Question: Plot the capital market line (CML), the

Plot the capital market line (CML), the nine stocks, and the three portfolios on a graph of average returns versus standard deviation. Compare the mean-variance efficiency of the three portfolios and the market index. Does the comparison support the CAPM?

> If New Fund’s expense ratio (see the previous problem) was 1.1% and the management fee was .7%, what were the total fees paid to the fund’s investment managers during the year? What were other administrative expenses?

> The New Fund had average daily assets of $2.2 billion last year. The fund sold $400 million worth of stock and purchased $500 million during the year. What was its turnover ratio?

> Consider a mutual fund with $200 million in assets at the start of the year and 10 million shares outstanding. The fund invests in a portfolio of stocks that provides dividend income at the end of the year of $2 million. The stocks included in the fund’s

> A portfolio manager at Superior Trust Company is structuring a fixed-income portfolio to meet the objectives of a client. The portfolio manager compares coupon U.S. Treasuries with zero coupon stripped U.S. Treasuries and observes a significant yield adv

> The Closed Fund is a closed-end investment company with a portfolio currently worth $200 million. It has liabilities of $3 million and 5 million shares outstanding. a. What is the NAV of the fund? b. If the fund sells for $36 per share, what is its premi

> Reconsider the Fingroup Fund in the previous problem. If during the year the portfolio manager sells all of the holdings of stock D and replaces it with 200,000 shares of stock E at $50 per share and 200,000 shares of stock F at $25 per share, what is th

> Why do call options with exercise prices greater than the price of the underlying stock sell for positive prices?

> Explain the difference between a call option and a long position in a futures contract.

> Explain the difference between a put option and a short position in a futures contract.

> Both a call and a put currently are traded on stock XYZ; both have strike prices of $50 and expirations of 6 months. What will be the profit to an investor who buys the call for $4 in the following scenarios for stock prices in 6 months? What will be the

> Why have average trade sizes declined in recent years?

> What reforms to the financial system might reduce its exposure to systemic risk?

> Look at the futures listings for the corn contract in Table 2.7. Suppose you buy one contract for March 2019 delivery. If the contract closes in March at a level of 4.06, what will your profit be?

> Why do financial assets show up as a component of household wealth, but not of national wealth? Why do financial assets still matter for the material well-being of an economy?

> Sandra Kapple is a fixed-income portfolio manager who works with large institutional clients. Kapple is meeting with Maria VanHusen, consultant to the Star Hospital Pension Plan, to discuss management of the fund’s approximately $100 mi

> Here is some price information on FinCorp stock. Suppose that FinCorp trades in a dealer market. a. Suppose you have submitted an order to your broker to buy at market. At what price will your trade be executed? b. Suppose you have submitted an order to

> Find the equivalent taxable yield of a short-term municipal bond with a yield of 4% for tax brackets of (a) zero, (b) 10%, (c) 20%, and (d) 30%.

> The average rate of return on investments in large stocks has outpaced that on investments in Treasury bills by about 8% since 1926. Why, then, does anyone invest in Treasury bills?

> An investor is in a 30% combined federal plus state tax bracket. If corporate bonds offer 6% yields, what yield must municipals offer for the investor to prefer them to corporate bonds?

> Corporate Fund started the year with a net asset value of $12.50. By year-end, its NAV equaled $12.10. The fund paid year-end distributions of income and capital gains of $1.50. What was the (pretax) rate of return to an investor in the fund?

> You are bullish on Telecom stock. The current market price is $50 per share, and you have $5,000 of your own to invest. You borrow an additional $5,000 from your broker at an interest rate of 8% per year and invest $10,000 in the stock. a. What will be y

> You are bearish on Telecom and decide to sell short 100 shares at the current market price of $50 per share. a. How much in cash or securities must you put into your brokerage account if the broker’s initial margin requirement is 50% of the value of the

> Which of the following choices best completes the following statement? Explain. An investor with a higher degree of risk aversion, compared to one with a lower degree, will most prefer investment portfolios a. with higher risk premiums. b. that are riski

> Consider the following $1,000 par value zero-coupon bonds: According to the expectations hypothesis, what is the market’s expectation of the yield curve one year from now? Specifically, what are the expected values of next yearâ&#

> a. Assuming that the expectations hypothesis is valid, compute the expected price of the 4-year bond in Problem 7 at the end of (i) the first year; (ii) the second year; (iii) the third year; (iv) the fourth year. b. What is the rate of return of the bon

