Question: Refer to Exhibits 6.3, 6.5,

Refer to Exhibits 6.3, 6.5, 6.7, 6.8, and 6.12.

Required:

Identify

a. An issue in respect of which the practices of several countries discussed in this chapter are at variance with IFRS.

b. The most important financial accounting practice for each of the five countries which is at variance with IFRS. Also explain the reason(s) for your selection.

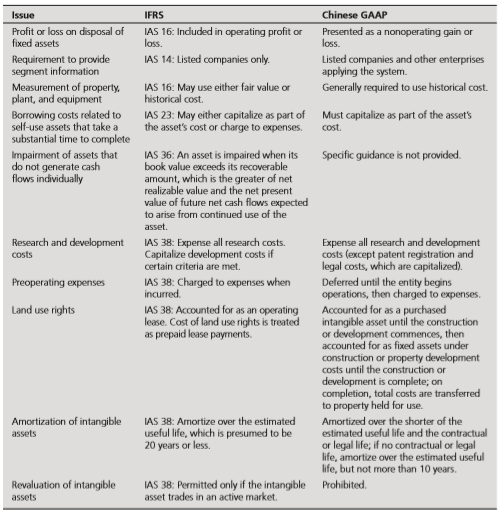

Exhibits 6.3:

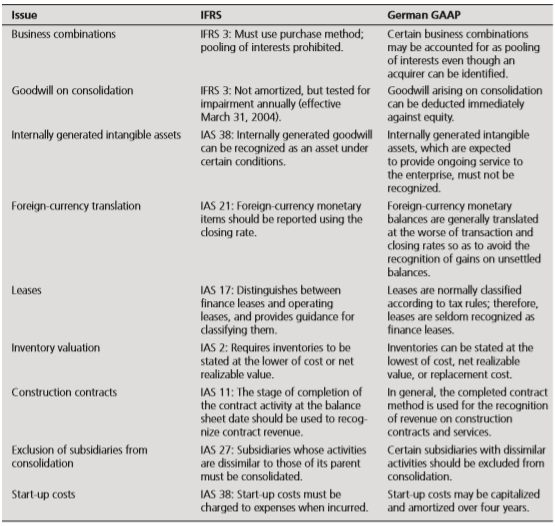

Exhibits 6.5:

Exhibits 6.7:

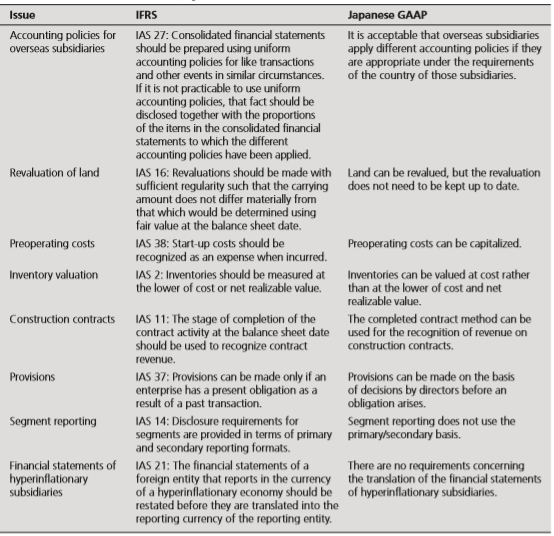

Exhibits 6.8:

Exhibits 6.12:

Transcribed Image Text:

