Question: Nature’s Elixir Corporation operates three

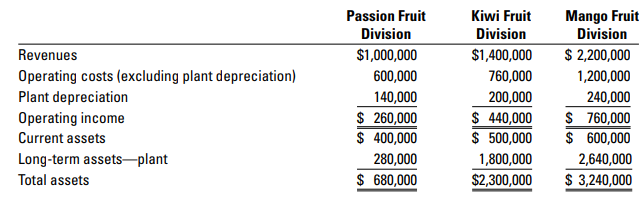

Nature’s Elixir Corporation operates three divisions that process and bottle natural fruit juices. The historical-cost accounting system reports the following information for 2015:

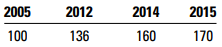

Nature’s Elixir estimates the useful life of each plant to be 12 years, with no terminal disposal value. The straight-line depreciation method is used. At the end of 2015, the Passion Fruit plant is 10 years old, the Kiwi Fruit plant is 3 years old, and the Mango Fruit plant is 1 year old. An index of construction costs over the 10-year period that Nature’s Elixir has been operating (2005 year-end = 100) is

Given the high turnover of current assets, management believes that the historical-cost and current-cost measures of current assets are approximately the same.

Required:

1. Compute the ROI ratio (operating income to total assets) of each division using historical-cost measures. Comment on the results.

2. Use the approach into compute the ROI of each division, incorporating current-cost estimates as of 2015 for depreciation expense and long-term assets. Comment on the results.

3. What advantages might arise from using current-cost asset measures as compared with historical cost measures for evaluating the performance of the managers of the three divisions?

Transcribed Image Text:

Passion Fruit Kiwi Fruit Mango Fruit Division Division Division Revenues $1,000,000 $1,400,000 $ 2,200,000 Operating costs (excluding plant depreciation) Plant depreciation 600,000 760,000 1,200,000 140,000 $ 260,000 $ 400,000 200,000 240,000 $ 440,000 $ 500,000 1,800,000 $2,300,000 $ 760,000 $ 600,000 2,640,000 $ 3,240,000 Operating income Current assets Long-term assets-plant 280,000 Total assets $ 680,000 2005 2012 2014 2015 100 136 160 170

> The outstanding capital stock of Edna Millay Corporation consists of 2,000 shares of $100 par value, 8% preferred, and 5,000 shares of $50 par value common. Instructions Assuming that the company has retained earnings of $90,000, all of which is to be

> Presented below is information from the annual report of Emporia Plastics, Inc. Instructions a. Compute the return on common stockholders’ equity and the rate of interest paid on bonds. (Assume balances for debt and equity accounts a

> Kathleen Battle Corporation was organized on January 1, 2017. It is authorized to issue 10,000 shares of 8%, $100 par value preferred stock, and 500,000 shares of no-par common stock with a stated value of $1 per share. The following stock transactions w

> Shown below is the liabilities and stockholders’ equity section of the balance sheet for Jana Kingston Company and Mary Ann Benson Company. Each has assets totaling $4,200,000. For the year, each company has earned the same income bef

> Anne Cleves Company reported the following amounts in the stockholders’ equity section of its December 31, 2016, balance sheet. Preferred stock, 10%, $100 par (10,000 shares authorized, 2,000 shares issued) ………………………………………………………...$200,000 Common stock,

> Bruno Corporation’s post-closing trial balance at December 31, 2017, is shown as follows. At December 31, 2017, Bruno had the following number of common and preferred shares. The dividends on preferred stock are $4 cumulative. In a

> Sinise Industries acquired two copyrights during 2017. One copyright related to a textbook that was developed internally at a cost of $9,900. This textbook is estimated to have a useful life of 3 years from September 1, 2017, the date it was published. T

> Recall from Chapter 13 that Hincapie Co. (a specialty bike-accessory manufacturer) is expecting growth in sales of some products targeted to the low-price market. Hincapie is contemplating a preferred stock issue to help finance this expansion in operati

> LVT is an international manufacturer of fragrances for women. Management at LVT is considering expanding the product line to men’s fragrances. From the best estimates of the marketing and production managers, annual sales (all for cash) for this new line

> Fox Valley Healthcare Inc. is a not-for-profit organization that operates eight nursing homes and 10 assisted-living facilities. The company has grown considerably over the last three years and expects to continue to expand in the years ahead, particular

