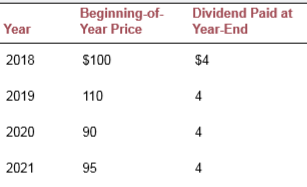

Question: XYZ stock price and dividend history are

XYZ stock price and dividend history are as follows:

An investor buys three shares of XYZ at the beginning of 2018, buys another two shares at the beginning of 2019, sells one share at the beginning of 2020, and sells all four remaining shares at the beginning of 2021

a. What are the arithmetic and geometric average time-weighted rates of return for the investor? b. What is the dollar-weighted rate of return? (Hint: Carefully prepare a chart of cash flows for the four dates corresponding to the turns of the year for January 1, 2018, to January 1, 2021. If your calculator cannot calculate internal rate of return, you will have to use a spreadsheet or trial and error.)

> In Problem below, assume the risk-free rate is 8% and the expected rate of return on the market is 18%. Use the SML of the simple (one-factor) CAPM to answer this question. A stock has an expected return of 6%. What is its beta?

> Assume that both X and Y are well-diversified portfolios and the risk-free rate is 8%. In this situation you could conclude that portfolios X and Y: a. Are in equilibrium. b. Offer an arbitrage opportunity. c. Are both underpriced. d. Are both fairly

> Which of the following statements about the standard deviation is/are true? A standard deviation: a. Is the square root of the variance. b. Is denominated in the same units as the original data. c. Can be a positive or a negative number.

> In Problem below, assume the risk-free rate is 8% and the expected rate of return on the market is 18%. Use the SML of the simple (one-factor) CAPM to answer this question. I am buying a firm with an expected perpetual cash flow of $1,000 but am unsure o

> In Problem below, assume the risk-free rate is 8% and the expected rate of return on the market is 18%. Use the SML of the simple (one-factor) CAPM to answer this question. A share of stock is now selling for $100. It will pay a dividend of $9 per share

> Go to Connect and link to Chapter 7 materials, where you will find a spreadsheet with monthly returns for GM, Ford, Toyota, the S&P 500, and Treasury bills. a. Estimate the index model for each firm over the full five-year period. Compare the betas of e

> Consider the statement: “If we can identify a portfolio with a higher Sharpe ratio than the S&P 500 Index portfolio, then we should reject the single-index CAPM.” Do you agree or disagree? Explain.

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> Which of the following statements about the security market line (SML) are true? a. The SML provides a benchmark for evaluating expected investment performance. b. The SML leads all investors to invest in the same portfolio of risky assets. c. The SML

> If the simple CAPM is valid, which of the situations in Problem below is possible? Explain. Consider each situation independently.

> Consider the following table, which gives a security analyst’s expected return on two stocks and the market index in two scenarios: a. What are the betas of the two stocks? b. What is the expected rate of return on each stock? c. If t

> You are a consultant to a large manufacturing corporation considering a project with the following net after-tax cash flows (in millions of dollars): The project’s beta is 1.7. Assuming rf = 9% and E(rM) = 19%, what is the net present v

> The market price of a security is $40. Its expected rate of return is 13%. The risk-free rate is 7%, and the market risk premium is 8%. What will the market price of the security be if its beta doubles (and all other variables remain unchanged)? Assume t

> Suppose investors believe that the standard deviation of the market-index portfolio has increased by 50%. What does the CAPM imply about the effect of this change on the required rate of return on Google’s investment projects?

> A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a Tbill money market fund that yields a sure rate of 5.5%. The probability distributions o

> A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a Tbill money market fund that yields a sure rate of 5.5%. The probability distributions o

> Use the rate-of-return data for the stock and bond funds presented in Spreadsheet 6.1, but now assume that the probability of each scenario is as follows: severe recession: .10; mild recession: .20; normal growth: .35; boom: .35. a. Would you expect the

> Suppose that the returns on the stock fund presented in Spreadsheet 6.1 were −40%, −14%, 17%, and 33% in the four scenarios. a. Would you expect the mean return and variance of the stock fund to be more than, less than, or equal to the values computed i

> The standard deviation of the market index portfolio is 20%. Stock A has a beta of 1.5 and a residual standard deviation of 30%. a. What would make for a larger increase in the stock’s variance: an increase of 0.15 in its beta or an increase of 3% (from

> Dudley Trudy, CFA, recently met with one of his clients. Trudy typically invests in a master list of 30 equities drawn from several industries. As the meeting concluded, the client made the following statement: “I trust your stock-picking ability and bel

> An investor ponders various allocations to the optimal risky portfolio and risk-free T-bills to construct his complete portfolio. How would the Sharpe ratio of the complete portfolio be affected by this choice?