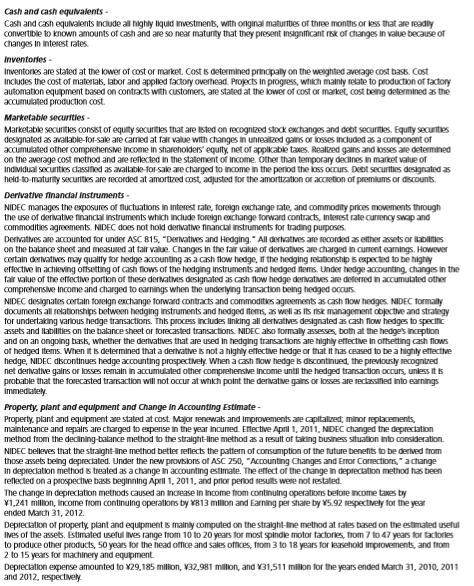

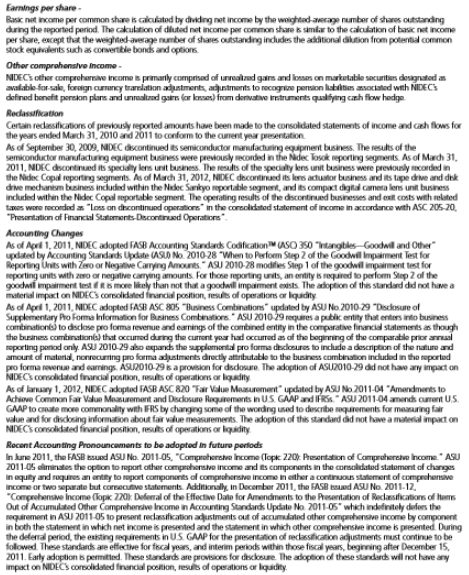

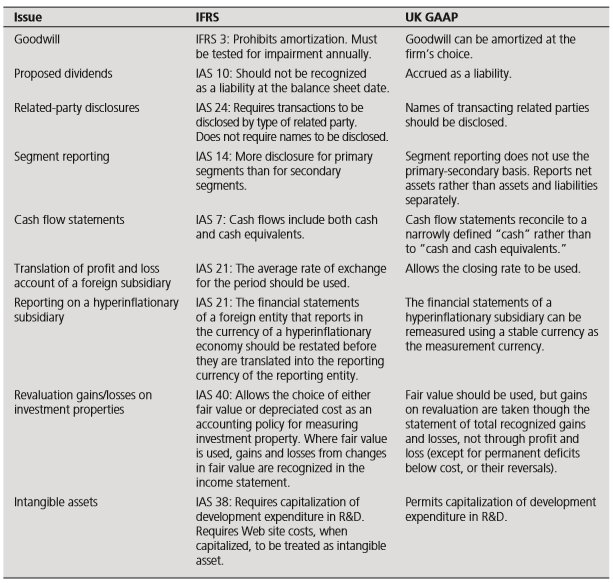

Issue IFRS Chinese GAAP Profit or loss on disposal of fixed assets IAS 16: Induded in operating profit or loss. Presented as a nonoperating gain or loss. IAS 14: Listed companies only. Requirement to provide segment information Measurement of property, plant, and equipment Listed companies and other enterprises applying the system. IAS 16: May use either fair value or historical cost. Generally required to use historical cost. Borrowing costs related to self-use assets that take a substantial time to complete IAS 23: May either capitalize as part of Must capitalize as part of the asset's the asset's cost or charge to expenses. cost. Impairment of assets that do not generate cash flows individually IAS 36: An asset is impaired when its book value exceeds its recoverable amount, which is the greater of net realizable value and the net present value of future net cash flows expected to arise from continued use of the Specific guidance is not provided. asset. Expense all research and development costs (except patent registration and legal costs, which are capitalized). Deferred until the entity begins operations, then charged to expenses. Research and development costs IAS 38: Expense all research costs. Capitalize development costs if certain criteria are met. IAS 38: Charged to expenses when incurred. IAS 38: Accounted for as an operating lease. Cost of land use rights is treated as prepaid lease payments. Preoperating expenses Land use rights Accounted for as a purchased intangible asset until the construction or development commences, then accounted for as fixed assets under construction or property development costs until the construction or development is complete; on completion, total costs are transferred to property held for use. Amortization of intangible IAS 38: Amortize over the estimated useful life, which is presumed to be 20 years or less. Amortized over the shorter of the estimated useful life and the contractual or legal life; if no contractual or legal life, amortize over the estimated useful life, but not more than 10 years. assets Revaluation of intangible IAS 38: Permitted only if the intangible asset trades in an active market. Prohibited. assets Issue IFRS German GAAP Business combinations IFRS 3: Must use purchase method; pooling of interests prohibited. Certain business combinations may be accounted for as pooling of interests even though an acquirer can be identified. Goodwill on consolidation IFRS 3: Not amortized, but tested for Goodwill arising on consolidation can be deducted immediately impairment annually (effective March 31, 2004). against equity. Internally generated Intangible assets IAS 38: Internally generated goodwill Internally generated intangible can be recognized as an asset under assets, which are expected to provide ongoing service to the enterprise, must not be certain conditions. recognized. IAS 21: Foreign-currency monetary items should be reported using the dosing rate. Foreign-currency translation Foreign-currency monetary balances are generally translated at the worse of transaction and closing rates so as to avoid the recognition of gains on unsettled balances. IAS 17: Distinguishes between finance leases and operating leases, and provides guidance for classifying them. Leases are normally dassified according to tax rules; therefore, leases are seldom recognized as finance leases. Leases Inventory valuation IAS 2: Requires inventories to be stated at the lower of cost or net realizable value. Inventories can be stated at the lowest of cost, net realizable value, or replacement cost. IAS 11: The stage of completion of the contract activity at the balance In general, the completed contract method is used for the recognition Construction contracts sheet date should be used to recog- of revenue on construction nize contract revenue. contracts and services. Exclusion of subsidiaries from consolidation IAS 27: Subsidiaries whose activities are dissimilar to those of its parent must be consolidated. Certain subsidiaries with dissimilar activities should be excluded from consolidation. Start-up costs IAS 38: Start-up costs must be charged to expenses when incurred. Start-up costs may be capitalized and amortized over four years. Issue IFRS Japanese GAAP It is acceptable that overseas subsidiaries apply different accounting policies if they are appropriate under the requirements of the country of those subsidiaries. Accounting policies for overseas subsidiaries IAS 27: Consolidated financial statements should be prepared using uniform accounting policies for like transactions and other events in similar circumstances. If it is not practicable to use uniform accounting policies, that fact should be disclosed together with the proportions of the items in the consolidated financial staternents to which the different accounting policies have been applied. Revaluation of land IAS 16: Revaluations should be made with Land can be revalued, but the revaluation sufficient regularity such that the carrying does not need to be kept up to date. amount does not differ materially from that which would be determined using fair value at the balance sheet date. IAS 38: Start-up costs should be recognized as an expense when incurred. Preoperating costs Preoperating costs can be capitalized. IAS 2: Inventories should be measured at the lower of cost or net realizable value. Inventory valuation Inventories can be valued at cost rather than at the lower of cost and net realizable value. Construction contracts IAS 11: The stage of completion of the The completed contract method can be contract activity at the balance sheet date used for the recognition of revenue on should be used to recognize contract construction contracts. revenue. IAS 37: Provisions can be made only if an Provisions can be made on the basis enterprise has a present obligation as a result of a past transaction. Provisions of decisions by directors before an obligation arises. IAS 14: Disdosure requirements for segments are provided in terms of primary primary/secondary basis. and secondary reporting formats. Segment reporting Segment reporting does not use the Financial statements of IAS 21: The financial statements of a hyperinflationary subsidiaries There are no requirements concerning foreign entity that reports in the currency the translation of the financial statements of a hyperinflationary economy should be of hyperinflationary subsidiaries. restated before they are translated into the reporting currency of the reporting entity. NIDEC CORPORATION Form F-20 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS For the fiscal yoar onded March 31, 2012 1. Nature of operations: NIDEC Corporation (the "Company") and its subsidiaries (collectively "NDEC) ae primarily engaged in the design, devalopment, manufacture and marketing of small precision motors, which include spinde motors for hard disk drives, motors for optical disk dives, small precsion fans and other small motors, i0 general motors, which are used in various electric household appliances, industrial equipment and automobies, id madchinery, which includes, test systems, measuring equipment, power transmsion equipment, factory automation systems, card readers and industrial robots, w electronic and optical components, which incude camera shuters, camera lens units, switches, trimmer potentiometers, motor driven actuator units, processing and precision plastic mold products, and v) other products, which include auto parts, pivot asemblies, other components and other services. Manufacturing operations are located primarily in Asia (China, Thailand, Vistnam and the Philippines), kapan and North America, and sakes subsidiaries are primarly located in Acia, North America and Europe. The main customers for NIDEC are manufacturors of hard disk drives. NIDEC ako salk its products to the manufacturors of varicus alkctric housahold appliances, automation aquipment, automotiva componants, home video game consoks, tekocommunication equipment and audio-visual equipmant. 2 Summary of significant accounting policles: The Company and its subsidiaries in lapan maintain their records and prepare their financial statements in accordance with accounting principles generally accepted in lapan, and its foreign subsidiaries in conformity with those of their countries of domice Certain adjustmenits and redassifications have been incorporated in the accompanying consolidated finandial statements to conform with accounting principles generally accepted in the United States of America. Significant acunting policies after reflecting adjustments for the above are as follows: Estimatos- The proparation of NDECS consolidated financial statoments in conformity with accounting principles genarally accepted in the United States of Amarica roquires management to make estimates and assumptions that affect the reported amounts of asats and labilties and contingent assets and kabilitios at the date of the financial statements, as well s the reported amounts of revers and oxperses during the reporting period. Some of the more significant estimates include the alkowance for doubtful accounts, depreciation and amortization of long-iwed assets, valation alkowance for deferred tax assets, far vale of financial instruments, uncertain tax positions, pension labilities, the recoverablity of long-lived assets and goodwill, and fair vakue of assets acquired and labilties assumed. Acthual results could differ from those estimates. Basts of consolidation and accounting for Investmonts in affifiated companies - The consoidated financial stataments include the accounts of the Company and those of its majority owned subsidiary companies All significant intarcompany trasactiors and accounts have been oliminatod. Companies over which NDEC exarcises significant influenca, but which it does not control, are dasafied as afilated companies and accounted for using the aquity method Consolidated net income includes NIDECS equity in cumrent earrings osan) of such companies, after elmination of urealized intercompany profits. On occasion, NIDEC may acquire additional shares of the voting rights of a consolidated subsidary or diposa of a part of those shares or a Nidec