> The tables below show, respectively, the characteristics of two annual-coupon bonds from the same issuer with the same priority in the event of default, as well as spot interest rates on zero coupon bonds. Neither coupon bond’s price is

> The following is a list of prices for zero-coupon bonds of various maturities. Maturity (years) Price of Bond 1……………………………… $943.40 2……………………………….. 898.47 3…………………………………847.62 4………………………………….792.16 a. Calculate the yield to maturity for a bond with a

> Assuming the pure expectations theory is correct, an upward-sloping yield curve implies: a. Interest rates are expected to increase in the future. b. Longer-term bonds are riskier than short-term bonds. c. Interest rates are expected to decline in the fu

> If the liquidity preference hypothesis is true, what shape should the term structure curve have in a period where interest rates are expected to be constant? a. Upward-sloping. b. Downward-sloping. c. Flat

> Under the liquidity preference theory, if inflation is expected to be falling over the next few years, long-term interest rates will be higher than short-term rates. True/false/uncertain? Why?

> Under the expectations hypothesis, if the yield curve is upward-sloping, the market must expect an increase in short-term interest rates. True/false/uncertain? Why?

> Consider a bond with a 10% coupon and yield to maturity = 8%. If the bond’s yield to maturity remains constant, then in one year, will the bond price be higher, lower, or unchanged? Why?

> Treasury bonds paying an 8% coupon rate with semiannual payments currently sell at par value. What coupon rate would they have to pay in order to sell at par if they paid their coupons annually? (Hint: What is the effective annual yield on the bond?)

> Which security has a higher effective annual interest rate? a. A 3-month T-bill selling at $97,645 with par value $100,000. b. A coupon bond selling at par and paying a 10% coupon semiannually.

> A bond with an annual coupon rate of 4.8% sells for $970. What is the bond’s current yield?

> The stated yield to maturity and realized compound yield to maturity of a (default-free) zerocoupon bond are always equal. Why?

> The 6-month Treasury bill spot rate is 4%, and the 1-year Treasury bill spot rate is 5%. What is the implied 6-month forward rate for six months from now?

> Which of the following most accurately describes the behavior of credit default swaps? a. When credit risk increases, swap premiums increase. b. When credit and interest rate risk increase, swap premiums increase. c. When credit risk increases, swap prem

> Suppose that today’s date is April 15. A bond with a 10% coupon paid semiannually every January 15 and July 15 is quoted as selling at an ask price of 101.25. If you buy the bond from a dealer today, what price will you pay for it?

> A 10-year bond of a firm in severe financial distress has a coupon rate of 14% and sells for $900. The firm is currently renegotiating the debt, and it appears that the lenders will allow the firm to reduce coupon payments on the bond to one-half the ori

> Two bonds have identical times to maturity and coupon rates. One is callable at 105, the other at 110. Which should have the higher yield to maturity? Why?

> A newly issued 20-year maturity, zero-coupon bond is issued with a yield to maturity of 8% and face value $1,000. Find the imputed interest income in (a) the first year; (b) the second year; and (c) the last year of the bond’s life.

> Return to Table 14.1, showing the cash flows for TIPS bonds. a. What is the nominal rate of return on the bond in year 2? b. What is the real rate of return in year 2? c. What is the nominal rate of return on the bond in year 3? d. What is the real rate

> Is the coupon rate of the bond in Problem 16 more or less than 9%?

> A bond has a current yield of 9% and a yield to maturity of 10%. Is the bond selling above or below par value? Explain.

> A bond with a coupon rate of 7% makes semiannual coupon payments on January 15 and July 15 of each year. The Wall Street Journal reports the ask price for the bond on January 30 at 100.125. What is the invoice price of the bond? The coupon period has 182

> Fill in the table below for the following zero-coupon bonds, all of which have par values of $1,000.

