Question: ZIM Inc. (ZIM) is a high-technology

ZIM Inc. (ZIM) is a high-technology company that develops, designs, and manufactures telecommunications equipment. ZIM was founded in Year 5 by Dr. Alex Zimmer, the former assistant head of research and development at a major telephone company. He and the director of marketing left the company to found ZIM. ZIM has been very successful. Sales reached $8.3 million in its first year and have grown by 80% annually since then. The key to ZIM's success has been the sophisticated software contained in the equipment it sells.

ZIM's board of directors recently decided to issue shares to raise funds for strategic objectives through an initial public offering of common shares. The shares will be listed on a major Canadian stock exchange. ZIM's underwriter, Mitchell Securities, believes that an offering price of 18 to 20 times the most recent fiscal year's earnings per share can be achieved. This opinion is based on selected industry comparisons.

ZIM has announced its intention to go public, and work has begun on the preparation of a preliminary prospectus. It should be filed with the relevant securities commissions in 40 days. The offering is expected to close in about 75 days. The company has a July 31 year-end. It is now September 8, Year 8.

You, a CPA, work for Chesther Chathan, Chartered Professional Accountants, the auditors of ZIM since its inception. You have just been put in charge of ZIM's audit, due to the sudden illness of the senior. ZIM's year-end audit has just commenced. At the same time, ZIM's staff and the underwriters are working 15-hour days trying to write the prospectus, complete the required legal work, and prepare for the public offering. The client says that the audit must be completed so that the financial statements can go to the printer in 22 days. ZIM plans to hire a qualified chief financial officer as soon as possible.

An extract from ZIM's accounting records is found in Exhibit IV. You have gathered the information in Exhibit V from the client. You have been asked by the audit partner to prepare a memo dealing with the key accounting issues.

Exhibit IV:

Exhibit V:

Transcribed Image Text:

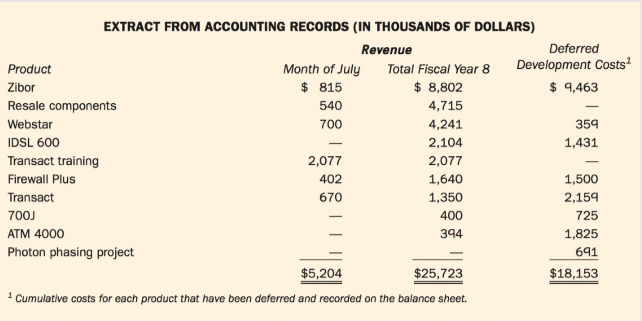

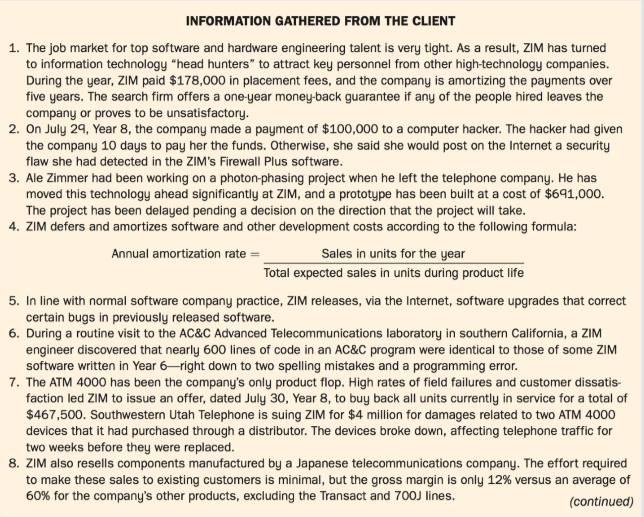

EXTRACT FROM ACCOUNTING RECORDS (IN THOUSANDS OF DOLLARS) Revenue Deferred Product Month of July Total Fiscal Year 8 Development Costs' Zibor $ 815 $ 8,802 $ 9,463 Resale components 540 4,715 Webstar 700 4,241 359 IDSL 600 2,104 1,431 Transact training 2,077 2,077 - Firewall Plus 402 1,640 1,500 Transact 670 1,350 2,159 700J 400 725 АTM 4000 394 1,825 Photon phasing project 691 $5,204 $25,723 $18,153 1 Cumulative costs for each product that have been deferred and recorded on the balance sheet. INFORMATION GATHERED FROM THE CLIENT 1. The job market for top software and hardware engineering talent is very tight. As a result, ZIM has turned to information technology “head hunters" to attract key personnel from other high-technology companies. During the year, ZIM paid $178,000 in placement fees, and the company is amortizing the payments over five years. The search firm offers a one-year money-back guarantee if any of the people hired leaves the company or proves to be unsatisfactory. 2. On July 29, Year 8, the company made a payment of $100,000 to a computer hacker. The hacker had given the company 10 days to pay her the funds. Otherwise, she said she would post on the Internet a security flaw she had detected in the ZIM's Firewall Plus software. 3. Ale Zimmer had been working on a photon-phasing project when he left the telephone company. He has moved this technology ahead significantly at ZIM, and a prototype has been built at a cost of $691,000. The project has been delayed pending a decision on the direction that the project will take. 4. ZIM defers and amortizes software and other development costs according to the following formula: Sales in units for the year Annual amortization rate Total expected sales in units during product life 5. In line with normal software company practice, ZIM releases, via the Internet, software upgrades that correct certain bugs in previously released software. 6. During a routine visit to the AC&C Advanced Telecommunications laboratory in southern California, a ZIM engineer discovered that nearly 600 lines of code in an AC&C program were identical to those of some ZIM software written in Year 6–right down to two spelling mistakes and a programming error. 7. The ATM 4000 has been the company's only product flop. High rates of field failures and customer dissatis- faction led ZIM to issue an offer, dated July 30, Year 8, to buy back all units currently in service for a total of $467,500. Southwestern Utah Telephone is suing ZIM for $4 million for damages related to two ATM 4000 devices that it had purchased through a distributor. The devices broke down, affecting telephone traffic for two weeks before they were replaced. 8. ZIM also resells components manufactured by a Japanese telecommunications company. The effort required to make these sales to existing customers is minimal, but the gross margin is only 12% versus an average of 60% for the company's other products, excluding the Transact and 700J lines. (continued) 9. During the first two years of operation, ZIM expensed all desktop computers (PCs) when purchased, on the grounds that they become obsolete so fast that their value after one year is almost negligible. In the current year, ZIM bought $429,000 worth of PCs and plans to write them off over two years. 10. Revenue is recognized on shipment for all equipment sold. Terms are FOB ZIM's shipping location. 11. ZIM's director of marketing, Albert Buzzer, has come up with a novel method of maximizing profits on the Transact product line. Transact is one of the few ZIM products that has direct competition. Transact routes telephone calls 20% faster than competing products but sells for 30% less. ZIM actually sells the product at a loss. However, without a special training course offered by ZIM, field efficiency cannot be maximized. Customers usually realize that they need the special training a couple of months after purchase. Buzzer estimates that the average telephone company will spend three dollars on training for every dollar spent on the product. Because of the way telephone companies budget and account for capital and training expendi- tures, most will not realize that they are spending three times as much on training as on the product. 12. In May Year 2, ZIM paid back a U.S. denominated, $25 million long-term debt prematurely to take advantage of a favourable interest rate. The US$25 million loan was subject to a cross-currency swap. The agreement with the third party was to pay CAN$33 million and receive US$25 million from the third party in May Year 4. This represented the exchange rate at the time the transactions were entered into. Although the swap was used to hedge the currency risk on the long-term debt, it was not formally des- ignated as a hedge for reporting purposes. The U.S. dollars exchange rate at the time of the payout was CAN$1.20. ZIM recognized the $3 million gain on the repayment of the U.S. loan. ZIM negotiated a CAN$30 million one-year loan with Beemow Bank to repay the US$25 million loan. The spot exchange rate as at January 31, Year 3, was CAN$1.27, whereas the forward exchange rate for contracts expiring in May Year 4 was CAN$1.25. 13. The IDSL equipment was sold to customers in May Year 8. In September Year, ZIM provided the custom soft- ware required to operate the IDSL 600 equipment. The software was "shipped" via the Internet.