> Argone division of Gemini Corporation is located in the United States. Its effective income tax rate is 20%. Another division of Gemini, Calcia, is located in Canada, where the income tax rate is 38%. Calcia manufactures, among other things, an intermedi

> The Ottawa Valley Instrument Company (OVIC) consists of the semiconductor division and the process-control division, each of which operates as an independent profit centre. The semiconductor division employs craftsmen who produce two different electronic

> Assume that Pat Borges, CEO of Crango, has mandated a transfer price equal to 200% of full cost. Now she decides to decentralize some management decisions and sends around a memo that states: “Effective immediately, each division of Crango is free to mak

> Crango Products is a cranberry cooperative that operates two divisions: a harvesting division and a processing division. Currently, all of Harvesting’s output is converted into cranberry juice by the processing division, and the juice i

> As a way to incent competition between divisions, the president of Industrial Products told the division managers that a quarterly bonus would be paid only to the most profitable division. However, absolute division operating income as conventionally com

> Light Seating Canada produces recliners, the device inside car seats that allows the seats to recline to a position comfortable to the driver but prevents the seat from trapping the driver in the case of a front crash. The company has always been associa

> Coventry Inc. is a diversified multidivisional corporation. One of its business units manufactures and sells industrial pumps. Coventry’s corporate management gives Industrial Pumps management considerable operating and investment autonomy in running the

> Corners Ltd. owns and manages three convenience stores. The following information has been collected for the year 2015: Required: 1. Compute the ROI for each store, where investment is measured at (a) historical cost and (b) current cost. 2. How would

> Transfer pricing is confined to profit centres.” Do you agree? Why?

> The following forecast variable costing income statement was prepared for Electric Machines Ltd. for the year ending April 2015: Sales ……………………………………..$100,000,000 Variable costs …………………………….45,000,000 Contribution margin ……………………55,000,000 Fixed costs

> Leader Automotive Canada is a Tier 1 supplier in the automotive industry (direct supplier to car assemblies), an industry that is considered the most competitive in the manufacturing sector. A couple of years ago the CEO decided to revise the bonus plan

> Mineral Waters Ltd. operates three divisions that process and bottle sparkling mineral water. The historical-cost accounting system reports the following data for 2015: Mineral Waters estimates the useful life of each plant to be 12 years with a zero t

> When the Smith & Bain Company formed three divisions a year ago, the president told the division managers that an annual bonus would be paid to the most profitable division. However, absolute division operating income as conventionally computed would

> United Forest Products (UFP) is a large timber and wood processing plant. UFP’s performance-evaluation system pays its managers substantial bonuses if the company achieves annual budgeted profit numbers. In the last quarter of 2015, Amy Kimbell, UFP’s co

> Hamilton Semiconductors manufactures specialized chips that sell for $20 each. Hamilton’s manufacturing costs consist of variable cost of $2 per chip and fixed costs of $9,000,000. Hamilton also incurs $400,000 in fixed marketing costs each year. Hamilto

> Community Credit Union (CCU) recently introduced a new bonus plan for its business unit executives. The company believes that current profitability and customer satisfaction levels are equally important to the bank’s long-term success.

> Murdoch Turner seeks your advice on revising the existing bonus plan for division managers of Green News Group. Assume division managers do not like bearing risk. Turner is considering three ideas: ■ Make each division manager’s compensation depend on di

> Green News Group has two major divisions: Print and Internet. Summary financial data (in millions) for 2014 and 2015 are as follows: he two division managers’ annual bonuses are based on division ROI (defined as operating income divid

> Italian Sausages Inc. is still a family-owned company located in Maple, Ontario. It has experienced significant growth in the last 10 years, and nowadays it employs more than 100 persons in production-related activities and another 20 persons in support

> Under the general transfer-pricing guideline, the minimum transfer price will vary depending on whether or not the supplying division has idle capacity.” Do you agree? Explain.