cosolidated subsidary may issue its shares to third parties. With espect to such transactions, all transactions for changes in a parent's ownership interest in a subsidary that do not result in the subsidary ceasing to be a subsidary are recogrized asequity tramactions. The FASB Accounting Standards Codification MASO 810, "Consolidalion" requres the consolidation or dsdosure of varable interest entities. NDEC does not hold any variable interests in a variable interest entity Translation of forolgn currancios - Non monetary asat and lablity accounts of foraign subsidiaries and affiliates are translated into lapanese yon at the your end eachange rates and all income and oxpersa acounts are trarslated at exchange rates that approsimate thoe provaling at the time of the transactions. The resulting trandation adustments are included as a component of accumulated other compreherive income in shareholders' oquty Monetary assats and lablities denominated in fornign curencies are trandated at the year-end exchange rates and the resulting transaction gains or kosses are taken into income Continued Cash and cash equivalents- Cash and cash equivalents Include all highly liquid investments, with onginal maturities of three months or less that are readly convertible to known amounts of cash and are so near maturity that they present Insignificant rsk of changes in value because of changes in interest rates. Inventories - Inventories are stated at the kower of cost or market. Cost is determined princpally on the weighted average cost bass. Cost Includes the cost of materiak, labor and applied factory overhead. Projects In progress, which mainly relate to production of factory automation equipment based on contracts with customers, are stated at the lower of cost or market, cost being determined as the accumulated production cost. Marketable securities - Marketable securities consist of equity securties that are isted on recognized stock exchanges and debt securtes. equity securities designated as avallable-for-sale are carried at far value with changes in unrealized gains or losses included as a component of accumulated other oomprehenstve Income in shareholders' equity, net of applkable taes. Realzed galns and losses are determined on the average cost method and are reflected in the statement of income. Other than temporary decines in market value of Individual securitiks dassified as avallable-for sale are charged to Income in the period the ioss occurs. Debt securties designated as held-to-maturity securities are recorded at amortized cost, adjusted for the amortzation or accietion of premlums or discounts. Derivative financdal Instruments - NIDEC manages the exposures of fluctuations in Interest rate, foreign exchange rate, and commodity prices movements through the use of derivatiMe financial instruments which include foreign exchange forward contracts, Interest rate currency swap and commodities agreements. NIDEC does not hold derivative financial instruments for trading purposes. Dervatives are accounted for under ASC 815, "Derivatives and Hedging." All dertvatives are recorded as ether assets or Ikabiites on the balance sheet and measured at fair value. Changes in the fair value of derivatives are charged in current earnings. However certain derivatives may quality for hedge accounting as a cash flow hedge, If the hedging retationship is expected to be highty effective in achieving offsetting of cash flows of the hedging instruments and hedged tems. Under hedge accounting, changes in the fair value of the effective portion of these dervatives designated as cash flow hedge derivatives are deterred in accumubated other comprehensive Income and charged to earnings when the underiying transaction being hedged occurs. NIDEC designates certain foreign exchange forward contracts and commoditics agreements as cash flow hedges. NIDEC formally documents all relationships between hedging instruments and hedged items, as well as Its rsk management objective and strategy for undertaking various hedge transactions. This process includes linking all dertvattves designated as cash flow hedges to specific assets and llabilities on the balance sheet or forecasted transactions. NIDEC aso formally assesses, both at the hedge's inception and on an ongoing bask, whether the derivatives that are used in hedging transactions are highly effective in oftsetting cash flows of hedged items. When it is determined that a derivative is not a highly effective hedge or that it has ceased to be a highly effective hedge, NIDEC discontinues hedge accounting prospectively. When a cash flow hedge is discontinued, the previously recognized net derivative galns or losses remain in accumulated other comprehensve Income until the hedged transaction occurs, unless it is probable that the forecasted transaction will not occur at which polnt the derivative gains or losses are rectzssifled Into earnings Immediately. Property, plant and equipment and Change in Accounting Estimate - Property, plant and equipment are stated at cost. Major renewats and Improvements are capitalized, minor replacements, maintenance and repairs are charged to expense in the year incured. Effective April 1, 2011, NDEC changed the deprectation method from the declining-balance method to the straight-line method as a result of taking business situation Into consideration. NIDEC belleves that the straight-line method better reflects the pattern of consumption of the future benefits to be dertved from those assets being depreciated. Under the new provisions of ASC 250, "Accounting Changes and Error Conections," achange In deprecdation method is treated as a change in accounting estimate. The effect of the change in deprectation method has been reflected on a prospective basis beginning April 1, 2011, and pror perod results were not restated. The change in depreciation methods caused an Increase in Income from continulng operations before ncome taxes by V1,241 millon, Income from continulng operations by ¥813 milion and Earning per share by ¥5.92 respectvely for the year ended March 31, 2012. Deprectation of property, plant and equipment is mainly computed on the straight-ine method at rates based on the estmaled useful Ives of the assets. Estimated useful Ives range from 10 to 20 years for most spindle motor factories, from 7 to 47 years for factornes to produce other products, 50 years for the head office and sales offices, from 3 to 18 years for leasehold improvements, and from 2 to 15 years for machinery and equipment. Deprectation expense amounted to ¥29,185 million, V32,981 millon, and V31,511 milon for the years ended March 31, 2010, 2011 and 2012, reрectму Lease NIDEC capitalizes leases and related obligations when any of the four orteria are met within the guidance of ASC 840 "Leases". Under ASC840, these leases and related obligations are capitalzed at the commencement of the lease at the lower of the far value of the leased property and the present value of the minimum lese payments. Goodwill and other Intangible assets - Goodwil and other intangitile asats are accountod for under ASC350, "Intangibikes Goodl and Other". Goodwil acquirad in business combinatikos s not amortized but tested anualy for impairment. NDEC tests for impairment at the reporting unit koval an lanuary Ist of aach yoar. In addition, NDEC tests for impairment between annual tests if an awent occurs ar drcumstances change that woukd more likely than not roduce the far value of a rmporting unit bekw ts carrying amount Thes test ka two-stop proces. The first step of the goodwill impairment test, used to identify potantial impairment, compares the fair value of the reporting unit with its carying amount, includng goodwil. f the far vakue, which is based on discounted future cash flows, ONCeds the camrying amount, goodwil is not considered impaired. If the canrying amount exceeds the fair value, the second step must be performed to measure the amount of the impairment koss, if any. The second step compares the implied fair vakue of the reporting unit's goodwill with the carrying amount of that goodwil Other intangble assets indude patent rights, proprietary techology and austomer relationships, as well as software and other intangible assets acquired in business combinations. Intangble assets with an indefinite fe are not subject to amortization and are tested for impairmerit once on lanuary 1st of each year or more frequently if an event occurs or drcumstances change. Intangible assets with a delinite Me are amortized on a straight-ine basis over their estimated uselul ives. The weighted average amortization period for patent rights, proprietary technology, austomer relatiornhips and software are 9 years, 11 yeurs, 19 yours and 5 yoars, respectively Long-lived assets - NIDEC eviews its long-ved asets for impairment whenewer events or changes in circumstances indicate that the carrying amount of an asset group may not be recoverable. An impairment kas would be recognized when the carrying amount of an aset group ONCeds the estimated undscounted futue cash flows expected to result from the use of the asset group and its eventual dspostion. The amount of the imparment koss to be recorded is calculated as the excess of the assets group's canying value over its fair value. Long-ved assets that are to be disposed of other than by sale are considered to be held and used unni the disposal. Long-ved assets tha are to be disposed of by sale are reported at the lower of their canying vale or fair value less costs to sell. Reductions in canying vakue are recogrized in the period in which long hed assets are dansfied as held for sale. Rovenue recogniion - NIDEC recogntzes rovonue when persuve evidence of an amrangement extsts, delhvery has occumad, the sales price is ftead or determinable and collectiblty is reasonably assured. For smal precksion motors, general motors and electronic and optical components, these citeria are generally met at the time a product is delvered to the Customers' site which is the time the customer has taken title to the product and the risk and rewards of ownership have been substantively transferred. These condtions are met at the time of delvery to customers in domestic sales FOB destination) and at the time of shipment for export sales FOB shipping point. Revenue for machinery