> Three companies, A, L, and M, whose December 31, Year 5, balance sheets appear below, have agreed to combine as at January 1, Year 6. Each of the companies has a very small proportion of an intensely competitive market dominated by four much larger compa

> G Company is considering the takeover of K Company whereby it will issue 7,400 common shares for all of the outstanding shares of K Company. K Company will become a wholly owned subsidiary of G Company. Prior to the acquisition, G Company had 13,000 shar

> The trial balances for Walla Corporation and Au Inc. at December 31, Year 4, just before the transaction described below, were as follows: On December 31, Year 4, Walla purchased all of the outstanding shares of Au Inc. by issuing 20,000 common shares

> The balance sheets of A Ltd. and B Ltd. on December 30, Year 6, are as follows: On December 31, Year 6, A issued 150 common shares for all 60 outstanding common shares of B. The fair value of each of B's common shares was $40 on this date. Required:

> Z Ltd. is a public company with factories and distribution centers located throughout Canada. It has 100,000 common shares outstanding. In past years, it has reported high earnings, but in Year 5, its earnings declined substantially in part due to a loss

> The financial statements for CAP Inc. and SAP Company for the year ended December 31, Year 5, follow: On December 31, Year 5, after the above figures were prepared, CAP issued $314,000 in debt and 12,400 new shares to the owners of SAP to purchase all

> Refer to Problem 11. All of the facts and data are the same except that in the proposed takeover, Myers Company will purchase all of the outstanding common shares of Norris Inc. Required: (a) Prepare the journal entries of Myers for each of the two pro

> Myers Company Ltd. was formed 10 years ago by the issuance of 34,000 common shares to three shareholders. Four years later, the company went public and issued an additional 30,000 common shares. The management of Myers is considering a takeover in which

> Which of the reporting methods described in this chapter would typically report the highest current ratio? Briefly explain.

> The following are summarized statements of financial position of three companies as at December 31, Year3: The fair values of the identifiable assets and liabilities of the three companies as at December 31, Year 3, were as follows: On January 2, Yea

> The balance sheets of Abdul Co. and Lana Co. on June 30, Year 2, just before the transaction described below, were as follows: On June 30, Year 2, Abdul Co. purchased all of Lana Co. assets and assumed all of Lana Co. liabilities for $58,000 in cash.

> All facts are the same as in Problem 8 except that COX applies ASPE. Follow the same instructions as those given in the Required: section of Problem 8. Data from Problem 8: COX Limited is a multinational telecommunication company owned by a Canadian b

> COX Limited is a multinational telecommunication company owned by a Canadian businesswoman. It has numerous long-term investments in a wide variety of equity instruments. Some investments have to be measured at fair value at each reporting date. In turn,

> Right Company purchased 25,000 common shares (25%) of ON Inc. on January 1, Year 11, for $250,000. Right uses the eq_uity method to report its investment in ON because it has significant influence in the operating and investing decisions made by ON. Righ

> On January 1, Year 2, Grow Corp. paid $200,000 to purchase 20,000 common shares of UP Inc., which represented an 8% interest in UP. On December 27, Year 2, UP declared and paid a dividend of $0.50 per common share. During Year 2, UP reported net income o

> Her Company purchased 22,000 common shares (20%) of Him Inc. on January 1, Year 4, for $374,000. Additional information on Him for the three years ending December 31, Year 6, is as follows: On December 31, Year 6, Her sold its investment in Him for $50

> Pender Corp. paid $285,000 for a 30% interest in Saltspring Limited on January 1, Year 6. During Year 6, Saltspring paid dividends of $110,000 and reported profit as follows: Pender's profit for Year 6 consisted of $990,000 in sales, expenses of $110,0

> On January 1, Year 5, Blake Corporation purchased 25% of the outstanding common shares of Stergis Limited for $1,850,000. The following relates to Stergis since the acquisition date: Required: (a) Assume that Blake is a public company and the number of

> Baskin purchased 20,000 common shares (20%) of Robbin on January 1, Year 5, for $275,000 and classified the investment as FVTPL. Robbin reported net income of $85,000 in Year 5 and $90,000 in Year 6, and paid dividends of $40,000 in each year. Robbin's s

> Briefly describe the trend in reporting of investments in equity securities over the past 12 years.