> A portfolio’s expected return is 12%, its standard deviation is 20%, and the risk-free rate is 4%. Which of the following would make for the greatest increase in the portfolio’s Sharpe ratio? a. An increase of 1% in expected return. b. A decrease of 1%

> Neighborhood Insurance sells fire insurance policies to local homeowners. The premium is $110, the probability of a fire is .001, and in the event of a fire, the insured damages (the payout on the policy) will be $100,000. a. Make a table of the two pos

> Log in to Connect to find rate-of-return data over a 60-month period for Alphabet, the parent company of Google; the T-bill rate; and the S&P 500, which we will use as the market index portfolio. a. Use these data and Excel’s regression function to comp

> Here are rates of return for six months for Generic Risk, Inc. What is Generic’s beta? (Hint: Find the answer by plotting the scatter diagram.

> Log in to Connect and link to the material for Chapter 6, where you will find a spreadsheet containing monthly rates of return for Apple, the S&P 500, and T-bills over a recent five-year period. Set up a spreadsheet just like that of Example 6.3 and find

> The following figure shows plots of monthly rates of return and the stock market for two stocks. a. Which stock is riskier to an investor currently holding a diversified portfolio of common stock? b. Which stock is riskier to an undiversified investor w

> Investors expect the market rate of return this year to be 10%. The expected rate of return on a stock with a beta of 1.2 is currently 12%. If the market return this year turns out to be 8%, how would you revise your expectation of the rate of return on

> When adding a risky asset to a portfolio of many risky assets, which property of the asset has a greater influence on risk: its standard deviation or its covariance with the other assets? Explain.

> A project has a 0.7 chance of doubling your investment in a year and a 0.3 chance of halving your investment in a year. What is the standard deviation of the rate of return on this investment?

> Hennessy & Associates manages a $30 million equity portfolio for the multimanager Wilstead Pension Fund. Jason Jones, financial vice president of Wilstead, noted that Hennessy had rather consistently achieved the best record among the Winsted’s six equit

> What is the relationship of the portfolio standard deviation to the weighted average of the standard deviations of the component assets?

> Your assistant gives you the following diagram as the efficient frontier of the group of stocks you asked him to analyze. The diagram looks a bit odd, but your assistant insists he double-checked his analysis. Would you trust him? Is it possible to get s

> Assume expected returns and standard deviations for all securities, as well as the riskfree rate for lending and borrowing, are known. Will investors necessarily arrive at the same optimal risky portfolio? Explain.

> You can find a spreadsheet containing annual returns on stocks and Treasury bonds in Connect. Copy the data for the last 20 years into a new spreadsheet. Analyze the risk-return trade-off that would have characterized portfolios constructed from large st

> Suppose that many stocks are traded in the market and that it is possible to borrow at the risk free rate, rf. The characteristics of two of the stocks are as follows: Could the equilibrium rf be greater than 10%? (Hint: Can a particular stock portfolio

> Stocks offer an expected rate of return of 10% with a standard deviation of 20%, and gold offers an expected return of 5% with a standard deviation of 25%. a. In light of the apparent inferiority of gold to stocks with respect to both mean return and vo

> A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a Tbill money market fund that yields a sure rate of 5.5%. The probability distributions o

> A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a Tbill money market fund that yields a sure rate of 5.5%. The probability distributions o

> A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a Tbill money market fund that yields a sure rate of 5.5%. The probability distributions o

> In forming a portfolio of two risky assets, what must be true of the correlation coefficient between their returns if there are to be gains from diversification? Explain.

> Hennessy & Associates manages a $30 million equity portfolio for the multimanager Wilstead Pension Fund. Jason Jones, financial vice president of Wilstead, noted that Hennessy had rather consistently achieved the best record among the Winsted’s six equit

> Using the historical risk premiums as your guide, what is your estimate of the expected annual HPR on the market index stock portfolio if the current risk-free interest rate is 3%?