sales is recognized upon receipt of final customer acceptance. At the time the related revere is recogriaed, NDEC makes provisions for estimated product returms. Rosoarch and dovalopment expenses- Research and development aperses, marly cosetng of personnel and deprecation axperses at nsaarch and dovalopment branches, are charged to operations z incumad Advertising costs - Advertising and sales promotion costs are expensed as incured. Adwertising costs were V156 milion, V246 milion, and V228 milion for the years ended March 31, 2010, 2011 and 2012, respectively. Incomo taxes - The provtion for income tas is computod basad on the protax income includad in the consoldatod statement of income. The aset and lablity approach is uned to rocognte defemad tax assats and labiltes for the axpectad future tax consaquences of tomporary difforences betwoen the carrying amounts and the tax banas of asets and lablites. Deforrod tax assets and labilties are mamuroed using enacted tax rates expected to apply to taxable income in the yoars in which thoe temporary differonces are expected to be reCovered or sotled Vakuation allowances are recorded to reduKe deferred tax assets when it is more likoly than not that a tax benefit will not be realzed. NIDEC recognizes the financial statement effects of tax positions when it is more lkaly than not, baed on the technical merits, that the tax postions will be sustained upon enamination by the tax authorities. Benefits from tax positions that meet the more-lkely- than-not recognition threshold are measured at the largest amount of benefit that is greater than 50 percent likely of being realeoed upon settlement. Interest and penalties accrued related to unrecognized tax benefies are included in other, net in the consolidated statements of income Continued Earnings per share Basic net income per common share is calculated by dviding net income by the woightad-aerage number of shares outstanding during the reported period. The cakulation of diuted net income per common share s simlar to the calculation of basic net income per share, except that the weighted-average number of shares outstanding indudes the aditional dilution from potertial common stock equivalents such as convertible bonds and options. Other comprohenslve Income - NIDECS other compreherrive income is primarly comprised of unreatad gans and lossas on marketabile sacurities designated as avalable for sak, foroign currency tradation aduntments, adjuntments to recogrize pension labilties asociated with NIDECS dofined benefit persion plans and unmaltzad gars (or kese) from dortvative irstruments qualfying czh flow hedge Redassification Certain redassifications of previously reported amounts have been made to the consoldated statements of income and cash flows for the years ended Mach 31, 2010 and 2011 to conform to the cument year presentation As of September 30, 2009, NIDEC discontinued its semiconductor manufacturing equipment business. The results of the semiconductor manufacturing equipment business were previously recorded in the Ndec Tosok reporting segments. As of March 31, 2011, NDEC dscontinued its specialty lens unit business. The results of the specialty kens unit business were previously corded in the Nidec Copal reporting segments. As of March 31, 2012, NIDEC dscontinued its lens actustor business and its tape drive and dek drive mechanism business included within the Nidec Sankyo mportable segment, and its compact digital camera lens unit business included within the Nidec Copal reportable segment. The operating results of the discontinued businesses and et costs with related tes wore recordod as "loss on drcontinund operations" in the consolidated statement of income in accordance with ASC 205-20, "Presantation of Financial Statoments-Dscontinued Operations". Accounting Changes As of Aprl 1, 2011, NIDEC adopted FASB Accounting Standards CodficationM ASO 350 htangbles Goodwil and Other" updated by Accounting Standards Update ASUO No 2010-28 "When to Perform Step 2 of the Goodwill Impairment Test for Reporting Units with Zwo or Negative Carrying Amounts." ASU 2010-28 modifies Siep 1 of the goodwill impairment test for reporting units with zero or negative carying amounts. For those reporting units, an entity is required to perfom Step 2 of the goodwil mpairment test fR more likely than not that a goodwill mpament exists. The adoption of this standard did not have a material impact on NIDECS consolidated financial position, resuts of operations or liquidity As of April 1, 2011, NIDEC adopted FASB ASC 805 "Business Combinations" updated by ASU No. 2010-29 "Discosure of Supplementary Pro Foma Information for Business Combinations. ASU 2010 29 requires a pubikc entity that enters into business combinationsi to dsclose pro forma revenue and earnings of the combined entity in the comparative financial statements as though the buraness combinatione that occumed during the curent yoar had occured as of the beginning of the Comparabile prior annsal reporting poriod anly. ASU 2010-29 abo xpands the supplamental pro forma dsclosures to include a description of the nature and amount of material, nonrecuting pro forma adustments drectly attributable to the business combination induded in the reportad pro forma revenue and earmings. ASU2010-29 s a provision for dsdosure. The adoption of ASU2010-29 dd not have any impact on NIDECS consolidated francial position, suts of operations or liquidity As of lanuary 1, 2012, NIDEC adopted FASB ASC 820 "Far Value Maasurement" updatod by ASU No 2011-04 "Amendments to Achieve Common Far Value Measurement and Dsclosure Roqurements in US. GAAP and IFRSS." ASU 2011-04 amends current U.S. GAAP to cate more commonality with IFRS by changing some of the wordng used to describe requrements for measuring fair value and for discosing information about far value measurements. The adoption of this standard did not have a material mpact on NIDECS consolidated firancial position, resuts of operations or liquidity Rocont Accounting Pronouncomants to be adopted in future peorfods In June 2011, the FASB sund ASU No. 2011-05, "Comprahershva Income (Topkc 220: Presentation of Compraherstve Income." ASU 2011-05 aliminates the option to report other comprshenstve income and its components in the consolidatod statement of changes in aquity and roquires an antity to roport components of comprehensive income in either a continuous statement of comprehensave Income or two separate but cormecutive statements. Addinkonally in December 2011, the FASB bued ASU No. 2011-12, "Comprehensive Income (lopik 220: Deferal of the Effective Dato for Amendments to the Presentatikon of Recdasifications of homs Out of Accumulated Other Compreherive Income in Accounting Standards Update No. 2011-05" which indefinitoly defers the requirement in ASU 2011-05 to present redasification adustments out of accumulated other comprehensve income by component in both the statement in which net income is presented and the statement in which other comprehensive income is presented During the deferral period, the existing equirements in U.S. GAAP for the presentation of recassification adjustments must continue to be followed. These standards are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2011. Early adoption is permitted. These standards are provtsions for discksure. The adoption of these standards will not have any impact on NIDECS corsolidated financial position, results of operations or liquidity. In September 2011, the FASB issued ASU No. 2011-08, "Intangibles-Goodwill and Other (Topic 350): Testing Goodwill for Impairment." ASU 2011-08 allows an entity the option of performing a qualitative assessment before calculating the fair value of a reporting unit. If an entity determines, on the basis of qualitative factors, that the fair value of the reporting unit is more likely than not less than the carrying amount, the two-step impairment test would be required. ASU 2011-08 is effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. Early adoption is permitted. NIDEC is currently evaluating the potential impact of adopting ASU 2011-08 on its consolidated financial position, results of operations or liquidity. Issue IFRS UK GAAP Goodwill IFRS 3: Prohibits amortization. Must Goodwill can be amortized at the be tested for impairment annually. IAS 10: Should not be recognized as a liability at the balance sheet date. firm's choice. Proposed dividends Accrued as a liability. Related-party disclosures IAS 24: Requires transactions to be disclosed by type of related party. Does not require names to be disclosed. Names of transacting related parties should be disclosed. Segment reporting IAS 14: More disclosure for primary segments than for secondary segments. Segment reporting does not use the primary-secondary basis. Reports net assets rather than assets and liabilities separately. Cash flow statements IAS 7: Cash flows include both cash Cash flow statements reconcile to a narrowly defined “cash“ rather than to "cash and cash equivalents." and cash equivalents. Translation of profit and loss account of a foreign subsidiary IAS 21: The average rate of exchange Allows the closing rate to be used. for the period should be used. Reporting on a hyperinflationary IAS 21: The financial statements of a foreign entity that reports in the currency of a hyperinflationary economy should be restated before they are translated into the reporting currency of the reporting entity. The financial statements of a subsidiary hyperinflationary subsidiary can be remeasured using a stable currency as the measurement currency. Revaluation gains/losses on investment properties IAS 40: Allows the choice of either Fair value should be used, but gains on revaluation are taken though the statement of total recognized gains fair value or depreciated cost as an accounting policy for measuring investment property. Where fair value and losses, not through profit and is used, gains and losses from changes loss (except for permanent deficits in fair value are recognized in the income statement. below cost, or their reversals). Permits capitalization of development expenditure in R&D. Intangible assets IAS 38: Requires capitalization of development expenditure in R&D. Requires Web site costs, when capitalized, to be treated as intangible asset.