> Harmandeep Ltd. is a private company in the pharmaceutical industry. It has been preparing its financial statements in accordance with ASPE. Since it has plans to go public in the next three to five years, it is considering changing to IFRS for the curre

> The summarized trial balances of Phase Limited and Step Limited as of December 31, Year 5, are as follows (amounts in thousands): Phase had acquired the investment in Step in three stages: The January 1, Year 2, acquisition enabled Phase to elect 3 m

> On December 31, Year 6, Ultra Software Limited purchased 70,000 common shares (70%) of a major competitor, Personal Program Corporation (PPC), at $30 per share. Several shareholders who were unwilling to sell at that time owned the remaining common share

> On January 1, Year 8, Panet Company acquired 40,000 common shares of Saffer Corporation, a public company, for $500,000. This purchase represented 8% of the outstanding shares of Saffer. It was the intention of Panet to acquire more shares in the future

> On January 1, Year 4, a Canadian firm, Canuck Enterprises Ltd., borrowed US$208,000 from a bank in Seattle, Washington. Interest of 7.5% per annum is to be paid on December 31 of each year during the four-year term of the loan. Principal is to be repaid

> The Valleytown Senior's Residential Home (Valleytown) engages in palliative care, education, and fundraising programs. The costs of each program include the costs of personnel, premises, and other expenses that are directly related to providing the progr

> The William Robertson Society is a charitable organization funded by government grants and private donations. It prepares its annual financial statements using the restricted fund method in accordance with the CPA Canada Handbook, and uses both an operat

> All facts about this NFPO are identical to those described in Problem 11, except that the deferral method of recording contributions is used for accounting and for external financial reporting. Fund accounting is not used. The Year 6 transactions are als

> The Far North Centre (the Centre) is an anti-poverty organization funded by contributions from governments and the general public. For a number of years, it has been run by a small group of permanent employees with the help of part-timers and dedicated v

> All facts about this NFPO are identical to those described in Problem 9, except that the Centre wants to use the restricted fund method of accounting for contributions. The Centre will use two separate funds--operating and capital. The capital fund will

> In Year 1, XZY Co. expensed all development costs as incurred. How would the current ratio, debt-to-equity ratio and return on equity change if XZY Co. had capitalized the development costs?

> On December 31, Year 2, PAT Inc. of Halifax acquired 90% of the voting shares of Gioco Limited of Italy, for 690,000 euros (€). On the acquisition date, the fair values equaled the carrying amounts for all of Gioco's identifiable assets

> The Ford Historical Society is an NFPO funded by government grants and private donations. It uses both an operating fund and a capital fund. The capital fund accounts for moneys received and restricted for major capital asset acquisitions. The operating

> The Brown Training Centre is a charitable organization dedicated to providing computer training to unemployed people. Individuals must apply to the center and indicate why they would like to take the three-month training session. If their application is

> All facts about this NFPO are identical to those described in Problem 5, except for the following: 1. The Society will use the restricted fund method of accounting for contributions. 2. The Society will use three separate funds for reporting purposes--

> The Fara Littlebear Society is an NFPO funded by government grants and private donations. It was established in Year 5 by the friends of Fara Littlebear to encourage and promote the work of Native Canadian artists. Fara achieved international recognition

> Protect Purple Plants (PPP) uses the deferral method of accounting for contributions and has no separate fund for restricted contributions. On January 1, Year 6, PPP received its first restricted cash contribution-$120,000 for the purchase and maintenanc

