts, which are sold to car manufacturers, repair shops, and retail outlets. In March Year 10, the union negotiated a new three-year contract with the company for t

> You, the controller, recently had the following discussion with the president: President: I just don't understand why we can't recognize the revenue from the intercompany sale of inventory on the consolidated financial statements. The subsidiary company

> Gerry's Fabrics Ltd. (GFL), a private company, manufactures a variety of clothing for women and children and sells it to retailers across Canada. Until recently, the company has operated from the same plant since its incorporation under federal legislati

> Beaver Ridge Oilers' Players Association and Mr. Slim, the CEO of the Beaver Ridge Oilers Hockey Club (Club), ask for your help in resolving a salary dispute. Mr. Slim presents the following income statement to the player representatives: Mr. Slim argu

> Total Protection Limited (TPL) was incorporated on January 1, Year 1, by five homebuilders in central Canada to provide warranty protection for new-home buyers. Each shareholder owns a 20% interest in TPL. While most homebuilders provide one-year warrant

> It is now mid-September Year 3. Growth Investments Limited (GIL) has been owned by Sam and Ida Growth since its incorporation under the Canada Business Corporations Act many years ago. The owners, both 55 years of age, have decided to effect a corporate

> BIO Company is a private company. It employs 30 engineers and scientists who are involved with research and development of various biomedical devices. All of the engineers and scientists are highly regarded and highly paid in the field of biomedical rese

> It is September 15, Year 8. The partner has called you, CPA, into his office to discuss a special engagement related to a purchase agreement. John Toffler, a successful entrepreneur with several different businesses in the automotive sector, is finalizin

> Lauder Adventures Limited (LAL) was incorporated over 40 years ago as an amusement park and golf course. Over time, a nearby city has grown to the point where it borders on LAL's properties. In recent years LAL's owners, who are all members of one family

> When Valero Energy Corp. acquired Ultramar Diamond Shamrock Corp. (UDS) for US$6 billion, it created the second-largest refiner of petroleum products in North America, with over 23,000 employees in the United States and Canada, total assets of $10 billio

> Briefly explain why the Canadian AcSB decided to create a separate section of the CPA Canada Handbook for private enterprises.

> Factory Optical Distributors (FOD) is a publicly held manufacturer and distributor of high-quality eyeglass lenses located in Burnaby, British Columbia. For the past 10 years, the company has sold its lenses on a wholesale basis to optical shops across C

> Planet Publishing Limited (Planet) is a medium-sized, privately owned Canadian company that holds exclusive Canadian distribution rights for the publications of Typset Daily Corporation (TDC). Space Communications Ltd. (Space), an unrelated privately own

> How are translation exchange gains and losses reflected in financial statements if the foreign operation's functional currency is the Canadian dollar? Would the treatment be different if the foreign operation's functional currency were not the Canadian d

> What translation method should be used for a subsidiary that operates in a highly inflationary environment? Why?

> What difference does it make whether the foreign operation's functional currency is the same or different than the parent's presentation currency? What method of translation should be used for each?

> What should happen if a foreign subsidiary's financial statements have been prepared using accounting principles different from those used in Canada?

> Define a foreign operation as per IAS 21.

> How are gains and losses on financial instruments used to hedge the net investment in a foreign operation reported in the consolidated financial statements when the PCT method is used to translate the foreign operation?

> Explain how the acquisition cost is determined for a reverse takeover.

> Why might a company want to hedge its balance sheet exposure? What is the paradox associated with hedging balance sheet exposure?

> What are the three major issues related to the translation of foreign currency financial statements?

> Would hedge accounting be used in a situation in which the hedged item and the hedging instrument were both monetary items on a company's statement of financial position? Explain.

> If the sales of a foreign subsidiary all occurred on one day during the year, would the sales be translated at the average rate for the year or the rate on the date of the sales? Explain.

> When translating the financial statements of the subsidiary at the date of acquisition by the parent, the exchange rate on the date of acquisition is used to translate plant assets rather than the exchange rate on the date when the subsidiary acquired th

> Explain how the FCT method produces results that are consistent with the normal measurement and valuation of assets and liabilities for domestic transactions and operations.

> "If the translation of a foreign operation produced a gain under the FCT method, the translation of the same company could produce a loss if the operation were translated under the PCT method." Do you agree with this statement? Explain.