> Mark’s division has been judged on the basis of its profit and return on investment. Top management has been working to gain effective results from a policy of decentralizing responsibility for all decisions except those relating to overall company polic

> Blue Ribbon Fisheries is a fishing company located on the Canadian Pacific coast. It has three divisions: 1. Harvesting—operates a fleet of 20 trawling vessels. 2. Processing—processes the raw fish into fillets. 3. Marketing—packages fillets in two-kilog

> Whengon Manufacturing makes electronic hearing aids. Department A manufactures 10,000 units of part HR-7 and Department B uses this part to make the finished product. HR-7 is a specific part for a patented product that cannot be purchased or sold outside

> The management of Kleinburg Industrial Bakery is analyzing two competing investment projects and they must decide which one can be done immediately and which one can be postponed for at least a year. The details of each proposed investment are shown on t

> LudmillaQuagg owns a fitness centre and is thinking of replacing the old Fit-O-Matic machine with a brand new Flab-Buster 3000. The old FitO-Matic has a historical cost of $50,000 and accumulated depreciation of $46,000, but has a trade-in value of $5,00

> Met-All Manufacturing manufactures over 20,000 different products made from metal, including building materials, tools, and furniture parts. The manager of the Furniture Parts division has proposed that his division expand into bicycle parts as well. The

> Nate Stately, a manager of the Plate division for the Great Slate Manufacturing Company, has the opportunity to expand the division by investing in additional machinery costing $320,000. He would depreciate the equipment using the straight-line method, a

> You have the opportunity to expand your business b y purchasing new equipment for $189,000. You expect to incur fixed costs of $96,000 per year to use this new equipment, and you expect to incur variable costs in the amount of approximately 10% of annual

> Christen Granite sells granite counter tops to the construction industry. Christen Granite has three customers: Homebuilders, a small construction company that builds private luxury homes; Kitchen Constructors, a company that designs and builds kitchens

> Refer to Exercise 21-28. Required: 1. Suppose the manager of Division A has the option of (a) cutting the external price to $195, with the certainty that sales will rise to 1,000 units or (b) maintaining the external price of $200 for the 800 units and

> Give two reasons why a dual-price approach to transfer pricing is not widely used.

> Europa Inc., has two divisions, A and B, which manufacture expensive bicycles. Division A produces the bicycle frame, and Division B assembles the rest of the bicycle onto the frame. There is a market for both the subassembly and the final product. Each

> Clover Inc. manufactures and sells television sets. Its assembly division (AD) buys television screens from the screen division (SD) and assembles the TV sets. The SD, which is operating at capacity, incurs an incremental manufacturing cost of $80 per sc

> Refer to Exercise 21-25. Assume that Division A can sell the 2,000 units to other customers at $155 per unit, with variable marketing cost of $5 per unit. Required: 1. Determine whether Allison-Chambers will benefit if Division C purchases the 2,000 uni

> Ajax Corporation has two divisions. The mining division makes toldine, which is then transferred to the metals division. The toldine is further processed by the metals division and sold to customers at a price of $150 per unit. The mining division is cur

> British Columbia Lumber has a raw lumber division and a finished lumber division. The variable costs are: ■ Raw lumber division: $100 per 100 board feet of raw lumber. ■ Finished lumber division: $125 per 100 board feet of finished lumber. Assume that no

> Zzwuig Multinational Inc. has divisions in Canada, Germany, and New Zealand. The Canadian division is the oldest and most established of the three, and has a cost of capital of 6%. The German division was started three years ago when the exchange rate fo

> Konekopf Corporation has a division in Canada and another in France. The investment in the French assets was made when the exchange rate was $1.20 per euro. The average exchange rate for the year was $1.30 per euro. The exchange rate at the end of the fi

> Peach Computer Corporation is the largest personal computer company in the world. The CEO of Peach is retiring, and the board of directors is considering external candidates to fill the position. The board’s top two choices are CEOs Pet

> Brasskey (BK) Company makes doorbells. It has a weighted-average cost of capital of 8%, and total assets of $5,690,000. BK has current liabilities of $700,000. Its operating income for the year was $649,000. BK does not have to pay any income taxes. One

> Bill Watts, president of Western Publications, accepts a capital-budgeting project advocated by Division X. This is the division in which the president spent his first 10 years with the company. On the same day, the president rejects a capital-budgeting

> The Dexter Division of AMCO sells car batteries. AMCO’s corporate management gives Dexter management considerable operating and investment autonomy in running the division. AMCO is considering how it should compensate Jim Marks, the general manager of th

> Lada Manufacturing makes fashion products and competes on the basis of quality and leading-edge designs. The company has $3,000,000 invested in assets in its clothing manufacturing division. After-tax operating income from sales of clothing this year is

> The Grandlund Corporation manufactures similar products in Canada and Norway. The Canadian and Norwegian operations are organized as decentralized divisions. The following information is available for 2016; ROI is calculated as operating income divided b

> Bailey Corporation recently announced a bonus plan to be awarded to the manager of the most profitable division. The three division managers are to choose whether ROI or RI will be used to measure profitability. In addition, they must decide whether inve