> 5.1 A decrease in the marginal propensity to import will _________ the multiplier for investment spending. 5.2. The _________ is positive because consumers import more goods and services as income rises. 5.3. Use the income-expenditure graph to illustr

> 3.1. In our simple model, if C = 100 + 0.8y, and I = 50, equilibrium output will be _________. 3.2. If in Exercise 3.1 I increase to 100, a. the equilibrium income will be _________. b. the multiplier is _________. 3.3. The slope of the consumption fu

> 4.1. Suppose the supply of labor increases. Draw a graph to show how potential output and wages change. 4.2. Draw a graph to show how potential output and wages change when the stock of capital decreases. 4.3. Full-employment output is the level of out

> A.1. Find the Multiplier. An economy has a marginal propensity to consume (b) of 0.6 and a marginal propensity to import (m) of 0.2. What is the multiplier for government spending for this economy? A.2. The Effects of Taxes and Spending. Suppose the eco

> 1.1. To decrease aggregate demand, a government can either decrease spending or _________ taxes. 1.2. Fiscal policy refers to the _________ and _________ policies used by the government to influence the economy. 1.3. If the multiplier for taxation is &

> 2.1. Fiscal year 2015 began on October 1, _________. 2.2. Corporate taxes are the largest component of federal revenue. _________ (True/False) 2.3. Federal spending consists of _________ and _________. 2.4. The largest category of federal spending is

> 3.1. _________ was the first president to consciously use fiscal policy to stabilize the economy. 3.2. Since both taxes and government spending increased in the United States during the 1930s, there was __________ (large/little/no) net fiscal expansion.