> The amount of the accumulated foreign exchange adjustments appearing in the translated financial statements of a subsidiary could be different from the amount appearing in the consolidated financial statements. Explain how.

> Does the FCT method use the same unit of measure as the PCT method? Explain.

> The FCT and PCT methods each produce different amounts for translation gains and losses due to the items at risk. Explain.

> When will the premium paid on a forward contract to hedge a firm commitment to purchase inventory be reported in income under a cash flow hedge? Explain.

> List some ways that a Canadian company could hedge against foreign currency exchange rate fluctuations.

> Differentiate between the accounting for a fair value hedge and a cash flow hedge.

> Differentiate between a spot rate and a closing rate.

> Describe when to use the closing rate and when to use the historical rate when translating assets and liabilities denominated in a foreign currency. Explain whether this practice is consistent with the way we normally measure assets and liabilities.

> How are foreign-currency-denominated assets and liabilities measured on the transaction date? How are they measured on a subsequent balance sheet date?

> Differentiate between a spot rate and a forward rate.

> You read in the newspaper, "One U.S. dollar can be exchanged for 1.15 Canadian dollars." Is this a direct or an indirect quotation? If your answer is indirect, what is the direct quotation? If your answer is direct, what is the indirect quotation?

> What is the difference between pegged and floating exchange rates?

> What is meant by hedge accounting?

> What is the suggested financial statement presentation of hedge accounts recorded under the gross method? Why?

> When long-term debt hedges a revenue stream, a portion of the long-term debt becomes exposed to the risk of changes in exchange rates. Why is this?

> How does the accounting for a fair value hedge differ from the accounting for a cash flow hedge of an unrecognized firm commitment?

> Explain the application of lower of cost and net realizable value to inventory that was purchased from a foreign supplier.

> If a foreign-currency-denominated payable has been hedged, why is it necessary to adjust the liability for balance sheet purposes?

> What are some typical reasons for acquiring a forward exchange contract?

> Briefly summarize the accounting issues arising from foreign-currency-denominated transactions.

> A parent company has recently acquired a subsidiary. On the date of acquisition, both the parent and the subsidiary had unused income tax losses that were unrecognized in their financial statements. How would this affect the consolidation figures on the

> X Company recently acquired control over Y Company. On the date of acquisition, the fair values of Y Company's assets exceeded their tax bases. How does this difference affect the consolidated balance sheet?

> Explain how the revenue recognition principle supports the recognition of a portion of gains occurring on transactions between the venturer and the joint venture.

> A venturer invested non-monetary assets in the formation of a new joint venture and did not receive any monetary consideration. The fair value of the assets invested was greater than the carrying amount in the accounting records of the venturer. Explain

> The treatment of an unrealized intercompany inventory profit differs between a parent subsidiary affiliation and a venture-joint venture affiliation. Explain where the differences lie.

> Briefly outline how the presentation of assets and liabilities on the statement of financial position of a government differs from the presentation shown on the balance sheet of a typical business enterprise.

> Y Company has a 62% interest in Z Company. Are there circumstances where this would not result in Z Company being a subsidiary of Y Company? Explain.

> Explain how to account for an interest in a joint operation.

> Explain how the definitions of assets and liabilities can be used to support the consolidation of special-purpose entities.

> What is a reverse takeover, and why is such a transaction entered into?

> Explain how the use of the information provided in segment disclosures can aid in the assessment of the overall profitability of a company.

> What sort of reconciliations are required for segmented reporting?

> In accordance with IFRS 8 Operating Segments, answer the following: (a) What information must be disclosed about business carried out in other countries? (b) What information must be disclosed about a company's products or services? (c) What information

> For each of its operating segments that require separate disclosure, what information must an enterprise disclose?

> Describe the three tests for identifying reportable operating segments.

> Explain how the definition of a liability supports the recognition of a deferred income tax liability when the fair value of an asset acquired in a business combination is greater than the tax base of this asset.

> Governments are different from business organizations and NFPOs in many respects and yet in some respect they are similar. Explain.

> Explain how it is possible to have a deferred tax liability with regard to the presentation of a subsidiary's assets in a consolidated balance sheet, whereas on the subsidiary's balance sheet the same assets produce a deferred tax asset.

> What is the difference between a deductible temporary difference and a taxable temporary difference?