> All facts about this NFPO are identical to those described in Problem 2, except that the association wants to use the deferral method of accounting for contributions. The center will continue to use the three separate funds. Required: Prepare a stateme

> The Perch Falls Minor Hockey Association was established in Perch Falls in January Year 5. Its mandate is to promote recreational hockey in the small community of Perch Falls. With the support of the provincial government, local business people, and many

> The OPI Care Centre is an NFPO funded by government grants and private donations. It prepares its annual financial statements using the deferral method of accounting for contributions, and it uses only the operations fund to account for all activities. T

> You, CPA, are employed at Beaulieu & Beauregard, Chartered Professional Accountants. On November 20, Year 3, Dominic Jones, a partner in your firm, sends you the following email: Our firm has been reappointed auditors of Floral Impressions Ltd. (FIL)

> Identify the financial statement ratios typically used to assess profitability, liquidity and solvency, respectively.

> Foreign Infants Adoption Inc. (FIA) is a consulting company wholly owned by Roger Tremblay, a wealthy, recently retired lawyer. FIA helps Canadian families adopt infants from other countries. Typically, these infants have been abandoned or have lost thei

> Mega Communications Inc. (MCI) is a Canadian-owned public company operating throughout North America. Its core business is communications media, including newspapers, radio, television, and cable. The company's year-end is December 31. You, a CPA, have r

> RAD Communications Ltd. (RAD), a Canadian public company, recently purchased the shares of TOP Systems Inc. (TOP), a Canadian-controlled private corporation. Both companies are in the communications industry and own television, radio, and magazine and ne

> Vulcan Manufacturing Limited (VML) is a Canadian-based multinational plastics firm, with subsidiaries in several foreign countries and worldwide consolidated total assets of $500 million. VML's shares are listed on a Canadian stock exchange. VML is attra

> Long Life Enterprises was a well-€stablished Toronto-based company engaged in the importation and wholesale marketing of specialty grocery items originating in various countries of the western Pacific Rim. They had recently also entered the high-risk bus

> The Rider Corporation operates throughout Canada buying and selling widgets. In hopes of expanding into more profitable markets, the company recently decided to open a small subsidiary in California. On October 1, Year 2, Rider invested CDN$1,000,000 in

> You, CPA, have been working for Plener and Partners, Chartered Professional Accountants (P&P), a mid-size CPA firm, for three years. You have been assigned a new project for a long-term client of your firm, Oxford Developments Inc. (ODI). Information

> The United Football League (UFL), a North American professional football league, has been in work stoppage since July 1, Year 9, immediately after the six-week training camp ended. Faced with stalled negotiations, the players' union representing the leag

> Canada Cola Inc. (CCI) is a public company engaged in the manufacture and distribution of soft drinks across Canada. Its primary product is Canada Cola ("Fresh as a Canadian stream"), which is a top seller in Canada and generates large export sales. You

> For the items listed in Exhibit 1.1, for which items would the debt-to-equity ratio not change when a company switched from ASPE to IFRS? Exhibit 1.1: Accounting Item IFRS ASPE Very extensive for many items, especially financial instruments, post-e

> Interfast Corporation, a fastener manufacturer, has recently been expanding its sales through exports to foreign markets. Earlier this year, the company negotiated the sale of several thousand cases of fasteners to a wholesaler in the country of Loznia.

> Segment reporting can provide useful information for investors and competitors. Segment disclosures can result in competitive harm for the company making the disclosures. By analyzing segment information, potential competitors can identify and concentrat

> P Co. is looking for some additional financing in order to renovate one of the company's manufacturing plants. It is having difficulty getting new debt financing because its debt-to-equity ratio is higher than the 3:1limit stated in its bank covenant. It

> Mr. Landman has spent the last 10 years developing small commercial strip malls and has been very successful. He buys a residential property in a high-traffic area, rezones the property, and then sells it to a contractor who builds the plaza and sells it