> a. Suppose you forecast that the standard deviation of the market return will be 20% in the coming year. If the measure of risk aversion in Equation 5.16 is A = 4, what would be a reasonable guess for the expected market risk premium? b. What value of A

> The stock of Business Adventures sells for $40 a share. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows: a. Calculate the expected holding-period return and standard deviation of the

> Suppose your expectations regarding the stock market are as follows: Use Equations 5.10–5.12 to compute the mean and standard deviation of the HPR on stocks

> You’ve just decided upon your capital allocation for the next year, when you realize that you’ve underestimated both the expected return and the standard deviation of your risky portfolio by a multiple of 1.05. Will you increase, decrease, or leave uncha

> When estimating a Sharpe ratio, would it make sense to use the average excess real return that accounts for inflation?

> Download the annual returns for the years 1927–2018 on the combined market index (of the NYSE/NASDAQ/AMEX markets) as well as the S&P 500 from Connect. For both indexes, calculate: a. Average return. b. Standard deviation of return. c. Skew of return.

> For each style portfolio, are real or nominal returns more volatile during each subperiod of Table 5.5?

> Convert the nominal returns on the broad market index to real rates. Reproduce the last column of Table 5.3 using real rates. Compare the results to those of Table 5.3. Are real or nominal returns more volatile in this sample period?

> Hennessy & Associates manages a $30 million equity portfolio for the multimanager Wilstead Pension Fund. Jason Jones, financial vice president of Wilstead, noted that Hennessy had rather consistently achieved the best record among the Winsted’s six equit

> Calculate the means and standard deviations of the four style indices in Table 5.4 (e.g., Big/Small, Value/Growth) for the same sub periods as in Table 5.5. a. Have Small/Growth stocks provided consistently better reward-to-volatility (Sharpe) ratios th

> The real interest rate approximately equals the nominal rate minus the inflation rate. Suppose the inflation rate increases from 3% to 5%. Does the Fisher equation imply that this increase will result in a fall in the real rate of interest? Explain.

> What is the reward-to-volatility (Sharpe) ratio for the equity fund in the previous problem?

> You manage an equity fund with an expected risk premium of 10% and a standard deviation of 14%. The rate on Treasury bills is 6%. Your client chooses to invest $60,000 of her portfolio in your equity fund and $40,000 in a T-bill money market fund. What a

> What do you think would happen to the expected return on stocks if investors perceived an increase in the volatility of stocks?

> Your client (see previous problem) wonders whether to switch the 70% that is invested in your fund to the index portfolio. a. Explain to your client the disadvantage of the switch. b. Show your client the maximum fee you could charge (as a percent of t

> You estimate that a passive portfolio invested to mimic the S&P 500 stock index provides an expected rate of return of 13% with a standard deviation of 25%. a. Draw the CML and your fund’s CAL on an expected return/standard deviation diagram. b. What i

> Suppose the same client as in the previous problem prefers to invest in your portfolio a proportion (y) that maximizes the expected return on the overall portfolio subject to the constraint that the overall portfolio’s standard deviation will not exceed

> Suppose the same client in the previous problem decides to invest in your risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 15%. a. What is the proportion y? b. What ar

> Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. a. What are the expected return and standard deviation of your client’s portfolio? b. Suppose your risky portfolio includes the follo

> Abigail Grace has a $900,000 fully diversified portfolio. She subsequently inherits ABC Company common stock worth $100,000. Her financial adviser provided her with the following estimates: The correlation coefficient of ABC stock returns with the origin

> Consider a risky portfolio. The end-of-year cash flow derived from the portfolio will be either $50,000 or $150,000, with equal probabilities of 0.5. The alternative riskless investment in T-bills pays 5%. a. If you require a risk premium of 10%, how mu

> What has been the historical average real rate of return on stocks, Treasury bonds, and Treasury bills?

> Suppose you’ve estimated that the fifth-percentile value at risk of a portfolio is −30%. Now you wish to estimate the portfolio’s first-percentile VaR (the value below which lie 1% of the returns). Will the 1% VaR be greater or less than −30%?

> What are some comparative advantages of investing your assets in the following: (LO 4-2) a. Unit investment trusts. b. Open-end mutual funds. c. Individual stocks and bonds that you choose for yourself.