> 3.1. The __________ depicts the relationship between the level of prices and the total quantity of goods and services that firms supply. 3.2. A decrease in material costs will shift the short-run aggregate supply __________. 3.3. The aggregate supply c

> 2.1. Which of the following is not a component of aggregate demand? a. Consumption b. Investment c. Government expenditures d. The supply of money e. Net exports 2.2. When we draw the aggregate demand curve, __________ should be on the x-axis and _

> 1.1. Arthur Okun distinguished between auction prices, which changed rapidly, and __________ prices, which are slow to change. 1.2 Auction prices are prices that adjust __________, while custom prices are prices that adjust __________. 1.3 The price sy

> 4.1. Suppose the supply of money increases, causing output to exceed full employment. Prices will __________ and real GDP will __________ in the short run, and prices will __________ and real GDP will __________ in the long run. 4.2. Consider a decrease

> 5.1. For each of the following pairs of population groups, indicate which group has a higher poverty rate: a. white vs. Hispanic b. white vs. Asian c. married couple vs. femaleheaded ho

> 3.1. A patent increases the incentive to develop new products because it the price of the product and thus generates profit to cover a firm’s costs of . 3.2. In some cases, a patent is socially inefficient because it merely

> 1.1. The firm-specific demand curve shows the relationship between the charged by the firm and the by the firm. 1.2. Consumers do not have a strong preference for the output of one seller over that of another in a market because the firms sell a standar

> 3.1. The key region of the brain for the valuation of benefits is the . 3.2. In the dopamine learning system, learning happens when the about the pleasure from a product are (correct/wrong). 3.3. The key region of the brain for the valuation of costs is

> 1.1. To compute the price elasticity of demand, we divide the percentage change in _________ by the percentage change in _________ and then take the value of the ratio. 1.2. If a 10 percent increase in price decreases the quantity demanded by 12 percent

> 1.1. The dollar against the euro when the European central bank lowers interest rates. 1.2. If the dollar appreciates against the euro, then the euro also against the dollar. 1.3. The price of one country’s currency in terms of another country’s curren

> 4.1. Professors Don _________ and Franco _________ developed the adjustment-process model used in this chapter. 4.2. Keynes’s objection to Say’s law was that it is possible for demand to create its own supply. _________ (True/ False) 4.3. Economists wh

> A.1. ____________ and ____________ are the two factors that determine how the stock of capital changes over time. A.2. Which of the following causes capital deepening to come to an end? a. The marginal principle b. The principle of diminishing returns

> 1.1. The income-expenditure model is most appropriate for long-run analysis. _________ (True/False) 1.2. Equilibrium output occurs when real output equals planned expenditures. _________ (True/False) 1.3. In our most basic model of the economy, the onl

> 2.1. Arrows up or down: An increase in the wage the opportunity cost of leisure time, which tends to leisure time and labor time. 2.2. Arrows up or down: An increase in the wage real income, and if leisure is a normal good

> 4.1. Government transfer and tax policies increase the income share of the lowest quintile of the income distribution from about percent to about percent. 4.2. The college premium is defined as the percentage difference be

> 1.1. The marginal revenue product of labor equals times . 1.2. A profit-maximizing firm will hire the number of workers where equals . 1.3. Your favorite professional team is considering hiring a new player for $3 mil

> 3.1. Arrows up or down: A decrease in the supply of nurses will the equilibrium wage and the equilibrium quantity of nursing services. 3.2. Arrows up or down: An increase in the demand for nursing services will the equilibrium wage and

> 3.1. Compared to a pollution tax, a uniform-abatement policy is (more/less) efficient because it does not exploit differences in across firms. 3.2. The “command” part of a command-and-control pollution policy specifies a f

> 1.1. The optimal level of pollution abatement is the level at which the of abatement equals the of abatement. 1.2. The marginal cost of abatement typically (increases/decreases) with the level of abatement. 1.3. The

> 2.1. The private cost of production includes the amount a firm pays for , , and . 2.2. The external cost of production is the cost incurred by . 2.3. The social cost of production equals the cost plus the c

> 4.1. Under a system of marketable pollution permits, a firm with (low/high) abatement costs will buy permits from a firm with (low/high) abatement costs. 4.2. Arrow up or down: A switch from regular pollution permits to marketable perm

> 3.1. According to the model of voting developed in the chapter, the choices made by the government match the preferences of the voter. 3.2. The self-interest theory of government explains why many states have limits on and . 3.3

> 4.1. Who developed the theory of scale of the market? a. Joseph Schumpeter b. Milton Friedman c. Adam Smith d. John Maynard Keynes 4.2. The notion that innovation is promoted by the competitive desire to break production monopolies is known as creat

> 6.1. When the economy operates at full employment, an increase in government spending must crowd out consumption. __________ (True/False) 6.2. A(n) __________ economy is open to trade, whereas a closed economy is not. 6.3. In an open economy, increases

> What are the differences in accounting for a forward contract used as a fair value hedge of (a) a foreign-currency-denominated asset or liability and (b) a foreign currency firm commitment?

> What are the differences in accounting for a forward contract used as (a) a cash flow hedge and (b) a fair value hedge of a foreign-currency-denominated asset or liability?

> Buch Corporation purchased Machine Z at the beginning of Year 1 at a cost of $100,000. The machine is used in the production of Product X. The machine is expected to have a useful life of 10 years and no residual value. The straight line method of deprec

> What is the concept underlying the two-transaction perspective to accounting for foreign currency transactions?

