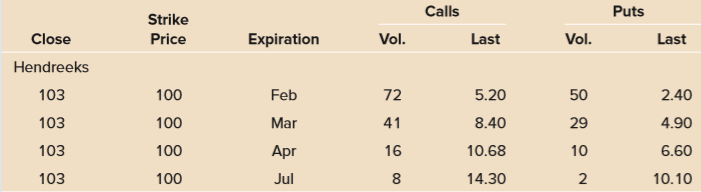

Question: Suppose you write 30 of the July

Suppose you write 30 of the July 100 put contracts. What is your net gain or loss if Hendreeks is selling for $90 at expiration? For $110? What is the break-even price, that is, the terminal stock price that results in a zero profit?

Transcribed Image Text:

Calls Puts Strike Price Close Expiration Vol. Last Vol. Last Hendreeks 103 100 Feb 72 5.20 50 2.40 103 100 Mar 41 8.40 29 4.90 103 100 Apr 16 10.68 10 6.60 103 100 Jul 8 14.30 10.10

> Many health care companies depend on patents to sustain profits. In the context of Porter’s five forces, how would a patent expiration impact a health care firm?

> Why do you think that consumer sentiment is considered a leading economic indicator?

> Which sector would be more sensitive to the business cycle: industrials or health care?

> Briefly explain the process of top-down analysis.

> If you are a U.S. investor who believes the Australian dollar is going to appreciate, would that make you more or less likely to invest in Australian stocks?

> If the economy was in recession, what monetary policies might the Fed employ?

> What is the impact on a bond’s coupon rate from, a. A call feature? b. A put feature?

> What is a put bond? Is the put feature desirable from the investor’s perspective? The issuer’s?

> With regard to the call feature, what are call protection and the call premium? What typically happens to the call premium through time?

> You own stock in a company that has just initiated employee stock options. How do the employee stock options benefit you as a shareholder?

> What is the difference between a revenue bond and a general obligation bond?

> What are the key differences between T-bills and T-bonds?

> One thing the put-call parity equation tells us is that given any three of a stock, a call, a put, and a T-bill, the fourth can be synthesized or replicated using the other three. For example, how can we replicate a share of stock using a put, a call, an

> In the context of the standard cash flow statement, what is operating cash flow?

> Why do we say depreciation is a “noncash item”?

> What is the relationship between net income and earnings per share (EPS)?

> Which is larger, gross margin or operating margin? Can either be negative? Can both?

> In general, employee stock options cannot be sold to another party. How do you think this affects the value of an employee stock option compared to a market-traded option?

> What makes current assets and liabilities “current”? Are operating assets “current”?

> What is the difference between the “retained earnings” number on the income statement and that on the balance sheet?

> What is vesting in regard to employee stock options? Why would a company use a vesting schedule with employee stock options?

> You notice that shares of stock in the Patel Corporation are going for $50 per share. Call options with an exercise price of $35 per share are selling for $10. What’s wrong here? Describe how you could take advantage of this mispricing if the option expi

> What is the intrinsic value of a put option? How do we interpret this value?

> What is the intrinsic value of a call option? How do we interpret this value?

> Buying a put option on a stock you own is sometimes called “stock price insurance.” Why?

> What is the impact of an increase in the volatility of the underlying stock on an option’s value? Explain.

> What are the 10K and 10Q reports? By whom are they filed? What do they contain? With whom are they filed? What is the easiest way to retrieve one?

> What are the six factors that determine an option’s price?

> Suppose you write 10 call option contracts with a $50 strike. The premium is $2.75. Evaluate your potential gains and losses at option expiration for stock prices of $40, $50, and $60.