> The following table shows yields to maturity of zero-coupon Treasury securities. Term to Maturity (years) Yield to Maturity (%) 1……………………………………………3.50% 2………………………………………….4.50 3………………………………………….5.00 4………………………………………….5.50 5………………………………………….6.00 10………………

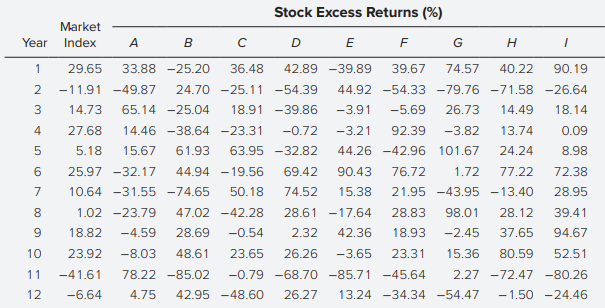

> Suppose that, in addition to the market factor that has been considered in Problems 1–7, a second factor is considered. The values of this factor for years 1 to 12 were as follows: / Perform the first-pass regressions as in the Chen, Roll, and Ross st

> Perform the second-pass SML regression by regressing the average excess return of each portfolio on its beta.

> Specify the hypotheses for the second-pass regression used to test the SML of the CAPM.

> Perform the first-pass regressions for a single-index model and tabulate the summary statistics.

> Match each example to one of the following behavioral characteristics.

> After Polly Shrum sells a stock, she avoids following it in the media. She is afraid that it may subsequently increase in price. Which behavioral characteristic is the basis for Shrum’s decision making? a. Fear of regret. b. Representativeness. c. Mental

> Jill Davis tells her broker that she does not want to sell her stocks that are below the price she paid for them. She believes that if she just holds on to them a little longer they will recover, at which time she will sell them. Which behavioral charact

> One seeming violation of the Law of One Price is the pervasive discrepancy of closed-end fund prices from their net asset values. Would you expect to observe greater discrepancies on diversified or less-diversified funds? Why?

> Using the following data, calculate the change in the confidence index from last year to this year. What besides a change in confidence might explain the pattern of yield changes?

> Briefly explain why bonds of different maturities might have different yields according to the expectations and liquidity preference hypotheses. Briefly describe the implications of each hypothesis when the yield curve is (1) upward-sloping and (2) downw

> In Table 12B, if the trading volume in advancing shares on day 1 was 530 million shares, while the volume in declining issues was 440 million shares, what was the trin statistic for that day? Was the trin bullish or bearish?

> Table 12B contains data on market advances and declines. Calculate cumulative breadth and decide whether this technical signal is bullish or bearish.

> Yesterday, the S&P 500 rose by .48%. However, 1,704 issues on the NYSE declined in price while 1,367 advanced. Why might a technical analyst be concerned even though the market index rose on this day?

> Baa-rated bonds currently yield 6%, while Aa-rated bonds yield 5%. Suppose that due to an increase in the expected inflation rate, the yields on both bonds increase by 1%. a. What would happen to the confidence index? b. Would this be interpreted as bull

> Collect data on the S&P 500 for a period covering a few months. Try to identify primary trends. Can you tell whether the market currently is in an upward or downward trend?

> Calculate breadth for the NASDAQ using the data in Figure 12.5. Is the signal bullish or bearish?

> Use the data from The Wall Street Journal in Figure 12.5 to calculate the trin ratio for the NASDAQ. Is the trin ratio bullish or bearish?

> Even if prices follow a random walk, they still may not be informationally efficient. Explain why this may be true and why it matters for the efficient allocation of capital.

> What do we mean by fundamental risk, and why may such risk allow behavioral biases to persist for long periods of time?

> Which of the following (hypothetical) observations would most contradict the proposition that the stock market is weakly efficient? Explain. a. Over 25% of mutual funds outperform the market on average. b. Insiders earn abnormal trading profits. c. Every

> a. An investment in a coupon bond will provide the investor with a return equal to the bond’s yield to maturity at the time of purchase if: i. The bond is not called for redemption at a price that exceeds its par value. ii. All sinking fund payments ar

> Steady Growth Industries has never missed a dividend payment in its 94-year history. Does this make it more attractive to you as a possible purchase for your stock portfolio?

> “If all securities are fairly priced, all must offer equal expected rates of return.” Comment.

> Good News, Inc., just announced an increase in its annual earnings, yet its stock price fell. Is there a rational explanation for this phenomenon?

> You know that firm XYZ is very poorly run. On a scale of 1 (worst) to 10 (best), you would give it a score of 3. The market consensus evaluation is that the management score is only 2. Should you buy or sell the stock?

> We know that the market should respond positively to good news and that good-news events such as the coming end of a recession can be predicted with at least some accuracy. Why, then, can we not predict that the market will go up as the economy recovers?