> Performance Auto Company operates a New Car Division (that sells high-performance sports cars) and a Performance Parts Division (that sells performance improvement parts for family cars). Some division financial measures for 2015 are as follows: Requir

> YardScapes Corporation manufactures furniture in several divisions, including the Patio Furniture division. The manager of the Patio Furniture division plans to retire in two years. The manager receives a bonus based on the division’s ROI, which is curre

> Summit Equipment specializes in the manufacture of medical equipment, a field that has become increasingly competitive. Approximately two years ago, Ben Harrington, president of Summit, decided to revise the bonus plan (based, at the time, entirely on op

> Ohms Motor Company makes electric cars and has only two products, the Simplegreen and the Superiorgreen. To produce the Simplegreen, Ohms Motor employed assets of $13,500,000 at the beginning of the period, and $13,400,000 of assets at the end of the per

> The Outdoor Sports Company produces a wide variety of outdoor sports equipment. Its newest division, Golf Technology, manufactures and sells a single product: AccuDriver, a golf club that uses global positioning satellite technology to improve the accura

> Learning World Inc. has two divisions: Test Preparation and Language Arts. Results (in millions) for the past three years are partially displayed here: Required: 1. Complete the table by filling in the blanks. 2. Use the DuPont method of profitability

> List and briefly describe the five major categories of cash flows included in capital investment projects.

> Return on investment (ROI) is often expressed as follows: Required: 1. What advantages are there in the breakdown of the computation into two separate components? 2. Fill in the following blanks: After filling in the blanks, comment on the relative p

> A number of terms are listed below: Required: Select the terms from the above list to complete the following sentences. Governance, or the management stewardship of assets management does not own, according to laws and regulations is more closely scrut

> In 2015, the Mandarin Division of Key Products Corporation generated an operating income of $3,000,000 from $20,000,000 of sales revenues and using assets worth $15,000,000. Mandarin managers are evaluated and rewarded on the basis of ROI defined as oper

> Home Appliance (HA) builds coffeemakers and battery-powered small tools. For a long time, HA held a reputation for strong, durable, and reliable appliances. This reputation began to decline, however, when increased competition forced HA to cut costs, and

> Wilcox is a familyowned company that has been making microwaves for almost 20 years. The company’s production line includes 10 models, ranging from a basic model to a deluxe stainless steel model. Most of its sales are through independe

> Francesca Freed wants a Burg-NFry franchise. The buy-in is $500,000. Burg-N-Fry headquarters tells Francesca that typical annual operating costs are $160,000 (cash) and that she can bring in “as much as” $260,000 in cash revenues per year. BurgN-Fry head

> The Allison Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit centre. Each division manager has been delegated full author

> Industrial Diamonds, Inc., based in Montreal, Quebec, has two divisions: â– South African mining division, which mines a rich diamond vein in South Africa. â– Canadian processing division, which polishes raw di amonds fo

> The Handit Company manufactures telecommunications equipment at its plant in Ottawa, Ontario. The company has marketing divisions throughout the world. A Handit marketing division in Vienna, Austria, imports 1,000 units of Product 4A36 from Canada. The f

> Quest Motors Inc. operates as a decentralized multidivision company. The tivo division of Quest Motors purchases most of its airbags from the airbag division. The airbag division’s incremental cost for manufacturing the airbags is $90 per unit. The airba

> The trouble with discounted cash flow techniques is that they ignore depreciation costs.” Do you agree? Explain.

> TECA Halifax makes kids’ bicycles. The frames division makes and paints the frames and supplies them to the assembly division where the bicycles are assembled. TECA is a successful and profitable corporation that attributes much of its success to its dec

> The Orsilo Corporation makes and sells 10,000 multisystem music players each year. Its assembly division purchases components from other divisions of Orsilo or from external suppliers and assembles the multisystem music players. In particular, the assemb

> User Friendly Computer Inc., with headquarters in Nepean, Ontario, manufactures and sells a premium desktop computer system. User Friendly has three divisions, each of which is located in a different country: a. China division—manufactu

> Fenster Corporation manufactures windows with wood and metal frames. Fenster has three departments: glass, wood, and metal. The glass department makes the window glass and sends it to either the wood or metal department, where the glass is framed. The wi

> Berry Chemicals consists of seven independent operating divisions. The operating divisions are assisted by a number of support groups, such as R&D, human resources, and environmental management. The environmental-management group consists of 20 environme