> On August 1, Year 1, Huntington Corporation placed an order to purchase merchandise from a foreign supplier at a price of 100,000 dinars. The merchandise is received and paid for on October 31, Year 1, and is fully consumed by December 31, Year 1. On Aug

> On October 1, Year 1, Butterworth Company entered into a forward contract to sell 100,000 rupees in four months (on January 31, Year 2). Relevant exchange rates for the rupee are as follows: Butterworth Company’s incremental borrowing

> Artco Inc. engages in various transactions with companies in the country of Santrica. On November 30, Year 1, Artco sold artwork at a price of 400,000 ricas to a Santrican customer, with payment to be received on January 31, Year 2. In addition, on Novem

> On November 1, Year 1, Alexandria Company sold merchandise to a foreign customer for 100,000 francs with payment to be received on April 30, Year 2. At the date of sale, Alexandria Company entered into a six-month forward contract to sell 100,000 francs.

> The same facts apply as in Exercise 14 except that Budvar Company purchases parts from a foreign supplier on December 1, Year 1, with payment of 20,000 crowns to be made on March 1, Year 2. On December 1, Year 1, Budvar enters into a forward contract to

> The Budvar Company sells parts to a foreign customer on December 1, Year 1, with payment of 20,000 crowns to be received on March 1, Year 2. Budvar enters into a forward contract on December 1, Year 1, to sell 20,000 crowns on March 1, Year 2

> Beech Corporation has three finished products (related to three different product lines) in its ending inventory at December 31, Year 1. The following table provides additional information about each product: Beech Corporation expects to incur sellin

> On September 30, Year 1, the Lester Company negotiated a two-year loan of 1,000,000 markkas from a foreign bank at an interest rate of 2 percent per annum. Interest payments are made annually on September 30, and the principal will be repaid on September

> On December 1, Year 1, El Primero Company purchases inventory from a foreign supplier for 40,000 coronas. Payment will be made in 90 days after El Primero has sold this merchandise. Sales are made rather quickly, and El Primero pays this entire obligatio

> Garden Grove Corporation made a sale to a foreign customer on September 15, Year 1, for 100,000 foreign currency units (FCU). Payment was received on October 15, Year 1. The following exchange rates apply: Date……………………………………U.S. Dollar per FCU September

> The process of professionalization of accounting in China has been unique. Required: Discuss the unique features of professionalization of accounting in China.

> Zorba Company, a U.S.-based importer of specialty olive oil, placed an order with a foreign supplier for 500 cases of olive oil at a price of 100 crowns per case. The total purchase price is 50,000 crowns. Relevant exchange rates are as follows: Zorba

> “In 2012, there were major reforms affecting accounting and financial reporting in the United Kingdom.” Do you agree? Explain.

> This chapter describes the mechanisms in place to regulate accounting and financial reporting in five countries. Required: Compare and contrast these mechanisms in the United Kingdom and China.

> Refer to the IASB Web site (www.iasb.org.uk). Required: a. Determine the manner in which IFRS are used in each of the five countries included in this chapter. b. Determine which of these countries has a resident who is a member of the IASB.

> Chapter 1 identified and described six major reasons for accounting diversity: legal system, taxation, providers of financing, inflation, political and economic ties, and culture. Required: a. Which factor or factors appear to have exerted the greatest

> How does a foreign currency option differ from a foreign currency forward contract?

> The number of professional accountants in a country indicates the status of the accounting profession in that country. Required: Determine the number of accountants per 100,000 of population in the United Kingdom and Japan. Explain why the numbers are s

> The NAFTA agreement has had a major impact on accounting and financial reporting by Mexican companies. Required: Discuss the nature of the impact referred to in the preceding statement.

> The JICPA has taken a number of positive steps toward convergence between Japanese GAAP and IFRS. Required: Explain the steps taken by the JICPA in this regard.

> Refer to Exhibits 6.3, 6.7, and 6.9. Required: Explain the main areas you would focus on in comparing financial statements prepared by companies in China, Japan, and Mexico with those prepared by companies using IFRS. Exhibits 6.3: Exhibits 6.7:

> The financial reporting issues facing Mexico are different in some respects from those of other countries covered in this chapter. Required: Provide two main reasons to support the above statement.

> China Petroleum and Chemical Corporation (CPCC) is one of a growing number of Chinese companies that has cross-listed its stock on foreign stock exchanges. To provide information that might be useful for a wide audience of readers outside of China, CPCC

> The Act of 2010 to modernize German accounting reflects a willingness to change as well as retain traditional German accounting practices. Required: Do you agree with the preceding statement? Explain.

> This chapter describes the major changes that have been introduced recently in Germany and Japan in the area of accounting regulation. Required: Describe any similarities between those changes in Germany and Japan.

> Indicate whether each of the following describes an accounting treatment that is acceptable under IFRS, U.S. GAAP, both, or neither by checking the appropriate box. Acceptable Under U.S. GAAP Both Neither IFRS • Bank overdrafts are netted against c

> This problem consists of two parts. Part A. On January 1, Year 1, Stone Company issued 100 stock options with an exercise price of $38 each to 10 employees (1,000 options in total). The employees can choose to settle the options either (a) in shares of

> Under what conditions can hedge accounting be used to account for a foreign currency option used to hedge a forecasted foreign currency transaction?

> The Campolino Company has a defined benefit post-retirement health-care plan for its employees. To fund the plan, Campolino makes an annual cash contribution to a health-care benefit fund on December 31 of each year. At the beginning of Year 5, Campolino

> n December 1, Year 1, Traylor Company sells $100,000 of short-term trade receivables to Main Street Bank for $98,000 in cash by guaranteeing to buy back the first $15,000 of defaulted receivables. Traylor’s historic rate of non collection on receivables

> On November 1, Year 1, Farley Corporation sells receivables due in six months with a carrying amount of $100,000 to Town Square Bank for a cash payment of $95,000, subject to full recourse. Under the right of recourse, Farley Corporation is obligated to

> Five years ago, Macro Arco Corporation (MAC) borrowed $12 million from Friendly Neighbor Bank (FNB) to finance the purchase of a new factory to be able to meet an expected increase in demand for its products. The expected increase in demand never materia

> On January 1, Year 1, Tempe extinguishes $10 million of 10 percent bonds payable due December 31, Year 2, that were originally issued at a discount by calling them at par value. The current carrying amount of the bonds payable is $9,950,000. To finance t