> Enviro Facilities Inc. (EFl) is a large, diversified Canadian-controlled private company with several Canadian and U.S. subsidiaries, operating mainly in the waste management and disposal industry. EFl was incorporated more than 50 years ago, and has gro

> You, a CPA, have recently accepted a job at the accounting firm of Cat, Scan & Partners, as a manager, and have been assigned the audit of Vision Clothing Inc. (VCI). The partner in charge had been at VCI the previous week and had met with the contro

> Dry Quick (DQ) is a medium-sized, private manufacturing company located near Timmins, Ontario. DQ has a June 30 year-end. Your firm, Poivre & Sel (P&S), has recently been appointed as auditors for DQ. It is now August 2, Year 10. You, CPA, have b

> Traveller Bus Lines Inc. (TBL) is a wholly owned subsidiary of Canada Transport Enterprises Inc. (CTE), a publicly traded transportation and communications conglomerate. TBL is primarily in the business of operating buses over short- and long distance ro

> Identify some of the financial statement items for which ASPE is different from IFRS.

> For the past 10 years, Prince Company (Prince) has owned 75,000 or 75% of the common shares of Stiff Inc. (Stiff). Elizabeth Winer owns another 20% and the other 5% are widely held. Although Prince has the controlling interest, you would never know it du

> On December 31, Year 7, Pepper Company, a public company, agreed to a business combination with Salt Limited, an unrelated private company. Pepper issued 72 of its common shares for all (50) of the outstanding common shares of Salt 'This transaction incr

> It is Monday, September 13, Year 10. You, CPA, work at Fife & Richardson LLP, a CPA firm. Ken Simpson, one of the partners, approaches you mid-morning regarding Brennan & Sons Limited (BSL), a private company client for which you performed the Au

> Stephanie Baker is an audit senior with the public accounting firm of Wilson & Lang. It is February Year 9, and the audit of Canadian Development Limited (CDL) for the year ended December 31, Year 8, is proceeding. Stephanie has identified several transa

> On January 1, Year 4, Plum purchased 100% of the common shares of Slum. On December 31, Year 5, Slum purchased a machine for $168,000 from an external supplier. The machine had an estimated useful life of six years with no residual value. On December 31,

> In early September Year 1, your firm's audit client, D Ltd. (D) acquired in separate transactions an 80% interest in N Ltd. (N) and a 40% interest in K Ltd. (K). All three companies are federally incorporated Canadian companies and have August 31 year-en

> Enron Corporation's 2000 financial statements disclosed the following transaction with LIM2, a nonconsolidated special purpose entity (SPE) that was formed by Enron: In June 2000, LIM2 purchased dark fibre optic cable from Enron for a purchase price of

> Digital Future Technologies (DFT) is a public technology company. It has a September 30 year-end, and last year it adopted IFRS. Kin Lo is a partner with Hi & Lo, the accounting firm that was newly appointed as DFT's auditor in July for the year endi

> Wedding Planners Limited (WP), owned by Anne and Francois Tremblay, provides wedding planning and related services. WP owns a building (the Pavilion) that has been custom-made for hosting weddings. Usually, WP plans a wedding from start to finish and hos

> You, the CPA, an audit senior at Grey & Co., Chartered Professional Accountants, are in charge of this year's audit of Plex-Fame Corporation (PFC). PFC is a rapidly expanding, diversified, and publicly owned entertainment company with operations througho

> Briefly explain why a Canadian private company may decide to follow IFRS even though it could follow ASPE.

> Distinguish between unrestricted and restricted contributions of a charitable organization.