> Balanced funds and asset allocation funds each invest in both the stock and bond markets. What is the difference between these types of funds?

> Would you expect a typical open-end fixed-income mutual fund to have higher or lower operating expenses than a fixed-income unit investment trust? Why?

> What are some differences between hedge funds and mutual funds?

> What are the advantages and disadvantages of exchange-traded funds versus mutual funds?

> What are some differences between a unit investment trust and a closed-end fund?

> What is a 12b-1 fee?

> George Stephenson’s current portfolio of $2 million is invested as follows: Stephenson soon expects to receive an additional $2 million and plans to invest the entire amount in an exchange-traded fund that best complements the current p

> The Investments Fund sells Class A shares with a front-end load of 6% and Class B shares with 12b1 fees of 0.5% annually as well as back-end load fees that start at 5% and fall by 1% for each full year the investor holds the portfolio (until the fifth ye

> You purchased 1,000 shares of the New Fund at a price of $20 per share at the beginning of the year. You paid a front-end load of 4%. The securities in which the fund invests increase in value by 12% during the year. The fund’s expense ratio is 1.2%. Wha

> The New Fund (from Problem 22) had an expense ratio of 1.1%, and its management fee was 0.7%. a. What were the total fees paid to the fund’s investment managers during the year? b. What were the other administrative expenses?

> The New Fund had average daily assets of $2.2 billion in the past year. The fund sold $400 million and purchased $500 million worth of stock during the year. What was its turnover ratio?

> Consider a mutual fund with $200 million in assets at the start of the year and with 10 million shares outstanding. The fund invests in a portfolio of stocks that provides dividend income at the end of the year of $2 million. The stocks included in the f

> a. Impressive Fund had excellent investment performance last year, with portfolio returns that placed it in the top 10% of all funds with the same investment policy. Do you expect it to be a top performer next year? Why or why not? b. Suppose instead th

> Why can closed-end funds sell at prices that differ from net value while open-end funds do not?

> City Street Fund has a portfolio of $450 million and liabilities of $10 million. a. If there are 44 million shares outstanding, what is the net asset value? b. If a large investor redeems 1 million shares, what happens to the portfolio value, to shares

> Loaded-Up Fund charges a 12b-1 fee of 1% and maintains an expense ratio of .75%. Economy Fund charges a front-end load of 2%, but has no 12b-1 fee and has an expense ratio of .25%. Assume the rate of return on both funds’ portfolios (before any fees) is

> A closed-end fund starts the year with a net asset value of $12. By year-end, NAV equals $12.10. At the beginning of the year, the fund is selling at a 2% premium to NAV. By the end of the year, the fund is selling at a 7% discount to NAV. The fund paid

> A three-asset portfolio has the following characteristics: What is the expected return on this three-asset portfolio?

> Corporate Fund started the year with a net asset value of $12.50. By year-end, its NAV equaled $12.10. The fund paid year-end distributions of income and capital gains of $1.50. What was the rate of return to an investor in the fund?

> The Closed Fund is a closed-end investment company with a portfolio currently worth $200 million. It has liabilities of $3 million and 5 million shares outstanding. a. What is the NAV of the fund? b. If the fund sells for $36 per share, what is its pre

> Reconsider the Fingroup Fund in the previous problem. If during the year the portfolio manager sells all of the holdings of stock D and replaces it with 200,000 shares of stock E at $50 per share and 200,000 shares of stock F at $25 per share, what is th

> The composition of the Fingroup Fund portfolio is as follows: The fund has not borrowed any funds, but its accrued management fee with the portfolio manager currently totals $30,000. There are 4 million shares outstanding. What is the net asset value of

> If the offering price of an open-end fund is $12.30 per share and the fund is sold with a front-end load of 5%, what is its net asset value?

> An open-end fund has a net asset value of $10.70 per share. It is sold with a front-end load of 6%. What is the offering price?

> Open-end equity mutual funds commonly keep a small fraction of total investments in very liquid money market assets. Closed-end funds do not have to maintain such a position in “cashequivalent” securities. What difference between open-end and closed-end

> What are the benefits to small investors of investing via mutual funds? What are the disadvantages?

> How does buying on margin magnify both the upside potential and downside risk of an investment portfolio?

> What is the role of an underwriter? A prospectus?