> Greystone Corporation manufactures stone tiles for kitchen counters and floors. Its strategy is to manufacture high-quality products at reasonable prices, and to rapidly deliver products following sales. Greystone sells to both hardware stores and contra

> A number of terms are listed below: Required: Select the terms from the above list to complete the following sentences. The CRA constrains global transfer-pricing choices, and provincial tax authorities constrain the interprovincial transfer-pricing ch

> Anna’s Bakery plans to purchase a new oven with an estimated useful life of four years. The estimated pretax cash flows for the oven are as shown in the table that follows, with no anticipated change in working capital. Annaâ€

> StrengthCo is considering an investment of $254,200 in special tools, with a life expectancy of four years and a residual price of $24,000. The tools would be purchased on December 31, 2016, and would enable StrengthCo to manufacture drill bits to very h

> KopiPro is considering the purchase of a photocopying machine for $5,500 on December 31, 2016. It has a useful life of five years and a zero residual disposal price. Depreciation will be applied on a straight-line basis. The cash operating savings are ex

> Describe the accrual accounting rate of return method. What are its main strengths and weaknesses?

> Microdot Inc. sells and distributes computer networking equipment; its overall margin on sales is 10%. Microdot has customers of two kinds: low and high volume. Lowvolume customers on average generate sales for $5,000 per year and the average tenure is f

> Edgeley Inc., a logistics operator located in Concord, Ontario, is considering replacing one of its tractor trailers (informally known as a 53’ truck). The truck was purchased for $64,800 two years ago, has a current book value of $45,600, and a remainin

> Windsor Hospital is a non-tax paying not for profit entity. It estimates that it can save $28,000 a year in cash operating costs for the next 10 years if it buys a special-purpose eye-testing machine at a cost of $110,000. No terminal disposal value is e

> Edilcan Inc. has been offered an automated special-purpose welder (robot) for $60,000. The machine is expected to have a useful life of eight years with a terminal disposal price of $12,000. Savings in cash operating costs are expected to be $15,000 per

> Homer Inc. plans to purchase a new rendering machine for its animation facility. The machine costs $102,500 and is expected to have a useful life of eight years, with a terminal disposal value of $22,500. Savings in cash operating costs are expected to b

> Muskoka Landscaping Ltd. is planning to buy equipment costing $25,000 to improve its services. The equipment is expected to save $8,000 in cash operating costs per year. Its estimated useful life is five years, and it will have zero terminal disposal pri

> Century Lab plans to purchase a new centrifuge machine for its Manitoba facility. The machine costs $137,500 and is expected to have a useful life of eight years, with a terminal disposal value of $37,500. Savings in cash operating costs are expected to

> Presentation Graphics prepares slides and other aids for individuals making presentations. It estimates it can save $42,000 a year in cash operating costs for the next five years if it buys a special-purpose colour-slide workstation at a cost of $90,000.

> Andrews Construction is analyzing its capital expenditure proposals for the purchase of equipment in the coming year. The capital budget is limited to $6,000,000 for the year. Lori Bart, staff analyst at Andrews, is preparing an analysis of the three pro

> New Bio Corporation is a rapidly growing biotech company that has a required rate of return of 12%. It plans to build a new facility in Mississauga, Ontario. The building will take two years to complete. The building contractor offered New Bio a choice o

> List and briefly describe each of the six parts in the capital budgeting decision process.

> Southern Cola is considering the purchase of a special-purpose bottling machine for $23,000. It is expected to have a useful life of four years with no terminal disposal value. The plant manager estimates the following savings in cash operating costs: Y

> Norberto Garcia, general manager of the Argentinean subsidiary of Innovation Inc., is considering the purchase of new industrial equipment to improve efficiency at its Cordoba plant. The equipment has an estimated useful life of five years. The estimated

> Panayiotis, the owner and manager of Micos Ltd., is evaluating the acquisition of new equipment needed to attend a new line of business. He has two alternatives: either buy two small machines or one large and more automatic machine: Required: 1. Determ

> Lethbridge Company runs hardware stores in Alberta. Lethbridge’s management estimates that if it invests $160,000 in a new computer system, it can save $60,000 in annual cash operating costs. The system has an expected useful life of five years and no te

> A number of terms are listed below: Select the terms from the above list to complete the following sentences. The goal of ________________ is to provide capacity in a planned and orderly manner that will match the predicted demand growth of the company