> You can also create a butterfly spread using puts by buying a put at K1, buying a put at K3, and selling two puts at K2. All of the puts are on the same stock and have the same expiration date, and the assumption that K2 = ½(K1 + K3) still holds. Puts on

> In Problem 16, what is the single monthly mortality for seasoned 50 PSA, 200 PSA, and 400 PSA mortgages? How do you interpret these numbers? Data from Problem 16: What are the conditional prepayment rates for seasoned 50 PSA, 200 PSA, and 400 PSA mortg

> What does an option’s delta tell us? Suppose a call option with a delta of 0.60 sells for $5.00. If the stock price rises by $1, what will happen to the call’s value?

> What are the conditional prepayment rates for seasoned 50 PSA, 200 PSA, and 400 PSA mortgages if the 100 PSA benchmark is 3 percent per year? How do you interpret these numbers?

> Suppose you write 15 put option contracts with a $45 strike. The premium is $2.40. Evaluate your potential gains and losses at option expiration for stock prices of $35, $45, and $55.

> Immediately after establishing your put options hedge, volatility for LLL stock suddenly jumps to 45 percent. This changes the number of put options required to hedge your employee stock options. How many put option contracts are now required?

> Suppose you hold LLL employee stock options representing options to buy 10,000 shares of LLL stock. You wish to hedge your position by buying put options with three-month expirations and a $22.50 strike price. How many put option contracts are required?

> In Problem 13, what would the total return be if the ending exchange rate were 88.65 ¥ / $? What does your answer tell you about the importance of currency fluctuations? Data from Problem 13: Suppose you are a U.S. investor who is planning to invest $1

> Based on Problems 14 and 15, what is the projected stock price assuming a 10 percent increase in sales? Kiwi Fruit Company Balance Sheet Cash and equivalents ……………………………………$ 570 Operating assets ………………………………………………..650 Property, plant, and equipment. …

> Following the examples in the chapter, prepare a pro forma income statement, balance sheet, and cash flow statement for Kiwi Fruit assuming a 10 percent increase in sales. Kiwi Fruit Company Balance Sheet Cash and equivalents ……………………………………$ 570 Operat

> Calculate the price-book, price-earnings, and price-cash flow ratios for Kiwi Fruit. Kiwi Fruit Company Balance Sheet Cash and equivalents ……………………………………$ 570 Operating assets ………………………………………………..650 Property, plant, and equipment. …………………….2,700 Othe

> One year has passed and Sands’s common equity price has increased to $58 per share. Name the two components of the convertible bond’s value. Indicate whether the value of each component should increase, stay the same, or decrease in response to the incre

> Determine whether the value of a callable convertible bond will increase, decrease, or remain unchanged if there is an increase in stock price volatility. What if there is an increase in interest rate volatility? Justify each of your responses.

> What is the time value of a call option? Of a put option? What happens to the time value of a call option as the maturity increases? What about a put option?

> In Problem 19, suppose the firm was operating at only 90 percent capacity in 2017. What is EFN now? Data from Problem 19: The most recent financial statements for Moose Tours, Inc., follow. Sales for 2017 are projected to grow by 15 percent. Interest e

> The most recent financial statements for Moose Tours, Inc., follow. Sales for 2017 are projected to grow by 15 percent. Interest expense will remain constant; the tax rate and the dividend payout rate will also remain constant. Costs, other expenses, cur

> For the company in Problem 17, suppose fixed assets are $420,000 and sales are projected to grow to $695,000. How much in new fixed assets is required to support this growth in sales? Data from Problem 17: Thorpe Mfg., Inc., is currently operating at o

> A stock with a current price of $78 has a call option available with a strike price of $80. The stock will move up by a factor of 0.95 or down by a factor of 0.80 each period for the next two periods and the risk-free rate is 3.5 percent. What is the pri

> A stock is currently priced at $35 and will move up by a factor of 1.18 or down by a factor of 0.85 each period over each of the next two periods. The risk-free rate of interest is 3 percent. What is the value of a put option with a strike price of $40?