> The Bockster Company issues $20 million of preferred shares on January 1, Year 1, at par value. The preferred shares have a 5 percent fixed annual cash dividend. Part A. The preferred shareholders have the option to redeem the preferred shares for cash e

> A. Harrington Company is a U.S.-based company that prepares its consolidated financial statements in accordance with U.S. GAAP. The company reported income in 2015 of $5,000,000 and stockholders’ equity at December 31, 2015, of $40,000,000. T he CFO of S

> On January 1, Year 1, Spectrum Fabricators Inc. issues $20 million of convertible bonds at par value. The bonds have a stated annual interest rate of 6 percent, pay interest annually, and come due December 31, Year 5. The bonds are convertible at any tim

> Saffron Enterprises Inc., a U.S.-based company, purchases a 4 percent bond denominated in euros for $1,500 on January 1, Year 1, when the exchange rate is $1.50 per euro. (In other words, the purchase price was 1,000 euros.) The bond was purchased at par

> Phil’s Sandwich Company sells sandwiches at several locations in the northeastern part of the country. Phil’s customers receive a card on their first visit that allows them to receive one free sandwich for every eight sandwiches purchased in a three-mont

> What is hedge accounting?

> Cypress Company enters into a fixed-fee contract to provide architectural services to the Gervais Group for $240,000. The Gervais Group, which will make monthly payments of $40,000, is a new client for Cypress Company. Cypress has agreed to provide Gerva

> he Miller-Porter Company sells powder coating equipment at a sales price of $50,000 per unit. The sales price includes delivery, installation, and initial testing of the equipment, as well as a monthly service call for one year in which a technician chec

> Ultima Company offers its customers discounts to purchase goods and take title before they actually need the goods. The company offers to hold the goods for the customers until they request delivery. This relieves the customers from making room in their

> Mishima Technologies Company introduced Product X to the market on December 1. The new product carries a one-year warranty. In its first month on the market, Mishima sold 1,000 units of the new product for a total of $1,000,000. Customers have an uncondi

> Gotti Manufacturing Inc., a U.S.-based company, operates in three countries in addition to the United States. The following table reports the company’s pretax income and the applicable tax rate in these countries for the year ended Dece

> Updike and Patterson Investments Inc. (UPI) holds equity investments with a cost basis of $250,000. UPI accounts for these investments as available-for sale securities. As such, the investments are carried on the balance sheet at fair value, with unreali

> SC Masterpiece Inc. granted 1,000 stock options to certain sales employees on January 1, Year 1. The options vest at the end of three years (cliff vesting) but are conditional upon selling 20,000 cases of barbecue sauce over the three-year service period

> Bessrawl Corporation is a U.S.-based company that prepares its consolidated financial statements in accordance with U.S. GAAP. The company reported income in 2014 of $1,000,000 and stockholders’ equity at December 31, 2014, of $8,000,000. The CFO of Bess

> On January 2, Year 1, Argy Company’s board of directors granted 12,000 stock options to a select group of senior employees. The requisite service period is three years, with one-third of the options vesting at the end of each calendar year (graded vestin

> White River Company has a defined benefit pension plan in which the fair value of plan assets (FVPA) exceeds the present value of defined benefit obligations (PVDBO). The following information is available at December 31, Year 1 (amounts in millions):

> In what way has the development of accounting and auditing in China differed from that in other countries?

> T he Baton Rouge Company compiled the following information for the current year related to its defined benefit pension plan: Present value of defined benefit obligation, beginning of year……………………..$1,000,000 Fair value of plan assets, beginning of year…

> In January 1, Year 1, the Hoverman Corporation made amendments to its defined benefit pension plan, resulting in $150,000 of past service costs. The plan has 100 active employees with an average expected remaining working life of 10 years. There currentl

> The Kissel Trucking Company Inc. has a defined benefit pension plan for its employees. At December 31, Year 1, the following information is available regarding Kissel’s plan: Fair value of plan assets……………………………………………………$30,000,000 Present value of defi

> T he board of directors of Chestnut Inc. approved a restructuring plan on November 1, Year 1. On December 1, Year 1, Chestnut publicly announced its plan to close a manufacturing division in New Jersey and move it to China, and the company’s New Jersey e

> On June 1, Year 1, Charley Horse Company entered into a contract with Good Feed Company to purchase 1,000 bales of organic hay on January 30, Year 2, at a price of $30 per bale. The hay will be grown especially for Charley Horse and is needed to feed the

> In Year 1, Better Sleep Company began to receive complaints from physicians that patients were experiencing unexpected side effects from the company’s sleep apnea drug. The company took the drug off the market near the end of Year 1. During Year 2, the c

> On January 1, Year 1, an entity acquires a new machine with an estimated useful life of 20 years for $100,000. The machine has an electrical motor that must be replaced every fi ve years at an estimated cost of $20,000. Continued operation of the machine

> Iptat International Ltd. provided the following reconciliation from IFRS to U.S. GAAP in its most recent annual report (amounts in thousands of CHF): Required: a. Explain why U.S. GAAP adjustment (a) results in an addition to net income. Explain why U

> With its broad portfolio of market-leading businesses, the Jardine Matheson Group is an Asian-based conglomerate with extensive experience in the region. Its business interests include Jardine Pacific, Jardine Motors Group, Hongkong Land, Dairy Farm, Man

> Madison Company acquired a depreciable asset at the beginning of Year 1 at a cost of $12 million. At December 31, Year 1, Madison gathered the following information related to this asset: Carrying amount (net of accumulated depreciation) ……………………………$10

> Briefly describe the current requirement for companies in Mexico to account for the effect of inflation in their annual financial statements.

> Jefferson Company acquired equipment on January 2, Year 1, at a cost of $10 million. The equipment has a five-year life, no residual value, and is depreciated on a straight-line basis. On January 2, Year 3, Jefferson Company determines the fair value of

> Godfrey Company constructed a new, highly automated chemical plant in Year 1, which began production on January 1, Year 2. The cost to construct the plant was $5,000,000: $1,500,000 for the building and $3,500,000 for machinery and equipment. The useful

> Quick Company acquired a piece of equipment in Year 1 at a cost of $100,000. The equipment has a 10-year estimated life, zero salvage value, and is depreciated on a straight-line basis. Technological innovations take place in the industry in which the co

> Stevenson Corporation acquires a one-year-old building at a cost of $500,000 at the beginning of Year 2. The building has an estimated useful life of 50 years. However, based on reliable historical data, the company believes the carpeting will need to be