> In a recent closely contested lawsuit, Apex sued Bpex for patent infringement. The jury came back today with its decision. The rate of return on Apex was rA = 3.1%. The rate of return on Bpex was only rB = 2.5%. The market today responded to very encoura

> An index model regression applied to past monthly returns in Ford’s stock price produces the following estimates, which are believed to be stable over time: rF = .10% + 1.1rM If the market index subsequently rises by 8% and Ford’s stock price rises by 7

> Suppose you find that prices of stocks before large dividend increases show on average consistently positive abnormal returns. Is this a violation of the EMH?

> Which of the following statements are true if the efficient market hypothesis holds? a. It implies that future events can be forecast with perfect accuracy. b. It implies that prices reflect all available information. c. It implies that security prices c

> Suppose that, after conducting an analysis of past stock prices, you come up with the following observations. Which would appear to contradict the weak form of the efficient market hypothesis? Explain. a. The average rate of return is significantly great

> a. Explain the likely impact on the offering yield of adding a call feature to a proposed bond issue. b. Explain the likely impact on the bond’s expected life of adding a call feature to a proposed bond issue. c. Describe one advantage and one disadvanta

> Which of the following sources of market inefficiency would be most easily exploited? a. A stock price drops suddenly due to a large sale by an institution. b. A stock is overpriced because traders are restricted from short sales. c. Stocks are overvalue

> If markets are efficient, what should be the correlation coefficient between stock returns for two nonoverlapping time periods?

> Orb Trust (Orb) has historically leaned toward a passive management style of its portfolios. The only model that Orb’s senior management has promoted in the past is the capital asset pricing model (CAPM). Now Orb’s management has asked one of its analyst

> Kaskin, Inc., stock has a beta of 1.2 and Quinn, Inc., stock has a beta of .6. Which of the following statements is most accurate? a. The expected rate of return will be higher for the stock of Kaskin, Inc., than that of Quinn, Inc. b. The stock of Kaski

> What is the expected rate of return for a stock that has a beta of 1.0 if the expected return on the market is 15%? a. 15%. b. More than 15%. c. Cannot be determined without the risk-free rate.

> Here are data on two companies. The T-bill rate is 4% and the market risk premium is 6%. What would be the fair return for each company according to the capital asset pricing model (CAPM)?

> Suppose that borrowing is restricted so that the zero-beta version of the CAPM holds. The expected return on the market portfolio is 17%, and on the zero-beta portfolio it is 8%. What is the expected return on a portfolio with a beta of .6?

> Assume that the risk-free rate of interest is 6% and the expected rate of return on the market is 16%. A stock has an expected rate of return of 4%. What is its beta?

> Assume that the risk-free rate of interest is 6% and the expected rate of return on the market is 16%. A share of stock sells for $50 today. It will pay a dividend of $6 per share at the end of the year. Its beta is 1.2. What do investors expect the stoc

> If the simple CAPM is valid, which of the following situations are possible? Explain. Consider each situation independently.

> On May 30, 2020, Janice Kerr is considering one of the newly issued 10-year AAA corporate bonds shown in the following exhibit. a. Suppose that market interest rates decline by 100 basis points (i.e., 1%). Contrast the effect of this decline on the price

> Hennessy & Associates manages a $30 million equity portfolio for the multimanager Wilstead Pension Fund. Jason Jones, financial vice president of Wilstead, noted that Hennessy had rather consistently achieved the best record among Wilstead’s six equity m

> If the simple CAPM is valid, which of the following situations are possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the following situations are possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the following situations are possible? Explain. Consider each situation independently.

> What must be the beta of a portfolio with E(rP) = 18%, if rf = 6% and E(rM) = 14%?

> Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA = 3% + .7RM + eA RB = −2% + 1.2RM + eB σM = 20%; R-squareA = .20; R-squareB = .12 What is the standard deviation of each stock?

> What is the basic trade-off when departing from pure indexing in favor of an actively managed portfolio?

> Based on current dividend yields and expected growth rates, the expected rates of return on stocks A and B are 11% and 14%, respectively. The beta of stock A is .8, while that of stock B is 1.5. The T-bill rate is currently 6%, while the expected rate of

> Suppose that the index model for stocks A and B is estimated from excess returns with the following results: Rework Problem 13 for portfolio Q with investment proportions of .50 in P, .30 in the market index, and .20 in T-bills.