> A stock is currently selling for $60. Over the next two periods, the stock will move up by a factor of 1.15 or down by a factor of 0.87 each period. A call option with a strike price of $60 is available. If the risk-free rate of interest is 3.2 percent p

> The most recent financial statements for Bradley, Inc., are shown here (assuming no income taxes): Assets and costs are proportional to sales. Debt and equity are not. No dividends are paid. Next year’s sales are projected to be $6,24

> Stock in Cheezy-Poofs Manufacturing is currently priced at $50 per share. A call option with a $50 strike and 90 days to maturity is quoted at $1.95. Compare the percentage gains and losses from a $97,500 investment in the stock versus the option in 90 d

> Given the following information for Smashville, Inc., construct an income statement for the year: Cost of goods sold: ………………………………….$164,000 Investment income: ……………………………………$1,200 Net sales: ………………………………………………..$318,000 Operating expense: …………………………………

> How do interest rates affect option prices? Explain.

> A 30-year, $250,000 mortgage has a rate of 5.4 percent. What are the interest and principal portions in the first payment? In the second?

> A stock with a current price of $58 has a put option available with a strike price of $55. The stock will move up by a factor of 1.13 or down by a factor of 0.88 over the next period and the risk-free rate is 3 percent. What is the price of the put optio

> The Federal Reserve announces an offering of Treasury bills with a face value of $60 billion. Noncompetitive bids are made for $8 billion, along with the following competitive bids: In a single-price auction, which bids are accepted and what prices are

> The most recent financial statements for Martin, Inc., are shown here: Assets and costs are proportional to sales. Debt and equity are not. A dividend of $850 was paid, and Martin wishes to maintain a constant payout ratio. Next year’

> Suppose you have a stock market portfolio with a beta of 1.15 that is currently worth $300 million. You wish to hedge against a decline using index options. Describe how you might do so with puts and calls. Suppose you decide to use SPX calls. Calculate

> A convertible bond has a 5 percent coupon, paid semiannually, and will mature in 10 years. If the bond were not convertible, it would be priced to yield 4 percent. The conversion ratio on the bond is 25 and the stock is currently selling for $49 per shar

> A call option is currently selling for $3. It has a strike price of $65 and six months to maturity. What is the price of a put option with a $65 strike price and six months to maturity? The current stock price is $66 and the risk-free interest rate is 5

> Mr. Johnson asks Mr. Wall to compute the value of the call option. Using the given information, what is the value of the embedded call option? a. $0.00 b. $1.21 c. $2.04

> Mr. Blanda instructs Mr. Houston to calculate the weighted average coupon rate (WAC) for the mortgage pools. Which of the following is closest to the WAC? a. 7.28 percent b. 7.78 percent c. 8.01 percent

> Mr. Wall believes he understands the relationship between interest rates and straight bonds but is unclear how callable bonds change as interest rates increase. How do prices of callable bonds react to an increase in interest rates? The price: a. Increas

> What happens to the stock price when the stock pays a dividend? What impact does a dividend have on the prices of call and put options?

> If VirtualCon had decided to slow its payment of accounts payable by 90 days instead of entering into a financing arrangement with the bank, what would be the impact on its operating cash flow (CFO) and financing cash flow (CFF) during the 90 days relati

> Mr. Wall is a little confused over the relationship between the embedded option and the callable bond. How does the value of the embedded call option change when interest rate volatility increases? a. It increases. b. It may increase or decrease. c. It d

> Mortgage pools also suffer from defaults. Explain how defaults are handled in a fully modified mortgage pool. In the case of a fully modified mortgage pool, explain why defaults appear as prepayments to the mortgage pool investor.

> Evaluate the following argument: “Prepayment is not a risk to mortgage investors because prepayment actually means that the investor is paid both in full and ahead of schedule.” Is the statement always true or false?

> What are some of the reasons that mortgages are paid off early? Under what circumstances are mortgage prepayments likely to rise sharply? Explain.

> Why is Macaulay duration an inadequate measure of interest rate risk for an MBS? Why is effective duration a better measure of interest rate risk for an MBS?