> Good Quality Auto Parts Limited (GQ) is a medium-sized, privately owned producer of auto parts, which are sold to car manufacturers, repair shops, and retail outlets. In March Year 10, the union negotiated a new three-year contract with the company for t

> You, the controller, recently had the following discussion with the president: President: I just don't understand why we can't recognize the revenue from the intercompany sale of inventory on the consolidated financial statements. The subsidiary company

> Gerry's Fabrics Ltd. (GFL), a private company, manufactures a variety of clothing for women and children and sells it to retailers across Canada. Until recently, the company has operated from the same plant since its incorporation under federal legislati

> Beaver Ridge Oilers' Players Association and Mr. Slim, the CEO of the Beaver Ridge Oilers Hockey Club (Club), ask for your help in resolving a salary dispute. Mr. Slim presents the following income statement to the player representatives: Mr. Slim argu

> Total Protection Limited (TPL) was incorporated on January 1, Year 1, by five homebuilders in central Canada to provide warranty protection for new-home buyers. Each shareholder owns a 20% interest in TPL. While most homebuilders provide one-year warrant

> It is now mid-September Year 3. Growth Investments Limited (GIL) has been owned by Sam and Ida Growth since its incorporation under the Canada Business Corporations Act many years ago. The owners, both 55 years of age, have decided to effect a corporate

> BIO Company is a private company. It employs 30 engineers and scientists who are involved with research and development of various biomedical devices. All of the engineers and scientists are highly regarded and highly paid in the field of biomedical rese

> It is September 15, Year 8. The partner has called you, CPA, into his office to discuss a special engagement related to a purchase agreement. John Toffler, a successful entrepreneur with several different businesses in the automotive sector, is finalizin

> Lauder Adventures Limited (LAL) was incorporated over 40 years ago as an amusement park and golf course. Over time, a nearby city has grown to the point where it borders on LAL's properties. In recent years LAL's owners, who are all members of one family

> When Valero Energy Corp. acquired Ultramar Diamond Shamrock Corp. (UDS) for US$6 billion, it created the second-largest refiner of petroleum products in North America, with over 23,000 employees in the United States and Canada, total assets of $10 billio

> Briefly explain why the Canadian AcSB decided to create a separate section of the CPA Canada Handbook for private enterprises.

> Factory Optical Distributors (FOD) is a publicly held manufacturer and distributor of high-quality eyeglass lenses located in Burnaby, British Columbia. For the past 10 years, the company has sold its lenses on a wholesale basis to optical shops across C

> On December 31, Year 7, Maple Company issued preferred shares with a fair value of $1,200,000 to acquire 24,000 (60%) of the common shares of Leafs Limited. The Leafs shares were trading in the market at around $40 per share just days prior to and just a

> Planet Publishing Limited (Planet) is a medium-sized, privately owned Canadian company that holds exclusive Canadian distribution rights for the publications of Typset Daily Corporation (TDC). Space Communications Ltd. (Space), an unrelated privately own

> How are translation exchange gains and losses reflected in financial statements if the foreign operation's functional currency is the Canadian dollar? Would the treatment be different if the foreign operation's functional currency were not the Canadian d

> What translation method should be used for a subsidiary that operates in a highly inflationary environment? Why?

> What difference does it make whether the foreign operation's functional currency is the same or different than the parent's presentation currency? What method of translation should be used for each?

> What should happen if a foreign subsidiary's financial statements have been prepared using accounting principles different from those used in Canada?

> Define a foreign operation as per IAS 21.

> How are gains and losses on financial instruments used to hedge the net investment in a foreign operation reported in the consolidated financial statements when the PCT method is used to translate the foreign operation?

> Explain how the acquisition cost is determined for a reverse takeover.

> Why might a company want to hedge its balance sheet exposure? What is the paradox associated with hedging balance sheet exposure?

> What are the three major issues related to the translation of foreign currency financial statements?

> Would hedge accounting be used in a situation in which the hedged item and the hedging instrument were both monetary items on a company's statement of financial position? Explain.

> If the sales of a foreign subsidiary all occurred on one day during the year, would the sales be translated at the average rate for the year or the rate on the date of the sales? Explain.

> When translating the financial statements of the subsidiary at the date of acquisition by the parent, the exchange rate on the date of acquisition is used to translate plant assets rather than the exchange rate on the date when the subsidiary acquired th

> Explain how the FCT method produces results that are consistent with the normal measurement and valuation of assets and liabilities for domestic transactions and operations.