> Explain in general terms how a protected amortization class (or PAC) CMO works.

> Consider a single whole bond sequential CMO. It has two tranches, an A-tranche and a Z-tranche. Explain how the payments are allocated to the two tranches. Which tranche is riskier?

> Which has greater interest rate risk, an IO or a PO strip?

> What is a collateralized mortgage obligation? Why do they exist? What are three popular types?

> In general, if you buy a call option, what stock price is needed for you to break even on the transaction ignoring taxes and commissions? If you buy a put option?

> What is a collateralized mortgage obligation? Why do they exist? What are three popular types?

> If you believed inflation was going to increase over the coming years, would you rather invest in short-term or long-term debt?

> Briefly explain why a high level of national debt may be detrimental for economic growth.

> Two callable bonds are essentially identical, except that one has a refunding provision while the other has no refunding provision. Which bond is more likely to be called by the issuer? Why?

> All else the same, callable bonds have less interest rate sensitivity than non callable bonds. Why? Is this a good thing?

> Explain the difference between an original-issue junk bond and a fallen angel bond.

> What are some examples of embedded options in bonds? How do they affect the price of a bond?

> From the bondholder’s perspective, what are the potential advantages and disadvantages of floating coupons?

> For a callable Treasury bond selling above par, is it necessarily true that the yield to call will be less than the yield to maturity? Why or why not?

> Treasury and municipal yields are often compared to calculate critical tax rates. What concerns might you have about such a comparison? What do you think is true about the calculated tax rate?

> Complete the following sentence for each of these investors: a. A buyer of call options. b. A buyer of put options. c. A seller (writer) of call options. d. A seller (writer) of put options. The (buyer/seller) of a (put/call) option (pays/receives) money

> From an investor’s standpoint, what are the main differences between Treasury and municipal issues?

> From an investor’s standpoint, what are the key differences between Treasury and agency issues?

> What is a bond refunding? Is it the same thing as a call?

> What is the difference between gross margin and operating margin? What do they tell us? Generally speaking, are larger or smaller values better?

> Both ROA and ROE measure profitability. Which one is more useful for comparing two companies? Why?

> Why do you think most long-term financial planning begins with sales forecasts? Put differently, why are future sales the key input?

> A put and a call option have the same maturity and strike price. If both are at the money, which is worth more? Prove your answer and then provide an intuitive explanation.

> Recall the option strategies of a protective put and covered call discussed in the text. Suppose you have sold short some shares of stock. Discuss analogous option strategies and how you would implement them. (Hint: They’re called protective calls and co

> A put and a call option have the same maturity and strike price. If they also have the same price, which one is in the money?

> Are the put options in the money? What is the intrinsic value of a Milson Corp. put option? Calls Puts Option & Strike N.Y. Close Price Expiration Vol. Last Vol. Last Milson 59 55 Mar 98 3.50 66 1.06 59 55 Apr 54 6.25 40 1.94 59 55 Jul 25 8.63 17 3.

> Are the call options in the money? What is the intrinsic value of a Milson Corp. call option? Calls Puts Option & Strike N.Y. Close Price Expiration Vol. Last Vol. Last Milson 59 55 Mar 98 3.50 66 1.06 59 55 Apr 54 6.25 40 1.94 59 55 Jul 25 8.63 17

> How many option contracts on Milson stock were traded with an expiration date of July? How many underlying shares of stock do these option contracts represent? Calls Puts Option & Strike N.Y. Close Price Expiration Vol. Last Vol. Last Milson 59 55 M

> Regarding Ms. Smith’s and Mr. Van Eaton’s statements made about the competitive strategy of the South Winery: a. Both are incorrect. b. Both are correct. c. Only one is correct.

> Two of the options are clearly mispriced. Which ones? At a minimum, what should the mispriced options sell for? Explain how you could profit from the mispricing in each case. Calls Puts Option & Strike N.Y. Close Price Expiration Vol. Last Vol. Last